Global Market Comments

May 13, 2020

Fiat Lux

Featured Trade:

(HERE’S AN EASY WAY TO PLAY ARTIFICIAL INTELLIGENCE),

(BOTZ), (NVDA), (ISRG)

Global Market Comments

May 13, 2020

Fiat Lux

Featured Trade:

(HERE’S AN EASY WAY TO PLAY ARTIFICIAL INTELLIGENCE),

(BOTZ), (NVDA), (ISRG)

We are now in the throes of a market correction that could last anywhere from a couple of weeks more to a couple of months. So, generational opportunities are starting to open up in some of the best long term market sectors.

Suppose there was an exchange-traded fund that focused on the single most important technology trend in the world today.

You might think that I was smoking California’s largest export (it’s not grapes). But such a fund DOES

The Global X Robotics & Artificial Intelligence ETF (BOTZ) drops a golden opportunity into investors’ laps as a way to capture part of the growing movement behind automation.

The fund currently has an impressive $2.2 billion in assets under management.

The universal trend of preferring automation over human labor is spreading with each passing day. Suffice to say, there is the unfortunate emotional element of sacking a human and the negative knock-on effect to the local community like in Detroit, Michigan.

But simply put, robots do a better job, don’t complain, don’t fall ill, don’t join unions, or don’t ask for pay raises. It’s all very much a capitalist’s dream come true.

Instead of dallying around in single stock symbols, now is the time to seize the moment and take advantage of the single seminal trend of our lifetime.

No, it’s not online dating, gambling, or bitcoin, it’s Artificial Intelligence.

Selecting individual stocks that are purely exposed to A.I. is a challenging endeavor. Companies need a way to generate returns to shareholders first and foremost, hence, most pure A.I. plays do not exist right now.

However, the Mad Hedge Fund Trader has found the most unadulterated A.I. play out there. A real diamond in the rough.

The best way to expose yourself to this A.I. trend is through Global X Robotics & Artificial Intelligence ETF (BOTZ).

This ETF tracks the price and yield performance of ten crucial companies that sit on the forefront of the A.I. and robotic development curve. It invests at least 80% of its total assets in the securities of the underlying index. The expense ratio is only 0.68%.

Another caveat is that the underlying companies are only derived from developed countries. Out of the 10 disclosed largest holdings, seven are from Japan, two are from Silicon Valley, and one, ABB Group, is a Swedish-Swiss multinational headquartered in Zurich, Switzerland.

Robotics and A.I. walk hand in hand, and robotics are entirely dependent on the germination prospects of A.I. Without A.I., robots are just a clunk of heavy metal.

Robots require a high level of A.I. to meld seamlessly into our workforce. The stronger the A.I. functions, the stronger the robot’s ability, filtering down to the bottom line.

A.I.-embedded robots are especially prevalent in the military, car manufacturing, and heavy machinery. The industrial robot industry projects to reach $80 billion per year in sales by 2024 as more of the workforce gradually becomes automated.

The robotics industry has become so prominent in the automotive industry that they constitute greater than 50% of robot investments in America.

Let’s get the ball rolling and familiarize readers of the Mad Hedge Technology Letter with the top 5 weightings in the underlying ETF (BOTZ).

Nvidia (NVDA)

Nvidia Corporation is a company I often write about as their main business is producing GPU chips for the video game industry.

This Santa Clara, California-based company is spearheading the next wave of A.I. advancement by focusing on autonomous vehicle technology and A.I.-integrated cloud data centers as their next cash cow.

All these new groundbreaking technologies require ample amounts of GPU chips. Consumers will eventually cohabitate with state of the art IOT products (internet of things), fueled by GPU chips, coming to mass market like the Apple Homepod.

The company is led by genius Jensen Huang, a Taiwanese American, who cut his teeth as a microprocessor designer at competitor Advanced Micro Devices (AMD).

Nvidia constitutes a hefty 8.70% of the BOTZ ETF.

To visit their website, please click here.

Yaskawa Electric (Japan)

Yaskawa Electric is the world's largest manufacturer of AC Inverter Drives, Servo and Motion Control, and Robotics Automation Systems, headquartered in Kitakyushu, Japan.

It is a company I know well, having covered this former zaibatsu company as a budding young analyst in Japan 45 years ago.

Yaskawa has fully committed to improving global productivity through automation. It comprises the 2nd largest portion of BOTZ at 8.35%.

To visit Yaskawa’s website, please click here.

Fanuc Corp. (Japan)

The 3rd largest portion in the (BOTZ) ETF at 7.78% is Fanuc Corp. This company provides automation products and computer numerical control systems, headquartered in Oshino, Yamanashi.

Fanuc was one of the hot robotics companies I used to trade in during the 1970s and I have visited their main factory many times.

They were once a subsidiary of Fujitsu, which focused on the field of numerical control. The bulk of their business is done with American and Japanese automakers and electronics manufacturers.

They have snapped up 65% of the worldwide market in the computerized numerical device market (CNC). Fanuc has branch offices in 46 different countries.

To visit their company website, please click here.

Intuitive Surgical (ISRG)

Intuitive Surgical Inc (ISRG) trades on Nasdaq and is located in sun-drenched Sunnyvale, California.

This local firm designs, manufactures, and markets surgical systems and is completely industriously focused on the medical industry.

The company's da Vinci Surgical System converts surgeon's hand movements into corresponding micro-movements of instruments positioned inside the patient.

The products include surgeon's consoles, patient-side carts, 3D vision systems, da Vinci skills simulators, da Vinci Xi integrated table motions.

This company comprises 7.60% of BOTZ. To visit their website, please click here.

Keyence Corp (Japan)

Keyence Corp is the leading supplier of automation sensors, vision systems, barcode readers, laser markers, measuring instruments, and digital microscope.

They offer a full array of service support and closely work with customers to guarantee full functionality and operation of the equipment. Their technical staff and sales teams add value to the company by cooperating with its buyers.

They have been consistently ranked as the top 10 best companies in Japan and boast an eye-opening 50% operating margin.

They are headquartered in Osaka, Japan and make up 7.54% of the BOTZ ETF.

To visit their website, please click here.

(BOTZ) does have some pros and cons. The best AI plays are either still private at the venture capital level or have already been taken over by giant firms like NVIDIA.

You also need to have a pretty broad definition of AI to bring together enough companies to make up a decent ETF.

However, it does get you a cheap entry into many for the illiquid foreign names in this fund.

Automation is one of the reasons why this is turning into the deflationary century and I recommend all readers who don’t own their own robotic-led business pick up some Global X Robotics & Artificial Intelligence ETF (BOTZ).

And by the way, the entry point right here on the charts is almost perfect.

To learn more about (BOTZ), please visit their website by clicking here.

Global Market Comments

May 12, 2020

Fiat Lux

Featured Trade:

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM TRIPLED MY PERFORMANCE)

I couldn’t believe my eyes.

Upon analyzing my performance data for the past year, it couldn’t be clearer.

After three years of battle testing, the algorithm has earned its stripes. I started posting it at the top of every newsletter and Trade Alert last year and will continue to do so in the future.

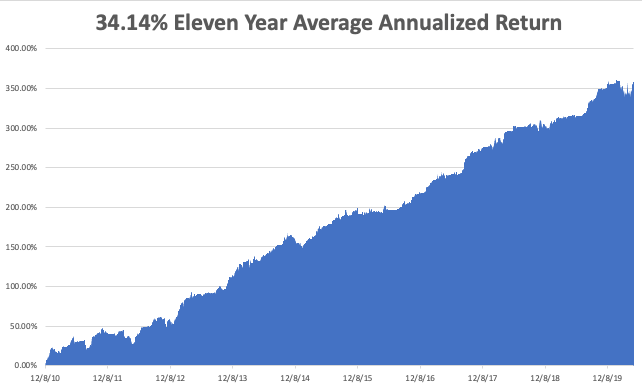

Once I implemented my proprietary Mad Hedge Market Timing Index in October 2016, the average annualized performance of my Trade Alert service has soared to an eye-popping 34.14%.

As a result, new subscribers have been beating down the doors trying to get in.

Let me list the highpoints of having a friendly algorithm looking over your shoulder on every trade.

*Algorithms have become so dominant in the market, accounting for up to 80% of total trading volume, that you should never trade without one

*It does the work of a seasoned 100-man research department in seconds

*It runs real-time and optimizes returns with the addition of every new data point far faster than any human can. Imagine a trading strategy that updates itself 30 times a day!

*It is artificial intelligence-driven and self-learning.

*Don’t go to a gunfight with a knife. If you are trading against algos alone,

you WILL lose!

*Algorithms provide you with a defined systematic trading discipline that will enhance your profits.

And here’s the amazing thing. My Mad Hedge Market Timing Index correctly predicted the outcome of the presidential election, while I got it dead wrong.

You saw this in stocks like US Steel, which took off like a scalded chimp the week before the election.

When my and the Market Timing Index’s views sharply diverge, I go into cash rather than bet against it.

Since then, my Trade Alert performance has been on an absolute tear. In 2017, we earned an eye-popping 57.39%. In 2018, I clocked 23.67% while the Dow Average was down 8%, a beat of 31%. In 2019, I clocked a blockbuster 56%

Here are just a handful of some of the elements which the Mad Hedge Market Timing Index analysis in real-time, 24/7.

50 and 200-day moving averages across all markets and industries

The Volatility Index (VIX)

The junk bond (JNK)/US Treasury bond spread (TLT)

Stocks hitting 52-day highs versus 52-day lows

McClellan Volume Summation Index

20-day stock bond performance spread

5-day put/call ratio

Stocks with rising versus falling volume

Relative Strength Indicator

12-month US GDP Trend

Case Shiller S&P 500 National Home Price Index

Of course, the Trade Alert service is not entirely algorithm-driven. It is just one tool to use among many others.

Yes, 50 years of experience trading the markets is still worth quite a lot.

I plan to constantly revise and upgrade the algorithm that drives the Mad Hedge Market Timing Index continuously, as new data sets become available.

Obviously, in light of the recent stock market crash, a ton of new valuable data is available for which my algo can mine.

Global Market Comments

May 11, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT GOLDEN AGE HAS ALREADY STARTED)

(TLT), (TBT), (SPY), (INDU), (VIX),

(DAL), (BRK/A), (LUV), (AA), (UAL)

I always get my best ideas when hiking up a steep mountain carrying a heavy backpack.

Yesterday, I was just passing through the 9,000-foot level on the Tahoe Rim Trail when suddenly, the fog lifted and the skies cleared. I was hit with an epiphany.

It was my “AHA” moment.

The next American Golden Age, the next Roaring Twenties, started on March 23.

However, you have to dive deep into investor psychology to reach that astonishing conclusion.

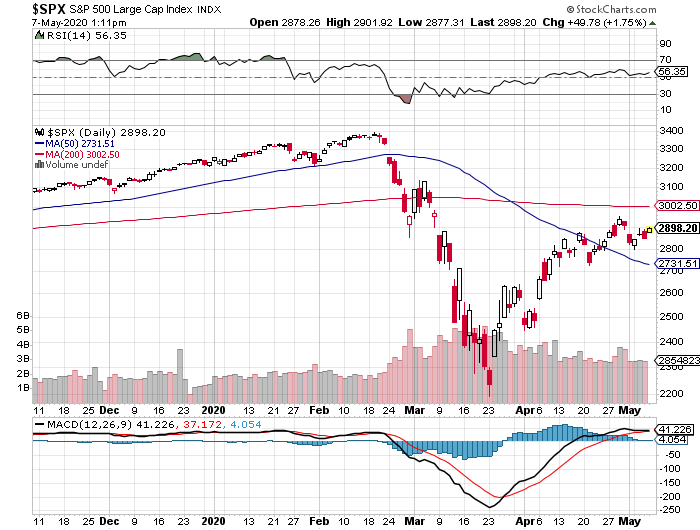

The conundrum of the day is why stocks are trading at a plus 30X multiple two months into a Great Depression. The economic data has been so horrific that the mainstream news has been reporting them.

Some 30 million unemployed on the way to 51 million? Those are Fed numbers, not mine (click here for the link ). Over 52% of small businesses going bankrupt in the next six months? A GDP that is shrinking at an amazing -40% annualized rate?

Yet, we have a Dow Average that has risen a breathtaking 38% in six weeks. The market has essentially dropped 38% and risen 38% over three months, with the Volatility Index (VIX) making a brief visit to the $80 handle.

To understand these massive contradictions, you have to understand what investors think they are buying. They are not hoovering up stocks that are cheap, offer value, or at the bottom of an economic cycle.

Instead, they are investing in a hope, a vision, an expectation that the coming decade will bring a major economic boom. Yes, they are buying my coming American Golden Age.

Only 10% of the value of a stock is reflected in current year earnings, according to Dr. Jeremy Siegal at the Wharton School of Economics (click here to go to the site). The other 90% is in the following nine years. Investors have written off this year’s earnings and are paying up for the following nine.

Long term followers of this newsletter are well aware of my approaching forecast of the next Roaring Twenties (click here for the link).

Except that this time we have a catapult, the pump-priming effects of the pandemic. The government has stepped in with $14 trillion worth of fiscal and monetary stimulus. Creative destruction is taking place at an exponential rate. Companies have to become hyper-efficient overnight or die.

It’s not rocket science. More than 85 million millennials are aging into their peak spending years, buying homes, cars, and all the luxuries of life. Every time this has happened for the past century, US economic growth leaped to 4%.

It happened in the 1920s, the 1960s, the 1990s, and is about to take place in the 2020s. And with each pop in growth, the stock market rises about 400%. Look at your long-term charts and you’ll see I’m dead right.

That takes us from the March 23 Dow Average low at 18,000 up to 72,000 by 2030, except that it’s a low number. Throw in the hyper-acceleration of innovation by the technology and biotech sectors, a Dow 120,000 is within reach.

You may recall that number from my marketing pitches, except that this time it’s happening. In a decade you are going to look like an absolute genius by following the recommendation of the Mad Hedge Fund Trader.

It also means that we may not see market corrections of any more than 10% this year. That would take us down to a Dow Average of 22,500, and an (SPX) of 2,600 in the coming months. That’s where you should jump in and buy with both hands. The only way I would be wrong is if the US epidemic explodes to unimaginable levels, which is not impossible.

Last week, U-6 unemployment rates exploding to a stratospheric 22.8%. The rate was far higher among high school graduates, but only 8% for college grads. Some 20.2 million lost jobs, ten times the previous record, and more than seen during the Great Depression. The BLS (click here) said the true figure was probably 5% higher due to counting anomalies and a huge backlog of data. And this is just the beginning. The good news is that next month, only 10 million jobs will be lost.

NASDAQ (QQQ) turned positive for 2020, and the followers who piled into tech LEAPS at the March bottom are eternally grateful. Tech and biotech are the only places to be. Everywhere else is a waste of time and money. The entire country is turning into a tech economy or going out of business. Buy tech on dips.

Warren Buffet sold all his airline shares, taking a major loss, including Delta (DAL), Southwest (LUV), American (AA) and United (UAL). The Fed’s $50 billion airline bailout blocked him from making a real killing. His Berkshire Hathaway (BRK/A) (click here) owned close to 10% of all of them. The complete collapse of tourism and business travel are the issues. He sees no recovery in the foreseeable future. They don’t call him the “Oracle of Omaha” for nothing.

US Auto Sales are down a mind-blowing -48% in April, the worst on record. Only 8.6 million cars were sold in the US against last year’s annual rate of 17 million. Toyota and Honda saw the biggest falls as their ships can’t unload due to lack of storage space.

The US Treasury will borrow $3 Trillion this Quarter to fund the massive bailout programs. Announced programs amount to 20 times the $789 billion 2009 rescue package, which Republicans opposed. I’m increasing my bond shorts. Sell short (TLT) again, even if we don’t get a decent rally. Oh, and Trump is threatening a default too. He doesn’t see the connection.

Bonds crashed on massive issuance, with the Treasury announcing a record 20-year bond floatation. Yields hit a one-month high. With the (TLT) down $18 from its recent high, I am taking profits on my bond shorts. I’ll be selling the next rally….again. This could be my core trade for the next decade.

Consumer Debt soared to $14.3 trillion in Q1, a new all-time high. A lot of people are living on their credit cards right now.

Trump threatens to cancel China trade deal, blaming them for Covid-19, sending stocks into a 400-point dive. The last time he did this, shares plunged 20%. It’s all part of an effort to divert attention from the administration’s disastrous handling of the pandemic. America’s Corona deaths are now 20 times China’s, and they are still an emerging nation. Just what we needed, a renewed trade war on top of a pandemic-caused Great Depression, as if the market needed more uncertainty. Sell rallies in the (SPY)

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years again, up a gob-smacking +6.46%. We are now only 0.65% short of a new all-time high.

My aggressive short bond positions came in big time on the back of theannounced $3 trillion in new debt issuance in Q2. Short bonds are far and away the better quality trade of buying stocks at these elevated levels.

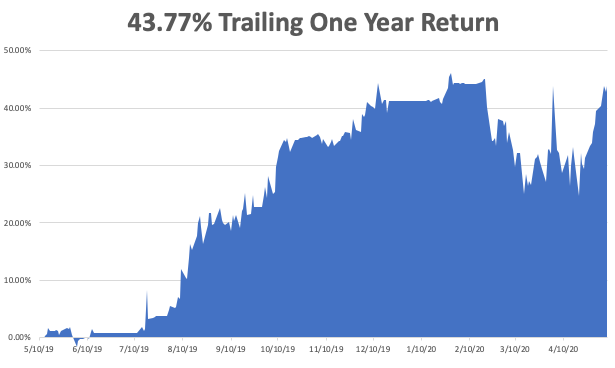

May is up +6.46%, taking my 2020 YTD return up to 2.59%. That compares to a loss for the Dow Average of -13.43% from the February top. My trailing one-year return exploded to 43.77%. My ten-year average annualized profit returned to +34.14%.

This week, Q1 earnings reports continue, and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 11 at 10:00 AM, the April US Inflation Expectations are out. Caesar’s Entertainment (CZR) and Marriot International (MAR) report earnings.

On Tuesday, May 12 at 5:00 PM, the NFIB Small Business Optimism Index for April is released. Toyota Motors (TM) reports earnings.

On Wednesday, May 13 at 9:30 AM, the ever fascinating weekly Cushing Crude Oil Stocks is announced. Cisco Systems (CSCO) reports earnings.

On Thursday, May 14 at 8:30 AM, we get another blockbuster Weekly Jobless Claims. Advanced Micro Devices (AMD) reports earnings.

On Friday, May 15 at 7:30, AM the Empire State Manufacturing Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll continue my solo circumlocution of the 160 mile Tahoe Rim Trail every afternoon in ten-mile segments. Why solo? Do you know anyone else who wants to hike 160 miles at 10,000 feet in two weeks?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 8, 2020

Fiat Lux

Featured Trade:

(MAY 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(UNG), (UAL), (DAL), (INDU), (SPY), (SDS),

(P), (BA), (TWTR), (GLD), (TLT), (TBT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 6 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What broker do you use? The last four bond trades I couldn’t get done.

A: That is purely a function of selling into a falling market. The bond market started to collapse 2 weeks ago. We got into the very beginning of that. We put out seven trade alerts to sell bonds, we’re out of five of them now. And whenever you hit the market with a sell, everyone just automatically drops their bids among the market makers. It’s hard to get an accurate, executable price when a market is falling that fast. The important point is that you were given the right asset class with a ticker symbol and the right direction and that is golden. People who have been with my service for a long time learn how to work around these trade alerts.

Q: Is there any specific catalyst apart from the second wave that will trigger the expected selloff?

A: First of all, if corona deaths go from 2 to 3, 4, 5 thousand a day, that could take us back down to the lows. Also, the market is currently expecting a V-shaped recovery in the economy which is not going to happen. The best we can get is a U-shape and the worst is an L-shape, which is no recovery at all. What if everything opens up and no customers show? This is almost certain to happen in the beginning.

Q: How long will the depression last?

A: Initially, I thought we could get out of this in 3-6 months. As more data comes in and the damage to the economy becomes known, I would say more like 6-9, or even 9-12 months.

Q: In natural gas, the (UNG) chart looks like a bullish breakout. Does it seem like a good trade?

A: No, the energy disaster is far from over. We still have a massive supply/demand gap. And with (UNG), you want to be especially careful because there is an enormous contango—up to 50 or 100% a year—between the spot price and the one-year contract price, which (UNG) owns. Once I saw the spot price of natural gas rise by 40% and the (UNG) fell by 40%. So, you could have a chart on the (UNG) which looks bullish, but the actual spot prices in front month could be bearish. That's almost certainly what’s going to happen. In fact, a lot of people are predicting negative prices again on the June oil contract futures expiration, which comes in a couple of weeks.

Q: What about LEAPS on United (UAL) and Delta (DAL)?

A: I am withdrawing all of my recommendations for LEAPS on the airlines. When Warren Buffet sells a sector for an enormous loss, I'm not inclined to argue with him. It’s really hard to visualize the airlines coming out of this without a complete government takeover and wipeout of all existing equity investors. Airlines have only enough cash to survive, at best, 6-8 months of zero sales, and when they do start up, they will have more virus-related costs, so I would just rather invest in tech stocks. If you’re in, I would get out even if it means taking a loss. They don’t call him the Oracle of Omaha for nothing.

Q: Any reason not to do bullish LEAPS on a selloff?

A: None at all, that is the best thing you can do. And I’m not doing LEAPS right now, I’m putting out lists of LEAPS to buy on a selloff, but I wouldn't be buying any right now. You’d be much better off waiting. Firstly, you get a longer expiration, and secondly, you get a much better price if you could buy a LEAP on a 2,000 or 3,000 point selloff in the Dow Average (INDU).

Q: Would you add the 2X ProShares Ultra Short S&P 500 (SDS) position here if you did not get on the original alert?

A: I would, I would just do a single 10% weighting. But don’t expect too much out of it, maybe you'll get a couple of points. And it’s also a good hedge for any longs you have.

Q: What happens if the second wave in the epidemic is smaller?

A: Second waves are always bigger because they’re starting off with a much larger base. There isn't a scientist out there expecting a smaller second wave than the first one. So, I wouldn't be making any investment bets on that.

Q: Pfizer (P) and others seem close to having a vaccine, moving on to human trials. Does that play into your view?

A: No, because no one has a vaccine that works yet. They may be getting tons of P.R. from the administration about potential vaccines, but the actual fact is that these are much more difficult to develop than most people understand. They have been trying to find an AIDS vaccine for 40 years and a cancer vaccine for 100 years. And it takes a year of testing just to see if they work at all. A bad vaccine could kill off a sizeable chunk of the US population. We’ve been taking flu shots for 30 years and they haven’t eliminated the flu because it keeps evolving, and it looks like coronavirus may be one of those. You may get better antivirals for treatment once you get the disease, but a vaccine is a good time off, if ever.

Q: Is this a good time to buy Boeing (BA)?

A: No, it’s too risky. The administration keeps pushing off the approval date for the 737 MAX because the planes are made in a blue state, Washington. The main customers of (BA), the airlines, are all going broke. I would imagine that their 1,000-plane order book has shrunk considerably. Go buy more tech instead, or a hotel or a home builder if you really want to roll the dice.

Q: How can the market actually drop to the lows, taking massive support from the Fed and further injections into account?

A: I don’t think we will get to new lows, I think we may test the lows. And my argument has been that we give half of the recent gains, which would take us down to 21,000 in the Dow and 2400 in the (SPX). But I've been waiting for a month for that to happen and it's not happening, which is why I've also developed my sideways scenario. That said, a lot of single stocks will go to new all-time lows, such as in retailers (RTF) and airlines (JETS).

Q: Would you stay in a Twitter (TWTR) LEAP?

A: If you have a profit, I would take it.

Q: What about Walt Disney (DIS)?

A: There are so many things wrong with Disney right now. Even though it's a great company for the long term, I'm waiting for more of a selloff, at least another $10. It’s actually rallying today on the earnings report. Around the low $90s I would really love to get into LEAPS on this. I think more bad news has to hit the stock for it to get lower.

Q: Are you continuing to play the (TLT)?

A: Absolutely yes, however, we’re at a level now where I want to take a break, let the market digest its recent fall, see if we can get any kind of a rally to sell into. I’ll sell into the next five-point rally.

Q: Any reason not to do calls outright versus spreads on LEAPS?

A: With LEAPS, because you are long and short, you could take a much larger position and therefore get a much bigger profit on a rise in the stock. Outright calls right now are some of the most expensive they’ve ever been. So, you really need to get something like a $10 or $15 rise in the stock just to break even on the premium that you’re paying. Calls are only good if you expect a very immediate short term move up in the stop in a matter of days. LEAPS you can run for two years.

Q: Is gold (GLD) still a buy?

A: Yes, the fundamental argument for gold is stronger than ever. However, it has been tracking one for one with the stock market lately. That's why I'm staying out of gold—I’d rather wait for a selloff in stocks to take gold down; then I’ll be in there as a buyer.

Q: Should I take profits on what I bought in April and reestablish on a correction?

A: Absolutely. If you have monster profits on a lot of these tech LEAPS you bought in the March/early April lows, then yes, I would take them. I think you will get another shot to buy these cheaper, and by coming out now and coming in later, you get to extend your maturity, which is always good in the LEAPS world.

Q: Would you buy casinos, or is it the same risk as the airlines?

A: I would buy casinos and hotels—they have a greater probability of survival than the airlines and a lot less debt, although they’re going to be losing money for years. I don’t know exactly how the casinos plan on getting out of this.

Q: Should we exit ProShares ultra short 20+ year Treasury Bond Fund (TBT) now?

A: No, that’s more of a longer-term trade. I would hang on to that—you could get from $16 to $20 or $25 in the foreseeable future if our down move in bond continues.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

"No one is line dancing over the fact that the market is at 2,700. No one feels good about it. The market likes to climb a wall of worry, and the stonemason has been hard at work. So I think we continue to grind higher," said Jason Trennert, chief investment strategist at Strategas Research Partners.

Global Market Comments

May 7, 2020

Fiat Lux

Featured Trade:

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD)

(AAPL)

(DINING WITH THE BOTTOM 20%)

(TESTIMONIAL)