Mad Hedge Biotech and Healthcare Letter

September 10, 2024

Fiat Lux

Featured Trade:

(THE NEW SHOT CALLER)

(PCVX), (PFE), (MRK)

Mad Hedge Biotech and Healthcare Letter

September 10, 2024

Fiat Lux

Featured Trade:

(THE NEW SHOT CALLER)

(PCVX), (PFE), (MRK)

There’s nothing like a little competition to shake things up in the vaccine world, and it looks like Vaxcyte (PCVX) just lobbed a serious challenge at the reigning king of pneumococcal shots, Pfizer (PFE).

You know that satisfying smack when a basketball, held under water, bursts free and cracks you in the nose? That’s what’s happening in the vaccine market right now.

Vaxcyte just threw down the gauntlet with its experimental pneumococcal vaccine, VAX-31, going toe-to-toe with Pfizer’s Prevnar 20 in an early-stage trial. And let’s just say, the results are giving Pfizer’s brass plenty to worry about at their next earnings call.

VAX-31 didn’t just keep pace—it outperformed Prevnar 20, showing a stronger immune response against 18 out of 20 strains of those pesky streptococcus bacteria. This isn’t just a pat on the back; it’s a flashing neon sign that a market shake-up is on the horizon.

For those not yet familiar with Vaxcyte, let’s break it down. This biotech upstart is developing next-generation vaccines designed to do more than just fight infections—they’re engineered to outsmart them.

Vaxcyte’s secret weapon? That would be their XpressCF platform, a game-changing cell-free protein synthesis technology that’s rewriting the rules of vaccine development.

Unlike conventional methods that rely on live cells to produce proteins—a process that can be as slow and finicky as trying to bake a soufflé in a wind tunnel—XpressCF takes a completely different approach.

Essentially, XpressCF makes it possible to create complex proteins in a controlled environment without the need for live cells.

By extracting and using only the essential components from Escherichia coli bacteria, Vaxcyte can synthesize proteins with a level of precision that’s simply unattainable with traditional cell-based systems.

This not only speeds up the production process—cutting out the unpredictable nature of working with live cells—but also allows Vaxcyte to fine-tune the proteins to be more effective against the bacteria they’re targeting.

And as for the result? Vaccines that are not just produced faster, but are also more precisely engineered to take down the most stubborn pathogens. It’s like swapping out a sledgehammer for a scalpel—more targeted, more effective, and less room for error.

This leap forward in technology means Vaxcyte can potentially offer broader protection with fewer side effects, all while dodging the common production headaches that have plagued traditional vaccine development for decades.

And, as expected, Vaxcyte’s pipeline is packing some serious heat with VAX-31 and VAX-24, targeting 31 and 24 strains of IPD, respectively.

These vaccines are aimed squarely at protecting the most vulnerable—infants and adults over 50—from these dangerous infections.

While VAX-24 is leading the charge with Phase 2 trials already showing promising results, VAX-31 is closing in fast and could be the breakout star when it hits the market.

And here’s where it gets even more interesting. Vaxcyte has its sights set on a Phase 3 trial for VAX-31 in adults by mid-2025, with data expected to roll in by 2026.

If everything goes according to plan, Vaxcyte could have not one but two blockbuster vaccines ready to rock the market by 2027 — just as Pfizer and Merck (MRK) might be getting a little too comfortable in their respective corners.

Now, let’s pivot to the bigger picture. Pfizer’s Prevnar 20 and its predecessor, Prevnar 13, are nothing short of cash cows, raking in $6.4 billion in 2023—more than all but two other Pfizer products.

Merck isn’t just sitting on the sidelines, either. Their Vaxneuvance and Pneumovax 23 contributed a cool $1.1 billion to the bottom line last year.

With VAX-31 stepping into the ring, though, it’s like David just found a very large and very effective rock.

But before we get too far ahead of ourselves, let’s remember that biotech is a high-stakes game. The risks are real, and the path to FDA approval is littered with potential setbacks.

Still, Vaxcyte’s got a few things going for it that could make this a winning bet.

For starters, they’ve got $518.7 million in cash, $934 million in short-term investments, and zero debt. That’s a war chest of $1.5 billion to fund their march toward FDA approval without breaking a sweat.

From a valuation standpoint, Vaxcyte’s market cap is sitting pretty at $12.5 billion, and while some might balk at their price-to-book ratio of 6.3 compared to the sector’s median of 2.4, I’d argue that you get what you pay for.

After all, you’re not just buying into a company. If anything, you’re actually buying into a potential industry leader. And in a market where the reigning king is starting to sweat, that might be the most valuable investment of all.

Mad Hedge Biotech and Healthcare Letter

September 5, 2024

Fiat Lux

Featured Trade:

(A VERY STRONG CELL-ING POINT)

(TXG), (NSTG), (BRKR), (ILMN), (BMY), (GILD), (BIO)

I've been tracking the biotech sector for decades now, and let me tell you, we're on the cusp of something big. Single-cell and spatial genomics are shaking up cancer research like nothing I've seen before.

Remember when we used to look at tumors as one big blob of cells? Those days are gone.

Now, it's not just about understanding tumors anymore – it's about dissecting them cell by cell, mapping them out like uncharted territories.

Single-cell genomics is giving us a front-row seat to the cellular soap opera playing out in every cancer.

From where I'm sitting, this is the kind of revolution that separates the wheat from the chaff in my portfolio. We're not just identifying the players anymore. Instead, we're mapping out their positions and interactions with unprecedented precision.

Take what's happening at St. Jude Children's Research Hospital. They're using single-cell genomics to crack the code on why some stages of B-cell acute lymphoblastic leukemia thumb their noses at chemotherapy.

And this isn't just academic navel-gazing. It's actually paving the way for treatments that pack a real punch.

Or look at what Fynn Biotechnologies is doing with 10X Genomics' (TXG) Xenium In Situ platform.

They're peering into breast cancer tumors and finding that the neighborhood where immune cells hang out can make or break immunotherapy.

This is the kind of insight that turns the one-size-fits-all approach to cancer treatment on its head.

Now, let's talk turkey. Where's the money in all this? I've got my eye on a few players.

First up, 10X Genomics. These folks aren't just dipping their toes in the single-cell and spatial genomics pool; they're doing cannonballs.

Their Chromium and Xenium platforms are becoming the go-to tools for researchers and clinics alike.

And the numbers don't lie – they pulled in $156 million in Q2 2024, up 25% from the year before.

NanoString Technologies (NSTG) is a bit of a different story. They've been a big name in spatial biology with their GeoMx Digital Spatial Profiler, but they've hit some rough waters.

Filing for Chapter 11 in early 2024 wasn't on anyone's bingo card. Despite a solid Q4 2022 with $36.2 million in revenue (up 29% year-over-year), their legal tussle with 10x Genomics and other financial headaches have put them in a tight spot.

But don't count them out yet – Bruker Corporation (BRKR) swooping in to buy up their assets might just be the lifeline they need.

Illumina Inc. (ILMN) is another heavyweight worth watching. I’ve said it before, and I’ll say this again – this biotech is the reigning 800-pound gorilla in DNA sequencing. And now, they're muscling into single-cell genomics.

Their acquisition of GRAIL shows they're serious about early cancer detection. Sure, they've had some regulatory speed bumps, but with a market cap of about $33 billion in Q3 2024, they're not going anywhere.

Don't overlook the big pharma players either. Bristol-Myers Squibb (BMY) is betting big on precision medicine, teaming up with 10X Genomics to bring single-cell analysis into their drug development pipeline.

With BMY’s oncology portfolio raking in $17.3 billion in 2023, they've got the cash to make big moves.

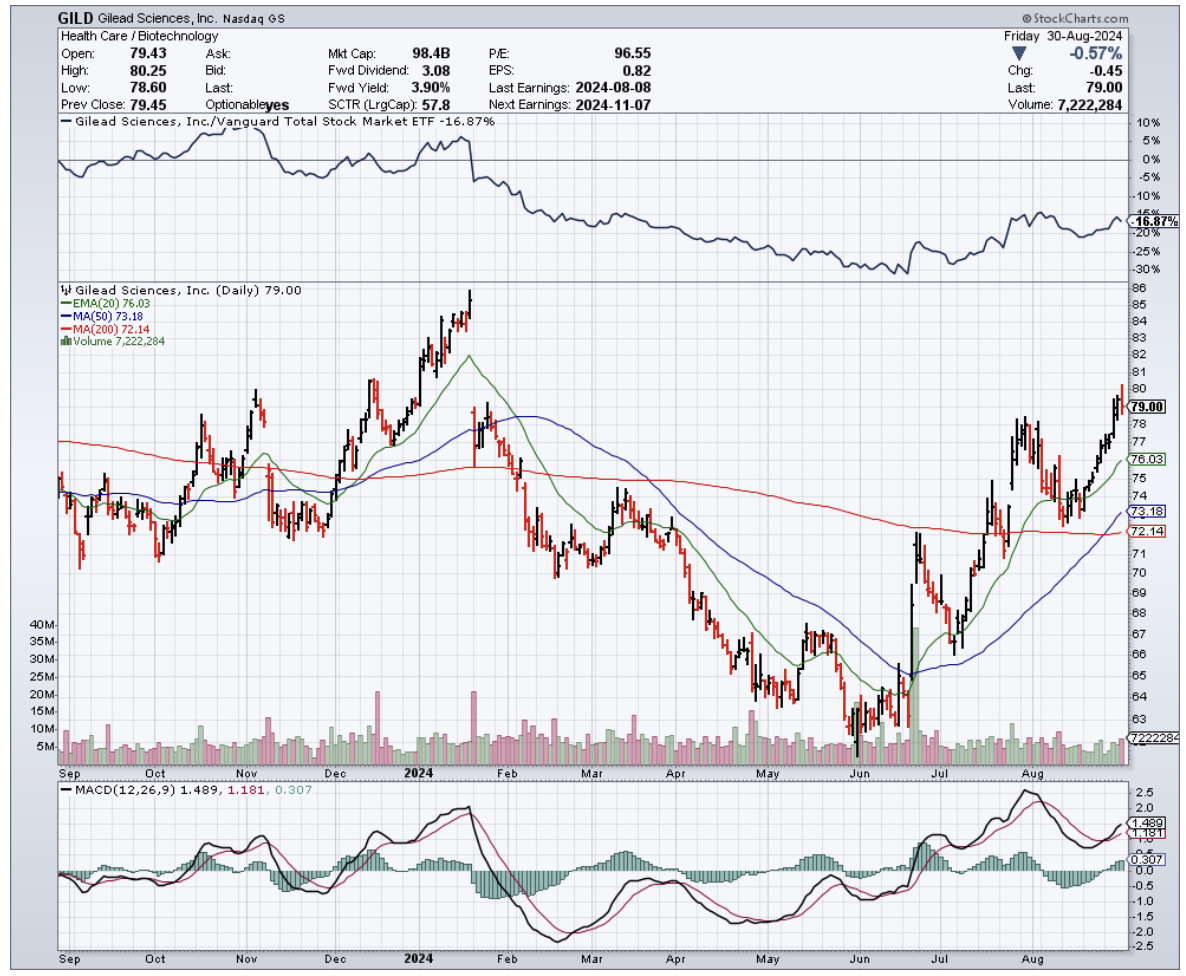

Gilead Sciences (GILD) is another one to keep an eye on. Their purchase of Kite Pharma put them in the cell therapy game, and they're not shy about using genomic data to develop new cancer treatments. In fact, their cancer segment grew by 22% in 2023.

And let's not forget Bio-Rad Laboratories (BIO). They might have seen a slight dip in net sales from $2.9 billion in 2022 to $2.68 billion in 2023, but their Single-Cell ATAC-Seq Solution is still a key player in epigenomic analysis.

Now, let's zoom out and connect the dots. The genomics market is on a tear.

We're looking at a jump from $18.85 billion in 2020 to a projected $62.9 billion by 2028. That’s a massive growth, and it's directly impacting companies across the board.

Take 10X Genomics, for instance. Their Q2 2024 revenue hit $156 million, a 25% year-over-year increase that's directly tied to the surging demand for their single-cell and spatial genomics tools.

The single-cell genomics market alone was worth $2.4 billion in 2022 and is looking at a CAGR of 16.7% from 2023 to 2030.

Meanwhile, the precision medicine market, fueled by these genomic advancements, is projected to balloon from $66.1 billion in 2023 to $140.6 billion by 2030.

Let's not kid ourselves, though. Biotech investing is not for the faint of heart. You've got to have the stomach for high R&D costs, regulatory labyrinths, and cutthroat competition.

Just look at NanoString Technologies - one minute they're reporting a 29% revenue increase, the next they're filing for Chapter 11. It's a rollercoaster, but for those who can hang on, the potential payoff is enormous.

So, where does this leave us? Well, I didn't spend decades in this game to tell you to play it safe, but I'm not here to see you bet the farm either. Instead, I’m here to tell you to play it smart.

Add those nimble upstarts like 10x Genomics to your watchlist - they're the racehorses that could leave the pack in the dust.

And when the market gets jittery, that's your cue to swoop in on steady workhorses like BMY and Gilead. They might not be as sexy, but they’ve got the tried-and-tested staying power.

Remember, in biotech, today's underdog can become tomorrow's alpha faster than you can sequence a genome.

So stay alert, keep your powder dry, and for Pete's sake, don't wait for a gilded invitation to buy the dip.

Mad Hedge Biotech and Healthcare Letter

September 3, 2024

Fiat Lux

Featured Trade:

(ROLLING THE DICE ON BIOTECH)

(RHHBY), (VNDA), (ZVRA), (HALO), (BMY), (GILD)

Remember when you'd jump into a hot tub and the water was just right? That's what the biotech sector feels like right now - it's warming up and ready for a splash.

After years of treading water, biotech stocks are showing signs of life. High interest rates and cash crunches have kept this sector on the sidelines, but the game is changing.

September 2024 is shaping up to be a blockbuster month for the sector, with FDA decisions that could send stocks soaring - or sinking.

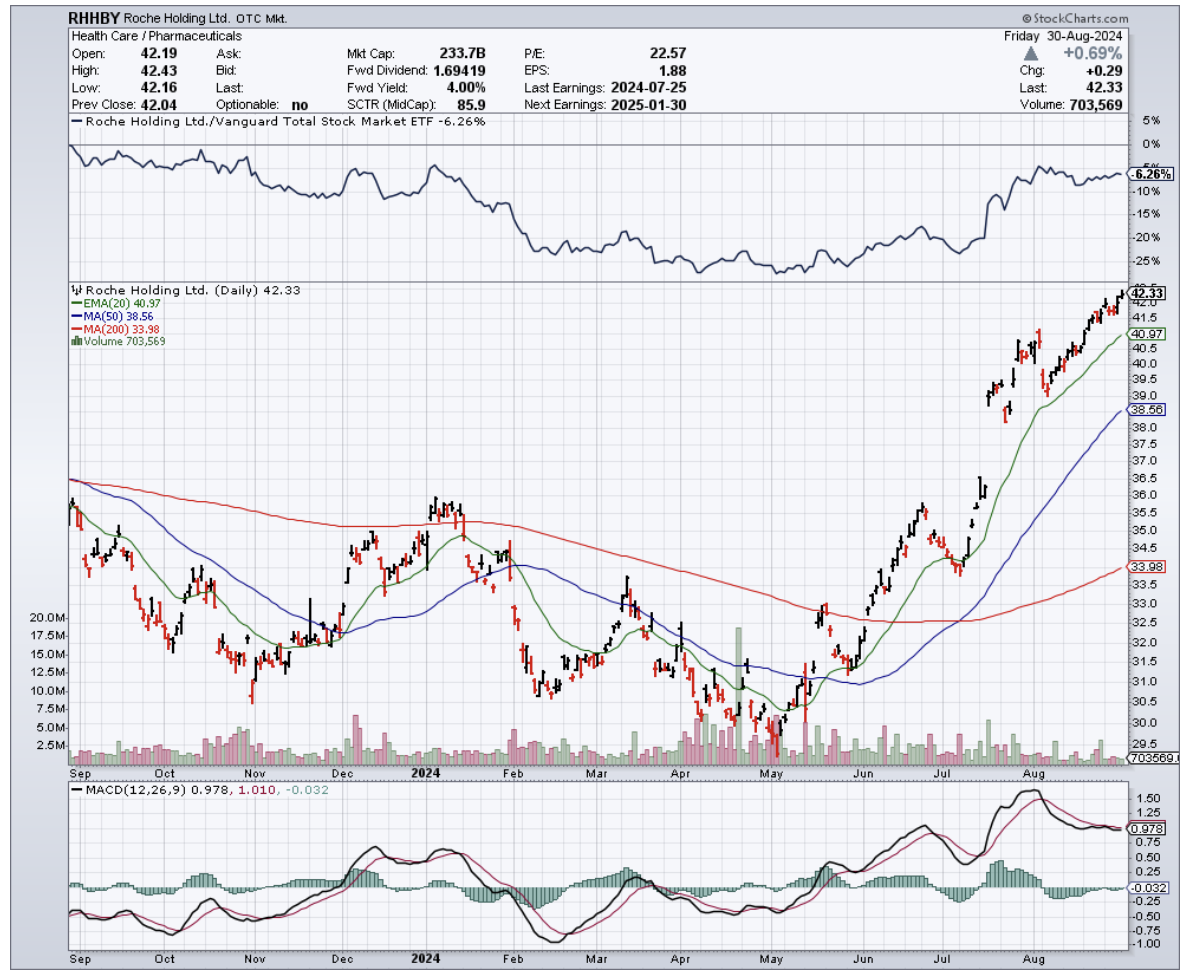

First up, Roche Holding AG (RHHBY) is waiting on pins and needles for the FDA's verdict on Ocrevus SC. This isn't just another drug - it's a new way to deliver their multiple sclerosis cash cow.

If the FDA gives the green light on September 13, Roche could be looking at a bigger slice of the MS pie. Why? Because this new version doesn't need fancy IV setups, opening doors to treatment centers that were previously off-limits.

But Roche isn't the only one with butterflies in its stomach.

Vanda Pharmaceuticals (VNDA) is hoping to make history on September 18 with Tradipitant. This drug aims to tackle gastroparesis, a condition that's been stuck in treatment limbo for four decades. If Tradipitant gets the nod, Vanda could find itself as the big fish in a very lucrative pond.

And let's not forget about the underdogs.

Zevra Therapeutics (ZVRA) is crossing its fingers for Arimoclomol. This potential game-changer targets Niemann-Pick disease type C, a rare brain disorder that's been waiting for its medical knight in shining armor. September 21 could be that day.

These approvals aren't just good news for the companies involved. They're like a shot of adrenaline for the whole biotech sector. Investors love nothing more than seeing potential turn into profit.

But it's not all about solo acts in biotech. These days, it's all about partnerships.

Take Halozyme Therapeutics (HALO), for instance. They've buddied up with Roche to develop Ocrevus SC, bringing their ENHANZE technology to the party.

These kinds of collaborations are golddust for smaller biotech firms. They get access to resources and markets they could only dream of on their own, making them much more attractive to investors with deep pockets.

Speaking of deep pockets, big pharma companies are on the prowl, and several biotech firms are looking mighty tasty.

Bristol-Myers Squibb (BMY) just showed us how it's done by snatching up Karuna Therapeutics. Why? Two words: KarXT.

This antipsychotic drug is currently under FDA review for schizophrenia, and if approved, it could be another lucrative revenue stream. This kind of deal is a win-win. The big fish gets new toys for its pipeline, and the smaller fish gets a cushy new home.

Now, let's talk about the elephant in the room - interest rates.

Biotech companies and high interest rates go together like oil and water. These firms need cash like plants need water, and high rates make that cash harder to come by.

But here's the thing: the Federal Reserve is hinting at rate cuts.

For biotech, that's like Christmas coming early. Lower rates mean easier borrowing and easier borrowing means more research, more trials, and potentially more breakthroughs.

So if rates drop, don't be surprised to see biotech stocks shoot up faster than a rocket.

But it's not just about drugs in the pipeline. The biotech sector is also home to some serious innovation.

Take gene editing and CRISPR. This isn't your grandpa's genetics - it's like we've found the “track changes” function for DNA.

The market for this molecular magic is set to explode from $4 billion in 2024 to a whopping $17.8 billion by 2034. That's a 16.1% annual growth rate, for those of you keeping score at home.

With this technology, I’m not just talking about curing rare diseases here. I’m talking about the possibility of having your own home testing kits that could make your 23andMe results look like a fortune cookie.

And then there’s personalized medicine, which is turning healthcare into a bespoke tailor shop. Your DNA is becoming the blueprint for your treatments, and the market is following suit.

We're looking at a jump from $300 billion in 2021 to $869.5 billion by 2031. Why the boom? Well, sequencing your DNA used to cost more than a mansion.

Now it's cheaper than a decent night out in New York - from over $1 million in 2007 to about $600 today.

Stem cells and regenerative medicine are also getting investors hot under the collar. We're talking about potentially regrowing organs or giving Parkinson's the boot.

This market is set to grow at a spicy 9.74% annually from 2023 to 2030. Basically, it’s like we're entering the age of biological LEGO.

And let's not forget AI - the new brainiac in the lab. It's turning drug discovery into a high-speed chess game, with the AI market in healthcare expected to hit $95.65 billion by 2028.

With the innovations from this tech, scientists could have supercomputers as their lab partners – ones that never need coffee breaks and can crunch data faster than you can say "blockbuster drug."

Given all these possibilities, I think it’s a good time to talk about strategy. After all, investing in biotech isn't one-size-fits-all. It's more like a buffet - you pick what suits your taste and risk appetite.

For the adrenaline junkies who like to walk the tightrope without a net, there's the high-risk, growth investor approach. These brave souls get their kicks from cutting-edge stuff like gene editing and personalized medicine, often diving into early-stage biotech firms working on the next big breakthrough.

It's not for the faint of heart - these stocks can swing wilder than a monkey on espresso. But when they hit, oh boy, do they hit.

Just look at the personalized medicine market - it's set to explode from $300 billion in 2021 to a mind-boggling $869.5 billion by 2031. That's the kind of growth that could make your portfolio do backflips, assuming you can stomach the ride.

On the other side of the petri dish, we've got the value and low-risk investors. These are the steady hands who prefer their biotech stocks aged like fine wine and served with a side of sleep-easy. They're eyeing established companies with robust pipelines, diverse portfolios of approved drugs, and ongoing trials.

Think Roche with its Ocrevus SC, or old guards like Gilead Sciences (GILD) that have weathered more storms than a lighthouse.

These investors are the tortoises in the biotech race - slow and steady, but with a knack for crossing the finish line, often with a healthy dividend check in hand. They might not make headlines, but they're more likely to let you sleep soundly while your portfolio does the heavy lifting.

No matter which style you choose, one thing is undeniable: the biotech sector is like a sleeping giant, and it's starting to stir. The question is, will you heed the wake-up call or sleep through the alarm?

Mad Hedge Biotech and Healthcare Letter

August 29, 2024

Fiat Lux

Featured Trade:

(ONE TEST TO RULE THEM ALL)

(ILMN), (BAYRY), (LLY), (MRK), (BMY), (AZN), (RHHBY), (NVS), (GH), (TEM), (TMO)

“One test to rule them all, one test to find them, one test to bring them all, and in the lab bind them,” the scientists at Illumina (ILMN) whispered – probably.

Their latest creation just got the FDA nod, and it's set to turn the world of cancer diagnostics on its head. It's as if Gandalf himself handed oncologists a palantír that reveals tumors' deepest secrets.

For those less versed in Middle-earth lore, this is like inventing a universal remote for tumor profiling, and oncologists can't wait to start channel surfing.

Now, you might be thinking, "What's the big deal?" Well, let me break it down for you.

This test, called TruSight Oncology Comprehensive (TSO for short), is the first FDA-approved genomic in vitro diagnostic kit that can make pan-cancer companion diagnostic claims.

In plain English, that means it's a single test that can be used across multiple cancer types. We're talking about a game-changer in precision oncology here.

Let's get into the nitty-gritty. This TSO test is a beast. It screens for a whopping 517 genes and provides comprehensive information on tumor mutational burden (TMB) and microsatellite instability (MSI).

These are crucial biomarkers that help determine how a patient might respond to immunotherapies. The breadth of data this single FDA-approved test can collect is unprecedented.

Now, you might be wondering, "Haven't we had companion diagnostics before?" Sure, but they've typically been limited to specific drugs or cancer types.

This pan-cancer test from Illumina is different. It can be applied to a wider range of solid tumors, and let me tell you, oncologists are loving it.

In fact, about 39% of U.S. oncologists have already said they strongly prefer using multi-gene panels over single-gene tests for guiding treatment decisions. That's a clear signal that there's demand for comprehensive diagnostic solutions like TSO.

Illumina's been busy across the pond, too. A version of this test has been available in Europe since 2022. But the U.S. version's got some new tricks up its sleeve.

It can help identify patients who might benefit from specific immunotherapies, including Bayer's (BAYRY) Vitrakvi and Eli Lilly's (LLY) Retevmo. The latter is a new addition compared to the EU version of the test.

Let's talk about these therapies for a second. Vitrakvi is used for adult and pediatric patients with certain NTRK mutations, regardless of their type of cancer. That's pretty cool, right?

But here's the kicker - these NTRK gene fusions are only found in about 0.1% to 0.3% of solid tumors, and they're tough to detect.

TSO's ability to scan both RNA and DNA means it can find multiple forms of this biomarker. That's a big deal for companies like Bayer, who've sometimes struggled to find eligible patients for this targeted therapy.

But Illumina's not resting on its laurels. They've got a growing pipeline of companion diagnostic claims in development, working hand in hand with drugmakers. They're planning to seek these in future regulatory submissions.

You see, Illumina's been playing the long game, forging partnerships with big pharma to co-develop companion diagnostics that align with targeted therapies.

Take their 2019 partnership with Merck (MRK), for instance. They teamed up to develop and commercialize a companion diagnostic using Illumina's TruSight Oncology 500 assay.

The goal? To identify genetic mutations in cancer patients that would respond to Merck's cancer drugs like Keytruda. This partnership boosted the adoption of Illumina's NGS platform in clinical oncology settings, contributing to both companies' growth.

The market liked what it saw at the time. Illumina's stock got a nice bump following the partnership announcement. And why wouldn't it?

The deal strengthened Illumina's position in the oncology diagnostics market, which is projected to grow at a CAGR of 12.4% from 2023 to 2030.

But Merck's not the only dance partner Illumina's got. They've also teamed up with Bristol-Myers Squibb (BMY) to use their TSO 500 assay as a companion diagnostic for immuno-oncology therapies.

This collaboration expanded Illumina's reach into new oncology applications, allowing BMY to use the TSO platform to identify patients most likely to benefit from its immune checkpoint inhibitors.

And there's more - Illumina's also forged partnerships with AstraZeneca (AZN), Roche (RHHBY), and Novartis (NVS) to develop companion diagnostic tests.

Next, let's talk numbers. Each new FDA-approved indication could potentially add $100 million to $200 million annually to Illumina's revenue. That's no chump change.

Unsurprisingly, Illumina's not the only player in this game.

Companies like Foundation Medicine (a Roche subsidiary), Guardant Health (GH), Tempus (TEM), Caris Life Sciences, Thermo Fisher Scientific (TMO), and GRAIL (another Illumina subsidiary) are all working towards pan-cancer or multi-cancer diagnostics.

Still, Illumina's TSO test is the first to secure FDA approval for pan-cancer companion diagnostic claims. This lead could translate into a significant market advantage.

Actually, Illumina already holds more than 70% market share in the global NGS market as of 2022. This means it’s well-positioned to benefit from this growth, and this latest FDA approval could further consolidate its market dominance.

Speaking of the FDA, they’ve been busy too. They've ramped up their support for precision medicine in recent years, approving a growing number of companion diagnostics and genomic tests.

From 2017 to 2021, they approved over 25 new companion diagnostics, a significant increase from the 5-10 approvals per year in the early 2010s. And a substantial portion of these approvals has been for oncology-related tests.

In 2021 alone, 68% of the FDA's new drug approvals were for cancer treatments.

Now, let's zoom out and look at the bigger picture. According to the World Health Organization, there were an estimated 19.3 million new cancer cases and 10 million cancer deaths worldwide in 2020.

The global cancer burden is expected to rise to 28.4 million cases by 2040, a 47% increase from 2020.

In the U.S., about 1.9 million new cancer cases are expected to be diagnosed in 2023.

The economic impact is also staggering. The economic burden of cancer in the U.S. was estimated at $157 billion in 2020, and it's projected to increase to over $246 billion by 2030.

These numbers stress the growing need for early detection and personalized treatment solutions.

But, unlike other companies, here's where advanced diagnostics like Illumina's TSO can make a difference. By ensuring patients receive the most effective treatments based on their genetic profiles, these tests can reduce unnecessary treatments and improve outcomes.

Studies have shown that using precision diagnostics can lower overall healthcare costs by 15% to 20% by avoiding ineffective therapies and hospitalizations.

Essentially, what we're seeing here is more than just a new test. It's a glimpse into the future of cancer treatment - more precise, more personalized, and potentially more effective.

For patients, it could mean better outcomes. For healthcare systems, it could mean more efficient use of resources. And for us? Well, it could mean significant opportunities in a rapidly growing market.

As Gandalf might say, "All we have to decide is what to do with the time that is given us." Illumina's chosen to use their time crafting this powerful new tool.

The quest to conquer cancer continues, and Illumina’s TSO might just be the ring-bearer we've been waiting for.

Keep your eyes peeled, fellow adventurers. The journey into precision oncology is only just beginning, and it promises to be an epic saga indeed.

Mad Hedge Biotech and Healthcare Letter

August 27, 2024

Fiat Lux

Featured Trade:

(NOT ALL THAT GLITTERS IS LILLY)

(JNJ), (LLY), (CRSP), (ISRG)

I've been so busy chasing after Eli Lilly (LLY) and its trillion-dollar dreams that I nearly overlooked a gem in the making.

While everyone's obsessing over LLY's march towards that coveted $1 trillion market cap, there's another pharma giant that's been quietly chugging along, building value like it has for over a century.

I'm talking about Johnson & Johnson (JNJ). You know, that little company that's only been around for 138 years.

I understand that JNJ isn’t as exciting as the likes of Crispr Therapeutics (CRSP) with their fancy gene editing therapies, or Intuitive Surgical (ISRG) with their robotic surgeons, but, let me tell you, sometimes boring is beautiful – especially when it comes with a 3% dividend yield and a rock-solid business model.

Let's break it down, shall we?

First off, JNJ isn't sitting on its laurels. Just last week, they dropped $1.7 billion to snatch up a private heart-device company. That's not chump change, even for a behemoth like JNJ.

And speaking of big moves, the FDA just gave them the green light for a chemotherapy-free lung cancer treatment.

We're talking about Rybrevant plus Lazcluze, which showed a 30% reduction in the risk of disease progression or death compared to AstraZeneca's (AZN) offering.

That's not just incremental progress – that's potentially life-changing stuff for patients.

But they’re not stopping there. They're also shelling out $600 million upfront (with potential milestone payments up to $1.1 billion) for V-Wave, a company making shunts for heart failure patients.

This deal's expected to close before the year's out, beefing up JNJ's already impressive MedTech division.

Now, let's talk numbers. JNJ's current market cap is sitting pretty at just under $400 billion. Sure, it's not in Lilly's $850 billion stratosphere, but remember – slow and steady wins the race.

And speaking of winning races, JNJ was the global leader in pharmaceutical sales last year, raking in $85 billion. That's a cool 30% higher than their closest competitor, Roche (RHHBY).

But here's where it gets interesting for value hunters. JNJ's currently trading at an enterprise value of 12.8 times forward EBITDA. In English? It's reasonably priced compared to its peers.

Even better, it's trading near the bottom of its five-year range for forward P/E ratio, EV-to-EBITDA, and price-to-free cash flow. Translation: This stock's on sale, folks.

Now, I know what some of you are thinking. "But what about those talcum powder lawsuits?" Fair question.

JNJ's looking at potentially settling around $6.5 billion worth of claims. That's not a small amount, even for these guys.

But here's the kicker – they've got over $25 billion in cash on hand and generated about $19 billion in free cash flow over the last 12 months. They can take the hit and keep on ticking.

Let's talk products. Stelara, Tremfya, Darzalex, Erleada – these aren't just random drug names. They're cash cows for JNJ. And with a diverse portfolio where no single drug accounts for more than 13% of total sales, they're not putting all their eggs in one basket.

Still, I'm not saying JNJ is going to double overnight. This isn't some flashy tech stock riding the AI hype wave.

But for those of us with a long-term horizon and a love for steady income, JNJ looks mighty attractive.

Think about it – they've raised their dividend for over six decades straight. That's longer than some of you reading this have been alive.

And with a 77% payout ratio, they've got room to keep that streak going.

Sure, over the past decade, JNJ's total return of 106% might not set your hair on fire. It lags behind the S&P 500's 234% and even the Health Care Select Sector SPDR Fund ETF's (XLV) 189%.

But remember, past performance doesn't always guarantee future results.

Here's my take: JNJ isn't for the get-rich-quick crowd. It's for investors who appreciate a good night's sleep knowing their money's in a company that's weathered world wars, depressions, and yes, even lawsuits.

Will JNJ hit that trillion-dollar mark? I'd bet my last bottle of Tylenol on it. It might take a decade, but hey, good things come to those who wait.