Global Market Comments

January 22, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LEARNING FROM YOUR LOSERS)

Global Market Comments

January 22, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LEARNING FROM YOUR LOSERS)

I don’t lose money in the market very often, but when I do, I really hate it. I also take each attack of red ink as a learning opportunity. Do this for 55 years and you get pretty good at it.

So what did I learn from my ill-timed double short in the S&P 500 last week? It turns out a lot.

The stock market was in the process of backing out six Fed rate cuts this year, which was never realistic, and returning to only three, which is much more realistic. The March tightening got pushed back at least until May.

You see this in the sectors that got hammered last week, big borrowers like airlines, cruise lines, and construction. Net creditors to the financial system, i.e. big tech rose almost every day. That lasted about two days.

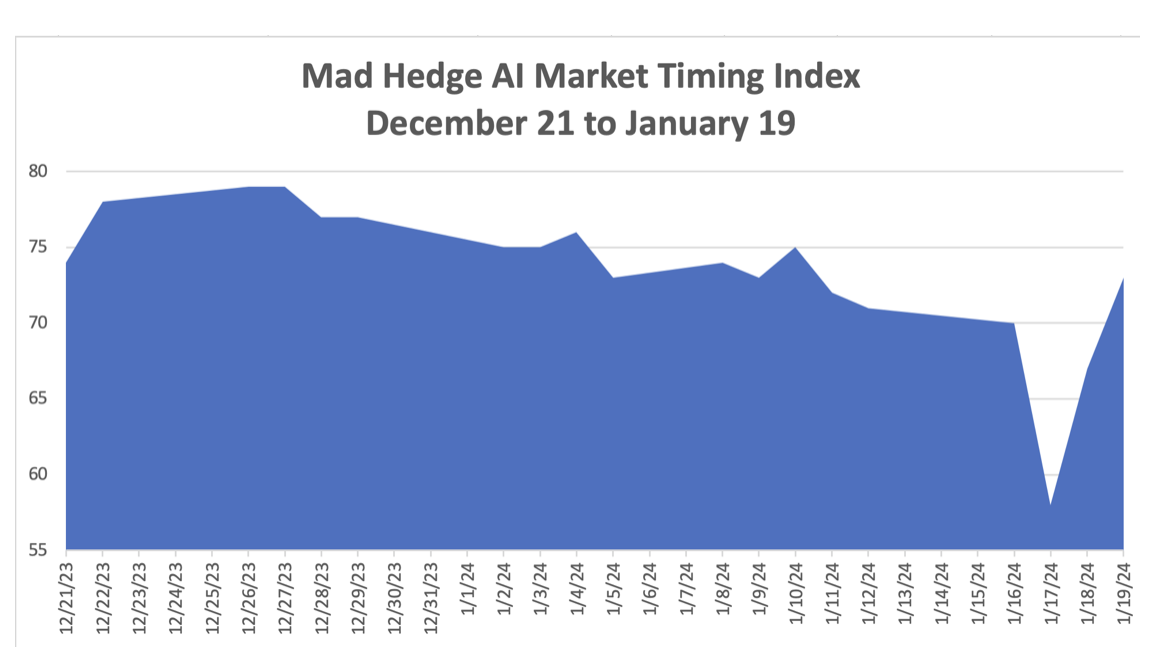

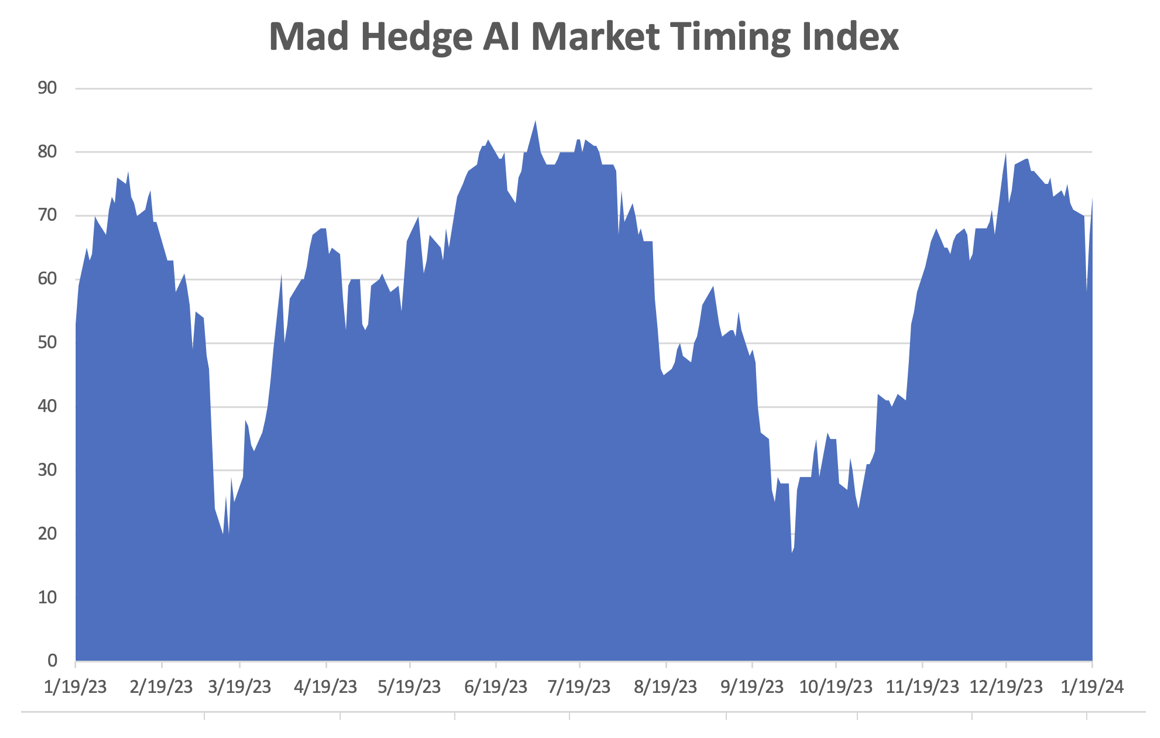

It turns out that the Mad Hedge AI Market Timing Index led me astray. I already knew that it was not perfect, but I had to be reminded from time to time of a loss. After the timing index peaked at a six-month high of 78 on December 26, it plunged all the way down to 58 on January 17, the classic sign of a market that is rolling over and dying.

So what did it do after that? A red-hot University of Michigan Consumer Sentiment Index hit an out-of-the-blue 2 1/2 year high, causing my own index to shoot up to 73. Ouch! Never underestimate the ability of the American consumer to spend money!

That triggered the mother of all short-covering rallies. It turns out that I am not the only one using an algorithm-driven market timing index these days, all of which drew the same conclusions on Wednesday and went short the (SPY). A January Friday options expiration added gasoline to the fire.

Fortunately, I had eight other long positions that will more than offset my short losses well before the February 16 option expiration in 20 trading days, such is the nature of my long/short strategy. But a hit is a hit, nonetheless.

It’s easy to get too aggressive and overconfident when you’ve had two back-to-back 80% plus years such as the case at the Mad Hedge Fund Trader. Occasionally, you have to get slapped in the face to dial it back down.

What is important here is to understand the broader message of what the market is trying to tell us. That artificial intelligence is worth far more than we understand. While the current market capitalization of the top AI leaders, (MSFT), (GOOGL), (TSLA), (META), and (NVDA) is now at $10 trillion, I bet that they will top $40 trillion in a decade. Markets are already discounting that target.

Once again that makes my own decade forecast of a Dow Average at 240,000 positively conservative.

And while NVIDIA now looks insanely expensive, with the doubling weighting I had gaining another 25% in 2024, it is in fact still the cheapest AI stock in the market. That’s because its earnings are growing far faster than its stock price….by a large margin.

It's definitely looking like a different market so far in 2024. We are going to have to work harder….and smarter.

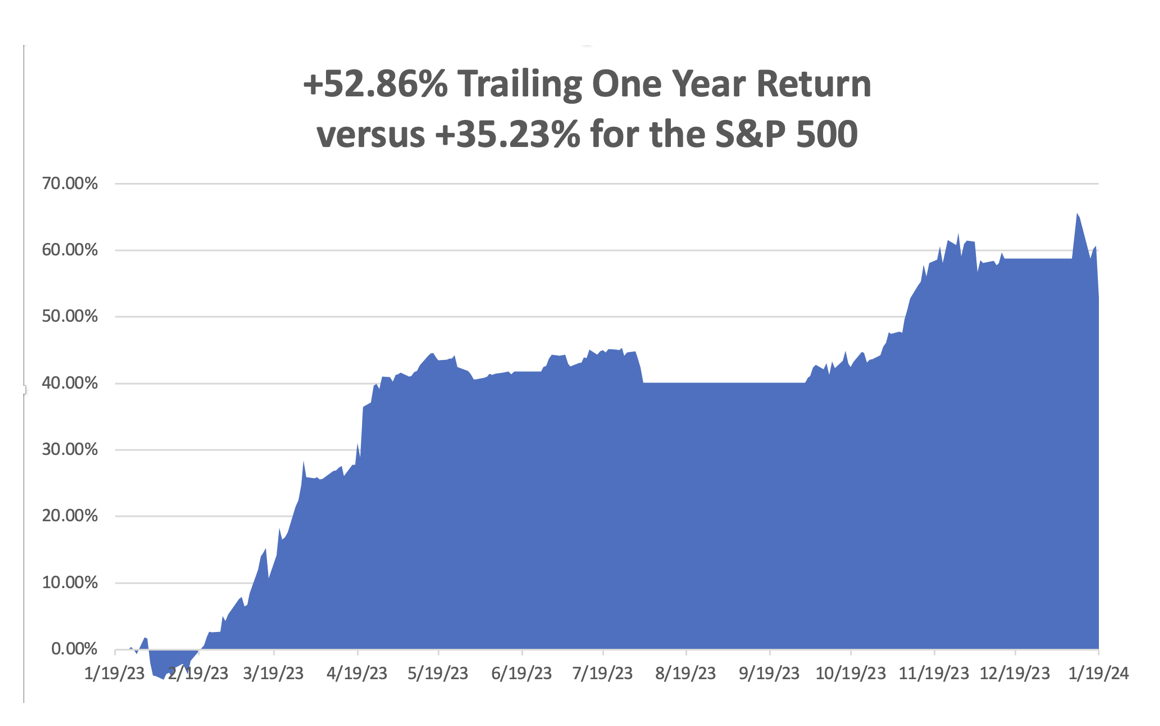

So far in January, we are down -5.89%. My 2024 year-to-date performance is also at -5.89%. The S&P 500 (SPY) is up +1.14% so far in 2024. My trailing one-year return reached +xx% versus +xx% for the S&P 500.

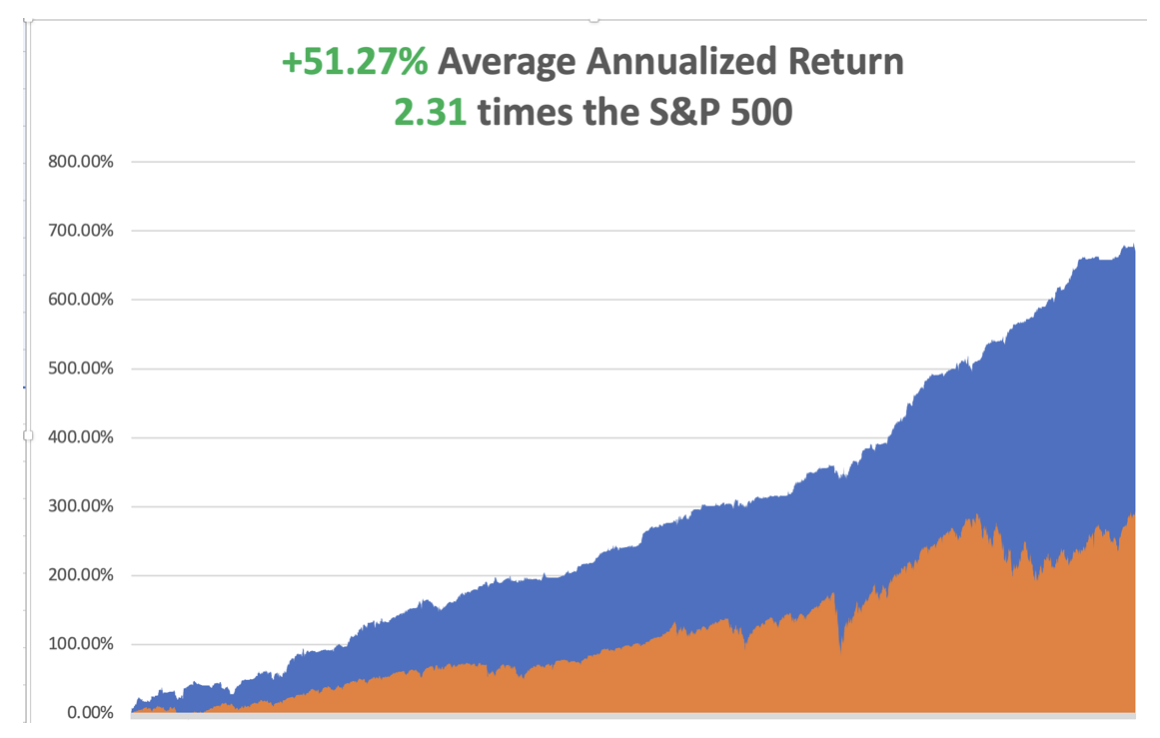

That brings my 15-year total return to +670.74%. My average annualized return has retreated to +51.27%, another new high.

Some 63 of my 70 trades last year were profitable in 2023. In 2024 100% of my trades have been profitable.

After a round of profit-taking, I am maintaining longs in (MSFT), (AMZN), (V), (PANW), (CCJ), (TLT). I am regrettably short the (SPY).

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

US Budget Funded for Two More Months, kicking the can down to March 8. Given byelections and their current death rate, Republicans may no longer have a majority by then. Those numbers include $1.59 trillion for fiscal year 2024, with $886 billion for defense spending and $704 billion in non-defense spending. Schumer and Johnson also agreed to a $69 billion side deal in adjustments that will go toward non-defense domestic spending. Not that markets care.

University of Michigan Consumer Index surged, up to 78.8 for January, its highest level since July 2021. Consumer sentiment has improved amid a drop in gasoline prices and solid stock market gains.

Building Permits Improve, at 1.50 million, up 1.9%. But the latest New Monthly Residential Construction report, released this morning jointly by the U.S. Census Bureau and the U.S. Department of Housing and Urban Development, is 7.6% above the December 2022 rate of 1.357 million. Declining mortgage rates are translating into mixed improvements in home production.

Homebuilder Sentiment Jumps, by seven points to 44, the most in nearly a year. Lower mortgage rates boosted customer traffic, sales, and the demand outlook. The US is short 10 million homes which will take a decade to build. Buy (KEN), (PHM), and (KBH) on dips.

US Retail Sales Come in Best in Three Months, up 0.6% in December, as analysts continue to underestimate the American consumer. Clothing, general merchandise, and e-commerce led gains. The “soft landing” is looking like a sure thing. Buy all major dips in stocks.

Weekly Jobless Claims plunged to 187,000, a 17-month low, underlining the “soft landing” scenario. Continuing claims stand at 1.80 million. Labor strength has persisted despite attempts by the Federal Reserve to slow the economy, and the jobs market in particular, through a series of interest rate hikes. Bonds and other interest rate plays sold off on the news.

On Monday, January 22, nothing of note is announced.

On Tuesday, January 23 at 8:30 AM EST, the Richmond Fed Manufacturing Shipments Index is released.

On Wednesday, January 24 at 2:00 PM, the S&P Global Flash PMI is published.

On Thursday, January 25 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Q4 US GDP first read.

On Friday, January 26 at 2:30 PM, the December Core PCE Index is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I recall my last trip around the world in 2018. I took the trip because I feared climate change would soon make visits to the equator impossible because of intolerable temperatures and the breakdown of civilization. As it turned out, the global pandemic began six months later, making such travel out of the question for two years.

I beat Phileas Fogg by 55 days, who needed 88 days to complete his trip around the world to settle a gentleman’s bet. But then he had to rely on elephants, sailing ships, and steam engines to complete his epic voyage or at least the one imagined by Jules Verne.

I actually took a much longer route, using a mix of Boeings and Airbuses to fly 80 hours over 40,000 miles on 18 flights through 12 countries in only 33 days. Incredibly, our baggage made it all the way, rather than see its contents sold on the black markets of Manila, New Delhi, or Cairo.

It was a trip around the world for the ages, made even more challenging by dragging my 13 and 15-year-old girls along with me. I have always considered my most valuable asset to be the trips I took to Europe, Africa, and Asia in 1968. The comparisons I can make today some 55 years later are nothing less than awe-inspiring.

I wanted to give the same gift to them.

It began with a 12 ½ hour flight from San Francisco to Auckland, New Zealand. Straight out of the airport I rented a left-hand drive Land Rover and drove three hours to high in the steam-covered mountains of Rarotonga where we were dinner guests of a Māori tribe. To earn my dinner of pork and vegetables cooked underground I had to dance the haka, a Māori war dance.

The Haka

Of course, with kids in tow, a natural stop was the Hobbit Village of Hobbiton 1½ hours outside of Auckland. I figured the owners of the idyllic sheep farm were earning at least $25 million a year showing tourists the movie set.

In all, I put 1,000 miles on the car in four days, even crossing New Zealand’s highest mountain range on a dirt road. The thick forests were so primeval my daughter expected to see a dinosaur around every curve. We reached our southernmost point at Mt. Ruapehu, a volcano used as the inspiration for Mt. Doom in Peter Jackson’s Lord of the Rings.

The focus of the Australia leg was ten strategy lectures which I presented around the country. I was mobbed at every stop, with turnout double what I expected. The Mad Hedge Fund Trader and the Mad Hedge Technology Letter picked up 100 new subscribers in the Land Down Under in five days.

Maybe it was something I said?

My kids’ only requirements were to feed real kangaroos and koala bears, which we duly accomplished on a freezing cold morning outside Melbourne. We also managed to squeeze in a tour of the incredible Sydney Opera House in between lectures, dashing here and there in Uber cabs.

I hosted five Mad Hedge Global Strategy Luncheons for existing customers in five days. The highlight was in Perth, where eight professional traders and I enjoyed a raucous, drunken meal. They had all done well off my advice, so I was popular, to say the least. Someone picked up the tab without me even noticing.

After that, it was a brief ten-hour flight to Manila in the Philippines, with a brief changeover in Hong Kong, where massive protest demonstrations were underway. Ever the history buff, I booked myself into General Douglas MacArthur’s suite at the historic Manila Hotel. The last time I was here I interviewed President Ferdinand Marcos and his lovely wife Imelda. After lunch with my enthusiastic Philippine staff, I was on my way to the airport.

I took Malaysian Airlines to New Delhi, India, which has lost two planes over the last five years and where the crew was definitely on edge. I asked why a second plane was lost somewhere over the South Indian Ocean and the universal response was that the pilot had gone insane. Security was so tight that they confiscated a bottle of Jamieson Irish Whiskey that I had just bought in duty-free.

India turned out to be a dystopian nightmare. If climate change continues this is your preview. With temperatures up to 120 degrees in 100% humidity people here dying of heat stroke by the hundreds. Elephants had to be hosed down to keep them alive. It was so hot you couldn’t stray from the air conditioning for more than an hour. The national radio warned us to stay indoors.

In Old Delhi, the kids were besieged by child beggars pawing them for food and there were mountains of trash everywhere. In the Taj Mahal, my older daughter passed out and we had to dump our remaining drinking water on her to cool her down and bring her back to life. We spent the rest of the day sightseeing indoors at the most heavily air-conditioned shops. The hand-woven Persian carpet should arrive any day now.

If global temperatures rise by just a few more degrees you’re going to lose a billion people in India very soon.

On the way to Abu Dhabi were flew directly over the tanker war at the Straits of Hormuz, one of my old flight paths during my Morgan Stanley days. It was too dusty to see any action there. We got a much better view of Sinai and the Red Sea, which, I told the kids, Moses parted 5,000 years ago (they’ve seen Charlton Heston in The Ten Commandments many times).

Upon landing at Cairo, Egypt’s ever-vigilant military intelligence service immediately picked me up. Apparently, I was still in their system dating back to my coverage of Henry Kissinger’s shuttle diplomacy for The Economist in 1976. That was all a long time ago. Having two kids with me meant I was not there to cause trouble, so they were very friendly. They even gave us a free ride to the downtown Nile Hilton.

After India, Cairo, and the Sahara Desert were downright pleasant, a dry and comfortable 100 degrees. We did the standard circuit, the pyramids, and the Sphynx followed by a camel ride into the desert.

If you are the least bit claustrophobic don’t even think about crawling into the center of the Great Pyramid on your hands and knees as we did. I was sore for two days. We spent the evening on a Nile dinner cruise, looking for alligators, entertained by an unusually talented belly dancer.

The next stage involved a one-day race to Greece, where we circled the Acropolis in all its glory, and then argued with a Greek taxi driver on how to get back to the airport. We ended up taking an efficient airport train, a remnant of the 2000 Athens Olympics. If impoverished and bankrupt Athens has such a great airport train, why doesn’t New York or San Francisco?

It was a quick hop across the Adriatic to Venice, Italy, where we caught an always exciting speed boat from the Marco Polo to our Airbnb near St. Mark’s Square. We ran through the ancient cathedral and the Palace of the Doges, admiring the massive canvases, the medieval weaponry, and of course, the dungeon.

One of the high points of the trip was a performance of Vivaldi’s Four Seasons in the very church it was composed for. A ferocious thunderstorm hit, flooding the plaza outside and causing the lead violinist’s string to break, halting the concert (rapid humidity change I guess).

When we got home with soggy feet, the Carabinieri had cordoned off our block with police tape because a big chunk of our 400-year-old roof had fallen into the street. It taxed my Italian to the max to get into our apartment that night. The Airbnb host asked me not to mention this in my review (I didn’t).

The next day brought a circuitous trip to Budapest via Brussels. Budapest was a charm, a former capital of the Austria-Hungarian Empire, and the architecture to prove it. The last time I was here 55 years ago the Russian Army was running the place and it was grim, oppressive, and dirty.

Today, it is a thriving hot spot for Europe’s young, with bars and nightclubs everywhere. Dinners dropped from $150 in Venice to $30. We topped the night with a Danube dinner cruise with a folk dancing troupe. I’m told you can live there like a king for $1,000 a month.

Visiting the Golden Age in Budapest

The next morning we drew closer to our final destination of Switzerland. A four-hour train ride brought us to my summer chalet in Zermatt and some much-needed rest. At the end of a long valley and lacking any cars, Zermatt is one of those places where you can just give the kids 50 Swiss francs and tell them to get lost. I spent mornings hiking up from the valley floor and afternoons getting caught up on the markets and my writing.

There’s nothing like recharging my batteries in the clean mountain air of the Alps. The forecast was rain every day for two weeks, but it never showed. As a result, I ended up hiking ten miles a day to the point where my legs were made of lead by the end.

The only downer was watching helicopters pick up the bodies of two climbers who fell near the top of the Matterhorn. As temperatures rise rapidly the ice holding the mountain together is melting, leading to a rising tide of fatal accidents.

I caught my last flight home from Milan. Anything for one more great dinner in Italy, which I enjoyed in the Galleria. At the train station, I chatted with a troop of Italian Boy Scouts in blue uniforms headed for the Italian Alps. The city was packed with Chinese tour groups, and there was a one-month wait to buy tickets for Leonardo DaVinci’s The Last Supper. Another Airbnb made sure I stayed up all night listening to the city’s yellow trolleys trundle by.

Finally, an 11-hour flight brought me back to the City by the Bay. Thanks to two sleeping pills of indeterminate origin I went to sleep over England and woke up over Oregon, preparing for a landing. It seems that somewhere along the way I proposed marriage to the Arab woman sitting next to me, but I have no memory of that whatsoever. At least that’s what the head flight attendant thought.

I am now planning this summer’s trip. After the Queen Mary and the Orient Express should I climb the Matterhorn again? Or should I summit Mount Kilimanjaro in Africa first? No transatlantic trip should ever be wasted. And I have to get home in time to join a 50-mile hike with the Boy Scouts in New Mexico and then cart two kids off to college.

What a great problem to have.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 19, 2024

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(A CHEAPER WAY TO DO DAVOS)

Dear John,

Remember me from the QE2? You don’t miss much, but I’m forwarding this AI story, in case you find it interesting. You are the best financial advisor I have ever found.

I know you’ve been a big believer in NVIDIA (NVDA) for years. When I read this, I really understand that (NVDA) is only going to get bigger. They and Microsoft (MSFT) MSFT are the two biggest investors in AI startups.

I hope you have a great 2024, thanks for all the hard work and great newsletters. |

Bill

Santa Barbara, CA

It’s that time of year again, when finance ministers, central bank governors, hedge fund managers, and assorted rock stars hold their annual confab high in the Alps at Davos, Switzerland.

When I was a director of one of the largest banks in Switzerland, I found myself a frequent visitor to Davos. The conference is one of those things that you only want to do once. More than that is too boring.

In years gone by, we provided the loans to the Canton of Graubünden needed to build the lifts and gondolas in Davos to develop it into a world-class ski resort and watering hole for the wealthy.

Without that money, Davos would have remained a small mountain hamlet on the way to long-established St. Moritz, possibly not even warranting its own train station.

Instead of renting out hotel suites for $10,000 a day, the residents would be filling their days cutting hay, milking cows, and making goat cheese. Generous government subsidies would keep the village in the green.

Thanks to our largess, I received a lifetime ski lift ticket there which I still use on occasion.

My friend, the intrepid New York Times reporter, Andrew Ross Sorkin, tells me that the minimum cost to attend the exclusive World Economic Forum for membership and a single ticket is $71,000, and that’s for the cheap tickets.

That just gets you general admission. If you hail from an up-and-coming emerging market, like China, you get a break on the price.

To join some of the private discussion groups, you need to upgrade to a $156,000 package. More exclusive access can be had for “Strategic Partners” for prices ranging up to $696,000 after the latest price increase and Swiss franc revaluation.

That does not include the cost of travel, meals, and accommodation, which are stratospheric, now that the Swiss franc is more valuable than the US dollar (I remember when it was 3:1). $75 for a hamburger? No problem!

All of this just to rub shoulders with hedge fund manager Ray Dalio, European Central Bank governor Christine Lagarde, rock star Bono, and others of their ilk.

Certainly, you can gain many of the insights found in Davos by simply reading the Mad Hedge Fund Trader, at a much lower price. I can get more information from the high and the mighty by chatting over the phone for five minutes rather than engaging in a media scrum in the mountains.

Do you suppose they still have a Youth Hostel in Davos? I think I left my sunglasses there….55 years ago!

“If you have the word “broker” in your job title the Internet is going to disintermediate you,” said Scott McNealy, founder of Sun Microsystems.

Global Market Comments

January 18, 2024

Fiat Lux

Featured Trade:

(MY 20 RULES FOR TRADING IN 2024)

Nothing like starting the new year by going back to basics and reviewing the rules that worked so well for us in 2023. Call this the refresher course for Trading 101.

I usually try to catch three or four trend changes a year, which might generate 100-200 trades and often come in frenzied bursts. In 2023, there were exactly two great entry points for stocks, the breakout of the regional banking crisis on March 15 and the peak fears of “higher for longer” on October 16.

Since I am one of the greatest tightwads that ever walked the planet, I only like to buy positions when we are at the height of despair and despondency, and traders are raining off the Golden Gate Bridge.

Similarly, I only like to sell when the markets are tripping on steroids and ecstasy and traders are convinced that they can live forever.

Some 99% of the time, the markets are in the middle, and there is nothing to do but do deep research and build shopping lists for the next trade. That is the purpose of this letter.

Over the five decades that I have been trading, I have learned a number of tried and true rules which have saved my bacon countless times. I will share them with you today.

1) Don’t over trade. This is the number one reason why individual investors lose money. Look at your trades of the past year and apply the 90/10 rule. Dump the least profitable 90% and watch your performance skyrocket. Then aim for that 10%. Over-trading is a great early retirement plan for your broker, not you.

2) Always use stops. Risk control is the measure of a good hedge fund trader. If you lose all your capital on the lemons, you can’t play when the great trades are set up. Consider cash as having an option value.

3) Don’t forget to sell. Date, don’t marry your positions. Remember, hogs get fed and pigs get slaughtered. My late mentor, Barton Biggs, told me to always leave the last 10% of a move for the next guy.

4) You don’t have to be a genius to play this game. If that was required, Wall Street would have run out of players a long time ago.

If you employ risk control and stop, then you can be wrong 40% of the time, and still make a living. That’s a little better than a coin toss. If you are wrong only 30% of the time, you can make millions.

If you are wrong a scant 20% of the time, you are heading a trading desk at Goldman Sachs. If you are wrong a scant 10% of the time, you are running a $20 billion hedge fund that the public only hears about when you pay $100 million for a pickled shark at a modern art auction.

If someone says they are never wrong, as is often claimed on the Internet, run a mile, because it is impossible. By the way, I was wrong 15% of the time in 2013. That’s what you’re paying for.

5) This is hard work. Trading attracts a lot of wide-eyed, naïve, but lazy people because it appears so easy from the outside. You buy a stock, watch it go up, and make money. How hard is that?

The reality is that successful investing requires twice as much work as a normal job. The more research you put into a trade, the more comfortable you will become, and the more profitable it will be. That’s what this letter is for.

6) Don’t chase the market. If you do, it will turn back and bite you. Wait for it to come to you. If you miss the train, there will be another one along in minutes, hours, days, weeks, or months. Patience is a virtue.

7) Limit Your Losses. When I put on a position, I calculate how much I am willing to lose to keep it. I then put a stop just below there. If I get triggered, I just walk away. Emotion never enters the equation.

Only enter a trade when the risk/ reward is in your favor. You can start at 3:1. That means only risk a dollar to potentially make three.

8) Don’t confuse a bull market with brilliance. I am not smart, just old as dirt.

9) Tape this quote from the great economist and early hedge fund trader of the 1930s, John Maynard Keynes, to your computer monitor: "Markets can remain illogical longer than you can remain solvent." Hang around long enough, and you will see this proven time and again (ten-year Treasuries at 1.38%?!).

10) Don’t believe the media. I know, I used to be one of them. Look for the hard data, the numbers, and you’ll see that often the talking heads, the paid industry apologists, and politicians don’t know what they are talking about (the Gulf oil spill will create a dead zone for decades?).

Average out all the public commentary, and half are bullish and half bearish at any given time. The problem is that they never tell you which one is right (that is my job). When they all go one way, the markets usually go in the opposite direction.

11) When you are running a long/short portfolio, 80% of your time is spent managing the shorts. If you don’t want to do the work, then cash beats a short any day of the week.

12) Sometimes the conventional wisdom is right.

13) Invest like a fundamentalist, and execute like a technical analyst. This is what all the pros do.

14) Use technical analysis only, and you will buy every rally, sell every dip, and end up broke. That said, learn what an “outside reversal” is, and who the hell is that Italian guy, Leonardo Fibonacci.

15) The simpler a market approach, the better it works. Everyone talks about “buy low and sell high”, but few do it. All black boxes eventually blow up, if they were ever there in the first place.

16) Markets are made up of people. Understand and anticipate how they think, and you will know what the markets are going to do.

17) Understand what information is in the market and what isn’t and you will make more money.

18) Do the hard trade, the one that everyone tells you that you are “Mad” to do. If you add a position and then throw up on your shoes afterward, then you know you’ve done the right thing. This is why people started calling me “Mad” 40 years ago. (What? Tech stocks were a huge buy the first week of January?).

19) If you are trying to get out of a hole, the first thing to do is quit digging and throw away the shovel. Sell everything. A blank position sheet can be invigorating and illuminating.

20) Making money in the market is an unnatural act, and fights against the tide of evolution.

We humans are predators and hunters evolved to track game on the horizon of an African savanna. Modern humans are maybe 5 million years old, but civilization has been around for only 10,000 years.

Our brains have not had time to make the adjustment. In the market, this means that if a stock has gone up, you believe it will continue to do so.

This is why market tops and bottoms see volume spikes. To make money, you have to go against these innate instincts.

Some people are born with this ability, while others can only learn it through decades of training. I am in the latter group.

Great Hunter, Lousy Trader

Global Market Comments

January 17, 2024

Fiat Lux

Featured Trade:

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

Not a day goes by without me hearing from a reader about the competition.

They previously subscribed to a newsletter that promised a top-drawer education, insider’s insights, and spectacular returns, sometimes 100% or more a month.

“Doubled in a day” is a frequently heard term.

The entry-level costs are only a few bucks, but they are ever teased onward by the “trade of the century”, a certain 100X winner that they will reveal to you only after another upgrade to their service.

Customers eventually spend outrageous amounts of money, $5,000, $10,000, or even $100,000 a year for the service.

They then lose their shirts.

I hear from readers who have gone through as many as ten of these scams before they find me. Some have lost millions of dollars. Others have been wiped out.

The sob stories are legion.

Then, they find the Diary of a Mad Hedge Fund Trader.

This is the source of all those effusive testimonials you find on my website (click here). Believe me, they come in every day. I don’t make this stuff up.

Here is the problem. I work in an industry where 99% of the participants are frauds. They are giant Internet marketing firms with hundreds or thousands of employees.

They spend millions to buy your email address. They then spend millions more on copywriters and programmers to pen and distribute top-rate invitations to you to get rich.

Some of these pitches are so compelling, that even I take a look from time to time. These guys are slick, really slick.

None of these people have ever worked on Wall Street. They have never been employed as traders. They have not even traded for their account.

They would know which end of stock to hold upward if you handed one to them.

For the most part, they are twenty-something kids who got an “A” in creative writing, if they ever went to school. Many haven’t.

So by putting your faith and your wealth in these newsletters and “trade-mentoring” services, you are placing them in the hands of kids without any experience whatsoever.

Hence, the disastrous results. You’d have a better outcome tossing a coin or throwing darts at a dartboard.

Some of the larger service hires washed out have been investment professionals who become the “face” of the company and lend it some bogus credibility.

They know the lingo, can quote you statistics all day long, and may even boast of proprietary models and hidden indicators. But chances are they have never made a trading dollar in their life.

Without exception, they are lightweights, has-beens, and wannabees who failed in the big show. None have ever traded for a living. If they did, they would be broke.

Better to sell the shovels to the gold miners than to try it themselves.

They include the oil newsletter that never saw the crash coming, the fixed income service that is always predicting the return of hyperinflation and a crash, and the perennial prediction that the Dow Average is about to plunge to 3,000.

And because these guys are lousy at their jobs, they always tell you to do THE EXACT OPPOSITE of the right thing to do at market extremes.

Just saw a flash crash? Sell everything! The next crash is here! Just hit a new all-time high? Load the boat! The market is about to double! For them, markets are always about to zero, or to infinity.

Here’s another problem. Negativity outsells a positive outlook hugely, sometimes by 10:1. It makes people look smarter. That’s the source of all of these Armageddon scenarios. They make a ton of money for their purveyors.

It’s not about being right, or dispensing sage advice and proper guidance. It’s only about making a dollar, nothing else. There is no guilt or responsibility involved whatsoever.

All of this is done at your expense. I get emails from victims who sold their houses at the market bottom and want to know what to do now that the house has doubled in value and rents are rising.

There are a lot of people out there who drank the Master Limited Partnership Kool-Aid and put all of their assets there to get double-digit yields. If they are lucky, they are down only 90%.

The precious metal area is a favorite of Internet marketers. Readers who bought this sector on margin, as they were urged to do with great urgency, lost everything.

I know this all sounds like sour grapes coming from me. The sad reality is that out of hundreds of competing investment and trading newsletters in the industry, I can count on one hand those run by true professionals, and I know most of them.

The rest are all crooks.

Yes, I know who these people are. But I am not going to name any names. No time to sling mud here. I can hear the collective sighs of relief already.

This is why I strive to provide the opposite of the con men. To me, it is more important to be right than to be rich. I will give you my unvarnished, undiluted views, even if it is bad for my business, which it often is.

This is why we publish our model trading performance on a daily basis, warts and all.

Notice that no other newsletter does this. If they did, they would only show huge losses, which don’t sell well. It’s all about making tons of incredible claims without a shred of documentation.

So please continue trolling the web for new investment insights and trading opportunities. After all, that’s how you found me all those years ago. But I will give you a piece of advice:

Caveat emptor!

Buyer beware!