Mad Hedge Biotech and Healthcare Letter

July 1, 2025

Fiat Lux

Featured Trade:

(BOTTOM OF THE NINTH FOR THIS BIOPHARMA)

(BMY), (BNTX)

Mad Hedge Biotech and Healthcare Letter

July 1, 2025

Fiat Lux

Featured Trade:

(BOTTOM OF THE NINTH FOR THIS BIOPHARMA)

(BMY), (BNTX)

I was at a Yankees game once, bottom of the ninth, crowd roaring, and the pitcher tosses what looks like a meatball right down Broadway.

Everyone around me starts groaning. They’re sure it’s a trick pitch, a slider in disguise. But the batter swings anyway and sends it into the cheap seats.

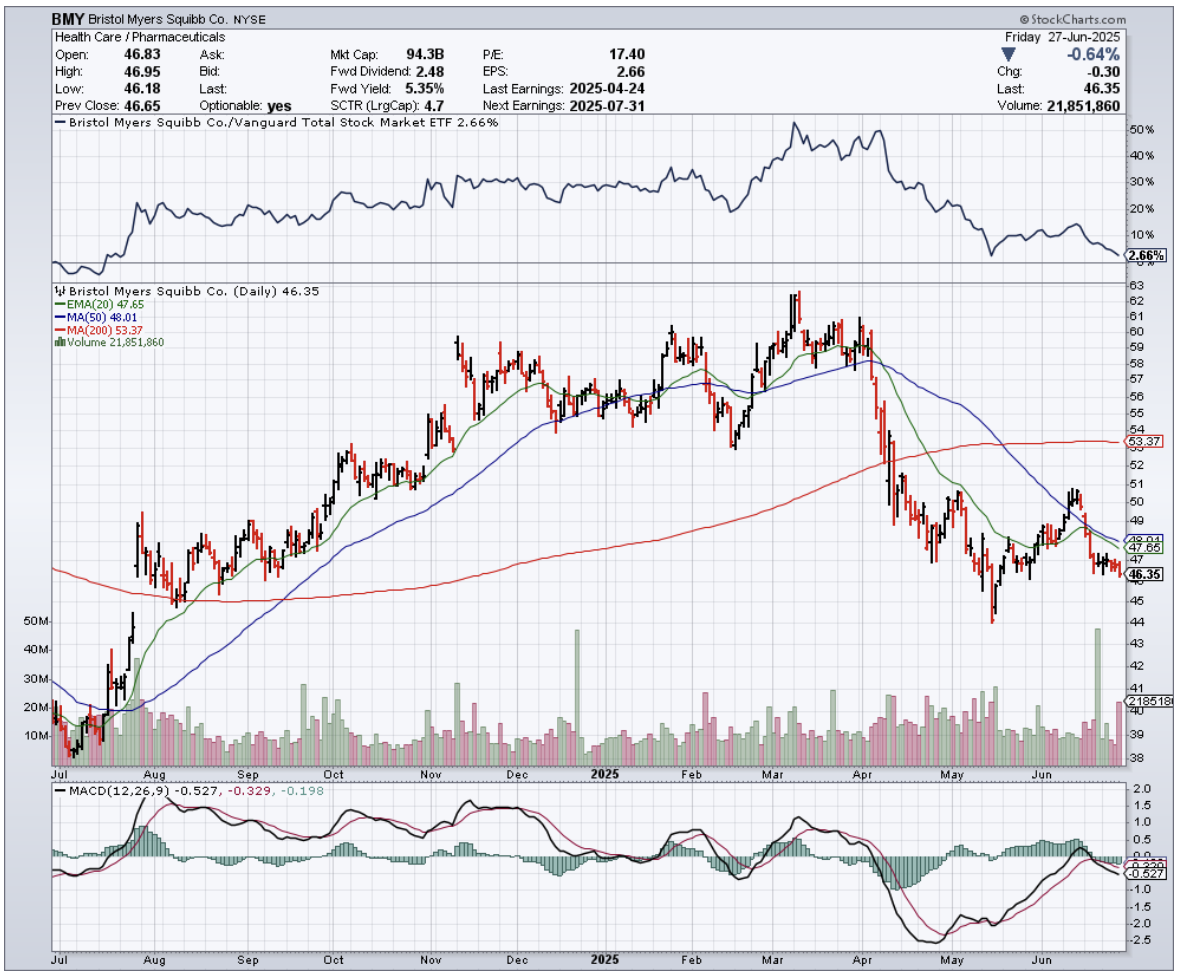

That, my friends, is Bristol-Myers Squibb (BMY) right now.

And if there’s one thing I’ve learned from decades in the game, it’s that sometimes the pitch you think you should avoid is the one that changes everything.

Let’s get serious. BMY is slogging through a growth transition with more bumps than the FDR Drive.

Their cash cows are aging out. Blockbusters like Eliquis and Opdivo are facing loss of exclusivity through 2028. The generic wolves are circling, and that revenue cliff is no mirage.

But what separates BMY from a slow-motion train wreck is simple: they’re not standing still.

This is precisely where BioNTech (BNTX) enters the picture. BMY just dropped $1.5 billion upfront, with potential payments totaling $11 billion, to co-develop BNT327, a bispecific antibody targeting PD-L1 and VEGF-A.

Translation: a moonshot aimed squarely at the $50 billion immuno-oncology market.

And unlike many pharma deals where one side gets dinner and the other a napkin, this one’s 50/50 on development and commercialization.

This isn’t charity. It’s strategic triage.

Management knows it must replace legacy sales with high-octane new therapies. By 2028, they plan to shift 30% to 40% of current IV business to Opdivo Qvantig.

That’s more than just a pivot for BMY. That’s a full-blown reinvention, paired with $2 billion in cost savings and accelerated ramp-up in the growth portfolio.

Now, don’t misunderstand the backdrop here: it’s brutal.

Legacy headwinds aren’t just nibbling; they’re gnawing. The company’s Q1 results showed ongoing structural drag that’s unlikely to reverse before 2027.

Yet rather than simply reacting defensively, BMY has been aggressively making offensive plays. They’ve signaled intent to grow their business development pipeline aggressively.

The BioNTech partnership isn’t a one-off; it’s part of a wider effort to build out a durable oncology pipeline and diversify future revenue sources.

Despite these strategic moves, the market continues to yawn.

Valuation has slumped to 6.9x earnings, marking a 35% discount to healthcare peers and a level last seen during peak COVID panic.

Meanwhile, free cash flow is still flowing like boxed wine at a barbecue: $15 billion in 2025, $13.1 billion projected in 2026. And as for that juicy 5% dividend? Secure as Fort Knox.

If you’re the kind of investor who enjoys being paid to wait, this is your front-row seat.

Still, experts continue to tag them as “dead money.” Analysts have cautiously lifted near-term estimates, but consensus remains that a meaningful re-rating won’t happen before 2027. There’s understandable skepticism here.

RFK Jr. at HHS has injected fresh uncertainty into regulatory policy, and ongoing debates about Medicare price negotiation and pharma tariffs continue to weigh on sentiment.

However, beneath all this noise, BMY is methodically executing a turnaround strategy.

Management has outlined a clear path forward: pivoting its IV portfolio to more durable therapies like Opdivo Qvantig, aggressively investing in its pipeline through deals like the BioNTech collaboration, and maintaining robust free cash flow to support dividends and R&D.

The BioNTech deal represents far more than just a way to pacify fidgety investors. It’s a tactical entry into bispecific antibodies, a class of therapies gaining serious traction for difficult-to-treat cancers.

If successful, it could provide a critical platform for long-term growth and validate BMY’s evolving innovation model. These coordinated steps suggest BMY is not managing decline, but actually engineering a comeback.

You don’t get these setups often: deep value, solid income, and a credible shot at long-term upside.

The company that once looked like it was managing decline is now throwing heaters. The market may not be ready to believe it yet, but those who buy into the story now might just be the ones bragging about it in a few years.

Remember, the best curveballs are the ones the batter almost doesn’t swing at — and then drives out of the park. Swing for the fences, folks. This one could be going, going…

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

July 1, 2025

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

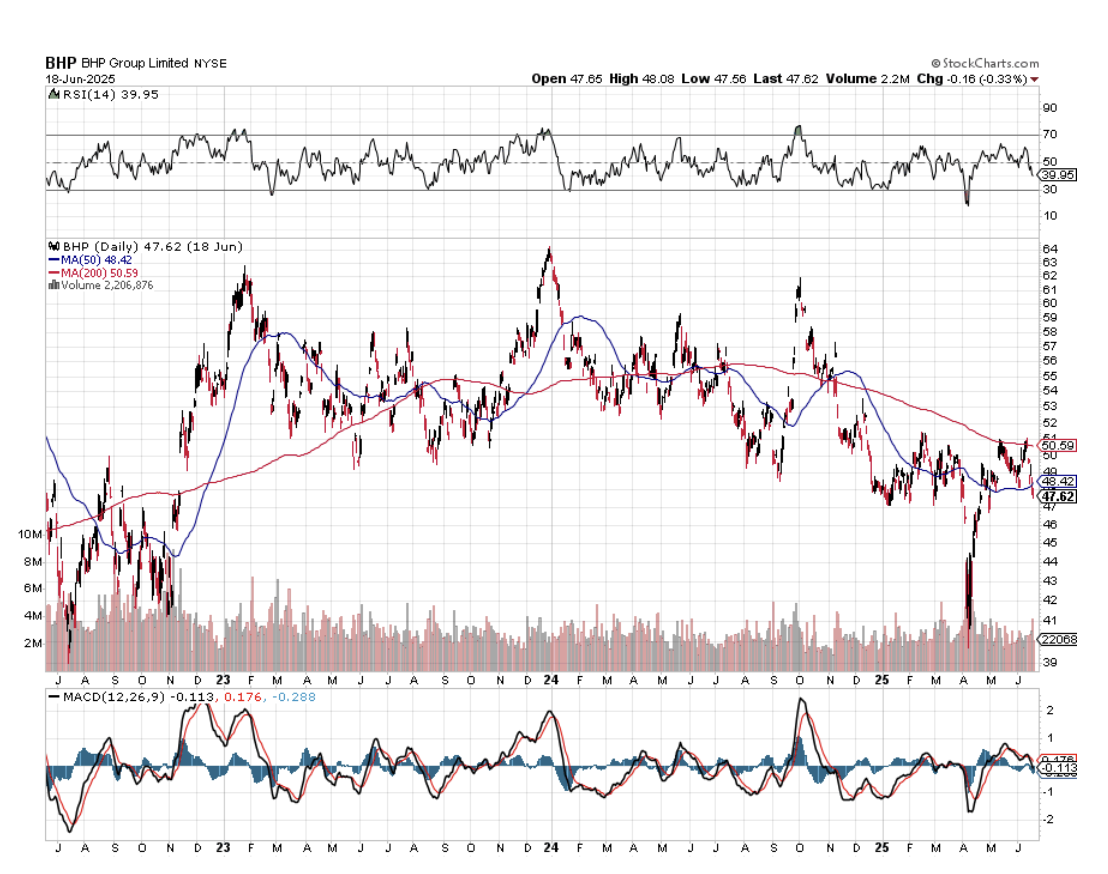

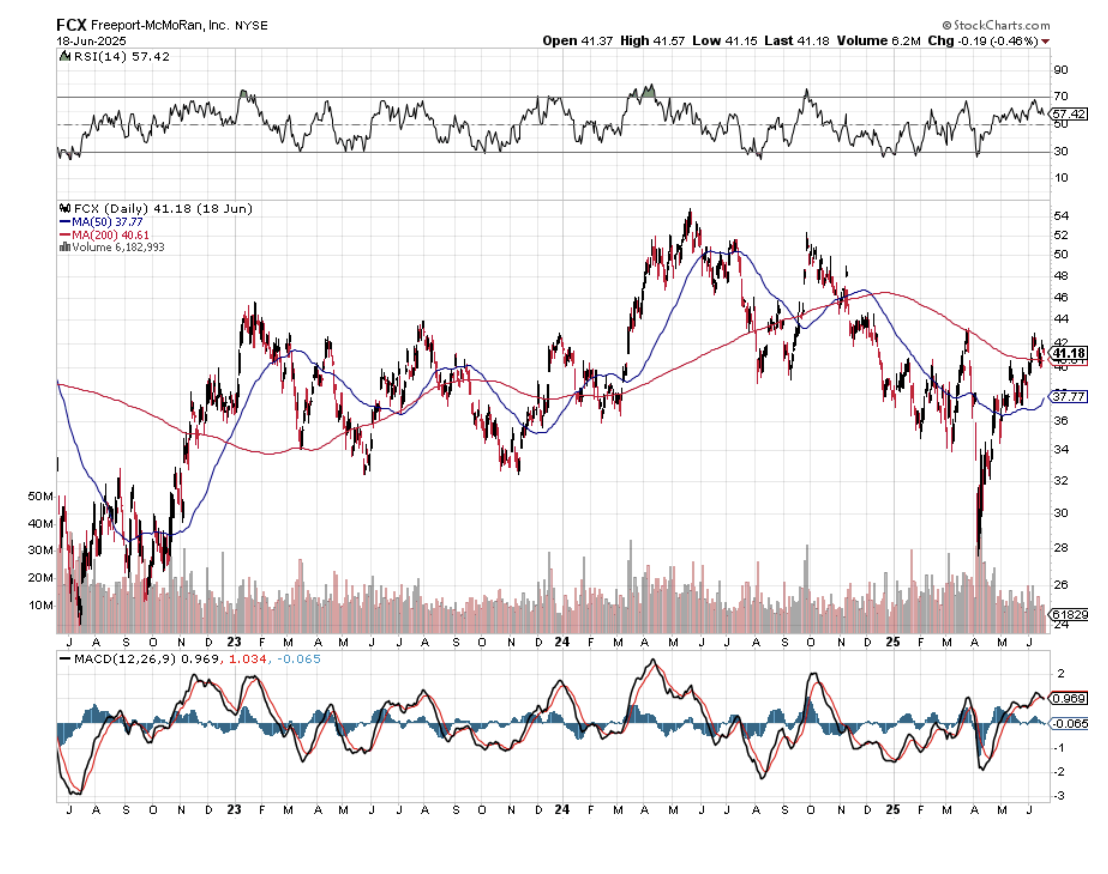

When I closed out my position in Freeport McMoran (FCX) near its max profit earlier this year, I received a hurried email from a reader asking if he should still keep the stock. I replied very quickly:

“Hell, yes!”

When I toured Australia a couple of years ago, I couldn’t help but notice a surprising number of fresh-faced young people driving luxury Ferraris, Lamborghinis, and Porsches.

I remarked to my Aussie friend that there must be a lot of indulgent parents in The Lucky Country these days. “It’s not the parents who are buying these cars,” he remarked, “It’s the kids.”

He went on to explain that the mining boom had driven wages for skilled labor to spectacular levels. Workers in their early twenties could earn as much as $200,000 a year, with generous benefits.

The big resource companies flew them by private jet a thousand miles to remote locations where they toiled at four-week on, four-week off schedules.

This was creating social problems, as it is tough for parents to manage offspring who make far more than they do.

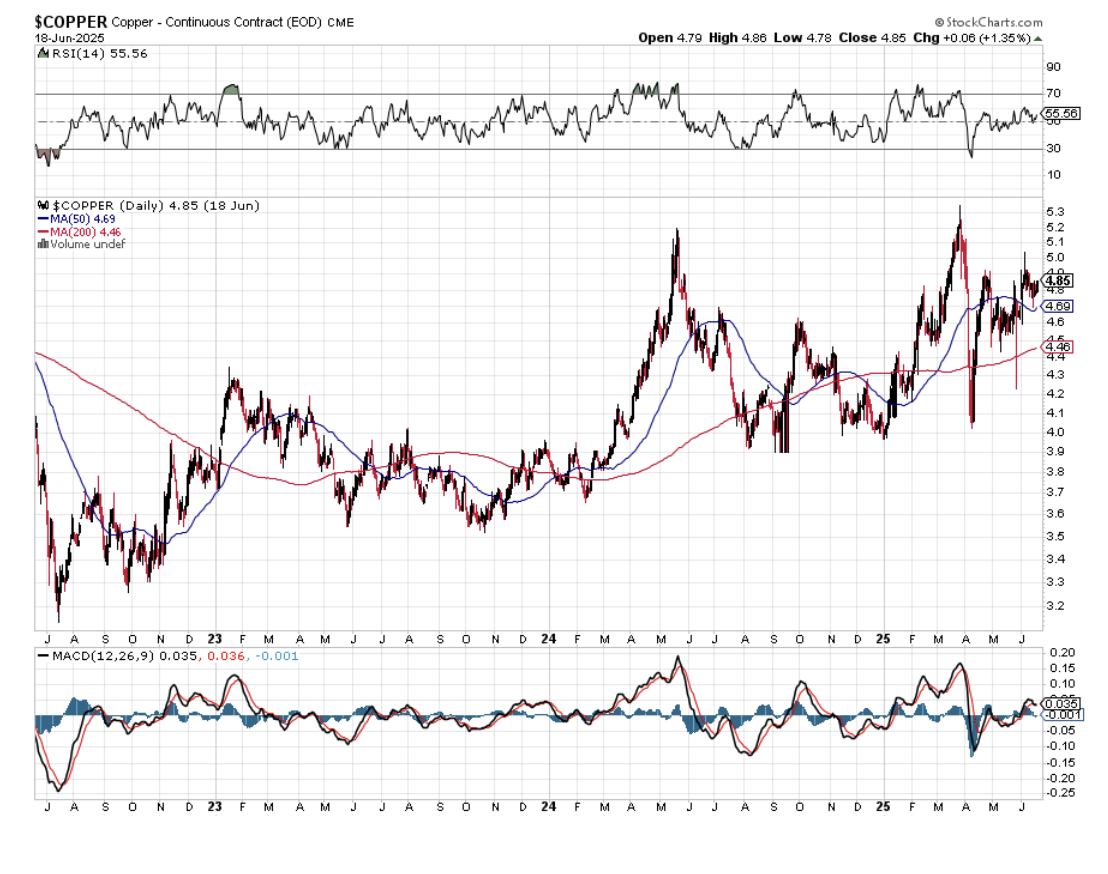

The Great Commodity Boom has started, and in fact, we are already years into a prolonged super cycle.

China, the world’s largest consumer of commodities, is currently stimulating its economy on multiple fronts, including generous corporate tax breaks and relaxed reserve requirements. Get a trigger like the impending settlement of its trade war with the US, and it will be off to the races once more for the entire sector.

The last bear market in commodities was certainly punishing. From the 2011 peaks, copper (COPX) shed 65%, gold (GLD) gave back 47%, and iron ore was cut by 78%. One research house estimated that some $150 billion in resource projects in Australia were suspended or cancelled.

Budgeted capital spending during 2012-2015 was slashed by a blood-curdling 30%. Contract negotiations for price breaks demanded by end consumers broke out like a bad case of chicken pox.

The shellacking was reflected in the major producer shares, like BHP Billiton (BHP), Freeport McMoran (FCX), and Rio Tinto (RIO), with prices down by half or more. Write-downs of asset values became epidemic at many of these firms.

The selloff was especially punishing for the gold miners, with lead firm Barrack Gold (GOLD) seeing its stock down by nearly 80% at one point, lower than the darkest days of the 2008-9 stock market crash.

You also saw the bloodshed in the currencies of commodity-producing countries. The Australian dollar led the retreat, falling 30%. The South African Rand has also taken it on the nose, off 30%. In Canada, the Loonie got cooked.

The impact of China cannot be underestimated. In 2012, it consumed 11.7% of the planet’s oil, 40% of its copper, 46% of its iron ore, 46% of its aluminum, and 50% of its coal. It is much smaller than that today, with its annual growth rate dropping by more than half, from 13.7% to 2.3% in 2020.

What happens to commodity prices if China recovers the heady growth rates of yore? It boggles the mind. If China doesn’t step up, then India certainly will.

The rise of emerging market standards of living will also provide a boost to hard asset prices. As China goes, so do its satellite trading partners, who rely on the Middle Kingdom as their largest customer. Many are also major commodity exporters themselves, like Chile (ECH), Brazil (EWZ), and Indonesia (IDX), are looking to come back big time.

As a result, Western hedge funds will soon be moving money out of paper assets, like stocks and bonds, into hard ones, such as gold, silver (SIL), palladium (PALL), platinum (PPLT), and copper.

A massive US stock market rally has sent managers in search of any investment that can’t be created with a printing press. Look at the best-performing sectors this year, and they are dominated by the commodity space.

The bulls may be right for as long as a decade thanks to the cruel arithmetic of the commodities cycle. These are your classic textbook inelastic markets.

Mines often take 10-15 years to progress from conception to production. Deposits need to be mapped, plans drafted, permits obtained, infrastructure built, capital raised, and bribes paid in certain countries. By the time they come online, prices have peaked, drowning investors in red ink.

So a 1% rise in demand can trigger a price rise of 50% or more. There are not a lot of substitutes for iron ore. Hedge funds then throw gasoline on the fire with excess leverage and high-frequency trading. That gives us higher highs, to be followed by lower lows.

I am old enough to have lived through a couple of these cycles now, so it is all old news for me. The previous bull legs of super cycles ran from 1870-1913 and 1945-1973. The current one started for the whole range of commodities in 2016. Before that, it was down for seven years.

While the present one is short in terms of years, no one can deny how business cycles will be greatly accelerated by the end of the pandemic.

Some new factors are weighing on miners that didn’t plague them in the past. Reregulation of the US banking system has forced several large players, like JP Morgan (JPM) and Goldman Sachs (GS), to pull out of the industry completely. That impairs trading liquidity and widens spreads— developments that can only accelerate upside price moves.

The prospect of falling US interest rates is also attracting capital. That reduces the opportunity cost of staying in raw metals, which pay neither interest nor dividends.

The future is bright for the resource industry. While the gains in Chinese demand are smaller than they have been in the past, they are off a much larger base. In 20 years, Chinese GDP has soared from $1 trillion to $14.5 trillion.

Some 20 million people a year are still moving from the countryside to the coastal cities in search of a better standard of living and improved prospects for their children.

That is the good news. The bad news is that it looks like the headaches of Australian parents of juvenile high earners may persist for a lot longer than they wish.

Buy all commodities on dips for the next several years.