My tuxes are packed, the hotels are booked, and the limo is waiting outside. The Lear jet is fully fueled up and waiting for me at nearby Buchanan Field, the flight plan already filed. I am taking off for Europe today for a mix of business and pleasure.

Along the way I will be meeting with other hedge fund managers, senior government officials, CEO?s at major banks and Fortune 500 companies, large institutional investors, and a Nobel Prize winner or two. Getting out into the real world and soaking up new data and opinions is invaluable in shaping my own global view, and your performance benefits from it. I don?t find these people walking across my living room, so go out into the world and seek them I must.

I?ll kick off my trip with a strategy luncheon in Chicago on June 29, which is always well attended. Pit traders from the CME should note that tank tops and flip flops are not permitted by the club. With any luck, you will later find me that evening at the Windy City?s Union Station waiting for the overnight train to New York, the famed Lake Shore Limited. I always get a ton of writing done on these long train rides.

The Fourth of July will find me on a reader?s mega yacht watching the fireworks near the Brooklyn Bridge. I hope to reconnect with many old friends at my New York strategy seminar on July 5. The next day I will enjoy the view from my penthouse suite on Cunard?s Queen Mary II as we pass the Statue of Liberty outbound for Southampton, England. Hopefully, those who signed up for my Seminar at Sea are well stocked with motion sickness pills.

In London I?ll catch William Shakespeare?s The Tempest at the Globe Theater, spend an evening at the Royal Ballet, and visit the Royal Academy of Arts Summer Exhibition. At least one morning you will find me catching an old fashioned straight razor shave at the Jermyn Street Barbers, and topping up my supply of business shirts at Turnbull & Asser. The cheese trolley at the Michelin restaurant is to die for.

For accommodations, I?ll be staying at the ever reliable, if not spartan, British Navy Officers Club. You know, the place where Horatio Nelson used to hang out with his pals? After my July 16 London strategy luncheon it will be a race to St. Pancreas Station to catch the Eurostar under the English Channel to Paris.

I will spend the night at the French Army Officers Club. You know, the place where Napoleon killed time with his buddies? Last time I had dinner there, the table on my right saw a group packed with French Air Force officers planning the next NATO air strike on Libya, while the one on my left saw a group negotiating to sell an aircraft carrier to some Chinese admirals. My ears were ringing for a week.

Frankfurt is next on the agenda where I?ll be hosting a strategy lunch on July 18, intermixed with meetings with the CEO?s of major German industrial companies seeking how to navigate the global economy in the ?new normal.? After that, I am counting on my winter of polka instructions to pay off big time.

In the lead up to my July 27 strategy seminar in Zermatt, I?ll be consulting with the representatives of some Middle Eastern royal families while they vacation in the Alps. One afternoon will be devoted to taking the paddle wheel steamer on Lake Geneva to the Chateau de Chillon in Montreux where Lord Byron used to live, sipping fine Swiss white wines along the way.

The high point of my trip, both literally and figuratively, will be my annual assault on the Matterhorn, which at 14,692 feet is higher than anything we have in the continental US. With another year of arduous training under my belt, it?s now or never. I?ll spend my evenings at public steam rooms where, afterwards, I roll around in the snow with the local fr?uleins and beat myself with birch branches. It is invigorating, to say the least. Those Europeans are so open-minded.

The chalet that I have reserved has a granite boulder foundation, an outhouse, and high-speed broadband. I will be ducking out from my mountain hideout only to fly to London for the day from the nearby Swiss Air Force base at Sion on a client?s private jet to attend the opening ceremony for the Olympics.

Next, it?s on to Milan.? If a new Brioni suit and pair of Gucci shoes throw themselves upon me while I stroll through the Galleria I may be unable to resist.

I will be traveling with my laptop and keeping touch with the markets. While 17th and 18th century Internet service is passable, it is unreliable. So unless I see something extraordinary, I will be issuing few new trade alerts. The remaining positions in the model portfolio are best left to ferment over a slow summer and profit from the time decay.

After grinding out more quality content than anyone else on the Internet and maintaining an average annualized 30% return, I deserve a break. The month of May alone saw me shoot out 28 trade alerts, 20 letters, 5 live webinars, and countless radio and TV interviews. I?m basically writing the equivalent of ?War and Peace? every six months. It took Tolstoy ten years to pen his, but then he didn?t have Microsoft Office. I need to spend some time alone on a mountain top, communing with the spirits, attempting to focus on long term financial trends through the smoke and dust.

While on the road, I will be re-running some of my favorite research pieces from the past, interspersed with some new pieces that I will write on the road. This is to expose my thousands of new subscribers to the golden oldies, and to remind the legacy readers who have since forgotten them. I?ll return to my desk in San Francisco full time on August 8.

In the meantime, I shall be raising a glass of vintage Champagne to all of you at dinner as we pass over the Titanic on the 100th anniversary of its sinking, the loyal readers of the Diary of a Mad Hedge Fund Trader. Salut! Prost! And Cheers! I couldn?t do all of this without you. Thank you for my great life!

I?ll Meet You on Top

Buried in the recently passed Dodd-Frank financial reform bill are massive financial rewards for turning in your crooked boss. The SEC is hoping that multimillion dollar rewards amounting to 10%-30% of sanction amounts will drive a stampede of whistleblowers to their doors with evidence of malfeasance and fraud by their employers.

If such rules were in place at the time of the settlement with Goldman Sachs (GS), the bonus, in theory, could have been worth up to $500 million. Wall Street firms are bracing themselves for an onslaught of claims, legitimate and otherwise, by droves of hungry gold diggers looking for an early retirement.

Don't count on this as a get rich quick scheme. Government hurdles to meet the requirement of a true stoolie can be daunting. The standard of evidence demanded is high, and must be matched with the violation of specific federal laws. Idle chit chat at the water cooler won't do. Litigation can stretch out over five years, involve substantial legal costs, and often lead to a non-financial settlement with no reward. For those who do deliver the goods, death threats from defendants are not unheard of.

Having 'rat' on your resume doesn't exactly look inviting either. Just ask Sherron Watkins, the in-house CPA who turned in energy giant Enron's Ken Lay, Andy Fastow, and Jeffrey Skilling just before it crashed in flames. Nearly a decade later, Sherron earns a modest living on the lecture circuit warning of the risks of false accounting, and whistleblowing. There have been no job offers.

The great thing about running an online newsletter is that it is not only self-correcting, it is self-enhancing. Whenever I make a mistake or state a factual error, my inbox catches on fire when corrections, additional data, and chastisements. Ditto when I exclude some key points to bolster my own arguments. So I thought I would publish a letter I received from a reader from the subcontinent regarding yesterday?s piece on ?India is Catching Up With China? (click here).

?Dear Sir,

I am surprised in your comparison with China because you have missed several important points. India is a democracy. It does not have a Ponzi/mafia political party which focuses on looting the nation. Check out the number of billionaires in the Communist Party of China. Patents are relatively much safer in India. The press is free and vibrant. There is no "mad" overcapacity in anything like empty buildings/cities and the like.

The Indian judiciary is slow and generally very fair. India does not have problems of one child policy. Air pollution in Indian cities is probably lower. Most importantly: the fundamentals of the Indian economy in many ways are better than the Chinese. India does not control its currency artificially. There are fewer Indians trying to run out of India than Chinese trying to run out of China. In fact, most Indians can take foreign currency outside the country up to a limit. Few do it in China.?

Regards,

Kshitij Gupta

Here?s the Better Bet

When I first visited Calcutta in 1976, more than 800,000 people were sleeping on the sidewalks, I was hauled everywhere by a very lean, barefoot rickshaw driver, and drinking the water out of a tap was tantamount to committing suicide. Some 36 years later, and the subcontinent is poised to overtake China's white hot growth rate.

My friends at the International Monetary Fund just put out a report predicting that India will grow by 8.5% this year. While the country's total GDP is only a quarter of China's $5 trillion, its growth could exceed that in the Middle Kingdom as early as 2013. Many hedge funds believe that India will be the top growing major emerging market for the next 25 years, and are positioning themselves accordingly.

India certainly has a lot of catching up to do. According to the World Bank, its per capita income is $3,275, compared to $6,800 in China and $46,400 in the US. This is with the two populations close in size, at 1.3 billion for China and 1.2 billion for India.

But India has a number of advantages that China lacks. To paraphrase hockey great, Wayne Gretzky, you want to aim not where the puck is, but where it's going to be. The massive infrastructure projects that have powered much of Chinese growth for the past three decades, such as the Three Gorges Dam, are missing in India. But financing and construction for huge transportation, power generation, water, and pollution control projects are underway.

A large network of private schools is boosting education levels, enabling the country to capitalize on its English language advantage. When planning the expansion of my own business, I was presented with the choice of hiring a website designer here for $60,000 a year, or in India for $5,000. That's why booking a ticket on United Airlines or calling technical support at Dell Computer gets you someone in Bangalore.

India is also a huge winner on the demographic front, with one of the lowest ratios of social service demanding retirees in the world. China's 30 year old 'one child' policy is going to drive it into a wall in ten years, when the number of retirees starts to outnumber their children.

There is one more issue out there that few are talking about. The reform of the Chinese electoral process at the next People's Congress in 2013 could lead to posturing and political instability which the markets could find unsettling. India is the world's largest democracy, and much of its current prosperity can be traced to wide ranging deregulation and modernization than took place 20 years ago.

I have been a big fan of India for a long time, and not just because they constantly help me fix my computers. In August, I recommended Tata Motors (TTM), and it has gone up in a straight line since, instantly making it one of my top picks of the year. On the next decent dip take a look at the Indian ETF's (INP), (PIN), and (EPI).

Better to Own This Pyramid

Than This Pyramid

Taxi! Taxi!

I have spent many hours speaking at length with the generals who are running our wars in the Middle East, like David Petraeus, and James E. Cartwright. To get the boots on the ground view, I attended the graduation of a friend at the Defense Language Institute in Monterey, California, the world's preeminent language training facility.

As I circulated at the reception at the once top secret installation, I heard the same view repeated over and over in the many conversations swirling around me. While we can handily beat armies, defeating an idea is impossible. With the planet's fastest growing population, Muslims are expected to double from one to two billion by 2050, the terrorists can breed replacements faster than we can kill them. The US will have to maintain a military presence in the Middle East for another 100 years. The goal is not to win, but to keep the war at a low cost, slow burn, over there, and away from the US.

I have never met a more determined, disciplined, and motivated group of students. There were seven teachers for 16 students, some with PhD's and all native Arabic speakers. The Defense Department calculates the cost of this 63 week, total emersion course at $200,000 per student.

They are taught not just language, but also the history, culture, and politics of the region as well. I found myself discussing at length the origins of the Sunni/Shiite split in the 7th century, the rise of the Mughals in India in the 16th century, and the fall of the Ottoman Empire after WWI, and this was with a 19 year old private from Kentucky whose previous employment had been at Wal-Mart! I doubt most Americans his age could find the Middle East on a map. Students graduated with near perfect scores. If you fail a class, you get sent to Iraq, unless you are in the Air Force, which kicks you out of the service completely.

As we feasted on hummus and other Arab delicacies, I studied the pictures on the wall describing the early history of the DLI in WWII, and realized that I knew several of the participants. The school was founded in 1941 to train Japanese Americans in their own language to gain an intelligence advantage in the Pacific war. General 'Vinegar Joe' Stillwell said their contribution shortened the war by two years. General Douglas McArthur believed that an army had never before gone to war with so much advance knowledge about its enemy. To this day, the school's motto is 'Yankee Samurai'.

My old friends at the Foreign Correspondents' Club of Japan will remember well the late Al Pinder. He spent the summer of 1941 photographing every Eastern facing beach in Japan, successfully smuggled them out hidden in a chest full of Japanese sex toys. He then spent the rest of the war working for the OSS in China. I know this because I shared a desk in Tokyo with Al for nearly ten years. His picture is there in all his youth, accepting the Japanese surrender in Korea with DLI graduates.

I Guess I Should Have Studied Harder

It was 3:30 am when one of my old staffers from Morgan Stanley in London called. He was now running a proprietary trading desk at Goldman Sachs, and I didn?t think he was rousing me out of a dead sleep to reminisce about the good old days. He told me that the firm?s research department was issuing a call to sell the S&P 500 up here at 1,360 immediately and they were calling all their top clients at home, well ahead of the New York opening. He thought I?d like to know.

Damn right I?d like to know! I said thanks and offered him a free ticket to attend my upcoming July 16 London strategy luncheon. I said I?d catch up with him later at the Seashell Restaurant on Lisson Grove, the best fish and chips joint in London. I then staggered downstairs, fired up my computer, and started writing Trade Alerts for my readers faster than a one-armed paper hanger. It was clear that I had to unload the entire equity exposure of the model portfolio pronto, which before the early call stood at a hefty 75%.

The market has been cruising for a bruising all week. During my biweekly Wednesday strategy webinar, I practically begged readers to take this opportunity to sell stocks (SPX), the Russell 2000 (IWM), the Euro (FXE), the Ausie, and oil (USO). Moody?s was believed to downgrade the US banks imminently, some by several notches. The brief respite of bad news from Europe was creating a great dumping opportunity. When the Federal Reserve decision hit, which was hugely negative for the entire ?RISK ON? trade, traders were strangely frozen like a deer in the headlights, leaving the markets nearly unchanged on the day.

I couldn?t believe my good luck when the market actually opened up on Thursday a touch stronger off the back of the modest 2,000 decline in weekly jobless claims. Out went my urgent alerts to sell Apple (AAPL), JP Morgan (JPM), and Walt Disney (DIS). I hated to let these great companies go, but when a stampede hits, even the best stocks get trampled, so it is best to watch from the sidelines. I can always buy them back cheaper.

Over the last seven weeks, I have issued no less than 44 urgent trade alerts. This is on top of writing 35 daily letters, holding global webinars, and conducting countless TV and radio interviews. In addition, I did live speaking engagements in Baltimore, Washington DC, Scottsdale, Los Angeles, Palm Springs, and San Francisco. It all worked, with the year to date performance now standing at 8.5%. But I have to tell you that I am getting a little bit tired.

It?s not only me, but the entire Mad Hedge Fund Trader network is worn out, including the editors, web administrators, marketers, bloggers, research assistants, accountants, and even the person who runs down to Starbucks to get my grande carmel machiatos. So I will be reducing the volume of trade alerts for the next month or so.

There is another reason for downshifting the intensity. Since the April model portfolio performance low, we are up an eye popping 57%. My experience over a 40 year trading career is that whenever I enjoy a huge performance run like this, the next trade turns out to be a really bad one. One gets overconfident, overaggressive, and mistakes are made.

I have two remaining options positions that expire in three weeks, a deep out of the money call spread on the Treasury bond market (TLT) and the same on the Japanese yen (FXY). These have both been unfolding strangely identical charts for the last few weeks. These ?RISK OFF? ASSETS usually fly on a day like this. Instead, they have been dead in the water, further boosting my P&L. To me this means that the stock market is going down, but isn?t crashing, that the top in the Treasury market may be closer than we think, and that trading conditions are going to absolutely suck for the foreseeable future. These are further reasons to get out of Dodge.

Those who followed my advice to sell in May and go away did extremely well, earning a stunning 20.5% following my trade alert service. So far in June, we are up another 14%. Well now you have a second chance to sell at the May prices, almost. But only if you act fast enough.

Did Somebody Say Sell?

Paid up subscribers to Global Trading Dispatch and the Diary of a Mad Hedge Fund Trader newsletter are entitled to a password that gives them access to my premium content. Without it you will be unable to access the best parts of the new website, including my daily real time trading portfolio, trade alert tutorial and user?s manual, my Review of 2011, 2012 Outlook, and live biweekly strategy webinars. Only if you are paid up, but have never logged in to the site, please email us at support@madhedgefundtrader.com . A new password will be issued promptly.

For those who are yet to have their investment returns enhanced beyond their wildest imagination by Global Trading Dispatch, please sign up for the newsletter only for $500 a quarter. If you like what you see, then you can upgrade later to the full service for $3,000 a year and we will give you a credit for what you already spent.

Global Trading Dispatch, my highly innovative and successful trade mentoring program, earned a net return for readers of 40.17% in 2011, and has an annualized 30.3% return since inception. The 2012 year to date performance as of last night was 8.7%. The service includes my Trade Alert Service, daily newsletter, real time trading portfolio, an enormous trading idea data base, and live biweekly strategy webinars. The goal is to level the playing field for you and Wall Street. To subscribe, please go to my website at www.madhedgefundtrader.com , find the Global Trading Dispatch box on the right, and click on the lime green ?SUBSCRIBE NOW? button.

Global Trading Dispatch?s Trade Alert Service posted a new all-time high yesterday, clocking a 48% return since inception. That takes the average annualized return up to 30.3%, ranking it among the top five performing hedge funds in the world. Those happy subscribers who bought my service in early May reaped an instant 35% profit following my advice.

I really nailed the top of the market on April 2, piling on hefty short positions in the S&P 500 (SPY) and the Russell 2000 (IWM) within a week. Predicting that the conflagration in Europe would get worse, my heavy short in the Euro (FXE), (EUO) was a total home run. I took in opportunistic profits trading the Japanese yen (FXY), (YCS) and the Treasury bond market (TLT) from the short side. I was then able to lock in these profits by covering all of my shorts with 60 seconds of the May 28 market bottom.

In June I caught almost the entire move up with a portfolio packed with ?RISK ON? trades. I picked up Apple (AAPL) at $530 for a rapid $50 gain. I seized the once in a lifetime opportunity to buy JP Morgan (JPM) at a 40% discount to book value, picking up shares at $31, correctly analyzing that the ?London Whale? problem was confined and solvable. My long position in Walt Disney (DIS) performed like the park?s ?Trip to the Moon? ride. While Hewlett Packard (HPQ) fell a disappointing 5% on me, I was able to add 140 basis points to my performance through time decay on an options position.

My satisfaction in all of this comes from the knowledge that thousands of followers are making money in the markets that never would otherwise. I am protecting them from getting ripped off by the sharks on Wall Street with their conflicted and indifferent research. I am expanding their understanding of not just financial markets, but the world at large. And I am doing this during some of the most difficult trading conditions in history.

Global Trading Dispatch, my highly innovative and successful trade mentoring program, earned a net return for readers of 40.17% in 2011. The service includes my Trade Alert Service, daily newsletter, real time trading portfolio, an enormous trading idea database, and live biweekly strategy webinars. To subscribe, please go to my website at www.madhedgefundtrader.com , find the ?Global Trading Dispatch? box on the right, and click on the lime green ?SUBSCRIBE NOW? button.

Diary Entry for Monday, June 18, 2012

Dear Diary,

4:30 PM Sunday- Looks like my Monday is going to start early this week.

One of my Athens readers e-mailed me that New Democracy was a slam dunk to win the election and would form a right of center, pro bailout, pro Euro (FXE) coalition government. Looks like it is going to mean a ?RISK ON? week. US Treasuries nosedive in the overnight market. Looks like we are going to get a shot at selling short the Euro (EUO) one more time.

6:30 PM Sunday-Take kids to see the new DreamWorks animated blockbuster, ?Madagascar 3?, with voiceovers by Ben Stiller, Chris Rock, Jada Pinkett Smith and David Schwimmer. Notice how the kid movies are better than the adult movies these days. There are ample double entendres and innuendos to keep the grownups laughing all the way. I loved the penguins, fowl after my own heart.

9:00 PM-Call from a friend at the People?s Bank of China in Beijing. He wants to know if they have missed the top of the Treasury bond market, and if they should start unloading their $1 trillion worth of holdings. I said don?t worry. I expect the ?RISK OFF? trade to take the ten year yield up to 1.25% on a spike at some point, and then levitate, possibly for years. The world is suffering from a savings glut and a bond shortage. Plus, you will get a double kicker with a strong dollar. But please don?t try and sell ahead of a three day weekend, like you did last time. And thanks for the Peking Duck dinner in Shenzhen last year.

9:30 PM- Hit the rack and try and catch some shuteye before the next call.

2:00 AM-One of my former staff members at Morgan Stanley calls me from a Private Bank in Geneva to tell me that the Spanish bond market was in free fall, with yields piecing 7%. Is it time to buy? I said not yet, not until the fat lady sings, and slammed the phone back on the hook to go to sleep.

Spanish 10 Year Bond Yields

3:00 AM- Call from one of the top New York trading houses. There are rumors that the Oracle (ORCL) would announce blowout earnings in a few hours. Did I want to buy anymore stock? I said no thanks, that I already had 50% of my portfolio in high tech names like Apple (AAPL) and Hewlett Packard (HPQ). Can he please come up with any new top performing industries? People are getting tired of hearing the Apple story for the umpteenth time.

5:00 AM-Woken up by an earthquake that sounds like a truck just hit the house. I turn on the TV and learn that I am directly above the epicenter. It?s the third one since Wednesday. Ah, the joys of living in California next door to the San Andreas Fault.

6:00 AM-My website administrator calls me in a panic. The store is down. A hacker attack prompted PayPal to suspend my account. Since I am one of their largest customers, I call my account rep and get it reopened.

6:15 AM-An old friend from the Swiss National Bank called asking my read on the Fed meeting this week. I said that things weren?t dire enough for a QE3, but he could count on a ?twist? extension to include home mortgage securities. The board was most frustrated my its inability to revive the real estate market with the lowest interest rates in history, and such a move could take 30 years fixed rates loans from 3.75% to 2.75% in weeks. I said I owed him a fondue diner with a bottle of Schnapps for giving me the heads up on the Swiss franc devaluation last year where my followers earned a 400% profit on the puts (FXF). But to collect, he had to take the cog railway up to Zermatt and attend my strategy seminar on July 27.

6:45 AM-I get flooded with 30 emails from Trade Alert Service followers asking if they should take profits on their long Apple calls spreads. I ignore them. Don?t bother me with the small change. I can?t hold everyone?s hand.

7:00 AM- Another call from my website administrator. The website is down. The Greek election brought a traffic spike that is causing the servers to melt. I am burning up the Internet.

7:30 AM- Conference call with support team. We agree to build in new infrastructure to accommodate a tenfold increase in new business. Couldn?t I be wrong a little more often to bring the growth down to a more manageable level? Pass.

8:00 AM- I get a call from a leading hedge fund in London?s Mayfair district. Europe is closing. Should we run the Euro short overnight? You betcha! And go have a pint of bitter for me at the Pig & Whistle next door, will you.

9:00 AM-Call from a large family office in Chicago. Should we use today?s weakness in gold to unwind out more hedges against core longs? Absolutely. Grab the brass ring. The barbaric relic is going to $2,300 before the fat lady sings, and will go higher if the ECB launches another LTRO, which is just a matter of time.

10:00 AM-Better get to work on today?s letter. I?m already behind the eight ball. I?ve gotta lead the gold story, which is starting to emerge from its long hibernation and exhibit some virile stirrings. Platinum (PPLT) looks even better.

12:00 PM-Break for lunch. Isn?t it great the way enchiladas always taste better after they have been reheated for a third day?

1:00PM- Market close with a small loss. Looks like another day of ?RISK OFF? for Tuesday.

1:15 PM-My friend, JR, a senior exec at an oil major, calls from Houston. What the hell was going on with the price of oil (USO)? Three months ago, it was at $109, then he blinked, and it was $80. I told him that the oil companies lost control of the price of Texas tea last year and the high frequency traders were now in the saddle. Better get used to the new frontier. He said thanks, and next time I was in town he would buy me a 24-ounce chicken fried steak at Billy Bob?s that spilled over both sides of the plate. I can?t wait. I?ll let my doctor have the heart attack.

1:20 PM- It?s official. Oracle earns $3.45 billion, or 69 cents a share, for the three months ended in May, compared with $3.2 billion, or 62 cents, a year earlier. The stock pops 5% in the aftermarket. Damn! I bought Hewlett Packard instead.

2:00 PM-Still haven?t started on the letter yet. I have been answering 200 email requests for information about the Trade Alert Service. This always happens whenever I have a hot trade on. The watchers want to become players. A 20.5% May and an 11% June month to date brings them in the droves.

2:30 PM- I unplug the phones and close the curtains to do a one our live show on the recent market volatility as a guest on a local radio station.

4:45 PM- Well, I got the letter done, but I?m too late. The web editor has gone to the DMV to register her new Prius, and the backup has gone to the yoga studio. Ouch! 10% sales tax for new cars in Washington state! They must be as broke as California.

4:30 PM-The traffic stats for the site have gone down. I called the webmaster, but she has gone off to a line dancing lesson in Dallas.

5:00 PM-Ooops. Forgot to take the trash out.? My garbage man, an Afghan immigrant, must wonder what goes on here. Every week, I recycle a giant bin of newspapers, magazines, and assorted broker research, but only throw out a tiny bag of actual trash. Am I green, or what? He notices that my T-shirt reads in Pashto script ?Defense Language Institute. We learn, so you don?t have to.? He says his son was stationed at Fort Hood in Texas and that he hasn?t heard from him in two months. I make a quick call Washington and find out that he has been transferred to Afghanistan as a translator. I tell him not to worry. It?s the other guys who usually die, not ours.

5:30 PM-I put on a 60-pound pack and my heavy climbing boots and head out the back door on a three hour hike to climb Grizzly Peak as I do every evening. Gotta stay boot camp ready. You never know when Uncle San is going to call again. Who cares if I?m 60? During Desert Storm, my flight commander was drafted at 65, and I heard of another guy they took who was 85. Turns out there was no one left in the Navy who knew how to run a coal fired steamship.

9:00 PM-Back to my screens. The Euro has broken $1.27. The Greek stock market is up 25% in days. Where was I last week? Asleep? If you turned off your TV, the centrist win was a no brainer.

10:00 PM-Time to call it a night and break out a bottle of Duckhorn merlot. How many wine clubs do I belong to now? 12? As of now I am committed to buy more wine this year than I can possibly drink or give away. That?s the price of living next door to Napa Valley. I?m shipping a case to my suite on the Queen Mary II so I can give away to fellow diners en route from New York to Southampton in a few weeks. The captain always likes a bottle too.

12:00 AM- Time to do some early Christmas shopping. Bonham?s in London is holding their fine jewelry auction today, and lot no. 62 is a 5 carat diamond solitaire that is a real beat.

12:10 AM-Damn! Outbid by the Chinese again, who are running up the price of luxury goods absolutely everywhere to insane levels. Time to get some sleep. Maybe next time. I?m obviously not working hard enough. I unplug my phones, as it?s the only way I can sleep. It looks like tomorrow is going to be another busy day. Does anybody want my job?

Note to Greece: Please Quit Waking Me Up!

It seems that all you hear about these days is deflation. That is certainly what the bond market is telling us, with my screen blaring at me a miserable 1.58% yield for the ten year Treasury bond.

But there is a new definition for this economic malady that applies to we hapless consumers. In the new deflation, the value of our income falls, while the prices of things we need to buy are going through the roof. It is a particularly pernicious form of deflation, as it is burning our candles at both ends at the same time.

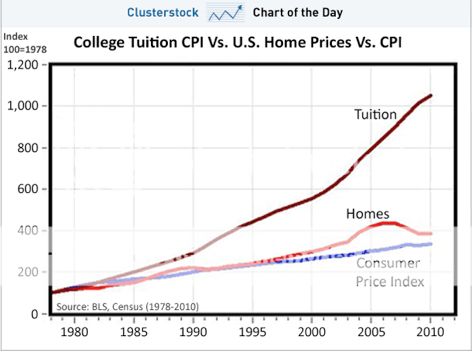

Take a look at the chart below, showing the cost of college tuition versus the consumer price index and home prices. This hits home particularly hard, as I have just put three kids through college, and am reduced to riffling through the sofa cushions looking for spare change or washing windshields at street corners on weekends in order to meet the bills. When I graduated from the University of California in the seventies the tuition was $3,000 a year. Today it is $16,000, and climbing at a 20% annual rate.

The saddest part of the story is that rampant wage deflation means that recent graduates have a grim choice between taking a poorly paid job, or no job at all. That leaves them woefully unable to repay the student loans they ran up to obtain their rapidly devaluing diplomas. The $1 trillion in outstanding student loans is begging to become the next subprime crisis.

And if you were planning on becoming a teacher, forget it, unless you want to move to Saudi Arabia, Russia, or South Korea. After watching tens of millions of jobs get shipped to China over the last decade, did you expect anything less? Just add this problem to the ever lengthening list of ways we are getting screwed.

Deflation Can Be a Bitch!