Other than that, Mrs. Lincoln, how was the play?

I thought I'd never see a 1987 crash again. But my problem is that I lived too long.

Welcome to the first flash crash of 2018, and probably not the last. And here's the really good news. It's not over!

As I write this, the Volatility Index (VIX) is trading in the aftermarket at $53, up 36% from the close. The Short Volatility ETN that I bought right a the close at $93 is now trading at $16!

Clearly a major short (VIX) player has gone bust, triggering a forced liquidation in the aftermarket. We'll find out who in a couple of days.

This could market the top of the (VIX) and the bottom in stocks once we endure one more horrific opening.

When looking for the guilty party in the mass murder, you have to vote for "All of the above."

The president declassified a memo, despite the FBI announcing in advance that it was false, prompting foreign concerns of an American right wing coup 'd etat. He preceded this with a State of the Union address which could have been lifted from George Orwell's Animal House.

Notice that every selloff started with a big share dump from Europeans concerned about American political risk. Gee, I can't believe I'm saying that.

Fed governor Janet Yellen, the greatest stock market booster of all time, retired on Friday. Markets have a history of greeting new Fed governors with a slap in the face.

The yield on the ten-year Treasury bond yield popped 45 basis points to 2.85% in a month, taking away the punch bowl for many highly leveraged traders.

Then the January Nonfarm Payroll Report revealed the highest wage growth in many years, unleashing inflation fears.

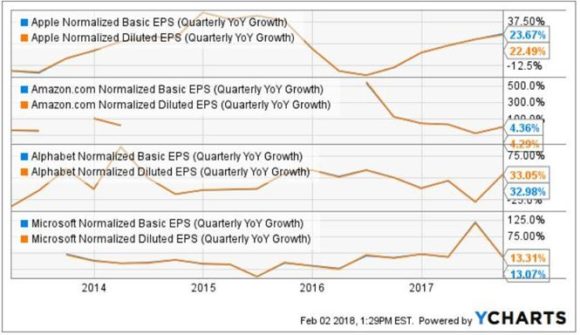

And what about all those share buy backs, a major prop to the market? Sorry, they ain't happening baby, not during the earnings quiet period. Apple shareholders will just have to wait for $270 billion in buying to hit the market.

While you can't swing a dead cat without hitting a victim of the Dow Average's 2,800-point, 10.5% decline, there were several winners.

ETF's traded remarkably well, except for the above noted volatility plays. There were no forced liquidations into penny bids, as we saw with the last flash crash.

And I have to say, the trading strategy of the Mad Hedge Fund Trader has been totally vindicated. Our Trade Alert performance has lost only 3.09% so far in February and is still up +1.00% on the year. And we'll be up in February at the options expiration on Friday next week.

I went into the meltdown with a 50% cash position, and 50% in hedged spreads in options with only 9 days to expiration. I then cut all my higher risk positions right after the Monday opening, when the market was briefly up. My long positions in gold (GLD) and bonds (TLT) actually rose today.

It looks like the harder I work, the luckier I get.

To show you how crazy things got, Yahoo mail was up and down all day, the Interactive Brokers platform regularly crashed every ten minutes, and the data inputs for the Mad Hedge Market Timing Index froze when it hit 40.

When the dust settles, we will be set up for the best buying opportunity of 2018. The market price earnings multiple has just fallen from 19X to 16X, and it may be at 15X before it is all over. That could be right after theTuesday opening.

It is hard to imagine that institutions left behind by the January melt down will ignore this opportunity.

The best thing you can do now is to make lists of stocks to buy at the bottom, focusing on the premier technology names. Recent research names provided by the Mad Hedge Fund Trader would be a good place to start.

Sorry for the short letter today, but I have been working the phones trying to get to the root of things.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader