Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

It is not at all surprising that the biggest names in the healthcare industry are dominating the COVID-19 vaccine race.

After all, Big Pharmas such as Pfizer (PFE), AstraZeneca (AZN), Johnson & Johnson (JNJ), and Sanofi (SNY) are backed with vast resources that even media favorites like Moderna (MRNA) find challenging to compete against.

For months now though, going head to head with these big-name frontrunners is a clear outlier: Novavax (NVAX).

So far, there are only 10 COVID-19 vaccine candidates that have reached late-stage testing and Novavax’s NVX-CoV2373 has been performing at par (if not better) than its rivals—and the market has definitely noticed.

When 2020 started, Novavax’s market capitalization was less than $130 million and traded at roughly $4 per share.

Ten months into the pandemic, this small biotechnology company’s market cap grew to over $6.5 billion and has been trading at $110 per share—and that is already after a price decrease in the past weeks.

Given the disparity in its size and resources compared to its competitors, it’s safe to say that Novavax has been punching way above its weight class particularly in terms of landing supply agreements for its COVID-19 program.

Novavax first received a CEPI grant in March worth $4 million, which was immediately dwarfed by the $384 million the biotech company got in May.

In a matter of months, Novavax joined the major league players and secured a $1.6 billion funding courtesy of the US government’s Operation Warp Speed program.

In exchange, the biotech company will supply 100 million doses of NVX-CoV2373 to the US upon approval.

Novavax also inked an agreement with the UK for 60 million doses and another with Canada for 76 million doses.

Novavax has also landed deals with Japan through Takeda Pharmaceutical (TAK) and India via the Serum Institute of India.

As expected, the grants and supply agreements were perceived as votes of confidence on Novavax’s work and the company reaped the rewards.

In March, the prices started moving from less than $10 per share to almost $50.

By May, the price moved up to roughly $80 per share.

After its Operation Warp Speed contract in July, Novavax’s price per share soared all the way to $189 before eventually falling to $110 this October.

Novavax has only conducted late-stage testing in the UK. But, Phase 3 is expected to begin in the US soon as well.

Admittedly, a lot is riding on NVX-CoV2373.

However, the company has actually offloaded the majority—if not all—of its financial risks linked to the program.

Riding the momentum of its COVID-19 vaccine candidate, Novavax has been working on a related influenza vaccine called Nanoflu.

Given the market size for this, Nanoflu is estimated to rake in an annual revenue somewhere between $550 million and $1.7 billion.

Another potential blockbuster is respiratory syncytial virus (RSV) vaccine ResVax, which is projected to reach peak sales of $2 billion.

Novavax is also working on a vaccine candidate for the Ebola virus, the Middle East Respiratory Syndrome (MERS-CoV), and Severe Acute Respiratory Syndrome (SARS).

While NVX-CoV2373 is anticipated as Novavax’s moneymaker in the coming years, the biotech company can only realistically expect massive sales from this until 2023.

Looking at the company’s manufacturing partnerships and the aggressive timeline it has taken, Novavax is expected to produce 2 billion doses of its COVID-19 vaccine by mid-2021.

This is great news for its investors because of Novavax’s smaller market capitalization compared to its competitors.

Since the biotech company is projected as one of the first companies—if not the first—to offer a vaccine, then it can cover a substantial market share before its bigger rivals take over the market.

Even if Novavax prices its COVID-19 vaccine cheaply, say, $10 per dose, it can still generate $20 billion in annual sales.

Moreover, the late-stage success of NVX-CoV2373 will definitely cause Novavax’s stock price to skyrocket.

Despite this potential though, it’s important to keep in mind that this biotech company still has a way lower market cap than its rivals.

That means its share price will move a lot higher compared to the stocks of the other vaccine leaders.

Therefore, Novavax’s small size is not a negative for its investors—it is actually an advantage.

So for biotech investors who are searching for a promising COVID-19 vaccine stock, there’s nothing cheaper and more promising than Novavax.

Mad Hedge Biotech & Healthcare Letter

October 20, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

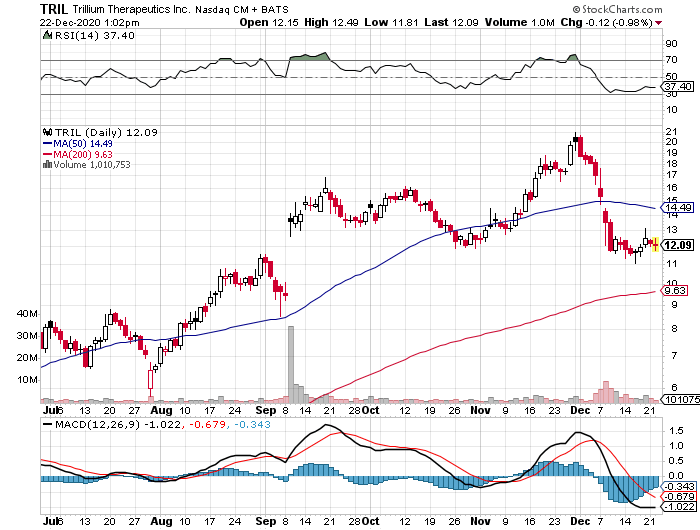

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

October 15, 2020

Fiat Lux

FEATURED TRADE:

(KEEP AN EYE OUT ON THE SLOWER RUNNERS IN THE COVID-19 VACCINE RACE)

(SNY), (GSK), (MRNA), (FPE), (AZN), (PRNB)

Under normal circumstances, it would be unheard of for a biotechnology or pharmaceutical company to begin the construction of manufacturing facilities for any drug that has not gained approval from the US Food and Drug Administration (FDA).

However, the year 2020 has been anything but “normal.”

In fact, the US government has already released billions of dollars to companies working to create a COVID-19 vaccine well ahead of their candidates’ approvals by the FDA.

While we have yet to determine which vaccine candidates would work, the amount of money pouring into these programs give us a very real sense of the size of the vaccine market.

Among the companies working on a vaccine, Sanofi (SNY) and GlaxoSmithKline (GSK) emerged as early favorites.

Even without any candidate in late-stage trials, the two drug makers landed a $2.1 billion deal with the US government for their COVID-19 vaccine candidate in July.

This will cover 100 million doses initially, which would put the vaccine cost at $21 per dose.

If all goes well, the US government has the option to buy an additional 500 million doses of the Sanofi-GSK vaccine. The two companies are also negotiating terms with other countries particularly in Europe and Asia.

Sanofi is the lead partner in this program, with the company producing the COVID-19 vaccine itself. As for GSK, it will be adding an adjuvant which would boost the immune response.

Initial data from this study is expected to be released by December 2020, with the duo hoping to receive regulatory approval not later than June 2021.

The goal is to manufacture up to 1 billion doses annually from the time of its approval in 2021.

One of the reasons Sanofi and GSK candidate attracted attention despite the companies’ less aggressive timeline compared to competitors, like Moderna (MRNA), Pfizer (PFE), and AstraZeneca (AZN), is that it uses a protein-based technique already used in their flu vaccine called Flublok.

Using a tried and tested technology affords COVID-19 vaccine investors a safety net in case the newer and untested technologies of Moderna and Pfizer stumbles. For context, Flublok was approved by the FDA in 2013.

Aside from its COVID-19 vaccine program with GSK, Sanofi is working on a separate candidate with Massachusetts-based company Translate Bio.

This candidate, which uses mRNA technology, is expected to start human trials by November.

If all works out, Sanofi and Translate Bio estimate that they can produce 90 million to 360 million doses of this two-dose COVID-19 candidate in 2021.

Sanofi is no stranger to the vaccine market. In 2019, the company enjoyed a 4.8% year-over-year jump in its net sales and over 9% increase in the sales of its vaccines.

While Sanofi’s net sales slid by 4.9% in the first six months of 2020, the company still reported a healthy 9.2% growth in its earnings per share in the same period.

Thanks to its top-selling eczema drug Dupixent, the company’s specialty care segment rose by more than 17%.

In fact, the drug generated over $1 billion in sales in the first half of the year—a stunning 70% jump from its 2019 performance.

Riding this momentum, Sanofi has been aggressively adding new approvals for Dupixent and expanding its reach not only in the US but also in China.

Speaking of expansion, Sanofi recently completed a $3.7 billion acquisition of Principia Biopharma (PRNB) in August. This deal is a strong indicator that the company aims to focus more on its cancer and autoimmune sectors.

This also marks the second major acquisition of Sanofi in less than a year, with the company striking a $2.5 billion deal to acquire another cancer-focused biotechnology company Synthorx last December 2019.

Looking at the timeline of Sanofi compared to its competitor reminds me of the classic Aesop story, “The Hare and the Tortoise.”

However, the race for a COVID-19 vaccine is definitely not a winner-take-all scenario.

Sanofi and its partner GSK may look far behind the frontrunners, but these mega-companies have such extensive experience in developing and testing vaccines that they could easily close the gap in the next few months.

A successful COVID-19 vaccine would definitely be a gamechanger for Sanofi’s pipeline. The competition is stacked – several other resource-rich companies are also working on similar programs – and Sanofi’s candidates are nowhere near the finish line.

If Sanofi’s COVID-19 vaccine candidate is effective, however, there is really no good reason why it cannot snatch a piece of the pie.

Sanofi stock has not experienced any massive gains or losses since the pandemic started, and it probably will not make any investor get rich quick. But even without its COVID-19 vaccine candidate, this company is a tried-and-tested, reasonably priced value stock that any investor could simply buy and hold for decades.

Mad Hedge Biotech & Healthcare Letter

October 13, 2020

Fiat Lux

FEATURED TRADE:

(THE UNDERDOGS OF THE COVID-19 VACCINE RACE)

(BNTX), (PFE), (CVAC), (PFE), (RHHBY)

It’s about time we talk about the German reinforcements brought in to fight this war against COVID-19.

For all the horror that this health crisis brought us, it’s nearly impossible to believe that there could be an upside to all these.

However, there is a bit of good news here.

Since the pandemic started, efforts to determine its origin, understand how it works, and search for a cure and vaccine have kickstarted innovation across the entire healthcare spectrum – from the familiar pharmaceutical sector to the volatile oft-misunderstood biotechnology field.

In fact, the biotechnology industry has received more attention in the past 10 months than the combined coverage of this sector since it was first introduced in 1919.

Nowadays, companies like Moderna (MRNA) have enjoyed practically round the clock coverage for their work.

So let’s take a look at the other up-and-coming biotechnology companies that have not received enough air time but are just as impressive.

In particular, let’s check out two of the German companies leading the charge in the COVID-19 vaccine race.

One company that isn’t getting enough credit these days is BioNTech (BNTX).

Since this German company paired up with Pfizer (PFE) in its vaccine development program, it rarely gets mentioned in the news.

After all, Pfizer with its $204.99 billion market capitalization makes for a bigger story compared to BioNTech’s $20.95 billion.

Nonetheless, the duo’s COVID-19 vaccine candidate, BNT162b2, is arguably the leading candidate right now – just ask Bill Gates.

If BNT162b2 succeeds, BioNTech stands to enjoy a financial windfall in the coming years.

So far, its vaccine program with Pfizer has secured them deals with the US, Canada, and Japan.

The German biotechnology company has also sealed an agreement with Fosun Pharma to supply 10 million doses to Macau and Hong Kong.

By 2021, BioNTech is expected to produce 250 million doses of the vaccine every six months.

This is enough to cover roughly 125 million people.

At a price of $19.50 for every dose, the company is estimated to earn $9.75 billion in annual revenue—not bad for a biotechnology company of its size.

The success of BNT162b2 could also mean additional leverage to propel the pipeline candidates in BioNTech’snmessenger RNA (mRNA) platform.

BioNTech has been working with Roche (RHHBY) in developing an mRNA therapy, called BNT122, to offer as a first-line treatment for melanoma and other solid tumors.

Apart from that, the company also has six early-stage mRNA candidates that target various types of cancer.

Aside from its mRNA technology-based programs, BioNTech is working with Denmark’s Genmab (CPH: GMAB) on three antibody therapies in early-stage trials for solid tumors and pancreatic cancer.

Another German biotechnology company flying under the radar is CureVac (CVAC).

A possible reason why it has not been generating that much buzz in the US is because it only conducted its initial public offering on the Nasdaq stock exchange in August.

Ever since the pandemic began though, CureVac has been one of the most active vaccine developers.

CureVac’s COVID-19 vaccine candidate uses the same technology as Moderna, which utilizes mRNA to trigger the body’s immune system to generate antibodies.

While Moderna has a huge head start in terms of clinical trials, CureVac may still have an advantage over the more popular biotechnology company.

Based on recent data, CureVac’s vaccine candidate shows more promise because it can take effect at very low doses of 2 to 6 micrograms.

In comparison, Moderna’s mRNA-1273 COVID-19 vaccine candidate requires a 100-microgram dosage.

Like BioNTech, the success of CureVac’s vaccine candidate would also bode well for the rest of the company’s mRNA candidates in its pipeline.

Two of those candidates are for cancer immunotherapies; one targets non-small lung cancer and the other targets a rare kind of cancer called adenoid cystic carcinoma. These therapies are also being studied for advanced melanoma as well as cancers of the head and neck.

Neither BioNTech nor CureVac has been hailed a household name in the US, and they may never reach that status.

Regardless, both companies will become extremely important and relevant for so many American households in the not-too-distant-future.

Due to the money they received to fund their COVID-19 programs, neither are in danger of running out of capital sometime soon or even take dilutive financing options as an alternative recourse. This stability, albeit short term, makes both biotechnology companies worth checking out.

More importantly, the pipeline programs of BioNTech and CureVac look promising despite being in the early stages.

All things considered, BioNTech and CureVac look like risky bets. However, these are risks with the potential to transform into massive rewards.

So, what should you do?

It all boils down to your investing style.

If you are an aggressive investor with high-risk tolerance, buy shares from dynamic biotechnology players that offer promising gains in a relatively short period.

Companies like BioNTech and CureVac, if successful in their COVID-19 vaccine efforts, could extend those gains to the long term and even leverage them to eventually market new products.

If you have lower risk tolerance, you can still make a play on these biotechnology companies. The key is to take a small position. This will limit your losses if things go south, but would also offer you rewards if the candidates work out.

Mad Hedge Biotech & Healthcare Letter

October 8, 2020

Fiat Lux

FEATURED TRADE:

(CAN REGENERON TRUMP OTHER COVID-19 RIVALS?)

(REGN), (GILD), (SNY), (JNJ), (MRK)

If the experimental COVID-19 treatment of Regeneron Pharmaceuticals (REGN) is good enough for the US president, then this stock should be given more attention not only by the media but also by investors.

One of the biggest stories this October is that President Donald Trump got infected with COVID.

The bigger story for the stock market though is his choice of treatment.

According to his medical team, Trump was given Regeneron’s antibody cocktail, called REGN-COV2, which was actually developed based on the same technology used in the company’s experimental Ebola treatment.

Although REGN-COV2 is still in the trial phase, reports that Trump already beat COVID just three days since his diagnosis are doing wonders for the stock.

Apart from REGN-COV2, Trump also received Gilead Sciences’ (GILD) Remdisivir as well as dexamethasone, a common generic steroid he once touted as a “miracle COVID-19 cure.”

The president was given aspirin and famotidine, which is more widely known as Johnson & Johnson (JNJ) and Merck’s (MRK) Pepcid.

On top of these, he took zinc, Vitamin D, and two immune-boosting supplements.

Compared to how far Gilead’s Remdesivir has gone in terms of offering treatment to COVID-19 patients with severe symptoms, Regeneron’s candidate is nowhere near the finish line.

Among all these drugs, however, Regeneron enjoyed the most advantage, with its stocks rising to roughly 5% since the announcement. Gilead also experienced a boost from the news, with a 3% jump.

What does this mean for investors?

Well, this news triggered aggressive buying of Regeneron shares. As expected, the unusually heavy volume pushed the stock price up.

While it would be tempting to join the market mob in buying a hot stock in the hopes of it getting even hotter, you might want to consider switching gears instead.

Hot stocks that dominate the news tend to cool and end up sliding at some point.

Rather than buying Regeneron stock right now, think about buying its bullish call options.

Options are always cheaper than their associated stock, which means you’ll be less at risk if something happens that lowers the stock price.

Even if the stock continues to advance, investing in options will still ensure that you get a nice return.

After all, each options contract represents 100 shares of stock.

To date, Regeneron’s stock is up 7.2% at $605.

That means you should buy bullish November $600 call options for roughly $40 with the expectation that REGN-COV2 gets approved—or at least stays as a strong contender until the next earnings report.

Since Regeneron released its 2019 third-quarter earnings report on November 5, it’s reasonable to assume that the company will follow the same timeline for 2020.

Therefore, setting the expiration to November ensures that you cover its third-quarter earnings report this year.

Aside from that, you’ll have enough time to gauge the success of REGN-COV2 and how the results will affect the stock price.

If the company’s share price reaches $665 at the expiration date, which is its peak price in the past 52 weeks, the call would be worth $65. If it hits $700, then the call will be worth $100.

For context, Regeneron stock has been anywhere between $279.22 and $664.64 in the past 52 weeks.

If REGN-COV2 gains approval, its projected 2021 sales could reach $1.8 billion. Meanwhile, its 2022 sales could hit $2.4 billion, with a decline to $1.7 billion by 2023.

Outside its COVID-19 efforts, the company has a promising portfolio to keep investors interested.

Regeneron’s annual revenue for its marketed drugs has been consistently climbing since 2012, with the biotechnology company’s earnings beating estimates in the last four quarters.

At the moment, the company has over 30 programs in its pipeline, 9 of which are in Phase 3, ensuring that its portfolio still has so much room for growth.

At the height of the pandemic, Regeneron maintained its stellar balance sheet in the second quarter.

One of its top-selling drugs is atopic dermatitis medication Dupixent, which it developed with Sanofi (SNY), with $770 million in sales for that period alone.

Looking at the drug’s track record, Dupixent is projected to rake in $6.3 billion in sales in 2021.

However, the top performer in the second quarter is eye injection Eylea, which contributed $1.1 billion in sales.

Meanwhile, skin cancer treatment Libtayo generated $63 million and cardiovascular disease drug Praluent raked in $47 million.

Regeneron also finished the second quarter with $943 million in net cash flow, which is a massive jump from the $188 million it reported in the same period in 2019.

On top of Regeneron raking in huge rewards for ’s COVID-19 treatment if approved, the company also has other promising products in its portfolio—ones that can still sway investors in their favor regardless of REGN-COV2’s future.