Come join me in the grand appointments of the Cunard Line's flagship, the elegant and spacious Queen Mary 2, on an eastbound transatlantic cruise.

The ship departs New York at 10:00 AM on July 6, 2018 and arrives at Southampton on July 13. There I will be conducting the Mad Hedge Fund Trader's Strategy Update, a three-hour discussion on the global financial markets.

I'll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, energy, and real estate. I'll highlight the best long and short opportunities.

And to keep you in suspense, I'll be tossing a few surprises out there, too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $300 for the seminar only.

Attendees will be responsible for booking their own cabin through Cunard. They offer everything from an inside stateroom from $999 per person to $26,780 for a Q1 deluxe two-bedroom apartment with its own gym.

Just visit the Cunard website or call them directly at 800-728-6273 to make your own arrangements.

The weather this time of year can range from balmy to tempestuous, depending on our luck. A brisk walk three times around the boat deck adds up to a mile. Full Internet access will be available, for a price, to follow the markets.

Every dinner during the voyage will be black tie, so you might want to stop at Saks Fifth Avenue in Manhattan to get fitted for a second and third tux. Don't forget to bring your Dramamine and sea legs, although the 151,400 ton, 1,132-foot-long $900 million ship is so big I doubt you'll need them. The Queen Mary 2 just completed a major refit in Germany, so everything is brand new.

The event will be held at a luxurious penthouse suite on the ship's highest deck, the details of which will be emailed to you with your purchase confirmation. To instill us all with a proper sense of humility, I will conduct the seminar as we sail over the wreck of the Titanic. The ship will give a blast of its horn three times as a salute as we pass the site.

I look forward to meeting you and thank you for supporting my research.

To purchase tickets for the seminar alone, CLICK HERE.

That was the most boring week of 2018.

Not only did we get no net movement; the range was an infinitesimal 200 Dow points. It was hardly enough to make a dog's breakfast.

Of course, the big news was the yield on the 10-year U.S. Treasury bond (TLT), which rose to 3.12%, a seven-year high. You might have expected this to prompt a complete stock market rout. It didn't. Maybe that is next week's business.

It is rare that the bullish and bearish arguments reach a perfect balance, but that is what we got. In the meantime, trading volume is shrinking, never a good sign. Will the last one to leave please shut out the lights?

Which is all an indication of what I have been warning you about for months. This is setting up to be a dreadful summer. If you've already made your year, with a 19.88% gain like I have, you're better off taking a long cruise than trying to outsmart the algorithms.

I managed to squeeze off only one trade so far this month. I sold short the S&P 500 (SPY) right at the high of the week. However, when the downside momentum failed, and a Volatility Index (VIX) spike failed to confirm, I bailed for a small profit. Pickings are indeed thin.

Whenever my trading slows down, I get the inevitable customer complaints. My answer is always the same. Reach for the marginal trade and you will get your fingers bit off. Don't be in such a hurry to lose money. As my wise Latin professor used to say, "Festina lente," or "make haste slowly."

My May return is +0.53%, my year-to-date return stands at a robust 19.83%, my trailing one-year return has risen to 56.25%, and my eight-year profit sits at a 296.30% apex.

And remember, the market is making this move in the face of rising oil prices and interest rates, always bull market killers.

To mix a few metaphors, when the sun, moon, and stars line up once again I'll go pedal to the metal with the Trade Alerts once again.

If you held a gun to my head and ordered me to tell you how the markets will play out for the rest of the year, try this.

We remain is this narrowing trading range for months, ending with a final decisive break of the 200-day moving average to the downside, now at 23,909. But we find a new low only 1,000 points, or 4% below that.

Then we launch into the post midterm election year-end rally, which could take stocks up 15% to 20% from the 23,000 low. This is why I have been saying that the best trades of 2018 are ahead of us.

So, renew that subscription!

To witness how cruel and stock specific the current market is, look no further than hapless Campbell Soup (CPB), the first ticker symbol I have had to look up this year. There is probably not a reader alive who was not nursed back to health by its iconic red canned chicken noodle soup.

A surprise earnings loss triggered a hellacious 14% one-day plunge. It is the first big victim of the new steel tariffs. Although it amounts to only a few pennies a can, that can be disastrous in this hyper-competitive world. It also turns out that Millennials prefer eating fresh food rather that the canned stuff.

Give thanks for small mercies. With three daughters I am at ultimate risk for a tab for three weddings. The nuptials for Meghan Markle and Prince Harry are thought to cost $45 million, most of it on security. Hopefully I will not someday become the father-in-law of a prince.

This coming week has a plethora of Fed speakers, some key housing numbers, and that's about it.

On Monday, May 21, at 8:30 AM, we get April Chicago Fed National Activity Index.

On Tuesday, May 22, nothing of note is announced.

On Wednesday, May 23, at 10:00 AM, the April New Home Sales.

Thursday, May 24, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a rise of 11,000 last week from a 43-year low. At 10:00 AM, we get April Existing Home Sales.

On Friday, May 25, at 8:30 AM EST, we get April Durable Goods Orders.

We wrap up with the Baker Hughes Rig Count at 1:00 PM EST.

As for me, I will be spending the weekend putting the finishing touches on my 2018 Mad Hedge European Tour.

Thanks to rising U.S. interest rates and a strong dollar, the price of a continental trip has dropped about 10% since the beginning of the year. Got to love that Swiss franc at 1:1 parity with the greenback. Maybe I can afford an extra cheese fondue.

Good Luck and Good Trading.

Yes, It All Looks Like Magic

Global Market Comments

May 18, 2018

Fiat Lux

Featured Trade:

(THEY'RE NOT MAKING AMERICANS ANYMORE),

(THE DEATH OF THE FINANCIAL ADVISOR)

Global Market Comments

May 17, 2018

Fiat Lux

Featured Trade:

(WHY THE "MIDTERM EFFECT" RULES THE MARKETS),

(WHO SAYS THERE AREN'T ANY GOOD JOBS?),

(TESTIMONIAL)

If I had a dime for every trading nostrum I have heard over the past 50 years I would be as rich as Croesus by now. And here's a whopper for you.

A 20% corporate growth rate, a 2% inflation rate, and a 0% stock market: These are numbers you never would expect to see in the same sentence.

Yet, that is what we have at the close today, believe it or not.

And what's worse, this condition could last for another five months. It is clear that something is going on here.

For the past six months, my trading has been wildly successful betting that the stock market would go nowhere until the November 6 midterm elections.

While we have covered an awful lot of ground during this time with a very wide 3,300-point range in the Dow Average (INDU), we have gone absolutely nowhere. As a result, the Mad Hedge Trade Alert Service stands with a 19.83% so far in 2018.

It turns out that trading around midterm congressional elections is far more successful than any other market traditions, like "Sell in May and go Away." Call it the Midterm Effect.

Since the Dow Average was first created on May 26, 1896, the six months going into a midterm produced a feeble 1.4% gain, while the six months after hauled in a whopping 21.8% increase.

In fact, "Sell in May and go away" only works because of the enormous cyclicality of the Midterm Effect, which takes place only every four years. The other three years of that cycle are usually pretty wishy-washy or go the opposite way. Here we are in mid-May, and so far, the Midterm Effect looks pretty good.

The effect only works for midterm elections. It is much less predictive than the Presidential Election Cycle, another popular piece of folk wisdom.

The reason the Midterm Effect works so well is because of human psychology. Investors absolutely hate uncertainty. They are much more inclined to sit on their hands and do nothing ahead of a major market moving event even one 10 months away, when we entered the current range.

They would much rather pay a premium after an event for any securities they might buy rather than being wrong. Money managers tend to be a conservative lot, and this is how conservatism works.

The outcome of the election would have an enormous effect on corporate earnings. According to PredictIt, an online betting site, there is a 67% chance that the Democrats will take the House in November.

If that occurs, no major changes to the economy nor laws pass for at least two years. If that doesn't occur, the president will have a free hand to pursue his existing policies unfettered. However, the election is not for another five months, and in politics that could be five lifetimes.

So range trading it is. Buy the small dips and sell the small rallies for the foreseeable future. Wake me up around Halloween.

Global Market Comments

May 16, 2018

Fiat Lux

Featured Trade:

(THE LAWSUITS ARE PILING UP ON THE XIV),

(XIV), (VXX),

(KISS THAT UNION JOB GOODBYE),

(TESTIMONIAL)

One of the most painful experiences of my half century long trading life involved the Credit Suisse VelocityShares Daily Inverse VIX Short-Term ETNs (XIV).

I was certain that the Volatility Index (VIX) would peak for the year at the Wednesday, February 5, 8:30 AM market opening. So, I shot out a Trade Alert to place only 10% of your capital into the (XIV), a bet that the (VIX) would fall. There was only a 15-minute window before the market closed during which readers could get in. A few managed to do it.

The (XIV) had just fallen from $147 to $95.00. We got in at $97.08, and it closed the day at $100. The (VIX) closed at $37. And we had made money many times selling short volatility over the past decade on spikes just like this one. The (XIV) had been the fastest growing of 3,500 ETFs over the past five years. So far, so good.

Then an hour after the close, I received an urgent call from a client. The (XIV) was trading at $14. What's up?

My initial instinct was that a major hedge fund had either gone bankrupt or had a margin call and was suffering a forced liquidation in the aftermarket.

Overnight, the (XIV) traded as low as $6.50. I later heard that Credit Suisse itself was the major buyer of volatility in the aftermarket, in fact was the ONLY buyer, and that it was deliberately attempting to bankrupt its own fund to limit its liability. Those in management in Zurich were afraid that if the (VIX) shot up to $100 it might take the entire bank down. In short, they panicked.

The next morning they issued notice that they were closing the fund in 10 days. I was certain that the managers were guilty of insider trading and securities fraud in ordering the emergency short cover, and that it was just a matter of time before the class action suits emerged.

Three months later, the lawsuit has been filed by the Gibbs Law Group in Oakland, CA, in the Southern District of New York for unspecified damages, expenses, and legal fees, with a jury trial demanded.

The last time I was involved with one of these was with the MF Global bankruptcy in 2011, where I and most of the rest of the trading community had an account.

I was initially offered 25 cents on the dollar. I refused, expecting to eventually get paid in full. I knew that the MF assets in question were never lost, they were just caught up in a conflict between U.S. and U.S. bankruptcy law that would eventually be resolved. That is what happened, and I was paid in full three years later.

The (XIV) case is much more complicated because there was a huge real loss, about $2 billion, and it involved complex mathematically constructed derivatives. Since the managers behaved so reprehensibly, and because the evidence of their misdeeds is so overwhelming, it is unlikely that the case will ever come to trial. Instead, there will be an out-of-court settlement.

If the SEC takes action it will further strengthen the plaintiffs' hands. There is currently an investigation of Credit Suisse underway and it ultimately could get banned from doing business in the United States.

My bet is that investors will get at least half their money back, if not more. But it could take years to get it, and in a class action the lawyers get a big chunk of any awards for their efforts, usually one-third. Sometimes, class actions can last as long as 10 years.

As for my own followers, most followed my advice to put no more than 10% of their capital into the trade. As it turned out, they made back the 9% loss in less than a month, half of it through selling volatility short again. But this time I used put spreads on the iPath S&P 500 VIX Short-Term Futures ETN (VXX), a long volatility play that will never go to zero overnight.

To read the suit in its entirety, please click here.

To learn more about the suit, please click here and here.

Or you can call the Gibbs Law Group directly at 510-350-9700. I'm sure they'd love to hear from you.

Trading Volatility Can Be Hazardous to Your Wealth

Global Market Comments

May 15, 2018

Fiat Lux

Featured Trade:

(FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(GET READY FOR THE COMING GOLDEN AGE),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly.

This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call "intergenerational arbitrage" will be the principal impetus. The main reason that we are now enduring two "lost decades" of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million "Gen Xers."

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and "RISK ON" assets such as equities, and more buyers of assisted living facilities, health care, and "RISK OFF" assets such as bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward six years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the "millennial" generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

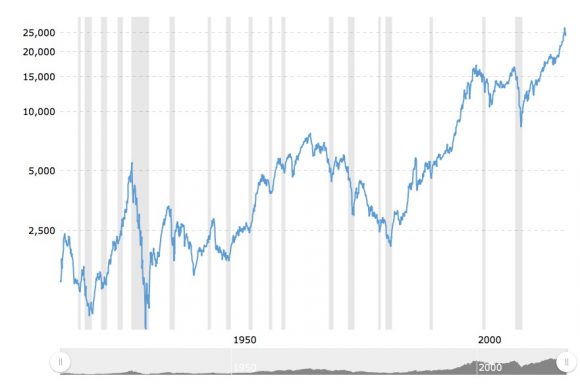

The stock market rockets in this scenario. Share prices may rise very gradually for the rest of the teens as long as tepid 2% growth persists. A 5% annual gain takes the Dow to 28,000 by 2019.

After that, after a brief dip, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 100,000 by 2030. If I'm wrong, it will hit 200,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well.

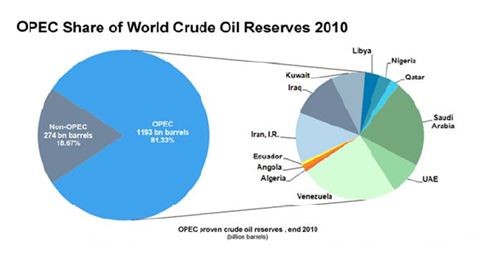

The 100-year supply of natural gas (UNG) we have recently discovered through the new "fracking" technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies.

Since 1995, the United States Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC's share of global reserves is collapsing.

This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.

Mileage for the average U.S. car has jumped from 23 to 24.7 miles per gallon in the past couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low.

Alternative energy technologies will also contribute in an important way in states such as California, accounting for 30% of total electric power generation by 2020, and 50% by 2030.

I now have an all-electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the U.S. from a net importer to an exporter of energy, with hugely positive implications for America's balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term.

That sets up a multiyear short for the world's big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it's great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos.

But at the enterprise level this is enabling speedy improvements in productivity that are filtering down to every business in the U.S., lowering costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area.

This is because the Golden State thumbed its nose at the federal government 10 years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn't afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver's seat on these innovations? The USA.

There is a political element to the new golden age as well. Gridlock in Washington can't last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but for which nobody wants to be blamed.

That means raising the retirement age from 66 to 70 where it belongs and means-testing recipients. Billionaires don't need the maximum $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them. That's why they have recently bought a second used aircraft carrier. The Middle East is now their headache.

The national debt then comes under control, and we don't end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens. The Fed has already told us as much by indicating that the Federal Reserve will only raise interest rates at an infinitesimally slow rate of 25 basis points a quarter.

Sure, this is all very long-term, over-the-horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won't kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

Dow Average 1908-2018

Another American Golden Age is Coming

Global Market Comments

May 14, 2018

Fiat Lux

Featured Trade:

(THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON),

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, OR TAKING ANOTHER BITE AT THE APPLE),

(AAPL),

(FAREWELL TO DAVID ROCKEFELLER)