I am pleased to announce the launch of the Mad Hedge Biotech & Healthcare Trade Alert Service.

The goal is to alert traders and investors when entry sweet spots occur for Biotech & Healthcare stocks with the strongest long-term fundamentals.

Don’t expect any immediate trade alerts today, tomorrow, this week, or even this month. Actual market sweet spots are rare and only take place after prolonged bottoming processes. However, they DO make it easier for investors to move into the best companies at the right time and achieve immediate profits.

Each alert will include recommendations for the stock, options, and ETF so you can tailor the position to your own level of experience and risk tolerance.

In order to receive Biotech text alerts, we need your cell phone number to get text messages to you immediately. To register, please click here.

I look forward to working with you with this service.

John Thomas

CEO & Publisher

The Mad Hedge Biotech & Healthcare Letter

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-05 10:02:082021-01-05 10:55:22Announcing the Mad Hedge Biotech & Healthcare Trade Alert Service

The latest update on AstraZeneca’s (AZN) COVID-19 vaccine candidate has received a lot of attention from investors.

The company and its research partner Oxford University recently landed a deal to deliver 2 million doses of their COVID-19 vaccine weekly to the UK starting mid-January.

This is on top of the massive deal AstraZeneca sealed with India for emergency use approval as well.

While these are exciting updates, the reality is that AstraZeneca aims to market its COVID-19 vaccine candidate at cost.

As the race to supply COVID-19 vaccine to the world continues, it’s undeniable that a huge chunk of the roughly $40 billion COVID-19 revenue would go to the current frontrunners Pfizer (PFE) and Moderna (MRNA).

This is particularly true for Moderna’s case as the biotechnology company employed a revolutionary technology to create its COVID-19 vaccine candidate.

The success of its vaccine so far is indicative of future treatments and even vaccines based on the mRNA technology. This offers incredible promise not only for the current pandemic but for a myriad of rare diseases.

In comparison, AstraZeneca and even Johnson & Johnson (JNJ) opted for more traditional approaches for their COVID-19 vaccine candidates.

While these are also promising, it’s likely that these companies do not anticipate their COVID-19 programs to be the profit centers for 2021.

In fact, there are a lot of good reasons to buy AstraZeneca shares right now – and its COVID-19 vaccine candidate didn’t make the top of the list.

One of the main reasons AstraZeneca deserves a spot in your portfolio is the fact that it already has an established and successful pipeline.

While its COVID-19 program definitely boosted its popularity, this effort was not altogether necessary in terms of the company’s overall growth.

Despite the pandemic that brought down businesses in 2020, including commercial launches of new drugs, sales of AstraZeneca’s new products rose 9% year over year.

In fact, throughout the past 12 months, the company managed to generate approximately $1.9 billion in free cash flow.

In the first nine months of 2020, the company reported core earnings growth of 13% year over year, with a 2.8% dividend.

To close the year with a bang, AstraZeneca announced its $39 billion acquisition of one of our closely-watched biotechnology companies: Alexion Pharmaceuticals (ALXN).

Although this initially didn’t bode well with its investors, AstraZeneca is set to gain the blockbuster franchise composed of the Soliris-Ultomiris duo.

At its current growth rate, Alexion’s prized Soliris franchise is estimated to generate at least $6 billion in sales in 2021.

Meanwhile, Soliris’ longer-lasting version, Ultomiris, which was launched in 2018, is projected to rake in almost twice in profits this year.

Both Soliris and Ultomiris require regular treatment, with the former administered every other week while the latter is an infusion needed every other month.

Although there are less expensive biosimilar options already making the in the market today, particularly for Soliris, the move of Alexion to develop Ultomiris as a longer-lasting and more convenient version all but obliterates any future competition.

Simply put, AstraZeneca will have a monopoly of this market once the acquisition is complete by mid-2021.

Speaking of convenient options for prolonged treatments, AstraZeneca recently gained expanded approval for its easy-to-swallow tablet called Tagrisso. This drug is developed for lung cancer patients with tumors caused by specific gene mutations.

The latest approval allows Tagrisso to be prescribed to newly diagnosed patients who just had their tumors removed surgically.

This presents a lucrative market for AstraZeneca considering that these patients undergo therapy for long periods.

More importantly, AstraZeneca doesn’t really need to market Tagrisso’s value to oncologists.

Clinical results show that the tablet can lower the risk of the disease’s recurrence or even death by as much as 80% among their patients.

Putting these results in the context of AstraZeneca’s records, Tagrisso’s sales for the third quarter of 2020 alone grew by 30% year over year to reach $4.6 billion.

With the recent FDA approval, this number is set to increase to transform Tagrisso into a certified blockbuster drug.

Other than Tagrisso, AstraZeneca has a number of oncology blockbusters in its portfolio and pipeline.

In the first nine months of 2020, the sales of the company’s therapies unit rose by 23% year over year to a record $8.2 billion. Admittedly, Tagrisso contributed a substantial amount.

However, it’s not the sole growth driver in AstraZeneca’s oncology lineup.

Another moneymaker is Lynparza, which showed a 42% jump year over year in its third quarter sales in 2020 to reach $1.9 billion.

This drug, which was initially approved as an ovarian cancer treatment, is now prescribed to treat prostate, pancreatic, and breast cancer. Therefore, the expanded approvals are expected to offer more lift this year.

Another promising addition to AstraZeneca’s oncology pipeline is Enhertu, which the company gained from its $1.35 billion collaboration project with Daiichi Sankyo.

Since the two companies started working together last year, Enhertu has received approval for breast cancer patients who relapse or do not respond to standard care.

Aside from this, Enhertu is also under review as a treatment for stomach cancer.

Although the companies are still awaiting approval, the treatment is reported to have a great chance at approval because of its impressive ability to lower the risk of cancer patients’ death by 41% compared to chemotherapy.

AstraZeneca’s decision to boost its oncology segment by adding the likes of Alexion Pharmaceuticals and collaborating with Daiichi Sankyo guarantees that the company remains in a position to be able to deliver gains no matter what happens to the broader economy.

The continuous success for all the products in AstraZeneca’s pipeline could lead to market-crushing gains.

However, investors who own the stock don’t necessarily need to rely on luck to know that they are set to get a healthy return.

That assurance makes AstraZeneca a great stock to buy today and hold for a long time.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-01-05 10:00:032021-01-10 00:15:56Why AstraZeneca Is Not Just A COVID Play

No other industry has ever been watched as closely in 2020 as the healthcare and biotechnology sector, with drug developers placed under pressure to deliver COVID-19 treatments and vaccines within an unprecedented timeframe.

Despite all the attention and fanfare, the overall performance of the sector’s stocks remained underwhelming. However, 2021 promises to bring in better returns and bring back the industry to pre-pandemic performance.

For perspective, the S&P 500 Health Care Sector Index rose by 8% through mid-December compared to the 13% increase of the S&P 500.

The financial and health crises affected the performance of the subgroups in different ways. For example, the diagnostics subgroup jumped by 31% while the demand for clinical labs was up 18%.

Meanwhile, biotechnology stocks rose by 13%. In comparison, traditional pharmaceutical stocks and even hospitals only managed to record a measly 3% increase.

As for retail pharmacies, this subgroup sank by 18%.

Despite the underperformance of the industry, there are still companies that stood out this year and are poised to soar come 2021.

One of them is Vertex Pharmaceuticals (VRTX).

Vertex is possibly one of the most undervalued large-cap biotechnology stocks in the market today.

This company, which has $61.7 billion in market capitalization, has been continuously growing and transforming into the most dominant player in the cystic fibrosis (CF) space.

Truth be told, Vertex holds the monopoly on the approved drugs used to treat CF, namely, Trikafta, Kalydeco, Orkambi, and Symdeko.

With the recent approvals the company received, this momentum is expected to grow.

Vertex just won additional EU approval for its CF drug Kaftrio. This indicates another cash cow for the company as the drug, also known as Trikafta, already transformed itself into a megablockbuster in the US market.

Apart from its efforts to continuously dominate the CF sector, Vertex also has several moonshots that can eventually turn into major catalysts.

Among those is its partnership with CRISPR Therapeutics (CRSP).

The two biotechnology companies are developing a gene therapy, called CTX001, which can cure rare genetic blood diseases. Specifically, CTX001 is designed to cure beta-thalassemia and sickle cell disease.

Apart from its partnership with CRISPR Therapeutics, Vertex also acquired Semma Therapeutics in 2019 with the goal of coming up with a cure for Type 1 diabetes.

If things go as planned, a gene therapy for this genetic disease will advance to clinical testing by early 2021.

Another under the radar biotechnology stock set to soar in 2020 is Illumina (ILMN).

Illumina, with a market capitalization of $54.10 billion, is the leader in the genomics market.

Since the pandemic broke, the biotechnology sector’s leading manufacturer of hardware for genetic sequencing has been supplying testing kits for hospitals across the US.

Apart from Illumina, other companies in the genomics sectors include Vertex’s partner, CRISPR Therapeutics, which has a market capitalization of $4.48 billion, and bluebird bio (BLUE) with $4.03 billion.

In a nutshell, genomics refers to the analysis of the genetic information found in human cells. Companies working on this field aim to not only develop more accurate and efficient disease testing processes but also come up with more personalized treatments for a range of diseases including cancer.

Looking at Illumina’s profile and even taking into consideration the effects of the recession along with the competitive pressure to be expected soon enough, this biotechnology company is still set to deliver solid returns over the next 3 to 5 years.

Ever since its establishment, Illumina has been hailed as the leader in the gene-sequencing segment.

To date, the company holds almost 90% of the market.

Apart from that, the company has been an active participant in the move to lower the costs of gene-sequencing processes. In effect, Illumina managed to expand its customer reach.

Illumina’s participation in the 13-year Human Genome Project, which started at $3 billion per genome submitted for sequencing in 2003.

Nowadays, the cost has dropped to $800 for each genome, with Illumina eyeing to drop the price to $100 via its NovaSeq platform.

Based on the company’s performance in the past years, Illumina’s revenue is expected to climb higher annually in the next 5 years.

By 2021, the company is projected to report a 21.16% year over year growth in annual revenue to reach 4.23 billion.

Meanwhile, its 2022 annual revenue is estimated to hit $4.79 billion, showing off a 13.37% increase.

Despite the attention it has been receiving, Illumina remains a bargain buy.

This is because the company’s gene-sequencing projects have been moving along at a decent pace even before the COVID-19 crisis hit.

Given the company’s growth and future plans, Illumina is a no-brainer long-term investment. However, investors looking for quick returns might find the company’s pace a bit sluggish for their liking.

Among the biotechnology companies out there today, I think Vertex and Illumina stand out the most because both hold a monopoly in their respective fields.

Sure, there would be competition eventually but the combination of all their strengths and the strong potential of their pipeline put them in a league of their own.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-31 12:00:542021-01-05 00:39:50Monopoly is the Name of the Game

Over the past month, COVID-19 vaccine developers like Pfizer (PFE), Moderna (MRNA), and AstraZeneca (AZN) have offered the world a bit of good news.

For the first time since the pandemic started, we have seen a light at the end of this crisis’ tunnel.

This time around next year, the economy should be close to its normal state.

Before we see the struggling financial market completely recover, you might want to consider buying shares of an under-the-radar COVID-19 vaccine developer that could be on its way to performing better in 2021: Merck (MRK).

Major healthcare and drug stocks rarely get this cheap relative to the S&P 500 in the last 15 years, Merck is a prime example of this once-in-a-blue-moon phenomenon.

Although it was slow to start and report on updates in its COVID-19 vaccine, Merck has been making strides in emerging as a major competitor against Gilead Sciences (GILD) when it comes to developing a COVID-19 drug.

To date, Merck landed a $356 million supply agreement with the US government to deliver 60,000 to 100,000 doses of its oral antiviral drug for COVID-19.

While vaccines are definitely valuable in helping prevent the spread of the virus, there is another important market that healthcare companies are targeting: the hospitalized COVID-19 patients.

With this recent announcement from Merck, it’s obvious that the company has its hands on both the vaccine market and the hospitalized patient group.

In terms of vaccine development, Merck may be behind Pfizer and Moderna but this New Jersey-based titan has one of the leading vaccine franchises in the industry.

The frontrunner in Merck’s vaccine franchise is its cervical cancer vaccine Gardasil, which is estimated to be worth half of its current market value of approximately $200 billion.

The company is also anticipated to record high single-digit earnings growth in the years to come, thanks to the 2021 spinoff of its Organon unit.

Following Pfizer and Mylan footsteps in the newly formed Viatris (VTRS), Organon will be used to unload the slower-growth products from Merck’s current portfolio.

With the purging of its product portfolio of the low-performing treatments comes the expansion of Merck’s R&D courtesy of its $2.75 acquisition of biotechnology startup VelosBio.

Thanks to this deal, Merck will gain access to VelosBio’s prized VLS-101, which is basically a miniature chemotherapy grenade that would disintegrate cancer cells.

This collaboration could turn out into another moneymaker for the company.

Merck is no stranger when it comes to picking winning oncology investments.

The last massive deal it completed was a $1.16 billion deal with AstraZeneca in 2017, with the two companies agreeing to milestone payments of up to $6.15 billion.

This partnership brought to life one of the highest-selling cancer drugs in the world today, Lynparza.

To date, Lynparza is not only used for prostate cancer but also gained expanded approval for breast and pancreatic cancer.

In the third quarter of 2020 alone, even with the pandemic still wreaking havoc everywhere, Merck’s share of profits for Lynparza jumped 59% year over year to reach $196 million—a number that is projected to continue to climb as the drug awaits more approvals from the EU.

Merck offers the most attractive upside case among the healthcare stocks today, with the company projected to report consistent revenue growth until at least 2025.

Moreover, this pharmaceutical company has a strong balance sheet, as seen in its recent acquisitions and potential partnerships still underway.

So far, Merck’s shares are down 12% this year to only $80, with the stock trading 13 times its projected earnings in 2021 at $6.29 per share.

This pharmaceutical giant has a stable dividend yield of 3.3%, which is double the S&P 500.

As the economy continues with its recovery, you can expect Merck to get stronger and the stock should rally sooner rather than later.

Hence, buying it before it completely bounces back could allow you to cash in some spectacular returns.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-29 11:00:432021-01-02 20:01:13Buy Before the Rally

Erratic. Unpredictable. Volatile. Take your pick of the descriptions used when it comes to biotechnology stocks. Each of these adjectives can be a fitting descriptor to the industry most of the time.

However, not all biotechnology companies fall under that category. Some are reasonably stable, offering steady and increasing profits.

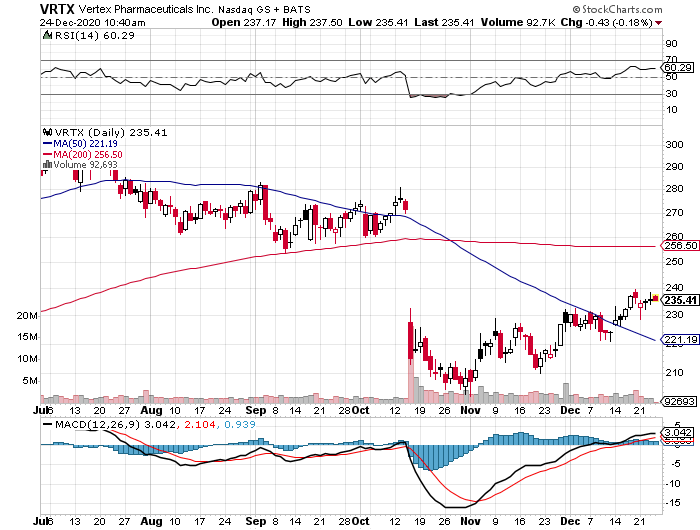

Vertex Pharmaceuticals (VRTX) is one of those biotechnology stocks that you can simply buy and hold for over a decade without losing any sleep.

One of the key factors in Vertex’s success is its monopoly on the cystic fibrosis (CF) market.

CF is a rare and life-threatening genetic disease that affects a patient’s digestive system and lungs. To date, there is no cure for this condition that overshadows the lives of 68,000 individuals in the US and the EU. However, there are treatment options for it.

Vertex developed the first-ever FDA-approved drug, Kalydeco, for the condition. As expected, it gained the much-coveted head start that led to its dominance today.

Its closest rivals, Proteostasis Therapeutics (PTI) and Galapagos NV (GLPG), are years away from ever catching up to the Massachusetts-based biotechnology stalwart. Neither has an approved drug as of today.

Since the approval of Kalydeco in 2012, Vertex stock has been enjoying an upward trajectory. With the recent addition of another CF blockbuster, Trikafta, the company is anticipated to keep its momentum.

From the moment Trikafta was released to the market, Vertex’s revenue and bottom line showed impressive growth. The drug, which is a triple combination therapy, is projected to capture almost 90% of the CF market worldwide.

Needless to say, Vertex has made it in the shade for at least the next 5 years, thanks to its CF market dominance.

In its second quarter earnings report, Vertex showed a 62% jump in its revenue year over year to hit $1.52 billion. Its net income of $837 million demonstrated a whopping 213% increase compared to the same period in 2019.

As anticipated, the star of the show was Trikafta.

The drug raked in $918 million in the second quarter alone – an amount higher than the combined sales of all the drugs in Vertex’s product line and an impressive growth from the $420 million it contributed last year.

As Vertex’s bottom line grew, its margins showed substantial improvement as well. Its operating margin for the second quarter of 2020 is at 57% compared to 44% during the same quarter last year.

With Vertex’s key metrics topping expectations, the company changed its 2020 revenue guidance from $5.7 billion to $5.9 billion, showing off a noteworthy increase from the $4 billion in sales it reported in 2019.

Although its CF pipeline has a number of promising candidates, Vertex is also looking outside the market for additional avenues of growth.

One of the most promising and exciting partnerships it forged in the past decade is with gene-editing company CRISPR Therapeutics (CRSP).

Just looking at this collaboration makes it clear that Vertex is once again playing the long game.

What we know so far is that the two companies are working on a treatment, called CTX001, for rare genetic blood disorders sickle cell disease and transfusion-dependent beta-thalassemia.

They are also developing two potential treatments for alpha-1 antitrypsin deficiency (AATD), which is a rare genetic liver and lung disorder that is similar to CF.

Detractors might point out that Vertex is a pricey stock. However, this biotechnology company currently has $71.2 billion in market capitalization.

More notably, it has no debt and holds $5.5 billion in cash. That puts the true value of Vertex at roughly $65.7 billion.

I believe that the biotechnology company’s overall outlook more than does justice for its valuation.

Granted that it is trading at 11 times its revenue and 26 times its adjusted EPS, its consistent performance and promising future ensure that its investors will be getting more bang for their buck.

In a word, Vertex remains a first-rate biotechnology stock to buy.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-24 11:00:592020-12-24 10:41:14How Vertex is Curing the Uncurable

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

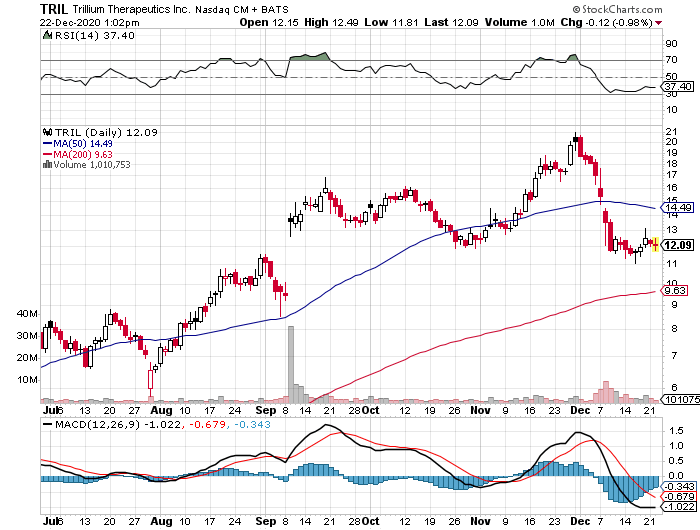

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-12-22 13:00:442020-12-23 17:22:33The Most Famous Cancer Stock You’ve Never Heard of

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.