Global Market Comments

January 4, 2018

Fiat Lux

Featured Trade:

(JANUARY 3 GLOBAL STRATEGY WEBINAR Q&A)

(TESTIMONIAL)

Global Market Comments

January 4, 2018

Fiat Lux

Featured Trade:

(JANUARY 3 GLOBAL STRATEGY WEBINAR Q&A)

(TESTIMONIAL)

Q: Is Apple (AAPL) moving to new highs?

A: The answer is yes, but you're not going to get the same massive returns that you got in 2017 with all of the FANG's.

Q: Will inflation rise in 2018?

A: Yes, but not by much. Technology is still creating giant deflationary headwinds. The only inflationary pressures we'll see is from commodities, energy, and from some wage rises in industries like tech.

Q: Do you see 2, 3, or 4 wage hikes in 2018?

A: I vote for three, but four is an outlier depending on how strong the economy gets.

Q: What do we do about NVIDIA?

A: The answer is to buy it. I was holding on for $160 as an entry point and it's not giving it to us. Long term, I think we have another double here. I spoke to the CEO a few weeks ago and he's wildly bullish about the company. AI is the major driver there and this is a $400 stock someday. They are in the sweet spot for every major trend in technology. Of course, there is some New Year reallocation buying going on now, but you can start dipping your toe in here and add to your position later.

Q: Will Japanese stocks rise fast enough to offset the weakness in the Japanese yen?

A: You could have a situation where they may rise and fall by equal amounts and you end up making no money. The answer is to buy the Wisdom Tree Japan Hedged Equity Fund (DXJ), which buys Japanese stocks and sells short the Japanese yen against it. That way you can play Japan with no yen exposure. It's a way of buying the Japanese stock market in dollar terms. The (DXJ) can add another 20% or 30% this year

Q: The ProShares Ultra Short 20+ Treasury ETF (TBT) is at $34. Do you think it will hit $50?

A: Absolutely yes. We have another 10 points to go at least in the (TBT). And that's the conservative target. The more aggressive one is $60. Ten (TLT) points are worth about 20 (TBT) points because of the 2X leverage in the (TBT). There should be another 50% upside from these levels.

Q: What is the catalyst for long term US bonds to decline?

A: Rising federal deficits and rising US interest rates. It's really that simple, and both of these are sure things.

Q: Will the polar vortex fundamentals helps natural gas prices high?

A: The answer is no. We've had a nice little rally in gas in the last week caused by the polar vortex. I would sell into that. I'm not looking for any sustainable rally in natural gas this year because increased fracking supply generates gas as a byproduct. In fact, it generates more gas than the system can supply. I wouldn't want to mess around with gas when there are so many other better things to do in the stock and bond markets.

Q: AMZN has a forward price earnings multiple of $130 so do you think that's expensive?

A: No, it's not expensive, it's meaningless. Amazon has never had an earnings growth type strategy. They've always been about market share. Amazon profits are about to double with all the things they have going on with Alexa, the cloud, AWS, and so on. Some 25% of all US retail sales went to Amazon in 2017. This is clearly a business that is growing by leaps and bounds. There is another double in Amazon, but I don't necessarily want to buy it today.

Q: I am hearing wildly divergent opinions about TESLA, what is your opinion?

A: That will always be the case. The world is divided into two different types of people; the believer and non-believers in the TESLA vision. Non-believers tend to be Trump type Republicans who see it all as a liberal conspiracy. I can tell you that I have been in the Tesla factory every quarter for the last 8 years, and I can tell you that Tesla is a real company and has real products. As they ramp up to 500,000 units per year, they will take over the world. They will be by far the largest car company in the world in 10 years and many value investors agree with me and have major positions in the stock. So, do not sell short (TSLA) under any circumstance. You will get your head handed to you if you do. Elon Musk loves squeezing shorts and has proved to be one of the most successful short squeezers of all time. Since I have been following the stock since it was $16.50, this has certainly been the case.

Q: Will emerging markets do better than the US markets in 2018?

A: Yes they will. You are really getting a perfect storm for emerging markets. A lower dollar, higher commodity prices, and a global synchronized economic recovery are all positive for emerging markets. Think of them as the small cap stock in the global stock world. They do better in these circumstances so look for them to do better than US stocks in 2018. My favorite is India, and you buy it with the (PIN).

Q: Should markets be worried about North Korea?

A: Forget about it because it's all noise. The two leaders are feeding off of each other using a tweet war to get publicity and public notice. It's all very damaging for the US over the long term and it hurts our long term interests in Asia by lowering us to North Korea's level. But no war will ever happen. North Korea has no ability to wage war, they have no single member in their military who has combat experience, while the US has been at war almost nonstop for the past 40 years. The North Korean missiles which you see on TV almost every day have no targeting system. All they can do is fire them in the air and watch them fall into the ocean. You do not arm those missiles with nuclear warheads, especially when 75% crash on take-off on the people who fired them. It's all a distraction from what is really happening on the geopolitical front and the financial market, which is a global US retreat from its alliances and international relationships. Don't waste any time worrying about North Korea.

Q: What do you think about cannabis stocks?

A: I don't want to touch them because they cannot participate in the banking system. Federal anti drug and money laundering banking laws prevent them from using banks. It's an all cash business or all bitcoin business where money is moved around in suitcases. By the way, these business are now the most heavily taxed businesses in the United States. There were no provisions for cannabis companies in the tax bill. Here in San Francisco, where it just became legal to buy pot for the first time, the sales tax is 35%. This will be a huge earner for the states that sell pot. California is looking to take in $8 billion in cannabis sales tax this year. I would not consider it a valid investment theme. Most people didn't even know that cannabis was illegal in California.

Q: Would you hold the CRISPR stocks like Editas Medicine (EDIT) and Intellia Therapeutics (NTLA) through 2018?

Yes, absolutely. CRISPR will be one of the big stories of 2018. These stocks have basically doubled since i recommended them last summer. You want to hang on to them because CRISPR technology is only just getting started. In the last few weeks, we have seen the first FDA approval of CRISPR generated technologies creating custom cures for rare diseases. Don't get off at the 2nd story of a 100-story elevator ride.

Q: Would an impeachment or resignation be market positive?

A: That could happen because it removes the prospect of impeachment and resignation and makes it a certainty. While it's an unknown, it will act as a greater drag on stocks than a known. I don't think it will happen this year. The Justice Department moves very slowly and we may not start getting investigator Robert Mueller's results until after the November midterm elections where you maybe get a Democratic majority. Then it'll be safe for the FBI to come out of its bunker and make its Russia investigation findings public.

I have always had a passion for the markets and the Mad Hedge Fund Trader gave me the courage to make my first trade. At the time I was unemployed and put in everything I could scrape together - about ten thousand dollars.

For me this was a free education, as the profits would pay for all the books and the fees. My father gave me some money as a gift, while telling me "I was crazy" following "some guy" off the Internet.

Every suggestion I have taken religiously. I follow all your lead indicators from the Shanghai stock market to Dr. Copper and the jobless claims.

Over the last couple of months I have started doing my own successful options trades based on the extra suggestions you give in the webinars and commentaries. Often, I do a trade and ten minutes later an alert comes.

My father who is worried about his future (like so many of us) is now joining the program. I am going to assist him with his first trades.

Another family member has asked me to manage his money. I really feel you are helping me become a hedge fund manager with this fantastic program.

Geoff

London - England

"It's a funny thing about life. If you refuse to accept anything but the best, you very often get it," said British Novelist, Somerset Maugham.

Global Market Comments

January 3, 2018

Fiat Lux

2018 Annual Asset Class Review

A Global Vision

FOR PAID SUBSCRIBERS ONLY

Featured Trade:

(SPX), (QQQQ), (XLF), (XLE), (XLI), (XLY),

(TLT), (TBT), (JNK), (PHB), (HYG), (PCY), (MUB), (HCP)

(FXE), (EUO), (FXC), (FXA), (YCS), (FXY),

(FCX), (VALE), (MOO), (DBA), (MOS), (MON), (AGU), (POT), (PHO), (FIW), (CORN), (WEAT), (JJG)

(DIG), (RIG), (USO), (UNG), (USO), (OXY),

(GLD), (GDX), (SLV),

(ITB), (LEN), (KBH), (PHM)

Global Market Comments

January 2, 2018

Fiat Lux

Featured Trade:

(JANUARY 3 GLOBAL STRATEGY WEBINAR),

(HAS THE WORLD HIT "PEAK DIAMONDS"),

(NILE), (AAL.L),

(THE NEW COLD WAR)

(TESTIMONIAL)

My next global strategy webinar will be held live from San Francisco on Wednesday, January 3 at 12:00 PM EST. Co-hosting the show will be my colleague, Mad Day Trader, Bill Davis.

I'll be giving you my updated outlook on stocks, bonds, commodities, currencies, precious metal, and real estate.

The goal is to find the cheapest assets in the world to buy, the most expensive to sell short, and the appropriate securities with which to take these positions.

I will also be opining on recent political events around the world and the investment implications therein.

I usually include some charts to highlight the most interesting new developments in the capital markets. There will be a live chat window with which you can pose your own questions.

The webinar will last 45 minutes to an hour. International readers who are unable to participate in the webinar live will find it posted on my website within a few hours.

I look forward to hearing from you.

To register for the webinar, please click the link we emailed you entitled "Mad Hedge Fund Trader Bi-Weekly Webinar - 1/3/2018" or click here

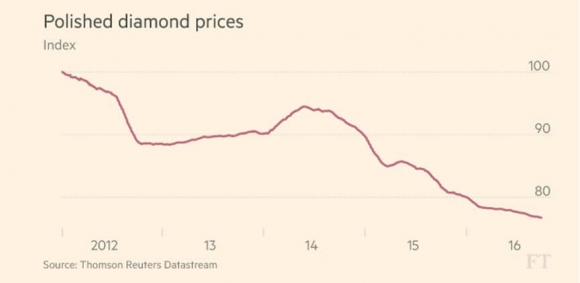

Is the world running out of diamonds?

No, it's worse.

The world is running out of diamond demand.

That is the only conclusion one can reach when looking at the chart below for polished diamonds for the past four years showing a 25% decline.

The diamond industry now produced 125 million carats a year, well down from 187 million ten years ago.

This is clearly not your father's diamond market.

In the old days you could rely on this highly concentrated form of carbon to appreciate an average of 5% a year over the long term.

Just for fun, I recently appraised the diamond I bought for my late wife, which I bought from a Hasidic Jew in an alley off of Manhattan's West 47th street. He kept his inventory hidden in an envelope in his sock.

How times have changed!

The two-carat, VVS1, round cut, yellow diamond that I paid $3,000 for in 1977, would fetch $39,800 today. Great trade!

However, now the rock solid investment thesis that underlay diamonds for so long is now turning to sand.

The problem is the millennial generation, which fails to see the value in the sparkly rocks seen by previous generations. Their discretionary spending instead goes into the latest electronic device, game, or Tesla.

Indeed, there is far more competition for the luxury dollar than in the past.

A luxury "glamping" safari in an African game reserve can easily set you back $30,000, the cost of in investment grade two carat diamond ring today. So will the private jet to get you there.

Kids this age are still about ten years away from when incomes, family formation, and spending patterns start to favor diamonds.

That leaves the current Gen Xers to support the market. However, there are only 65 million of them, compared to 85 million Millennials. Hence the softness in prices.

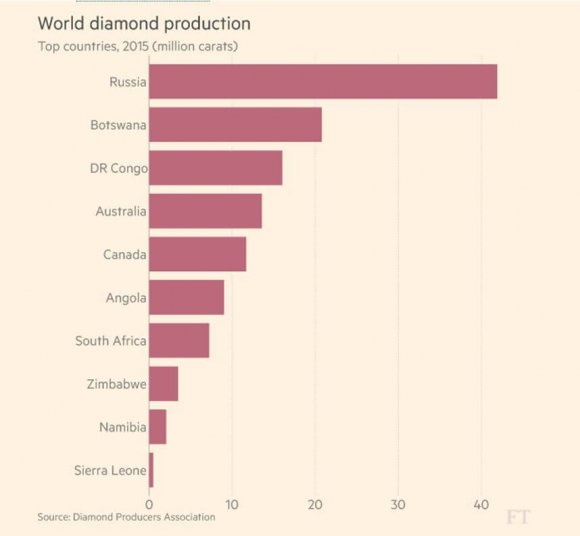

In 2015, global sales of diamond jewelry fell by 2% to $79 billion, the first decline in six years. Sales of rough diamonds plunged by 30% as dealers cut inventories in a soft market.

Structural changes in the industry are also having an impact.

DeBeers had a 90% world market share during the 1980's, and spend massively on advertising its product, some $200 million a year.

Now they account for only 31%, and the advertising spend has similarly withered.

Another problem is that the buyers of the very large diamonds in the Middle east have seen oil incomes shrink beyond imagination.

Industry analysts were shocked when the Lucara Diamond, at 1,109 carats the largest discovered in 100 years, failed to sell at auction in June.

Government anti-corruption efforts in China have had a similar drag.

And lets face it. The diamond industry has not exactly been at the cutting edge of technology.

Stodgy marketing strategies enabled Internet start-ups like Blue Nile (NILE) to come out of nowhere and seize an important part of the retails trade. (NILE) recently announced blockbuster sales that took is stock up an eye popping 35% in a single day.

In 2011, Anglo American took control of the Oppenheimer family owned DeBeers for $5.1 billion.

Another problem can be found in the middle tier of the diamond market, the so called "sightholders." These are the dealers, cutters, and retailers largely based in Antwerp, Belgium (great moules mariniere there by the way).

Since the 2008 financial crisis, banks have withdrawn loans from the industry, citing secrecy and the lack of transparency. This has lead to a wave of bankruptcies of small firms, and the consolidation of the rest.

Industry veterans are still optimistic about the future.

The US accounts for about half the world market, so the new frugality will be a challenge. Perhaps Trump inspired inflation will jolt this market back to life.

As standards of living steadily rise in China and India, and more western social practices are adopted, so should diamond consumption.

This could also be the greatest Millennial play of all time. If the past is any guide, Millennials DO eventually adopt their parents spending patterns.

They just do it much later than we did, another possible outcome of the financial crisis.

To avoid a week on the sofa, you might even think about buying next year's Valentine's surprise early, like NOW.

My friend, Ian Bremmer of the Eurasia Group, a global risk analyst who I regularly follow, has published an outstanding book entitled The End of the Free Markets: Who Wins the War Between States and Corporations.

I find this highly depressing, as it takes me as long to read one of Ian's books as it takes him to write another one. To read a review of his highly insightful tome published in 2008, The Fat Tail: The Power of Political Knowledge for Strategic Investing, please click here.

The world is reaching a tipping point. For the past 40 years, global multinationals with unfettered access to capital, consumer, and labor markets have driven the world economy. There is now a new competitor on the scene, the "state capitalist," where political considerations trump economic ones in the allocation of resources.

Of course, China is the main player, joined by several other emerging nations. The Middle Kingdom has posted double-digit annual growth for the past 30 years without freedom of speech, economic rules of the road, and independent judiciary, and credible property rights.

China's leadership is clearly worried that Western style freedoms will enable wealth to be generated outside their control and be used to orchestrate their overthrow.

Private Western companies can only engage in transactions, which stand on their own economically and deliver the short-term profits, which their shareholders demand.

In China, long-term political goals enable them to pay through the nose to obtain stable supplies of oil, gas, minerals, and materials. That keeps the country's massive work force employed, off the streets, and politically neutered.

The bottom line is that there are now two competing forms of capitalism. The recent financial crisis has accelerated their entrance to the global stage, moving us from a G7 to a G20 dominated world.

Globalization is not ending, but it is definitely entering a new chapter. For those of us who read tea leaves to ascertain major, market moving economic trends, this will be a must read. To buy the book at Amazon, please click here.

"Liquidity is a coward. It's never around when you need it." said market commentator, Jeff Saut.