Mad Hedge Biotech and Healthcare Letter

February 4, 2025

Fiat Lux

Featured Trade:

(TOO RICH TO FAIL, TOO EXPENSIVE TO SUCCEED)

(MRNA), (TSLA), (NVS), (SNY), (JNJ), (BNTX), (RHHBY), (REPL), (CRSP), (ORCL)

Mad Hedge Biotech and Healthcare Letter

February 4, 2025

Fiat Lux

Featured Trade:

(TOO RICH TO FAIL, TOO EXPENSIVE TO SUCCEED)

(MRNA), (TSLA), (NVS), (SNY), (JNJ), (BNTX), (RHHBY), (REPL), (CRSP), (ORCL)

Last weekend, while organizing my home office, I stumbled across an old COVID vaccination card. Remember those? It got me thinking about Moderna (MRNA), the biotech darling that went from relatively unknown to household name faster than you can say "messenger RNA."

Now, in early 2025, this once up-and-coming company is already facing what my grandmother would call "champagne problems" - too much cash to be broke, but burning through it faster than a Tesla (TSLA) on Ludicrous mode.

First, let's talk about this biotech's cash burn. In just nine months of 2024, Moderna torched through over $4 billion - that's the same amount they burned in all of 2023, suggesting their cash cremation rate is actually accelerating.

This acceleration in spending wouldn't be as worrying if they had endless reserves, but their current position shows $7 billion in cash and $2 billion in non-current investments.

The math isn't complex: at this burn rate, their runway is shorter than many investors realize.

The recent Health and Human Services (HHS) grant of $176 million in July 2024 for bird flu research barely registers on their financial statements.

While we've seen about 70 bird flu cases in the U.S. with one fatality in an elderly patient with underlying conditions, this isn't going to be another COVID-style revenue stream.

I've analyzed enough pharmaceutical companies to know that betting on another pandemic windfall is like expecting lightning to strike twice in the same spot.

What really interests me is Moderna's position in the competitive landscape. I spent last week analyzing patent data and geographic reach metrics across the industry.

First, you've got the old-guard pharma giants like Novartis (NVS), Sanofi (SNY), and Johnson & Johnson (JNJ), who have been at this game since before mRNA was a gleam in a scientist's eye.

Then, there are companies like BioNTech (BNTX) and Roche (RHHBY) with significantly higher geographic reach, while Replimune Group (REPL) and CRISPR Therapeutics (CRSP) demonstrate superior application diversity.

In comparison, Moderna's position in this landscape shows relatively low scores on both metrics - not exactly what you want to see from a company burning cash at this rate.

Stéphane Bancel, Moderna's CEO, recently outlined their pipeline: 2 approved medicines, 7 Phase 3 trials, and 45 candidates in development. They're also targeting $1.1 billion in annual R&D cost reductions by 2027.

But here's what keeps bothering me: their SG&A expenses have ballooned to nearly 10 times their pre-COVID levels, yet management is focusing on R&D cuts instead of addressing this administrative bloat.

The insider trading patterns since early 2024 haven't exactly inspired confidence either.

When I see heavy selling from insiders while a company is promising future breakthroughs, I can't help but remember all the biotech stories I've covered where the promise didn't match the reality.

Speaking of promises, Oracle's (ORCL) Larry Ellison recently made headlines talking about 48-hour personalized cancer vaccines using AI and robots.

While the technology sounds promising, I'm more interested in the practical path to profitability. Moderna isn't alone in this race, and their well-capitalized competitors have the luxury of funding similar development programs while maintaining positive cash flow.

Given Moderna's cash burn trajectory, their next three quarters will be telling.

I'll be watching that $4 billion nine-month burn rate closely, along with their progress on cost reductions - particularly those inflated SG&A expenses that management seems reluctant to address.

I'm keeping my old vaccination card as a reminder of Moderna's impressive COVID-19 achievement, but I'm not ready to bet on lightning striking twice.

Sometimes the hardest part of investing is knowing when to appreciate history without banking on its repeat performance.

Mad Hedge Biotech and Healthcare Letter

January 30, 2025

Fiat Lux

Featured Trade:

(A CRITICAL PAIN POINT)

(VRTX), (AMZN)

Last week, while having dinner with an old friend who's an emergency room physician in San Francisco, I heard a story that stopped me cold. She had just lost another patient to an opioid overdose - the fourth one that month.

"We desperately need alternatives," she said, pushing away her plate. "Something that works without killing people."

She's not wrong. More than 80,000 Americans died from opioid overdoses in 2022 alone - that's about 75% of all drug overdose deaths in the country.

To put that in perspective, that's more than double the number of people who die in car accidents each year. In New York alone, opioid-related deaths have quadrupled between 2010 and 2020.

You can see where this is going. There's a massive market opportunity here for any company that can crack the code of non-addictive pain management.

We're talking about a potential market worth tens of billions of dollars. The holy grail? A drug that works as well as opioids without the devastating addiction potential.

Enter Vertex Pharmaceuticals (VRTX) and their sodium channel inhibitor VX-548, now known as suzetrigine. The company has been quietly plugging away at this problem, and I've been watching them like a hawk.

For those who've been following my previous coverage, you'll remember I wrote about their interesting (though modest) results in post-surgical patients a few months ago.

And here's where it gets fascinating. Vertex has been running multiple trials because - as any doctor will tell you - pain isn't just pain.

It comes in more flavors than Ben & Jerry's ice cream: acute, chronic, neuropathic, cancer-related, post-surgical, and don't even get me started on phantom limb pain.

Just before the holiday break, they dropped their latest results for suzetrigine in sciatica patients.

Now, I have to tell you something that might sting a bit. The drug worked - but so did the placebo. Both groups saw their pain decrease by statistically similar amounts.

Vertex argues the placebo response was unusually high and that a larger Phase III trial should smooth things out.

Maybe they're right - but I've seen enough clinical trials to know that placebo effects in pain studies can be trickier than a Wall Street hedge fund manager.

The FDA is expected to make a decision by the end of this month on suzetrigine for moderate-to-severe acute pain.

Despite the recent speed bump in the sciatica trial, I'm still keeping my eye on the bigger picture here. Vertex isn't a one-trick pony.

Their cystic fibrosis (CF) portfolio is absolutely crushing it. They just got FDA approval for Alyftrek ahead of schedule.

They've expanded Trikafta's approval down to patients as young as two years old, which is huge for their market potential. Plus, they’ve been aggressively pushing into international markets over the past months.

Now, let's talk numbers. Suzetrigine revenue is projected to hit $5 billion by 2035. That's not chump change, even if we hit some bumps along the way.

Trading at a P/S multiple of almost 10, Vertex isn't cheap - but then again, neither was Amazon (AMZN) in 1997.

Still, this biotech’s pipeline goes beyond pain management. We're looking at treatments for diabetic peripheral neuropathy, IgA nephropathy, type 1 diabetes, and even gene editing therapy.

So, here's the bottom line: Yes, the market got spooked by the Phase II data. Yes, there are risks. But remember - the FDA is under enormous pressure to approve non-opioid painkillers.

With 80,000 Americans dying yearly from opioid overdoses, they need solutions more than my trader friends need their morning coffee.

I'll keep watching this one closely. The pain management market is like a sleeping giant, and despite the recent hiccup, Vertex might just have the alarm clock.

or long-term investors, this could be one of those "I wish I bought it back then" moments.

Watch this space. The opioid crisis isn't going anywhere, but neither is Vertex's determination to solve it.

Sometimes the biggest opportunities come disguised as disappointments.

Mad Hedge Biotech and Healthcare Letter

January 28, 2025

Fiat Lux

Featured Trade:

(READY, RESET, GO)

(JNJ), (AAPL), (PFE), (ABBV), (RHHBY), (AZN), (SNY), (NVS)

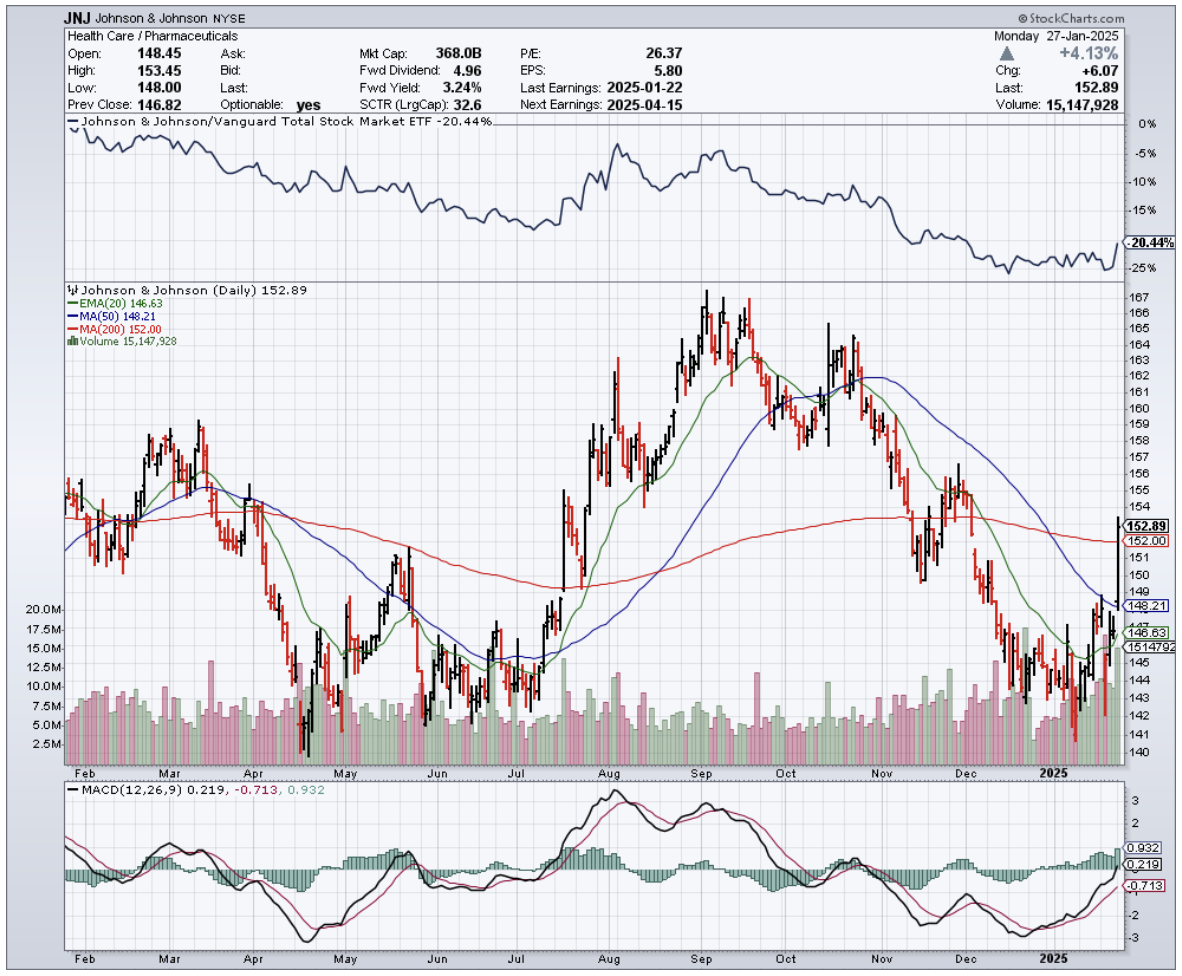

I had to laugh when I saw Johnson & Johnson's (JNJ) Q4 earnings hit my screen earlier this month.

Here we have Wall Street wringing its hands over a slight revenue miss, sending shares down 3.5%, while management is busy plotting its path to pharma industry dominance.

The numbers tell an interesting story.

Q4 revenues grew 5.3% (or 5.7% on an adjusted operational basis) to $22.5 billion. Wall Street got the vapors because earnings came in at $1.41 per share, well below their $2.04 consensus.

Reminds me of the time analysts completely missed Apple's (AAPL) transformation into a services company.

For the full year 2024, JNJ delivered 4.3% sales growth (5.4% operational) to $88.8 billion, with earnings per share landing at $5.79, or $9.98 adjusted after swallowing a $(0.67) hit from acquired IPR&D charges.

Not too shabby for a company in transition.

Looking into 2025, management is guiding for 2.5-3.5% operational sales growth ($90.9-91.7 billion) and adjusted operational EPS of $10.75-$10.95.

That's 8.7% growth at the midpoint, though they're careful to hedge around legal proceedings and acquisition costs.

And here's where it gets interesting.

During last week's JP Morgan Healthcare Conference, CEO Joaquin Duato was practically bouncing in his chair about their drug pipeline. Let's look at what's got him so excited.

Darzalex, their multiple myeloma superstar, raked in $11.67 billion in 2024, up 20%.

The new kid Carvykti exploded 93% higher to $963 million. Tecvayli landed $550 million in its rookie year.

Depression med Spravato jumped 56% to hit the magic $1 billion mark. Tremfya, their Stelara successor, grew 17% to $3.7 billion.

Speaking of Stelara – there's the elephant in the room.

JNJ's crown jewel is losing patent protection, already showing up in Europe with a >12% sequential decline in Q4 to $2.35 billion. Expect a 30% "haircut" this year.

But here's what Wall Street is missing: JNJ saw this coming years ago.

They just dropped $14.6 billion on Intracellular Therapies, mostly debt-funded (they can afford it with only $31.3 billion in long-term debt and $19.98 billion in cash).

This brings them Caplyta, an antipsychotic med with blockbuster potential that's already approved for schizophrenia and bipolar disorders.

The medical device business isn't sitting still either.

Q4 worldwide revenues jumped 6.7% year-on-year. While Surgery was flat at $2.5 billion and Orthopedics grew a modest 2.5% to $2.32 billion, Vision popped 9% to $1.3 billion.

But the real story? Cardiovascular surged 24% to $2.1 billion. Those Shockwave and Abiomed acquisitions are looking pretty smart right about now.

For the year, MedTech grew 4% to $31.56 billion. Operating margins slipped a bit – Innovative Medicines down from 42% to 39.4%, MedTech from 23.7% to 21.6%.

Late-stage pipeline products nearing approval should ease R&D expenses in 2025, just as JNJ gears up for its next growth phase.

The foundation looks rock solid - $19.98 billion in cash, $31.3 billion in long-term debt, 2025 adjusted EPS guidance of $10.75-$10.95, and that reliable $1.24 quarterly dividend.

But forget the current numbers - the real money's in what's coming next.

Here's what the market is missing: JNJ is promising 5-7% compound annual growth between 2025-2030, with ten drugs hitting $5+ billion in annual sales by decade's end.

Sound ambitious? Maybe. But they've got the pipeline to back it up – from immunology stars nipocalimab and icotrokinra to neuroscience contenders seltorexant and aticaprant, plus oncology plays like TAR-200 for bladder cancer.

I've seen this movie before with AbbVie (ABBV), which navigated the loss of $20+ billion Humira without missing a beat.

And JNJ looks even better positioned - their pharma division is targeting $58 billion in 2024 revenues, which would make them the biggest player in Big Pharma, ahead of Pfizer (PFE), AbbVie (ABBV), Roche (RHHBY), AstraZeneca (AZN), Sanofi (SNY) and Novartis (NVS).

The only real wildcard? That pesky talc litigation.

JNJ's latest move – spinning the lawsuits into Red River Talc LLC and filing for bankruptcy – could cap the damage at $8.5 billion. They claim 75% of claimants are on board, with a court ruling expected this month.

So, what's my take? I think JNJ's 2025 will be a "reset" year, especially the first half. But just like buying straw hats in winter, there might be an opportunity here for patient investors. Management says the back half will be stronger, setting up 2026 for what could be a very interesting guidance call.

While the market frets about Stelara's patent cliff, smart money is quietly building positions. That's why I'm maintaining my stand to buy the dip.

After all, sometimes the best trades are the ones that make you a bit uncomfortable at first. And if you're worried about patent cliffs, just ask any AbbVie shareholder how that worked out for them.

Mad Hedge Biotech and Healthcare Letter

January 23, 2025

Fiat Lux

Featured Trade:

(THE HARD TRUTH ABOUT THIS BIOTECH'S PIPELINE THAT WALL STREET DOESN'T GET)

(MRK), (AMGN), (AAPL)

Earlier this month, while reviewing my biotech holdings during a layover at Chicago O'Hare, I got an interesting call from a long-time reader.

He was panicking about Merck (MRK) after seeing it trading near its 52-week lows, convinced the pharmaceutical giant was headed for trouble.

"Have you seen what Medicare negotiations did to Januvia?" he asked, referencing the 79% price reduction. "And Keytruda's patent expires in 2028!"

Here's the hard truth about this biotech's pipeline that Wall Street doesn't get: while everyone's fixated on Keytruda's patent cliff, Merck has quietly tripled their late-stage pipeline in just over three years.

We're talking more than 20 unique assets in late-stage development, plus another 50 in early stages.

The last time I saw this kind of pipeline expansion was during the early days of Amgen (AMGN), which turned out pretty well for investors who saw past the obvious.

Actually, Merck's current "crisis" also reminds me of the time I bought Apple (AAPL) right after Steve Jobs announced the iPhone. Everyone worried about the risk, while I saw the opportunity.

Merck just posted Q3 2024 numbers that would make most CEOs envious: revenue up 7% year-over-year to $16.7 billion.

Keytruda, their cancer blockbuster, grew 21% to $7.4 billion. Even their Animal Health division jumped 11%. These aren't the numbers of a company in trouble.

Speaking of investors, they've enjoyed a 126% total return over the past decade with Merck, despite more ups and downs than my last flight through turbulence.

The company's 5-year average Return on Equity sits at 25% (recently climbing to 28%), with Return on Invested Capital steady at 20%.

With a Weighted Average Cost of Capital around 8%, there's plenty of room for growth.

Yesterday, I was discussing these numbers with a former FDA commissioner (who shall remain nameless) over coffee.

He pointed out something fascinating: Merck's R&D spending is increasing alongside revenue growth. That's like a tech company doubling down on product development – exactly what you want to see in pharma.

For dividend hunters (and I know many of you are), Merck offers a 3.3% yield with a 7% five-year dividend growth rate.

The payout looks sustainable too, consuming 68% of earnings and 55% of free cash flow. It's not going to make you quit your day job, but it's better than the 1.4% you'll get from the S&P 500.

Looking at valuation, Merck trades at a P/E of 20.5, below its historical average of 22.3.

My own growth projections suggest a 13% annual rate going forward. Optimistic? Perhaps. But with their robust pipeline and near-term analyst projections, I've seen crazier things work out.

The company just announced a $15 billion share repurchase program, including plans to spend $7.5 billion over the next 12 months. When management puts that kind of money where their mouth is, I tend to pay attention.

Yes, Keytruda's patent cliff in 2028 is real. But so is Merck's late-stage pipeline of antibody-drug conjugates (ADCs) – think smart missiles in the war against cancer.

And unlike some biotechs, Merck has the financial muscle to weather any storm, with decreasing net debt and a solid cash position.

Remember what I always say about buying straw hats in winter? Merck right now is like finding a premium pharma stock in the discount bin.

Just like my friend who panicked and sold everything after the November 8 election (and missed the subsequent rally), sometimes the best opportunities come disguised as problems.

As for me, I'm looking at Merck as a potential long-term hold. The company's fundamentals remind me of other great turnaround stories I've traded successfully over the years.

With the healthcare sector currently out of favor and Merck trading near its 52-week lows, this might be one of those moments we look back on and wish we'd bought more.

And speaking of patents, maybe I should patent my strategy: “Buy great companies when everyone else is afraid.” Though I suspect Warren Buffett already beat me to that one.

Mad Hedge Biotech and Healthcare Letter

January 21, 2025

Fiat Lux

Featured Trade:

(THE ONLY TIME FIGHTING YOURSELF MAKES MONEY)

(ABBV), (AMGN), (SDZNY), (CHRS), (PFE), (JNJ), (ALVO), (TEVA), (SNY), (BMY)

If I had a dollar for every time someone told me the biotech sector was overvalued, I'd have enough to fund my own drug development program.

Yet here we are, watching the global immunology market rocket from $55 billion to $166 billion in just a decade, with the sector projected to hit $192 billion by 2028.

If you're wondering why big pharma keeps pouring billions into autoimmune research - and believe me, this question came up in every meeting last week - the answer is simple: we've barely scratched the surface.

Despite thousands of PhDs burning midnight oil in labs from Boston to Basel, we still don't have effective treatments for systemic lupus erythematosus, scleroderma, or even something as visible as vitiligo.

Want to see where the smart money is going? Look no further than the biosimilar stampede into AbbVie's (ABBV) Humira territory.

Like bargain hunters at a Black Friday sale, everyone's getting in line: Amgen (AMGN) with Amjevita, Sandoz (SDZNY) with Hyrimoz, Coherus (CHRS) with Yusimry, and Pfizer (PFE) with Abrilada.

And just when you thought the party was over, here comes Amgen's Wezlana challenging Johnson & Johnson's (JNJ) Stelara, followed by Alvotech (ALVO) and Teva's (TEVA) Selarsdi.

But here's where it gets interesting. I've identified four companies that are trading at valuations that would make Benjamin Graham smile.

First up is AbbVie, trading at 15.96x earnings (11.9% below sector median), with projected EPS growth to $15.21 by 2027.

Their dynamic duo of Rinvoq and Skyrizi is performing like a biotech version of Batman and Robin.

Rinvoq sales hit $1.61 billion in Q3 2024, up 45.4% year-over-year, while Skyrizi broke $3 billion, thanks to its mid-2024 FDA approval for ulcerative colitis.

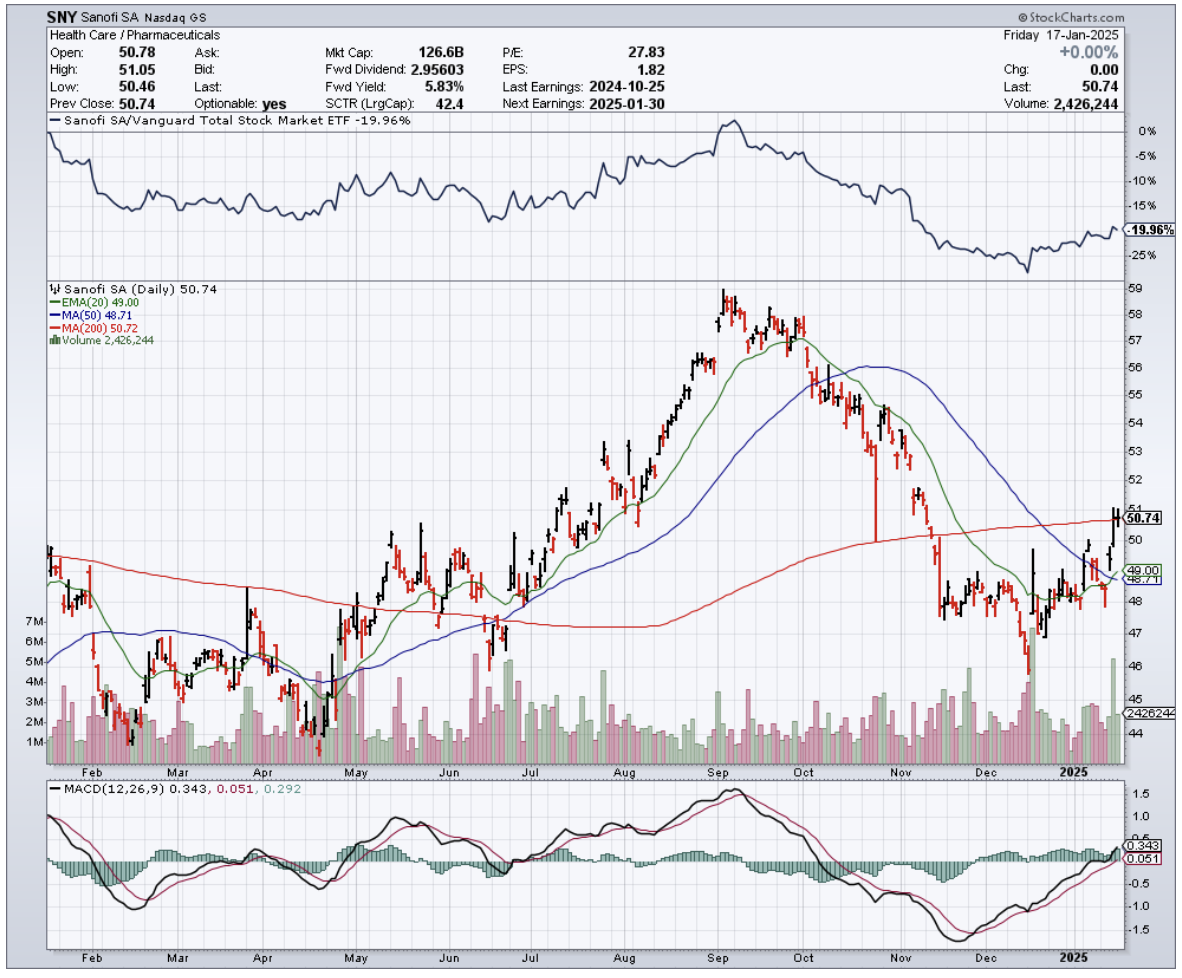

As for Sanofi (SNY)? Now we're talking value. At 11.7x earnings - 35.39% below sector median and 1.3% below its 5-year average - it's like finding a Ferrari priced like a Fiat.

Their star player Dupixent raked in 3.48 billion euros in Q3 2024, up 22.1% year-over-year and 5.2% quarter-over-quarter.

Then, there’s Teva Pharmaceuticals. Trading at a P/E ratio of 7.88x - that's 56.5% below the sector median - while projecting non-GAAP EPS growth to $3.6 by 2028.

But here's the kicker: their clinical trial data reads like a biotech investor's dream. Their new drug duvakitug achieved 47.8% clinical remission in ulcerative colitis patients versus 20.45% for placebo (p=0.003).

In Crohn's disease? Even better - 47.8% endoscopic response compared to 13% for placebo (p<0.001).

Finally, there's Bristol-Myers Squibb (BMY). Yes, it's trading at 47.5x earnings (162.1% above sector median), but here's where patience pays off - their P/E ratio is expected to drop to 8.82x by 2027.

Meanwhile, Zeposia sales jumped 19.5% year-over-year to $147 million in Q3 2024, while Sotyktu showed consecutive quarterly growth.

The cherry on top? These companies are paying you to wait. We're talking dividend yields from 3.8% to 4.41% - try getting that from your savings account.

Looking at these numbers reminds me of the tech sector in the late 1990s, but with one crucial difference - these companies are actually making money, lots of it.

They generate significant cash flow and have strong balance sheets, unlike many of the high-flying tech companies of the dot-com era that were burning through cash with no clear path to profitability.

While others are chasing the next meme stock or crypto moonshot, smart investors are quietly positioning themselves in companies that are literally changing the face of medicine.

Remember, buying umbrellas in the summer heat has always been my style.

Right now, the immunology sector is experiencing its own kind of summer, and these four stocks are your umbrellas.

The forecast? Growth storms ahead.