Crypto and Terraform Labs co-founder Do Kwon is no longer on the run.

Yes, that’s right – he’s a convict.

The Interpol red list that once alerted 195 countries to his status as a wanted fugitive has been retired, replaced by a federal prison number. We now know that his desperate transfer of 33,131 Bitcoins right after being added to that list was the final act of a man who knew the walls were closing in.

Kwon was the golden boy for stablecoins for quite some time as the native South Korean’s brash attitude led him to billions in wealth.

His “fake it ‘til you make it” attitude got him into deep water, and the quickly escalating investigations have now concluded with a definitive thud.

Why?

His brainchild, Terra’s UST stablecoin, lost its parity to the dollar in May 2022 in a $70 billion collapse, and today is nothing more than a digital tombstone.

Kwon and Terraform Labs fled South Korea for Singapore ahead of Terra’s meltdown, and then he fled Singapore, sparking a global manhunt that ended in Montenegro.

South Korean authorities finally got their answers regarding the violations of capital markets law that resulted in a slew of local suicides by investors who lost everything.

Investigators also confirmed what many suspected: his company misled investors in labeling UST as a stablecoin.

The courts have ruled that his stablecoin achieved the definition of a Ponzi scheme.

It feels like a lifetime ago when Terraform Labs successfully rallied an audience of fans that called themselves the “Lunatics,” praising Kwon as the project’s outspoken hero, as the price of its LUNA token rallied.

Kwon’s unique case set off US regulators with the intent of regulating stablecoins more rigidly, a goal that was realized with the passage of the GENIUS Act last year.

The South Korean sullied the stablecoin industry, and while the manhunt is over, the reputational stain remains.

U.S. lawmakers successfully passed the bill that introduced a ban on UST-like algorithmic stablecoins, safeguarding other decentralized dollar alternatives like MakerDAO’s DAI by forcing them to adhere to strict backing requirements.

Cryptocurrencies have been littered with non-stop streaming of negative headlines over the last few years.

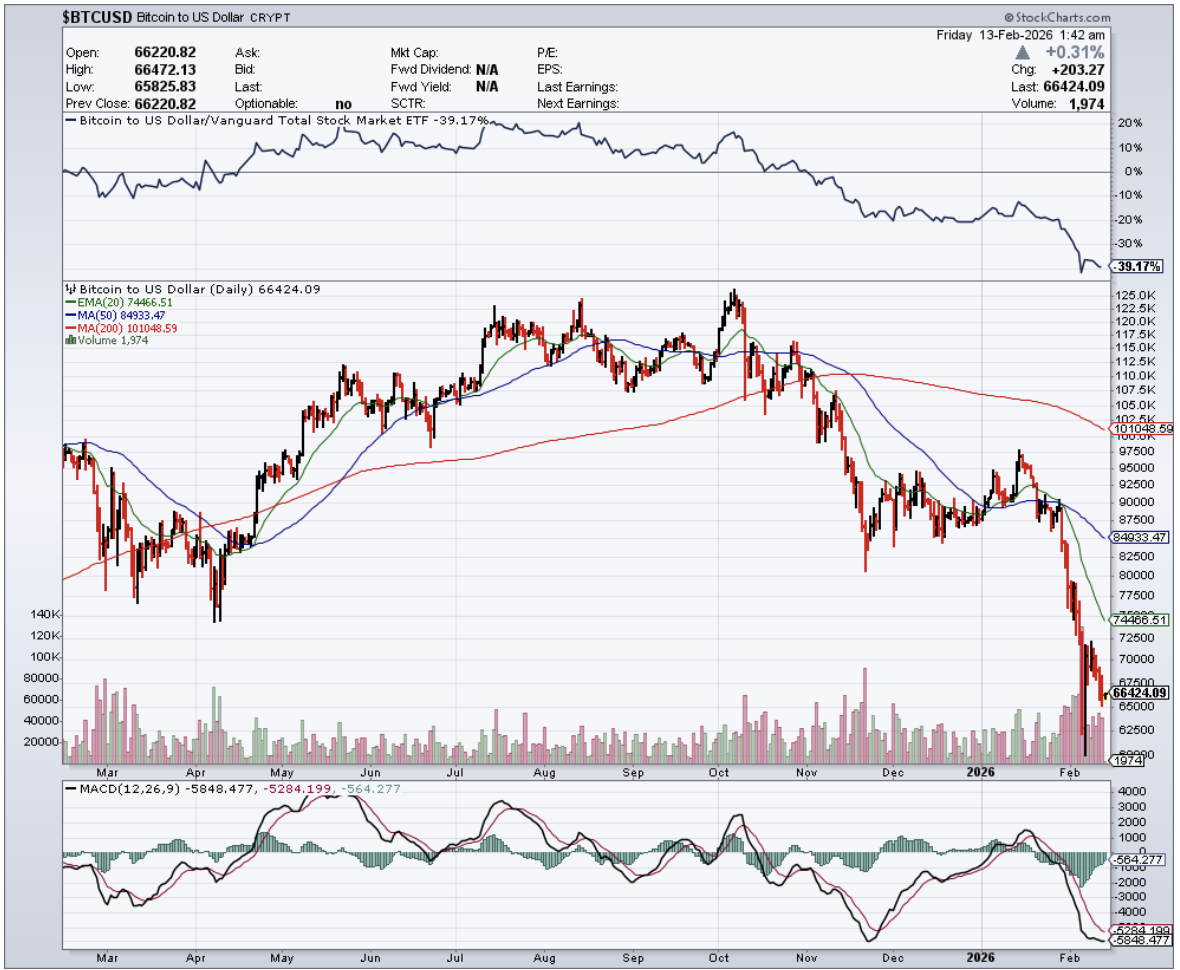

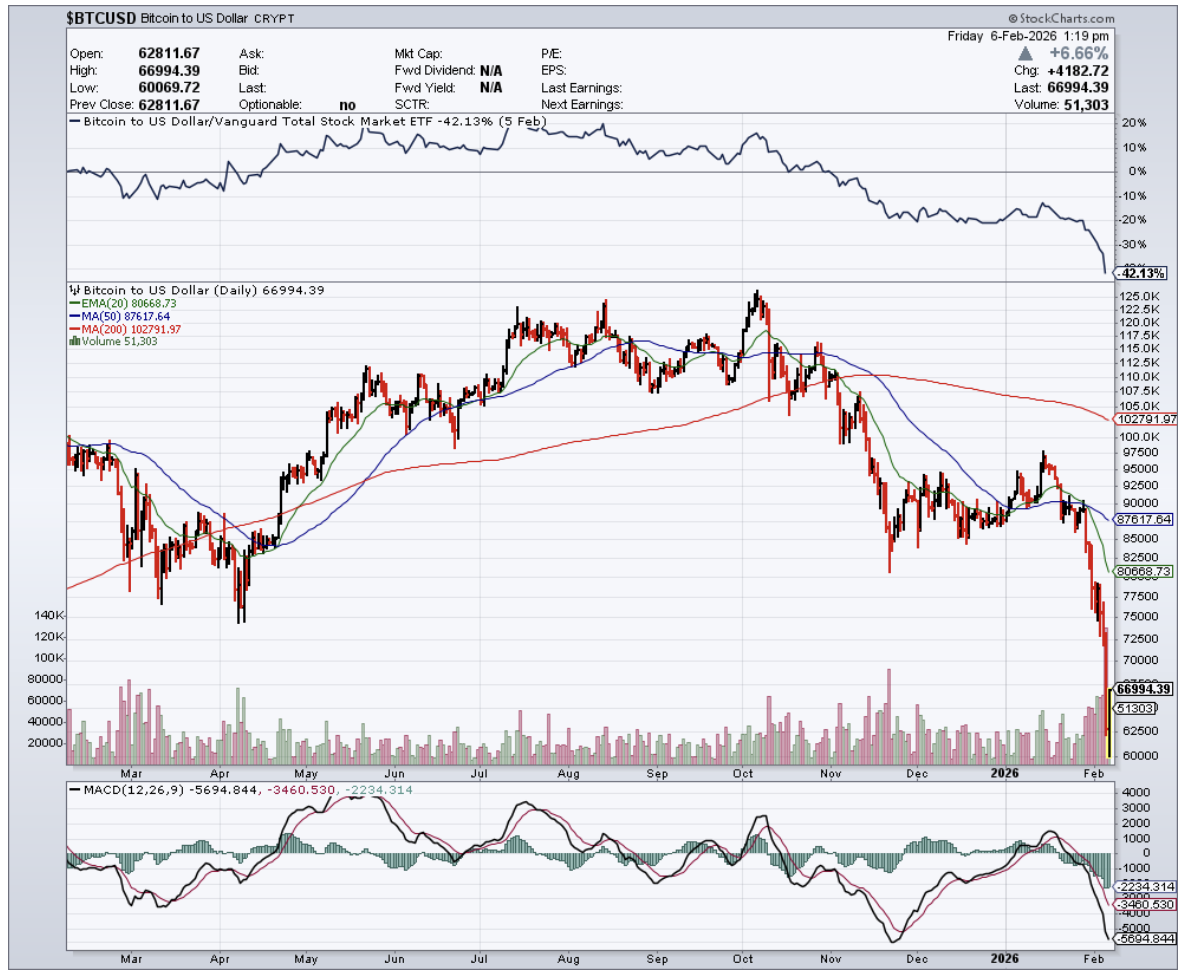

Bitcoin reaching $65,000 back then wasn’t in fact a celebration, but the calm before the storm, before a myriad of structural problems were revealed as the price of Bitcoin collapsed.

Kwon's incarceration has stopped his attempt at fixing LUNA, and the price levels remain a fraction of what they were before the collapse.

The conclusion of this international police case has heaped more fuel on the fire for incremental investors, signaling them to stay away from speculative cryptocurrencies, and rightly so.

Kwon is now serving a 15-year sentence, though legal experts believe he may still face additional time in his native homeland of South Korea.

Financial fraud and running a Ponzi scheme are serious matters in South Korea, which is infamous as a place where Korean oligarchs regularly flout the law, but Kwon was not spared.

Delaying the inevitable stirred up even more unrest for crypto, but at least one of its big-time CEOs can no longer evade the law.

The longer he hid internationally, the longer the damage to the reputation of crypto lasted.

The problem I have is that even with justice served, the lack of cash flow dispensing from these assets keeps them in a gray area of whether they are sustainable or not.

Even more worrisome, the strict regulations born from Kwon’s actions have wiped out the wild-west infrastructure that once fueled the industry's growth.

It caused manhunts for crypto CEOs and the bankruptcy of the masses.

These events remain highly bearish for the cryptocurrency industry's legacy, and I advise readers to continue heading for higher water.