Ingenious writing, John, in your Monday morning strategy letter. I forwarded it to all my family and kids, and made my 16-year-old read it out loud to my wife. I made sure he understood what he was reading. I got choked up by the whole article.

Go Ukraine!

Best regards,

Greg

Las Vegas, NV

https://www.madhedgefundtrader.com/wp-content/uploads/2018/06/Young-John-Thomas-with-gun-story-2-image-5-e1528406442448.jpg357250Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2026-04-07 09:04:082026-04-07 14:34:42Testimonial

I like to start out my day by calling readers on the US East Coast and Europe, asking how they like the service, are there any ways I can improve the service, and what topics would they like me to write about.

After all, at 5:00 AM Pacific time, they are the only ones around.

You’d be amazed at how many great ideas I pick up this way, especially when I speak to industry specialists or other hedge fund managers.

Even the 25-year-old day trader operating out of his mother’s garage has been known to educate me about something.

So when I talked with a gentleman from Tennessee in the morning, I heard a common complaint.

Naturally, I was reminded of my former girlfriend, Cybil, who owns a mansion on top of the levee in nearby Memphis overlooking the great Mississippi River.

As much as he loved the service, he didn’t have the time or the inclination to execute my market-beating Trade Alerts.

I said, “Don’t worry. There is an easier way to do this.”

Only about a quarter of my followers actually execute my Trade Alerts, and a lot of them are professionals. The rest rely on my research to correctly guide them in the management of the IRA’s 401(k)’s, pension funds, or other retirement assets.

There is also another, easier way to use the Trade Alert service. Think of it as “Trade Alert light.” Do the following.

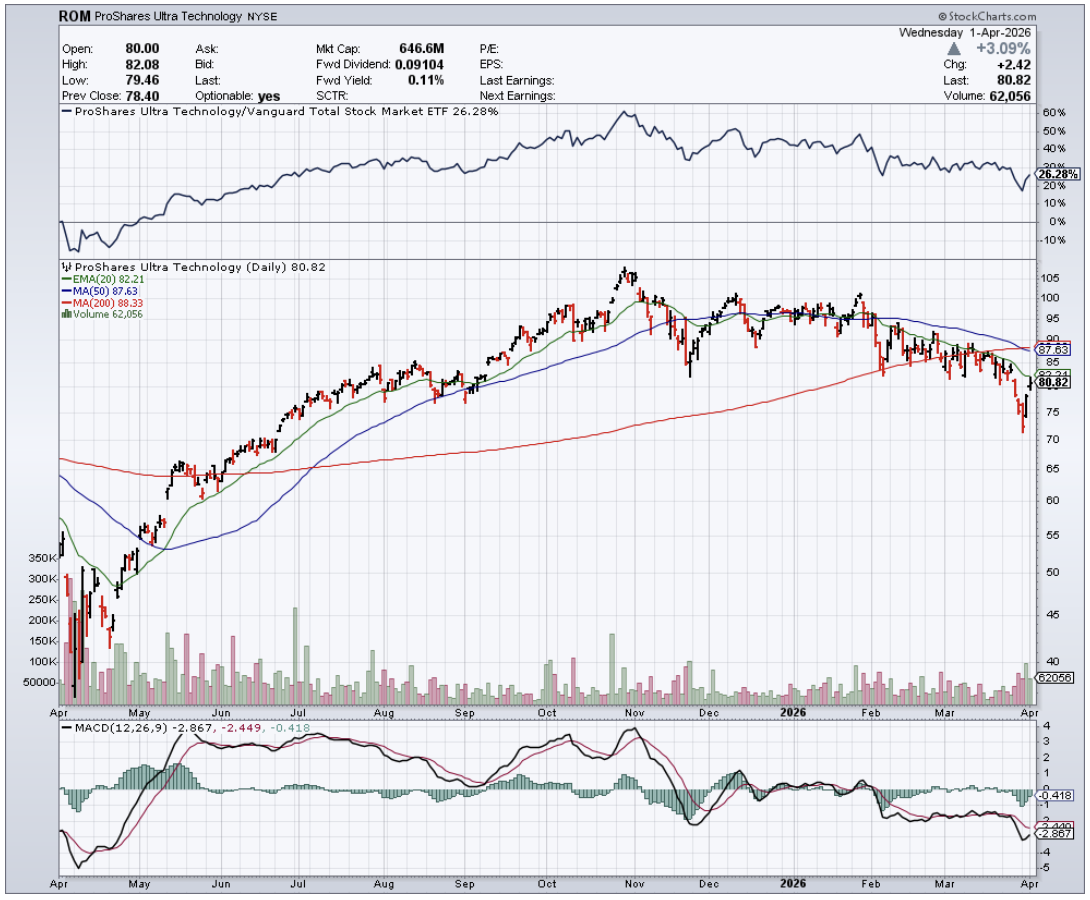

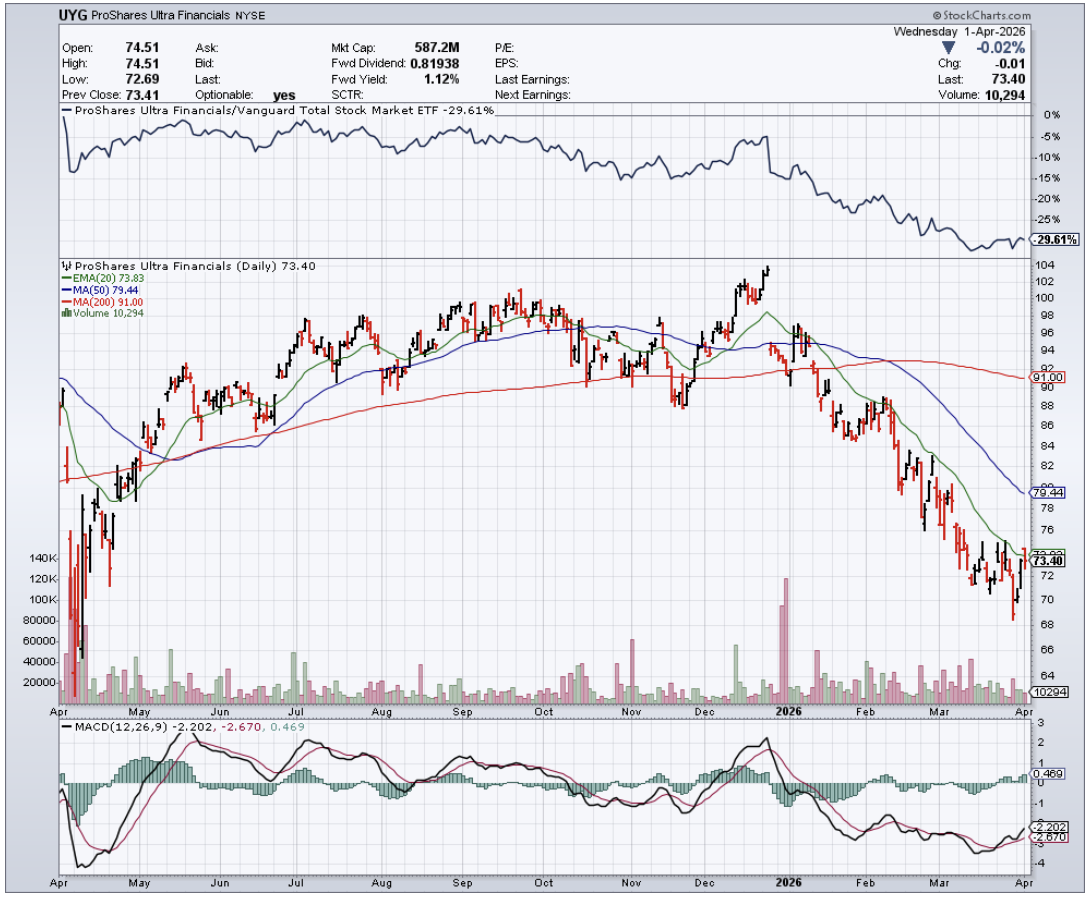

1) Only focus on the four best of the S&P 500’s 101 sectors. I have listed the ticker symbols below.

2) Wait for the chart technicals to line up. Bullish long-term“Golden crosses” will set up for several sectors, as with precious metals now.

3) Use a macroeconomic tailwind.

4) Shoot for a microeconomic sweet spot, companies and sectors that enjoy special attention.

5) Increase risk when the calendar is in your favor, such as from November to May.

6) Use a modest amount of leverage in the lowest risk bets, but not much. 2:1 will do.

7) Scale in, buying a few shares every day on down days. Don’t hold out for an absolute bottom. You will never get it.

The goal of this exercise is to focus your exposure on a small part of the market with the greatest probability of earning a profit at the best time of the year. This is what grown-up hedge funds do all day long.

Sounds like a plan. Now, what do we buy?

(ROM) – ProShares Ultra Technology 2X Fund – Gives you a double exposure to what will be the top-performing sector of the market for the next six months, and probably the rest of your life. Click here for details and the largest holdings.

(UXI) – ProShares Ultra Industrial Fund 2X– Is finally rebounding off the back of a dollar that will slow down its ascent once the first interest rate hike is behind us. Onshoring and incredibly cheap valuations are other big tailwinds here. For details and the largest holdings, click here.

(BIB) – ProShares Ultra NASDAQ Biotechnology 2X Fund – With technology, this will be the other hyper-growth sector in the stock market for the next 20 years. How much is a cancer cure worth to stock valuations? Oh, about $2 trillion. A basket approach favors this notoriously volatile sector by rotating in new winners to replace losers.

(UYG) – ProShares Ultra Financials 2X Fund – Yes, after six years of false starts, interest rates are finally going up, with a December rate hike by the Fed a certainty. My friend, Janet, is handing out her Christmas presents early this year. This instantly feeds into wider profit margins for financials of every stripe. For details and the largest holdings, click here.

Of course, you’ll need to keep reading my letter to confirm that the financial markets are proceeding according to the script. We all know that sectors can rotate rapidly, as they have just done.

You will also have to read the Trade Alerts, as we include a ton of deep research in the Updates.

You can then unload your quasi-trading book with hefty profits in the spring, just when markets are peaking out. “Sell in May and Go Away?” I bet it works better than ever in 2024.

For Those Who Invest at Their Leisure

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas.png387483MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2026-04-02 09:02:462026-04-02 10:44:05The Lazy Man’s Guide to Trading

The Diary of a Mad Hedge Fund Trader is now celebrating its 18th year of publication.

During this time, I have religiously pumped out 3,000 words a day, or 18 newsletters a week, of original, independent-minded, hard-hitting, and often wickedly funny research.

I spent my life as a war correspondent, Marine Corps combat pilot, Wall Street trader, and hedge fund manager, and if you can’t laugh after that, something is wrong with you.

I’ve been covering stocks, bonds, commodities, foreign exchange, energy, precious metals, real estate, and even agricultural products.

You’ve been kept up on my travels around the world and listened in on my conversations with those who drive the financial markets.

I also occasionally opine on politics, but only when it has a direct market impact, such as with the recent administration's economic and trade policies. There is no profit in taking a side.

The site now contains over 20 million words, or 30 times the length of Tolstoy’s epic War and Peace.

Unfortunately, it feels like I have written on every possible topic at least 100 times over.

So, I am reaching out to your, the reader, to suggest new areas of research that I may have missed until now which you believe justify further investigation.

Please send any and all ideas directly to me at support@madhedgefundtrader.com/, and put “RESEARCH IDEA” in the subject line.

The great thing about running an online business is that I can evolve it to meet your needs on a daily basis.

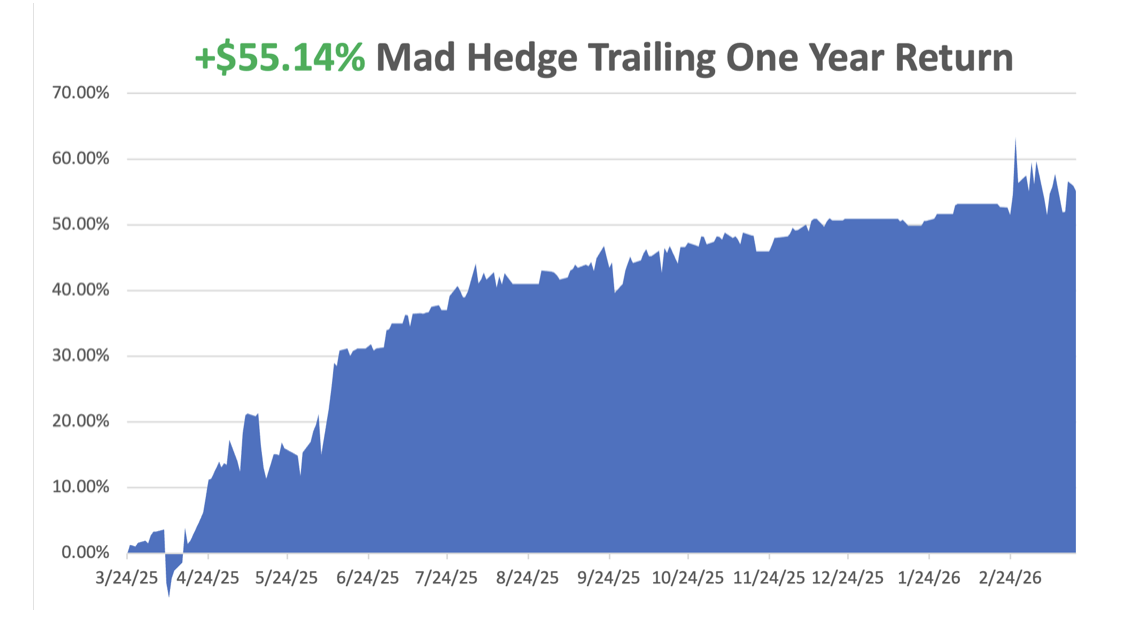

Many of the new products and services that I have introduced since 2008 have come at your suggestion. That has enabled me to improve the product’s quality, to your benefit. Notice how rapidly my trade alert performance is going up, now annualizing at +47%a year.

This originally started out as a daily email to my hedge fund investors, giving them an update on fast-moving market events. That was at a time when the financial markets were in free fall, and the end of the world seemed near.

Here’s a good trading rule of thumb: Usually, the world doesn’t end. History doesn’t repeat itself, but it certainly rhymes.

The daily emails gave me the scalability that I so desperately needed. Today’s global mega enterprise grew from there.

Today, the Diary of a Mad Hedge Fund Trader and its Global Trading Dispatch are read in over 140 countries by 30,000 followers. The Mad Hedge Technology Letter, the Mad Hedge Biotech & Health Care Letter, Mad Hedge AI, and Jacquie’s Post also have their own substantial followings. And the daily Mad Hedge Hot Tips is one of the most widely read publications in the financial industry.

I’m weak in distribution in North Korea and Mali, in both cases due to the lack of electricity. But that may change.

One can only hope.

If you want to read my first pitiful attempt at a post, please click here for my February 1, 2008, post.

It urged readers to buy gold at $950 (it soared to $2,200), and buy the Euro at $1.50 (it went to $1.60).

Now you know why this letter has become so outrageously popular.

Unfortunately, I also recommended that they sell bonds short. I wasn’t wrong on that one, just early, about eight years too early.

I always get asked how long I will keep doing this.

I am already collecting Social Security, so that deadline came and went. My old friend and early Mad Hedge subscriber, Warren Buffett, is still working at 92, so that seems like a realistic goal. And my old friend, Henry Kissinger, is still hard at it at 100 years old.

Hiking ten miles a day with a 50-pound pack, my doctor tells me I should live forever. He says he spends all day trying to convince his other patients to be like me, and the only one who actually does it is me.

The harsh truth is that I don’t know how to NOT work. Never tried it, never will.

The fact is that thousands of subscribers love me for what I do, pay for me to travel around the world first class to the most exotic destinations, eat in the best restaurants, fly the rarest historical aircraft, and then say thank you. I even get presents (keep those pounds of fudge and bottles of bourbon coming!).

Given the absolute blast I have doing this job, I would be Mad to actually retire.

Take a look at the testimonials I get on an almost daily basis, and you’ll see why this business is so hard to walk away from (click here to view them.)

In the end, you are going to have to pry my cold, dead fingers off of this keyboard to get me to give up.

Fiat Lux (let there be light).

https://www.madhedgefundtrader.com/wp-content/uploads/2020/07/John-Thomas-bull2.png514454april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-03-24 09:02:232026-03-24 16:03:51Founding the Mad Hedge Diary of a Mad Hedge Fund Trader

Actually, I just got started with investing as I’ve been living close to the edge raising kids all these years. I had $100K that I could float for a few months so I had it in the Eaton Vance Tax-Managed Diversified Equity Income Fund (ETY) until my old golf buddy/broker told me about you and your Tesla (TSLA) advice.

So, I went all-in on December 30. It’s the best move I ever made. I’m an entrepreneur/risk-taker so I bought as much Apple (AAPL) and NVIDIA (NVDA) on the way down as I could, which obviously turned out far better than I ever hoped.

So, like I said, it seems now or never for me. So, I subscribed to your Mad Hedge Biotech & Healthcare Letter and I’m going to do the best I can with it.

Thanks a “million.”

Greg

Las Vegas, NV

https://www.madhedgefundtrader.com/wp-content/uploads/2020/06/john-thomas-tesla.png204360Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2026-03-11 09:02:432026-03-11 14:03:21Testimonial

“War is God’s way of teaching the American people Geography,” said Lydia Polgreen of the New York Times.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-03-09 09:00:152026-03-09 13:35:01March 9, 2026 - Quote Of The Day

You can count on a bear market hitting sometime in 2038, one falling by at least 25%.

Worse, there is almost a guarantee that a financial crisis, severe bear market, and possibly another Great Depression will take place no later than 2058, which would take the major indexes down by 50% or more.

No, I have not taken to using a Ouija board, reading tea leaves, or examining animal entrails in order to predict the future. It’s much easier than that.

I simply read the data just released from the National Center for Health Statistics, a subsidiary of the federal Centers for Disease Control and Prevention (click here for their link).

The government agency reported that the US birth rate fell to a new all-time low for the second year in a row, to 60.2 births per 1,000 women of childbearing age. A birth rate of 125 per 1,000 is necessary for a population to break even. The absolute number of births is the lowest since 1987. In 2017, women had 500,000 fewer babies than in 2007.

These are the lowest numbers since WWII, when 17 million men were away in the military, a crucial part of the equation.

Babies grow up, at least most of them. In 20 years, they become consumers, earning wages, buying things, paying taxes, and generally contributing to economic growth.

In 45 years, they do so quite substantially, becoming the major drivers of the economy. When these numbers fall, recessions and bear markets occur with absolute certainty.

You have long heard me talk about the coming “Golden Age” of the 2020’s. That’s when a two-decade-long demographic tailwind ensues because the number of “peak spenders’ in the economy starts to balloon to generational highs. The last time this happened during the 1980’s and 19990’s stocks rose 20-fold.

Right now, we are just coming out of two decades of demographic headwind, when the number of big spenders in the economy reached a low ebb. This was the cause of the Great Recession, the stock market crash, and the anemic 2% annual growth since then.

The reasons for the maternity ward slowdown are many. The Great Recession certainly blew a hole in the family plans of many Millennials. Falling incomes always lead to lower birth rates, with many Millennial couples delaying children by five years or more. Millennial mothers are now having children later than at any time in history.

Burgeoning student debt, which just topped $1.5 trillion, is another. Many prospective mothers would rather get out from under substantial debt before they add to the population.

The rising education of women is another drag on childbearing and is a global trend. When spouses become serious wage earners, families inevitably shrink. Husbands would rather take the money and improve their lifestyles than have more kids to feed.

Women are also delaying having children to postpone the “pay gaps” that always kick in after they take maternity leave. Many are pegging income targets before they entertain starting families.

As a result of these trends, one in five children last year was born to women over the age of 35, a new high.

This is how Latin Americans moved from eight to two-child families in only one generation. The same is about to take place in Africa, where standards of living are rising rapidly, thanks to the eradication of several serious diseases.

The sharpest falls in the US have been with minorities. Since 2017, the birth rates for Hispanics have dropped by 27% from a very high level, African Americans 11%, whites 5%, and Asian 4%.

Europe has long had the same problem with plunging growth rates, but only much worse. Historically, the US has made up for the shortfall with immigration, but that is now falling thanks to the current administration's policies. Restricting immigration now is a guarantee of slowing economic growth in the future. It’s just a numbers game.

So watch that growth rate. When it starts to tick up again, it’s time to buy….in about 20 years. I’ll be there to remind you with this newsletter.

As for me, I’ve been doing my part. I have five kids aged 15-34, and my life is only half over. Where did you say they keep the Pampers?

I’m Doing My Part

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/John-and-family-story-1-image-e1526596823183.jpg266400april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2026-02-19 09:02:542026-02-19 16:24:48They’re Not Making Americans Anymore

Come join me for lunch for the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting in Orlando, Florida at 12:00 PM on Thursday, January 8, 2026. A three-course lunch is included.

I’ll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate.

And to keep you in suspense, I’ll be throwing a few surprises out there, too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $267.

I’ll be arriving early and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive hotel near Disneyland, the details of which will be emailed to you with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets for this luncheon, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2025/11/mickey-disney.jpg576918april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-11-21 09:04:022025-11-21 11:33:39January 8, 2026 Orlando, Florida Global Strategy Luncheon

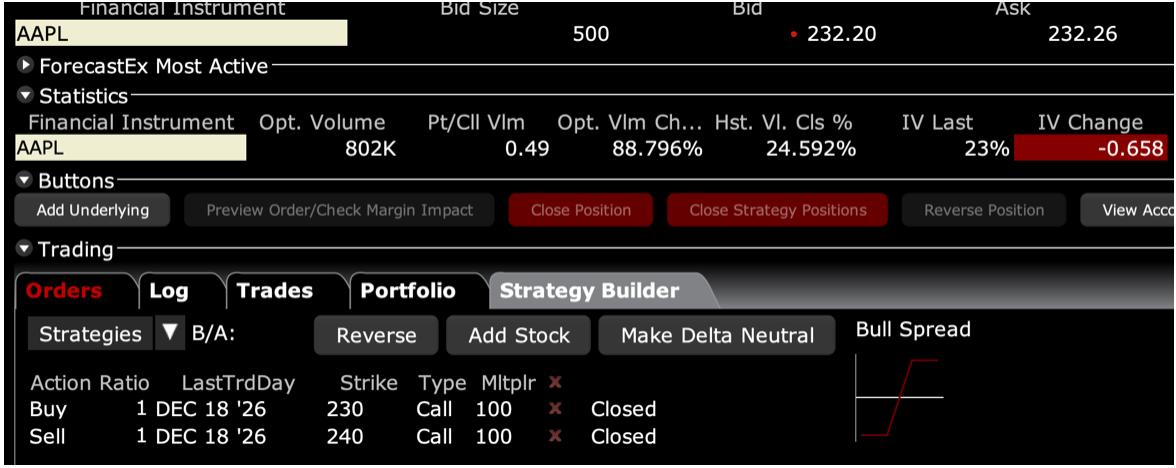

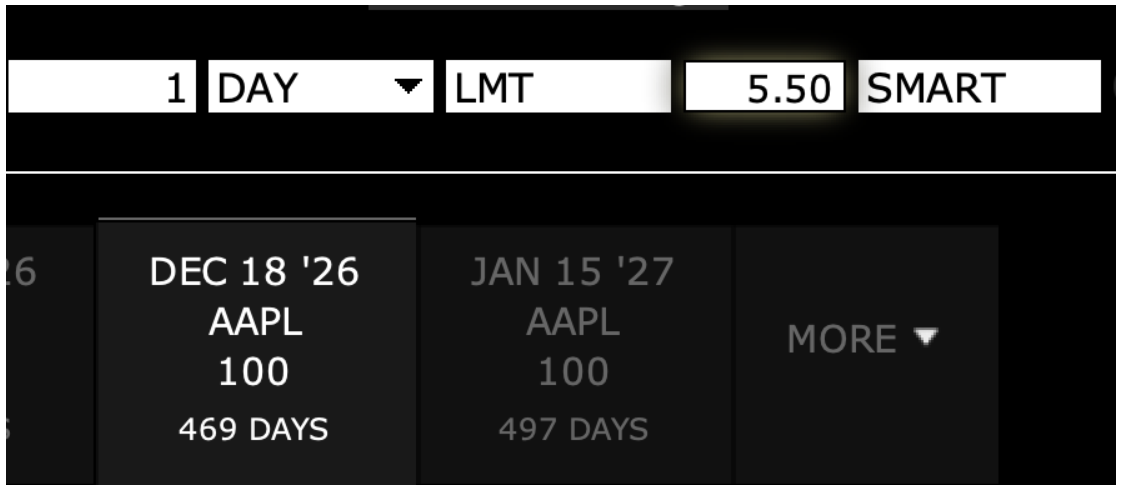

Trade Alert - (AAPL) – BUY BUY the Apple (AAPL) December 2026 $230-$240 at-the-money vertical Bull Call spread LEAPS at $5.50 or best

Opening Trade

9-5-2025

expiration date: December 18, 2026

Number of Contracts = 1 contract

With Apple about to announce its next-generation iPhone 17 on Sunday, which is AI-enabled, this is a good time to dive into a long-term Apple LEAPS.

You hear a lot of incredible stories in Silicon Valley.

An electronic compact disc is coming that can deliver perfect sound and movies. Have you heard of the Internet? Compaq is offering a computer that will sit on your laptop! Do you have any idea how Google is going to make money? Steve Jobs is building a smartphone! Is he out of his mind? Elon Musk is building an electric car with a 250-mile range. Hey, I heard about this thing called “artificial intelligence.”

So I listened very carefully the other day when a friend of mine told me he had scored the real estate deal of the century.

His house had sat on the market like dead wood for a year and a half, priced at $4.0 million. It was a very nice 5,000 square foot Italian villa-type home with a huge garden and a fantastic 360-degree view.

Then out of the blue, a cash buyer said he wanted to rent the house for a year for the spectacular over-the-market rent of $20,000 a month, plus all utilities. Then, he offered to pay 10% over the asking price, or $4.4 million to buy the house outright, and would pay $400,000 in cash for the option to do so, payable immediately.

My friend, puzzled but ecstatic, asked why he was going about buying a home in this way. The buyer answered that he had some stock options from his company that he didn’t want to cash in for a year. His profession? He had a PhD in artificial intelligence.

That set the alarm bells off in my head.

I pulled out a paper map of the San Francisco Bay Area and drew a circle around the house within one hour driving time to reduce the number of potential candidates. Then I called a seasoned technical analyst and asked him which big California stock had a chart that was just about to break out to the upside. He didn’t hesitate.

Apple!

It all makes so much sense. Apple is one company behind in artificial intelligence that has the most money to do something about it. All they have to do is buy a ready-made AI company like Perplexity, and it will be out front.The shares will race to $260. I then calculated how high Apple shares would have to rise to justify the enormous premium for my friend’s house. I hit bang on $260.

I am therefore buying the Apple (AAPL) December 2026 $230-$240 at-the-money vertical Bull Call spread LEAPS at $5.50 or best

DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES.

These LEAPS are illiquid, so you are going to have to play around with prices to get a position. Start at $5.00, then increase to $5.50, $5.60, $5.70, and so on. Don’t pay more than $7.00, or these will get expensive. It is easier to do this on days when the stock market is down.

This is a bet that Apple (APPL) will not fall below $240 by the December 18, 2026, option expiration in 15 months. Apple shares have to rise only 70 cents in 15 months to hit the upper strike in this LEAPS.

To learn more about the company, please click here to visit their website.

Notice that the day-to-day volatility of LEAPS prices is minuscule, less than 10%, since the time value is so great and you have a long position simultaneously offset by a short one.

This means that the day-to-day moves in your P&L will be small. It also means you can buy your position over the course of a month, just entering new orders every day. I know this can be tedious, but getting screwed by overpaying for a position is even more tedious.

Look at the math below, and you will see that a 70-cent rise in (AAPL) shares will generate an 82% profit with this position, such is the wonder of LEAPS. That gives you an implied leverage of 117:1. LEAPS stand for Long Term Equity Anticipation Securities.

(AAPL) doesn’t even have to get to a new all-time high of $260 to make the max profit in this position, which it will probably do in weeks, if not months. It only has to get back to $240, where it traded in March before the meltdown.

Only use a limit order. DO NOT USE MARKET ORDERS UNDER ANY CIRCUMSTANCES. Just enter a limit order and work it.

Here are the specific trades you need to execute this position:

Buy 1 December 2026 (AAPL) $230 calls at………….………$38.00

Sell short 1 December 2026 (AAPL) $240 calls at…………$32.50

Net Cost:………………………….………..………….…...................$5.50 Potential Profit: $10.00 - $5.50 = $4.50

(1 X 100 X $4.50) = $450 or 82% in 15 months.

To see how to enter this trade in your online platform, please look at the order ticket below, which I pulled off of Interactive Brokers.

If you are uncertain on how to execute an options spread, please watch my training video on “How to Execute a Vertical Bull Call Debit Spread”by clicking here.

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep in-the-money spread trades can be enormous.

Don’t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Keep in mind that these are ballpark prices at best. After the alerts go out, prices can be all over the map.

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.