Global Market Comments

January 17, 2019

Fiat Lux

Featured Trade:

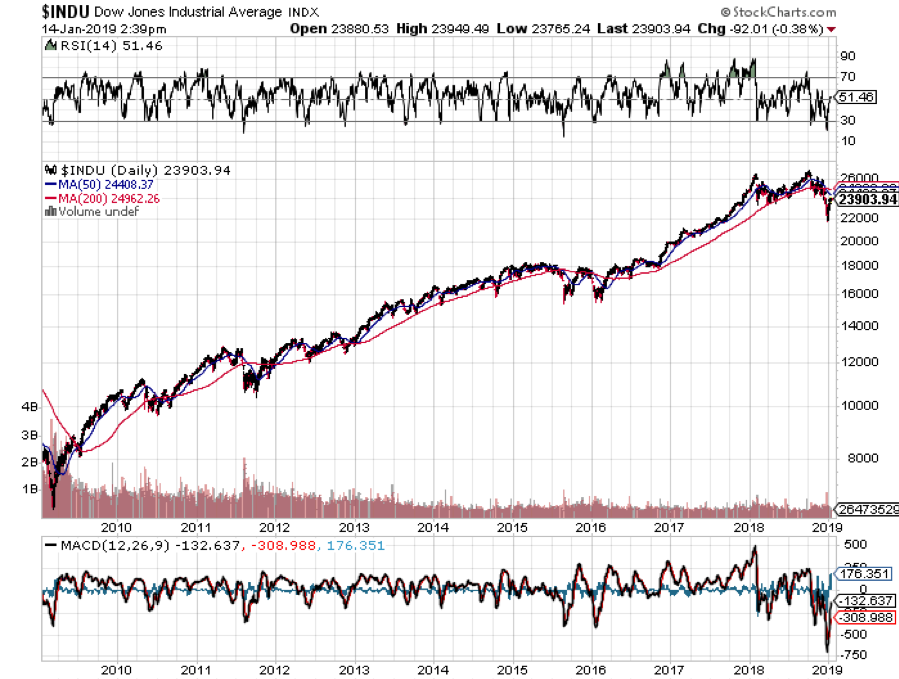

(WHAT HAPPENED TO THE DOW?)

($INDU), (EK), (S), (BS), (CVX), (DD), (MMM),

(FBHS), (MGDDY), (FL), (GE), (TSLA), (GM)

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

Global Market Comments

January 17, 2019

Fiat Lux

Featured Trade:

(WHAT HAPPENED TO THE DOW?)

($INDU), (EK), (S), (BS), (CVX), (DD), (MMM),

(FBHS), (MGDDY), (FL), (GE), (TSLA), (GM)

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

"If you can get a dividend higher than the yield on ten-year debt, it's an opportunity we haven't seen in our lifetime. On a five-year horizon, investing in large multinationals with high dividends will have a large payday," said Lawrence Fink, CEO of BlackRock.

Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(HAVE BONDS PEAKED?)

(TLT), (TBT),

(IS USA, INC. A SHORT?)

Selling short the US Treasury bond market (TLT) has been one of my core trades for the last 2 ½ years when rates hit a century low at 1.34%.

I call it my “Rich Uncle” trade. Every time bonds rallied five points, I unloaded government debt. If they rallied more, I doubled up. And my new “uncle” reliably wrote me a check every few weeks. As a result, I made money on 22 out of 23 consecutive Trade Alerts on this one asset class.

However, the gravy train may be coming to an end. Over the last week, two eminent authorities on bonds, my once Berkeley economics professor and former Federal Reserve governor Janet Yellen, and Golden Sachs (GS), one of the largest bond traders, have both opined that the yield on the ten-year US Treasury bond peaked last October at 3.25%.

My arguments against them are looking increasingly hollow, peaked, and facile. If bonds don’t resume their downtrend soon, I may have to surrender, run up the white flag, and toss my own 4.0% peak forecast in interest rates into the dustbin of history.

The data is undeniably starting to pile up in favor of Yellen and (GS). After a decade of economic expansion, inflation has absolutely failed to show. Sitting here in Silicon Valley which plans to use new technology to destroy 50 million jobs over the next 20 years, it was always obvious to me that wage gains in this recovery would be nil. Wages don’t rise in that circumstance.

So far, so good.

The China trade war continues to extract its pound of flesh from American business, trashing growth prospects everywhere. The government shutdown is also paring US growth by 0.10% a week. Hardly a day goes by now when another research house doesn’t predict a 2020 recession.

Current Fed governor Jay Powell has acknowledged as much, postponing any further interest rate hikes for the first half of this year.

If we peaked at 3.25% then where is the downside? How about zero, or better yet, negative -0.40%, the yield lows seen in Japan and Germany three years ago? That’s when my pal, hedge fund legend Paul Tudor Jones, started betting the ranch on the short side with European bonds making yet another fortune.

That’s when you’ll be able to refi your home with a 30-year conventional fixed rate loan of 2.0%. This is where home loans were available in Europe at the last lows.

After the traumatic move in yields from 3.25% down to 2.64% and (TLT) prices up from $111 to $124, you’d expect the market to give back half of its gains. That’s where we reassess. If the government shutdown is still on at that point, all bets are off.

Global Market Comments

January 15, 2019

Fiat Lux

SPECIAL ARMAGEDDON ISSUE

Featured Trade:

(HERE’S THE WORST-CASE SCENARIO),

($INDU), (SPY), (SDS), (TLT), (TBT), (FXE), (FXY),

(UUP), (DDP), (USO), (SCO), (GLD), (DGZ), (ITB)

Yesterday, I listed my Five Surprises of 2019 which will play out during the first half of the year prompting stocks to take another run at the highs, and then fail.

What if I’m wrong? I’ve always been a glass half full kind of guy. What if instead, we get the opposite of my five surprises? This is what they would look like. And better yet, this is how financial markets would perform.

*The government shutdown goes on indefinitely throwing the US economy into recession.

*The Chinese trade war escalates, deepening the recession both here and in the Middle Kingdom.

*The House moves to impeach the president, ignoring domestic issues, driven by the younger winners of the last election.

*A hard Brexit goes through completely cutting Britain off from Europe.

*The Mueller investigation concludes that Trump is a Russian agent and is guilty of 20 felonies including capital treason.

*All of the above are HUGELY risk negative and will trigger a MONSTER STOCK SELLOFF.

It’s really difficult to quantify how badly markets will behave given that this scenario amounts to five black swans landing simultaneously. However, we do have a recent benchmark with which to make comparisons, the 2008-2009 stock market crash and great recession. I’ll list off the damage report by asset class. I also include the exchange-traded fund you need to hedge yourself against Armageddon in each asset class.

*Stocks – Depending on how fast the above rolls out, you will see a stock market (SPY) collapse of Biblical proportions. You’ll easily unwind the Trump rally that started at a Dow Average of 18,000, down 25% from the current level, and off a gut-churning 9,000 points or 33% from the September top. The next support below is the 2015 low at 15,500, down 11,500 points, or 43% from the top. By comparison, during the 2008-2009 crash, we fell 52%. Everything falls and there is no safe place to hide. Buy the ProShares UltraShort S&P 500 bear ETF (SDS).

*Bonds – With the ten-year US Treasury yield peaking at 3.25% last summer, a buying panic would spill into the bond market. Inflation is nonexistent, we are running at only a 2.2% YOY rate now, so widespread deflation would rapidly swallow up the entire economy. In that case, all interest rates go to zero very quickly. The Fed cuts rates as fast as it can. Eventually, the ten-year yield drops to -0.40%, the bottom seen in Japanese and German debt three years ago. Buy the 2X short bond ETF (TBT) which will rocket to from $35 to $200.

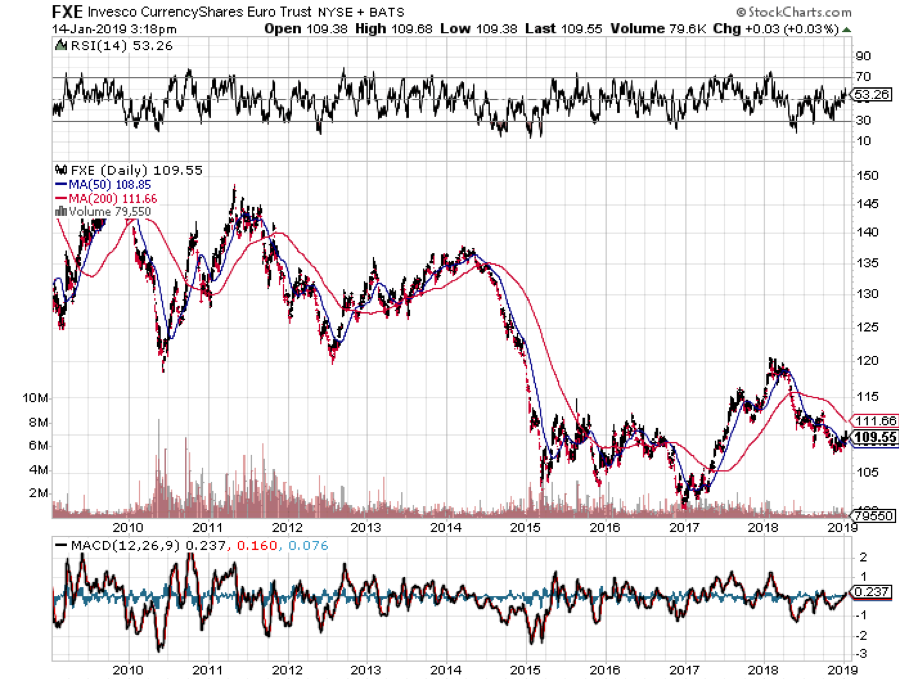

*Foreign Exchange – With US interest rates going to zero, the US Dollar (UUP) gets the stuffing knocked out of it. The Euro soars from $1.10 to $1.60 last seen in 2010, and the Japanese yen (FXY) revisits Y80. Strong currencies then crush the economies of our largest trading partners. Their governments take their interest rates back to negative numbers to cool their own currencies. Cash becomes trash….globally.

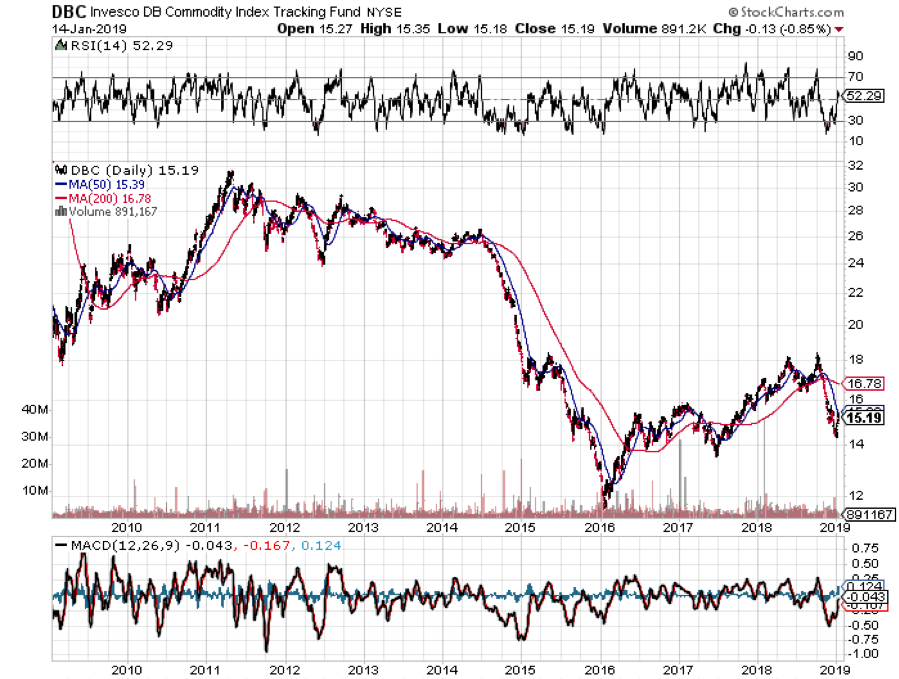

*Commodities

Here’s the really ugly part about commodities. They are only just starting to crawl OUT of a seven-year bear market. To hit them with another price collapse now would devastate the industry. Producer bankruptcies would be widespread. The ags would get especially hard hit as they have already been pummeled by the trade war with China. Midwestern regional banks would get wiped out. Buy the DB Commodity Short ETN (DDP).

*Energy

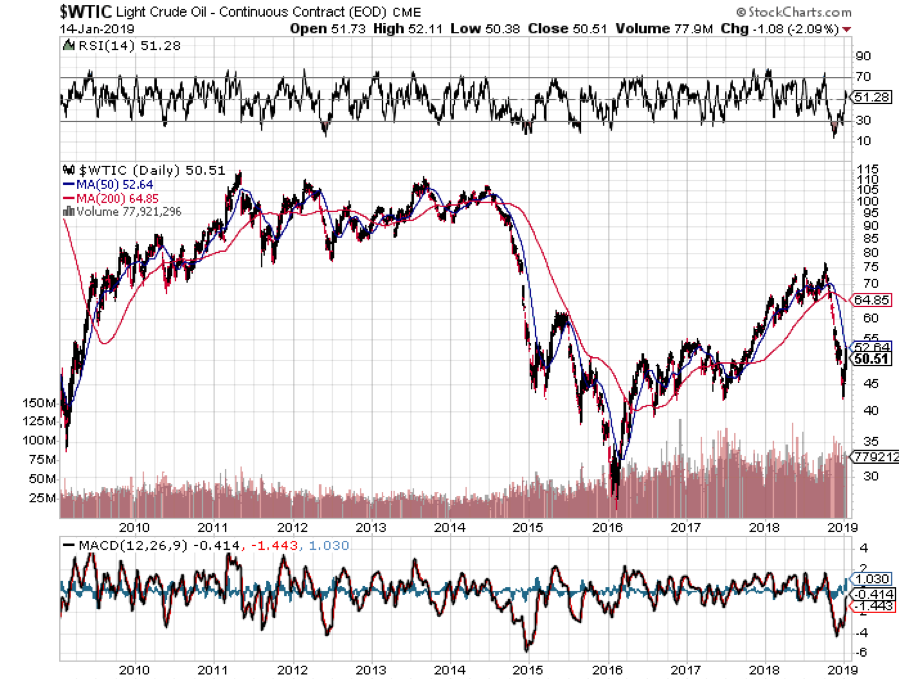

The price of oil (USO) is also just crawling back from a correction for the ages, down from $77 to $42 a barrel in only three months. Hit the sector with a recession now in the face of global overproduction and the 2009 low of $25 becomes a chip shot, and possibly much lower. Those who chased for yield with energy master limited partnerships will get flushed. Several smaller exploration and production companies will get destroyed. And gasoline drops to $1 a gallon. The Middle East collapses into a geopolitical nightmare and much of Texas files chapter 11. Buy the ProShares UltraShort Bloomberg Crude Oil ETF (SCO).

*Precious metals

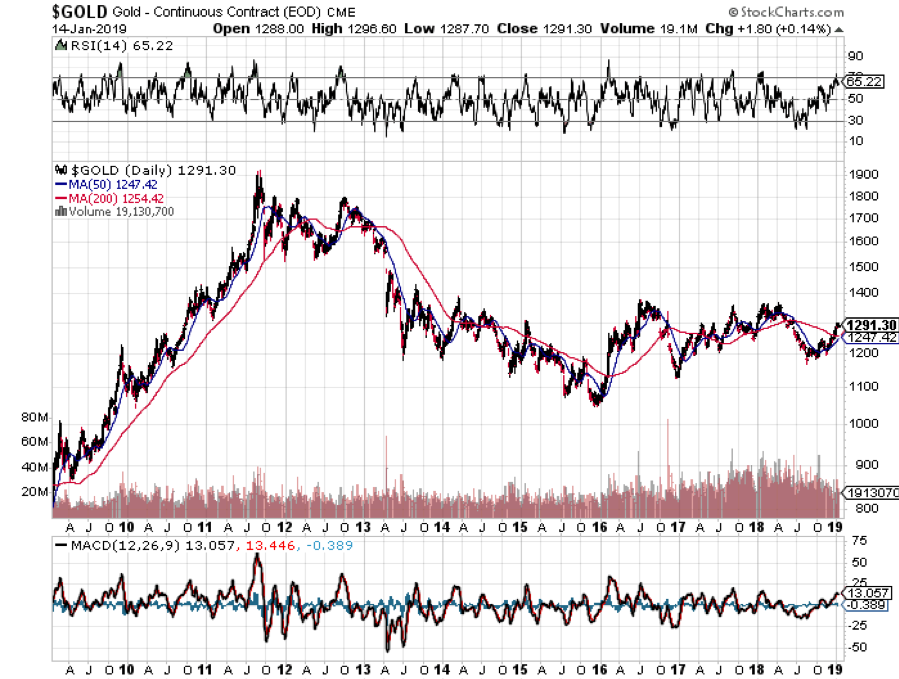

Gold (GLD) initially rallies on the flight to safety bid that we have seen since September. However, if things get really bad, EVERYTHING gets sold, even the barbarous relic, as margin clerks are in the driver’s seat. You sell what you can, not what you want to, as liquidity becomes paramount. This is what took the yellow metal down to $900 an ounce in 2009. Buy the DB Gold Short ETN (DGZ).

*Real Estate

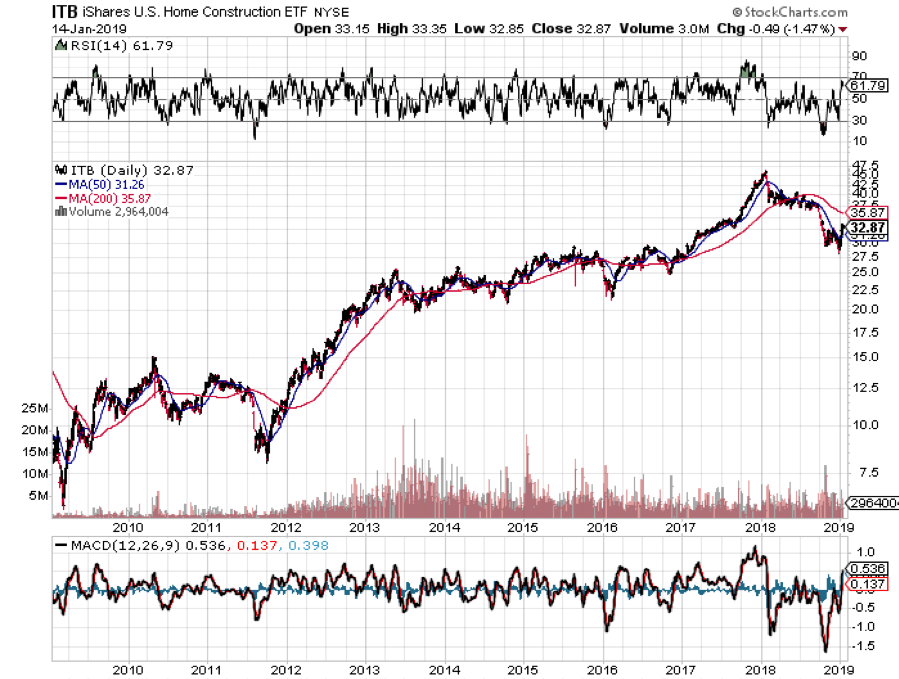

Believe it or not, real estate doesn’t do all that bad in a worst-case scenario. It is perhaps the safest asset class around if a new crisis financial unfolds. For a start, interest rates at zero would provide a huge cushion. The Dodd-Frank financial regulation bill successfully prevented lenders returning to even a fraction of the leverage they used in the run-up to the last recession. We are about to enter a major demographic tailwind in housing as the Millennial generation become the predominant home buyers. I’ve never seen a housing slump in the face of a structural shortage. And homebuilder stocks (ITB) have already been discounting the next recession for the past year. A lot is already baked in the price.

Conclusion

Of course, it is highly unlikely that any of the above happens. Think of it all as what Albert Einstein called a “thought experiment.” But it is better to do the thinking now so you can do the trading later. There may not be time to do otherwise.

Be Careful, They Bite!

Be Careful, They Bite!Global Market Comments

January 14, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IS THE BULL MARKET BACK?),

(SPY), (TLT), (MSFT), (AMZN), (CRM), (AAPL), (FXE),

(TESTIMONIAL)

During the Christmas Eve Massacre, a close friend sent me a research report he had just received entitled “30 Reasons Equities Will Fall in 2019.” It was laughable in its extreme negativity.

I thought this is it. This is the bottom. ALL of the bad news was there in the market. Stocks could only go up from here.

If I’d had WIFI at 12,000 feet on the ski slopes and if I’d thought you would be there to read them, I would have started shooting out Trade Alerts to followers right then and there. As it turned out, I had to wait a couple of days.

Two weeks later, and here I am basking in the glow of the hottest start to a new year in a decade, up 6.45%. So far in 2019, I am running a success rate of 100% ON MY TRADE ALERTS!

Don’t expect that to continue, but it is nice while it lasts.

I can clearly see how the year is going to play out from here. First of all, my Five Surprises of 2019 will play out during the first half of the year. In case you missed them, here they are.

*The government shutdown ends quickly

*The Chinese trade war ends

*The House makes no moves to impeach the president, focusing on domestic issues instead

*Britain votes to rejoin Europe

*The Mueller investigation concludes that Trump has an unpaid parking ticket in Queens from 1974 and that’s it.

*All of the above are HUGELY risk-positive and will trigger a MONSTER STOCK RALLY.

After that, the Fed will regain its confidence, raise interest rates two more times, and trigger a crash even worse than the one we just saw. We end up down on the year.

My long-held forecast that the bear market will start on May 10, 2019 at 4:00 PM EST is looking better than ever. However, I might be off by an hour. Those last hour algo-driven selloffs can be pretty vicious.

I make all of these predictions firmly with the knowledge that the biggest factors affecting stock prices and the economy are totally unpredictable, random, and could change at any time.

It was certainly an eventful week.

Fed governor Jay Powell essentially flipped from hawk to dove in a heartbeat, prompting a frenetic rally that spilled over into last week.

On the same day, China cut bank reserve requirements, instantly injecting $200 billion worth of stimulus into the economy. That’s the equivalent of spending $400 billion in the US. The last time they did this we saw a huge rally in stocks. It turns out that the Middle Kingdom has a far healthier balance sheet than the US.

Saudi Arabia chopped oil production by 500,000 barrels a day, sending prices soaring. It's not too late to get into what could be a 40% bottom to top rally to $62 (USO).

Macy's (M) disappointed, crushing all of retail with it, and taking down an overbought main market as well. It highlights an accelerating shift from brick and mortar to online, from analog to digital, and from old to new. Online sales in December grew 20% YOY. Will Amazon sponsor those wonderful Thanksgiving Day parades?

Home mortgage rates hit a nine-month low with the conventional 30-year fixed rate loan now wholesaling at an eye-popping 4.4%. Will it be enough to reignite the real estate market? It is actually a pretty decent time to start picking up investment properties with a long view.

My 2019 year to date return recovered to +6.45%, boosting my trailing one-year return back up to 31.68%. 2018 closed out at a respectable +23.67%.

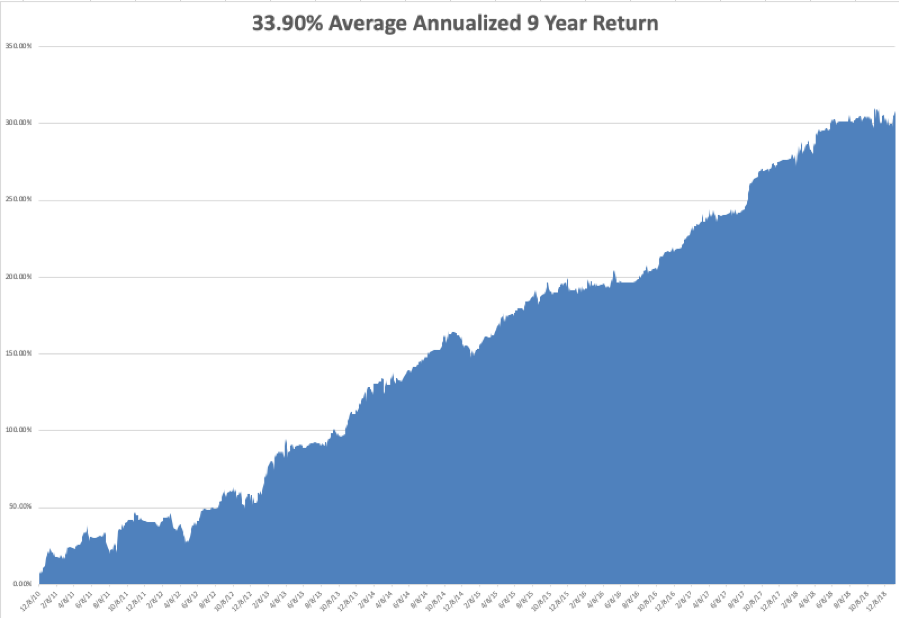

My nine-year return nudged up to +307.35, just short of a new all-time high. The average annualized return revived to +33.90.

I analyzed my Q4 performance on the chart below. While the (SPY) cratered -19.5% in three short months, my Trade Alert Service hung in with only a -4.9% loss. The quarter was all about defense, defense, defense. It was the hardest quarter I ever worked.

While everything failed last year, everything has proven a success this year. I came back from vacation a week early to pile everyone into big tech longs in Salesforce (CRM), Microsoft (MSFT), and Amazon (AMZN). I doubled up my short position in the bond market.

I even added a long position in the Euro (FXE) for the first time in years. If Britain votes to stay in Europe, it is going to go ballistic.

I also top ticketed a near-record rally by laying out a few short positions in Apple (AAPL) and the S&P 500 (SPY). I am now neutral, with “RISK ON” positions “RISK OFF” ones.

The upcoming week is very iffy on the data front because of the government shutdown. Some data may be delayed and other completely missing. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

On Monday, January 14 Citigroup (C) announces earnings.

On Tuesday, January 15, 8:30 AM EST, the December Producer Price Index is out. Delta Airlines (DAL), JP Morgan Chase (JPM), and Wells Fargo (WFC) announce earnings.

On Wednesday, January 16 at 8:30 AM EST, we learn December Retail Sales. Alcoa (AA) and Goldman Sachs (GS) announce earnings.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, January 17 at 8:30 AM EST, we get the usual Weekly Jobless Claims. At the same time, December Housing Starts are published. Netflix (NFLX) announces earnings.

On Friday, January 18, at 9:15 AM EST, December Industrial Production is out. The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings.

As for me, my girls have joined the Boy Scouts which has been renamed “Scouts.” Their goal is to become the first female Eagle Scouts.

So, I will retrieve my worn and dog-eared 1962 Boy Scout Manual and refresh myself with the ins and outs of square knots, taut line hitches, sheepshanks, and bowlines. Some pages are missing as they were used to start fires 55 years ago. I am already signed up to lead a 50-mile hike at Philmont in New Mexico next summer.

As for the Girl Scouts, they are suing the Boy Scouts to get the girls back, claiming that the BSA is infringing on its trademark, engaging in unfair competition, and causing “an extraordinary level of confusion among the public.”

Is there a merit badge for “Frivolous Lawsuits”?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 11, 2019

Fiat Lux

Featured Trade:

(WHY THE MARKET CRASHED IN DECEMBER),

(SPY), ($INDU), (VIX)

(THE GOVERNMENT’S WAR ON MONEY),

(TESTIMONIAL)

Were you horrified by the market action in December? The next one could get much worse.

We are all used to market corrections. Live long enough and you will endure hundreds of them.

But December? That was a real first class crash, a four times a century event. And to see this occur in the face of solid economic data made it totally unexpected by all. The only analysts predicting a collapse like this one are the ones who have been expecting it daily for the past decade.

To see a 20% decline in NASDAQ and a 50% plunge in market leaders in the face of a 3.2% GDP growth rate and a 3.9% unemployment rate is a first. It makes no sense.

This wasn’t a correction. This was an instance where the market ceased to function and was effectively closed. In fact, it took a conspiracy of several independent forces to get the meltdown we got.

The bottom line here is that this is not your father’s stock market.

The low hanging fruit here is to blame in the high-frequency algorithms. But that is the cheap shot. Algos don’t care which way markets go. They take volatility up sharply, but they take it down as well, as any long-suffering vol player will tell you.

Over time, their market impact is neutral. And algo traders go home 100% in cash every night. That doesn’t explain opening meltdowns of 500 points a day or more. No, there was something much more structural at work.

Human emotions are easy to predict. Take the humans out of the equation and markets can only be read by mainframe computers, at least on a short-term basis. That’s why so many of these market traditions, like “Sell in May and go away,” and the “Santa Claus rally” have quit working.

Only about 10% of today’s daily traders are the breathing kind. The rest are all made of silicon. Even I have come to rely heavily on my own personal algorithms in the Mad Hedge Market Timing Index. It has been worth its weight in gold and saved my bacon many times.

There is no doubt that pure quant strategies have blood on their hands. These funds strictly adhere to rules that have identified the long-term relationships between different asset classes and act accordingly.

For example, when bonds go up, you sell them and buy more stock, but sell more foreign currencies as well, and perhaps pick up some copper as well. All of this is adjusted for risk and volatility. There is thought to be about $1.5 trillion committed to this kind of strategy.

Among these, you can include “risk parity traders” of the kind pioneered by my friend Ray Dalio in the 1990s. (Ray will tell you how he did it in his fascinating book, Principals, out last year). Ray, by the way, is one of the top performing money managers over the last 30 years.

Trend followers pour more gasoline on the fire. If you sell, they will sell more, creating these massive 100 handle days in the S&P 500 (SPY).

Heightening fears was a never-ending torrent of bad news out of Washington. Two out of three key cabinet positions were emptied by presidential firings and remain unoccupied. Trade talks with China came to an impasse. It was not what investors wanted to hear.

All of this set up the perfect storm for December.

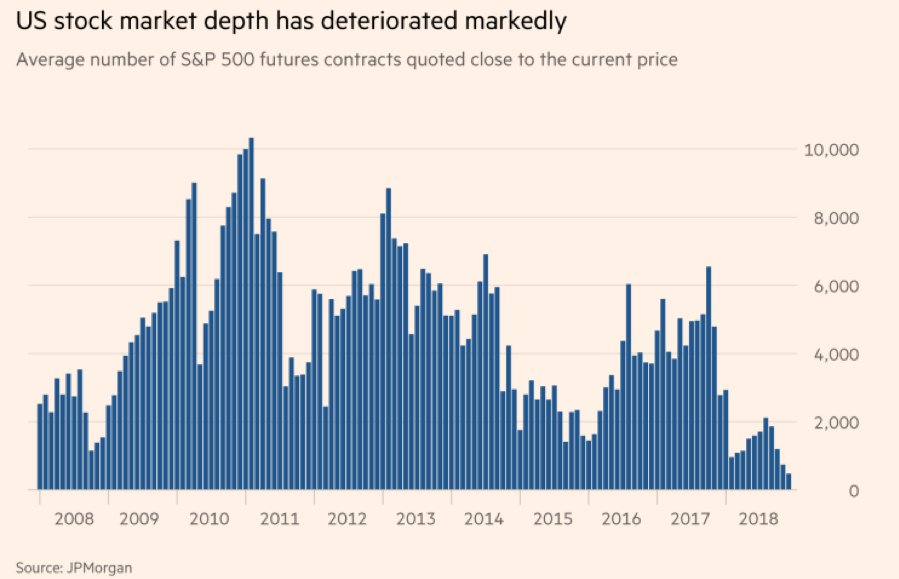

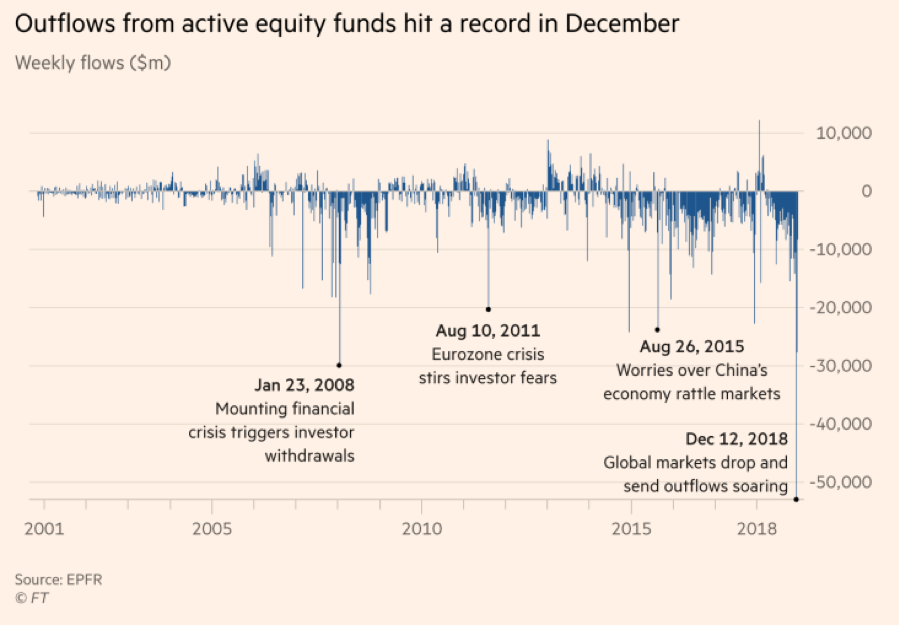

Equity mutual fund redemptions hit a record $53 billion in early December. Market liquidity dramatically shrank as players took off for the holidays, as seen on the chart below. Liquidity during the second half of December was thinner than the worst days of the 2008 financial crisis.

A two-decade-long flight of capital from the floor of the New York Stock Exchange was also a factor. The inevitable result was for the Volatility Index (VIX) to take a run at its highs for the year.

If you wanted to sell anything in size, it could only take place at throwaway prices. It all culminated in the notorious Christmas Eve Massacre which saw a 1,000-point range day in the Dow Average in a holiday-shortened trading day. If it had been a full day it might have been down 2,000 points.

Don’t expect any respite from these strategies any time soon. In fact, we could see worse moves ahead. The current administration believes in a free market, non-interventionist approach to securities markets. That means no new regulation.

The same thing happened in the run-up to the 2008 crash when Christopher Cox (brother of my old boss at Morgan Stanley, Archie Cox) was basically told to go play golf instead of regulate.

Welcome to the new age of investing. The bottom line for all of us traders and investors is that we are going to have to pedal a lot harder to earn our crust of bread….or become a computer.