Mad Hedge Biotech & Healthcare Letter

November 7, 2019

Fiat Lux

Featured Trade:

(BUY NOVARTIS ON THE DATA SCANDAL DIP),

(NVS)

Mad Hedge Biotech & Healthcare Letter

November 7, 2019

Fiat Lux

Featured Trade:

(BUY NOVARTIS ON THE DATA SCANDAL DIP),

(NVS)

Amid the public outcry over how Novartis A.G. (NVS) dealt with the data manipulation issue involving its $2.1 million gene therapy Zolgensma, the stock has been doing quite fine. In fact, the Food and Drug Administration (FDA) has reassured everyone that the drug is still a safe choice for spinal muscular atrophy.

Although the agency threatened to impose “civil or criminal penalties,” it also reiterated that the FDA “remains confident that Zolgensma should remain on the market.” This is probably because the data manipulation affected only a minimal part of the information submitted for Zolgensma’s approval. It had no connection at all to more pressing matters like human safety and efficacy tests.

Rather, it pertains to the mouse studies performed during the early stages of drug testing. The FDA explained that Novartis’ data “continues to provide compelling evidence supporting an overall favorable benefit-risk profile” for the drug.

Nonetheless, Novartis didn’t exactly go away scot-free as an ex-FDA commissioner said that “the key issue of trust in the face of overwhelming complexity is driving the stern warning and possible consequences.”

In terms of the effects of the issue on Zolgensma’s sales, it’s also unlikely that it will greatly affect Novartis as a whole. The treatment is currently estimated to bring $200 million in profits this quarter and possibly $300 million in the succeeding period. Assuming that the FDA decides to impose a more restrictive punishment, Zolgensma’s sales contribute a tiny drop in the bucket of the company’s $11.7 billion estimated quarterly earnings.

This is why despite all the hullabaloo, people who have no idea about the issue wouldn’t even catch a whiff of it from looking at the ticker. Reviewing Novartis’ performance during the height of the issue, its shares went down only 0.8% amid a general Biotech and Life Sciences market slowdown.

So, why isn’t Novartis getting penalized for this data manipulation scandal? Because at the moment, the issue -- no matter how humiliating -- seems highly unlikely to affect the stock’s bottom line.

In the second quarter of 2019, Novartis beat earnings and sales estimates with the company even raising its guidance for this year. It recorded core earnings of $1.34 per share, up from the $1.18 reported in 2018. The company’s profits increased to hit $11.8 billion as well. Compared to the rest of the industry, which suffered a 1.1% decline, Novartis recorded a 5.2% gain so far in 2019.

Now, let’s take a look at the performance so far of its two major growth drivers: Innovative Medicines (pharmaceuticals) and Sandoz (generics).

The pharma segment grew by 10% this year and reported sales worth $9.3 billion, indicating a 9% increase year over year. Among the notable performers in this division is psoriasis treatment Cosentyx, which has been gaining traction especially in the United States as shown by the 25% increase in its sales to hit $858 million.

A global uptake, particularly in the hospital and ambulatory demand for chronic heart failure medication Entresto, also boosted its sales by 81% to rake in $421 million.

Novartis’ oncology unit also showed an increase of 9% courtesy of acute lymphoblastic leukemia drug Kymriah, severe aplastic anemia medication Promacta, and breast cancer treatment Kisqali.

Even its Lutathera, the radioactive targeted therapy for neuroendocrine tumor that was a recent addition from the acquisition of Advanced Accelerator Applications (AAA), contributed to this solid performance. AAA sales reached $171 million with $109 million coming from Lutathera profits alone. Meanwhile, Kisqali’s sales grew 94% and Promacta profits grew 23%.

As for the Sandoz segment, the division recorded $4.8 billion in sales, up by 1%. Its biopharmaceuticals profits increased 14% mainly thanks to the notable double-digit growth of cancer and rheumatoid arthritis treatment Rixathon (a biosimilar of Roche Holding AG’s (RHHBY) Rituxan), plaque psoriasis medication Erelzi (a biosimilar of Amgen’s (AMGN) Enbrel), and rheumatoid arthritis drug Hyrimoz (a biosimilar of AbbVie’s Humira).

The strong performance during the second quarter pushed Novartis to boost its sales and earnings forecasts for 2019 to reflect mid-to-high single-digit increase. The new wave of drug approvals the company has gained provided added confidence to its performance in subsequent months.

Aside from expanding its rare genetic disorder portfolio with Zolgensma and oncology division with advanced breast cancer drug Piqray, Novartis is also looking to bring more depth to its ophthalmic pharmaceutical department with the acquisition of dry eye treatment Xiidra.

Given its current performance and the promising drug pipeline it has for 2019, Novartis is anticipated to become one of the top-performing biopharmas in the market today.

Buy (NVS) on the next dip.

Mad Hedge Biotech & Healthcare Letter

November 5, 2019

Fiat Lux

Featured Trade:

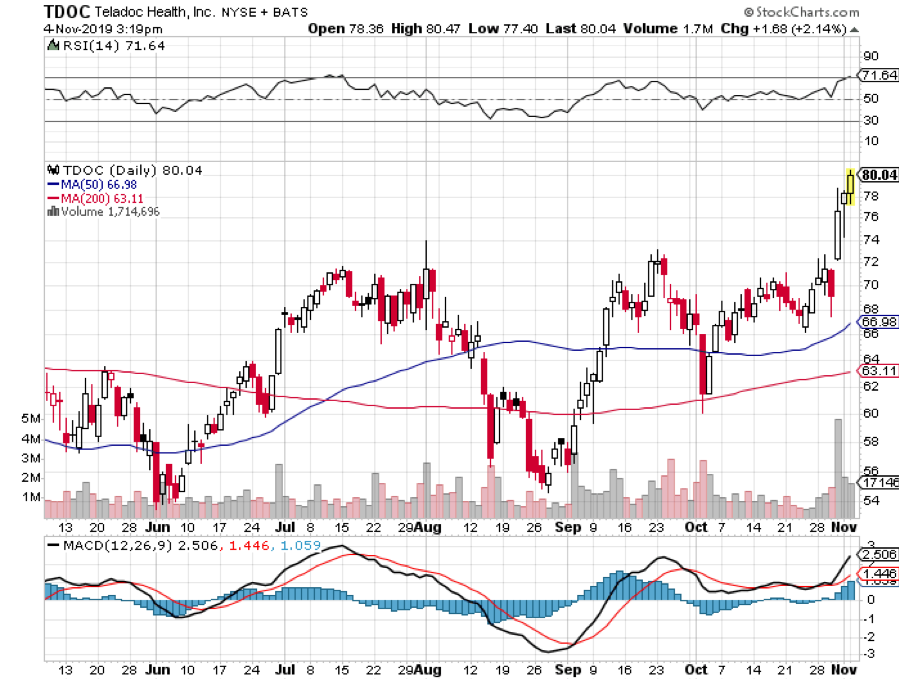

(DIALING FOR DOLLARS WITH TELEHEALTH),

(TDOC)

Healthcare consumers are experiencing a crisis. Over the past years, America has transformed into a country with the most expensive costs of care in the world with the American Medical Association reporting that the average spending of one person reaches $11,000 annually.

While this situation obviously burdens the consumers, looking at it from an investment perspective reveals just how much health insurers could stand to profit from it.

For instance, Anthem (ANTM) stock actually rose over 100% in the past three years, thanks to moderate revenue gains and huge bottom line profits. As enticing as that sounds, there are still healthcare companies out there aiming to keep the costs reasonable and the service convenient. One of them is Teladoc Health (TDOC).

Teladoc is a telehealth company that offers health services and medical advice to patients over the phone or via video conference calls. Although this is by no means a replacement of the traditional visits with your healthcare providers, the technology expands the reach of specialists especially when it comes to consultation services. It also provides a convenient platform for patients who will no longer need to actually make a trip to their doctors.

Most importantly, telehealth allows care providers to offer their services at lower prices. So far, spending on telehealth services is estimated to reach roughly $30 billion -- a staggering decrease from the multi-trillion-dollar amount Americans spend on healthcare services every year.

In the next five years or so though, the spending on telehealth services is anticipated to increase by approximately 20%. This could bring spending on this industry to a whopping $100 billion annually. Here is where Teladoc’s competitive advantage comes in.

At the moment, Teladoc is one of a handful of providers that actually has a global presence. The company is available in 130 countries and accessible in 30 languages. With such a broad market, Teladoc revenues showed an 89% increase year over year in 2017 and 79% in 2018. Meanwhile, the first half of 2019 saw the company’s profits hit a 40% increase year over year, with total patient visits rising 73% to reach 1.97 million.

Teladoc has also invested in promising acquisitions. Its $440 million merger with competitor Best Doctors back in 2017 has proved to be a great way to expand quickly and cover more ground.

For the third quarter of 2019, Teladoc once again delivered good results. The company’s revenues increased by 24% to reach $138 million, which surpassed Wall Street’s estimate of $136.5 million. Paid memberships in the United States grew by 55%, which now puts the total at 35 million members.

For its fourth-quarter earnings report, the company is expected to keep the momentum and rake in roughly $149 million to $153 million in profits, with a 2019 full-year revenue to be somewhere between $546 million and $550 million.

Despite the promising performance of Teladoc so far, there are still risks to consider before buying the stock. One of the major concerns is competition. Although Teladoc retains the title of being the leader in the telehealth services industry today, competitors American Well, Grand Rounds, and MDLive are gaining traction as well. Nonetheless, name recognition alone sets Teladoc apart from its rivals. However, the entrance of Amazon via its Amazon Care initiative in September is considered a major threat to the company.

All in all, Teladoc stock remains attractive. As with practically everything in investing, the key is to exercise due diligence and diversifying your portfolio. Teladoc is not a perfect company, but its sheer presence is already disrupting the healthcare industry. This makes the stock a good addition to a diversified portfolio, and the fact that you could be one of the pioneering investors makes it all the more exciting to own.

BUY (TDOC) on the next dip.

Mad Hedge Biotech & Healthcare Letter

October 31, 2019

Fiat Lux

Featured Trade:

(ONE PLUS ONE EQUALS THREE WITH THE PFIZER-MYLAN DEAL),

(PFE), (MYL)

"Greater than the sum of its parts." This is how the executives of Pfizer (PFE) described its merger with generic drug company Mylan NV (MYL) in the third quarter of 2019.

The deal, which is specifically between Mylan and Pfizer's off-patent department Upjohn, would result in the creation of the largest generics company by revenue in the world, reaching an enterprise worth $50 billion. In fact, this new company is anticipated to own roughly a third of all generics available today and approximately 15% of the generics market in the United States alone.

With the ever-changing pharmaceutical market, both Pfizer and Mylan have been grasping at straws in terms of reshaping their strategies and keeping up with the competition. Needless to say, this new powerhouse partnership comes as a relief for the investors of both Pfizer and Mylan.

This blockbuster deal allows Pfizer to focus its efforts on coming up with groundbreaking and more profitable products, hopefully beating its $54 billion sales in 2018. This move is a response to the insistent demand on the giant biopharma company to separate its Upjohn division, which works solely on legacy drugs, from the primary prescription-drug operations.

That way, Pfizer can focus on more lucrative, branded treatments like cancer medication Ibrance and pneumonia vaccine Prevnar.

This deal aligns with the recent moves by Pfizer acquiring potentially blockbuster treatments such as its $10.6 billion buyout bid of cancer treatment firm Array BioPharma earlier this year. This move is also reminiscent of Pfizer’s and GlaxoSmithKline’s (GSK) decision to merge their consumer healthcare departments.

Meanwhile, this all-stock deal provides Mylan with a financial lifeline following years of struggle. Its investors showed support over the deal as shares rose to as high as 19%, reaching $21.88 following the announcement.

While the generic drugs company, which is widely known for its emergency allergy medication EpiPen, is still far off from its all-time high of $67, this merger with Upjohn would allow both to amplify their efforts in dominating the market. More importantly, Mylan will retain a 43% stake in this new company.

For example, Mylan could boost Upjohn’s efforts in repackaging cholesterol drug Lipitor, nonsteroidal anti-inflammatory medication Celebrex, and erectile dysfunction medication Viagra as more attractive generic alternatives and boost their sales.

Since these drugs have expired or have expiring patents, their sales have been plummeting in the United States. With this merger though, Pfizer hopes to capitalize on the promising market called “branded generics” which has become quite popular in China.

“Branded generics” has gained a following in the Middle Kingdom due to the proliferation of fraudulent generic drugs – a trend that Pfizer has been eager to take advantage of seeing as the company actually moved Upjohn’s headquarters in Shanghai earlier this year.

Aside from Lipitor, Celebrex, and Viagra, the new company will also be handling the sales of over 7,500 Mylan products that include biosimilars and over-the-counter drugs.

With 165 markets targeted by this new company, its projected revenue is somewhere between $19 billion and $20 billion in 2020 and $22 billion in 2021. Meanwhile, its executives plan to solve the $25 billion worth of combined debt by targeting annual expense savings worth $1 billion to be reached by 2023.

In comparison, Mylan’s second-quarter adjusted earnings per share was at $1.03, with the company reaffirming its adjusted earnings for 2019 at $3.80 to $4.80 per share. Its profit for this year is estimated to reach $11.5 billion to $12.5 billion.

Meanwhile, Pfizer’s second-quarter report recorded $13.2 billion in sales, which indicates a 2% decrease from last year’s report during the same period. Meanwhile, Upjohn’s revenue fell by 11% year-over-year and hit $2.8 billion compared to the $3.1 billion last year.

With all these advantages, it can be safely said that Mylan was an excellent choice for Pfizer especially considering that the smaller company came in so cheap.

In 2018, Mylan was valued at $25 billion. Prior to the announcement in July though, Mylan only had a market cap of $10 billion. With the money saved on the deal, the newly formed company can push back on pricing and pour funds over marketing their generic products.

Even with the cheap buyout price, the new company will still be less levered compared to a stand-alone Mylan. It’s also projected to generate over $4 billion in free cash flow annually.

This deal eliminates a strategic bottleneck from Pfizer and solves the financial woes of Mylan. While there remains a lot to be seen in terms of achieving their goals, investors of both companies will definitely enjoy a brighter future.

After all, this new company boasts of an incredibly powerful mix of a portfolio that covers generics, branded products, over-the-counter meds, and biologics.

Buy Pfizer on dips. It is about to achieve a major breakout to the upside on the back of this fantastic deal.

Mad Hedge Biotech & Health Care Letter

October 29, 2019

Fiat Lux

Featured Trade:

(THE BIG MEDICARE PLAN WITH HUMANA),

(ANTM), (CI), (HUM), (UNH)

Sometimes, markets are right, and sometimes, they are wrong. With regard to the healthcare industry these days, they have definitely got it wrong. For they are overweighting the political risk to this group presented by the 2020 presidential election.

Even if the most extreme leftist candidate, Elizabeth Warren, wins, she will still have to get the plans through congress. And after the experience of the last three years, you can bet the next congress will be a pretty moderate bunch.

Just as President Trump found it impassable to kill Obamacare, even with an all-Republican Congress, Warren will find it equally difficult to get the most expensive form of Medicare for all passed into law.

Take this view, and all of a sudden, the healthcare industry becomes wildly cheap. In fact, it is one of the lowest valued, highest earning sectors in the entire stock market.

Shares of managed care companies have certainly struggled this year. For instance, Anthem (ANTM) went down 5.1%, Cigna (CI) sunk 13.2%, UnitedHealth Group (UNH) declined by 2.2%, and Humana (HUM) fell 0.3%.

Due to the country’s turbulent political climate courtesy of the impending 2020 elections, investors are anxious over Medicare for All, which has the capacity to shut down the entire industry altogether.

As expected, these fears have weighed heavily on health insurance stocks and these companies are anticipated to experience a rollercoaster of emotions in the next year and a half. However, there could be convincing reasons for Humana to stand out from the rest.

Zeroing in on “population health management” along with “social determinant of health,” the company has been working on boosting its dominance on nonclinical services to deliver better health results. This is because approximately 80% of health outcomes are linked to nonclinical issues. Hence, this initiative could lead to improved products for customers and cost savings.

This is why Medicare Advantage, which allows private insurers to collaborate with Medicare for care coverage, turned into the “crown jewel” of Humana’s growth strategies. Basically, this plan appears and functions like a private health plan but is actually a government-sponsored program.

To date, Humana is the second biggest Medicare Advantage provider growing its membership by 15% during the second quarter of both 2018 and 2019.

As of 2018, the company holds a 17% share of the 20.4 million people enrolled in the Medicare Advantage program, with plans comprising roughly a quarter of the managed care’s medical membership. This accounts for almost three times the industry average, which indicates a positive growth for Humana as Medicare is projected as the fastest-growing sector of the insurance industry in terms of spending.

Actually, basic math could easily illustrate Humana’s upward trajectory as well. The number of Americans eligible for a Medicare plan is increasing by roughly 3% annually. Based on data from the Congressional Budget Office, the number of Medicare recipients opting for Medicare Advantage is estimated to climb from 34% of those eligible for Medicare in 2018 to 42% by 2028. Clearly, this increase offers a lot of room for growth, and Humana is smack dab in the center of it.

Although UnitedHealth actually has more members in the said program at the moment, no other managed care company is as intensive and focused as Humana. In fact, 73% of Humana’s consolidated revenue comes from its Medicare Advantage membership earnings alone. This makes the company a Medicare Advantage pure play.

Holding its position as one of the leaders in this private option available within the Medicare community, Humana has established a stronghold in this ever-evolving and constantly turbulent industry. So far, the stock’s price target is projected to hit $315. Long-term investors could also finally expect to shake off healthcare fear jitters and big rewards from 2021 onwards if the elections result in Democratic leadership.

Looking at Humana’s earnings history, it can be seen that it has grown from $7.75 per share in 2015 to $14.55 by 2018. For this year, the company’s projected earnings is expected to reach $17.50 a share. However, the possibility of a federal tax on health insurers could pose a threat to the company’s growth.

Humana is well-poised for advancement on the back of its strategic plans involving its Medicare business and promising initiatives. In the past years, Humana has been deploying excess capital and hiking its dividend. Just in February 2019, the company increased its dividend by 10% to reach 55 cents a share.

As part of its repurchase strategy, Humana allocated $3 billion for its buyback plans. These moves further indicate the financial capacity of the company and could hopefully reinvigorate investor confidence.

Mad Hedge Biotech & Healthcare Letter

October 24, 2019

Fiat Lux

Featured Trade:

(SPECIAL CANCER ISSUE - PART II)

(LLY), (PFE), (GTHX)

The most groundbreaking biotechnology discoveries in this century have now reached the flashpoint between theoretical discussions and their realization. Billions of dollars have been poured into the research and development phases, with some companies already generating income. More impressively, potential cures for a number of fatal diseases are now in the pipeline. For early investors, this translates to massive earnings in the succeeding years.

Among the widely sought-after cures is for triple-negative breast cancer (TNBC), which is the most aggressive form of the disease. It also has a poorer prognosis compared to other types of breast cancer, so it’s crucial to offer treatments that can not only improve chances of survival but also improve the quality of life of the patients suffering from it.

Here are the three most promising developments in the search for the cure of TNBC.

Eli Lilly (LLY)

It’s always challenging to be a third-to-market treatment especially when you’re trailing a pioneering drug like Pfizer’s (PFE) groundbreaking drug Ibrance and Novartis’ blockbuster drug Kisqali. However, Eli Lilly (LLY) is hoping that its recent data on Verzenio would bolster its hold in the market.

While it remains to be seen if Verzenio can catch up with Ibrance’s success, the Eli Lilly drug has managed to surpass estimates by $19 million during the first quarter of 2019 following an underwhelming fourth quarter in 2018. As for the latest data on Verzenio, the company disclosed that a combination of the drug and hormone therapy improved the median to 46.7 months compared to the 37.3 months for those who solely underwent therapy.

The 9.4 survival advantage indicates a 25% decrease in mortality risk. Apart from that, patients also enjoyed a better quality of life as this combo allowed them to manage for 50 months -- or over four years -- without the need for follow-up chemotherapy. This is a huge advantage since hormone therapy alone only allowed 22 months before the next treatment.

The effects don’t end there though. Eli Lilly has another trick up its sleeve to make sure that it stands out from the drugs targeting similar diseases. According to the company, Verzenio is the only drug that can help patients with tough-to-treat diseases.

That is, the Eli Lilly drug took effect even on patients who were initially resistant to therapy as well as those who quickly relapsed after treatment. This resulted in a decrease in death risk by roughly 31%. While this aspect still requires additional tests, the results showed a promise that not even Pfizer’s Ibrance can deliver.

Merck & Co. (MRK)

Merck & Co. (MRK) has rallied virtually the entire force of its research and development team behind ensuring that Keytruda remains on top -- way ahead of competitors like Bristol Myers Squibb’s (BMY) Opdivo. At the moment, Merck’s moneymaker has approximately 1,050 clinical trials queued to assess the possibilities of this drug further dominating clinical practice.

So as Bristol Myers Squibb attempts to woo investors with the promising results of Opdivo, Merck has been busy adding another notch in its belt with another landmark first for Keytruda. Aside from its current applications, this Merck cash cow is also pegged as a promising treatment for TNBC when combined with therapy.

Based on the data on its breakthrough therapy designation, this indication is likely on the fast track towards an FDA approval soon. To date, Keytruda has more than 20 oncology indications in the United States alone with the giant biopharma receiving the green light to market the drug in China as well.

If things move forward as planned, Keytruda may very well be on its way to topple AbbVie Inc.’s (ABBV) Humira from the top of the list of best-selling drugs worldwide in the next five years. After all, revenues from the drug are expected to hit anywhere between $17 billion and $24 billion in 2024.

G1 Therapeutics (GTHX)

Joining the biopharma giants is newcomer G1 Therapeutics (GTHX). This up-and-coming firm has recently released its clinical data on oral selective estrogen receptor degrader (SERD) for metastatic TNBC. Called G1T48, this new treatment provided promising results when combined with the company’s own breakthrough therapy called trilaciclib.

For comparison, G1 Therapeutics’ combo is said to be more potent than AstraZeneca plc’s (AZN) Faslodex, which is currently the only FDA-approved SERD treatment in the market. Unlike Faslodex though, which requires intramuscular injection, G1 Therapeutics’ drug can be taken orally once a day. Needless to say, this mode of treatment offers an improved patient experience.

With such promising results, G1 Therapeutics plans to roll out new drug application submissions by the fourth quarter of 2019. If things move smoothly, then the treatment plan should be out in the market sometime in the second quarter of 2020.