Is Quantitative Easing Over?

That is certainly the conclusion of the financial markets. When Federal Reserve chairman, Ben Bernanke, failed to mention the magic words in his House Humphrey Hawkins testimony on Wednesday, risk assets were sent into a tailspin. Gold suffered a $100 move plunge in hours, the futures market seeing an almost instantaneous liquidation of $1.3 billion worth of contracts. Silver dropped 10%. Oil gave up $3 in a heartbeat.

What was truly impressive was the collapse of the Treasury bond market, which saw yields for the ten year leap from 1.92% to 2.05%. When a single order to sell 100,000 bond futures contracts worth $10 billion hit the market, many thought that a major firm had committed a grievous ?fat finger? error. But the ?cancel and correct? never came, and the trade stood. Clearly, a major hedge fund was betting that the 30 year bull market in bonds had peaked and moved to add some serious downside exposure.

The reason that I missed the extent of the serious rally in risk assets this year is that the current wave of quantitative easing was so paltry. One ?500 billion tranche in December followed by a second on February 29 is only a fraction of the tsunami sized liquidity the Fed?s previous QE1 and QE2 unleashed on the markets.

In any case, most of this cash stayed in Europe, with the banks bidding up sovereign bonds in a frenzied manner to captures a massive positive carry. Italian ten year yields collapsed from over 8% to under 5% in weeks. As expected, none of the dosh made it into the real economy where it could do some actual good. But traders have developed a Pavlovian response to the words ?quantitative easing?, which instantly triggers a rush of buying of all assets everywhere, as it has done in past cycles.

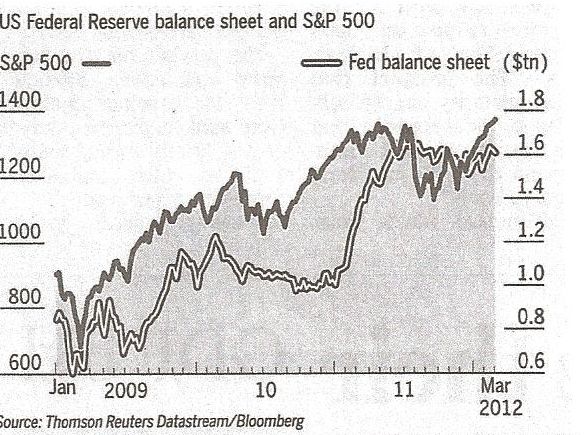

Never mind that the big liquidity surge wasn?t actually there. If you don?t believe me, take a look at the chart below showing the growth of the Fed balance sheet and its correlation with the S&P 500. When US central bank launched QE1 in early 2008, its assets soared from $600 billion to an amazing $1.7 trillion. Since mid-December when the ECB initiated its LTRO, it has climbed from $1.4 trillion to $1.8 trillion, a modest $400 billion, and represents only a recovery of its June 2010 high. That is only 36% of the earlier balance sheet expansion.

Since the onset of quantitative easing five years ago, this aggressive monetary policy tool has created anywhere from $3 trillion to $10 trillion in broader global liquidity. If you take away the punch bowl, the effect on risk assets could be dire. For a preview, take a look at what happened when we were in between QE waves from the end of the last Fed program in June to the European foreign language sequel in December. The S&P 500 collapsed by 25%, gold surrendered $400, and silver cratered nearly 50%, and $40 evaporated off of the price of oil.

I never believed that the Fed would follow up with a QE3, and I am sticking to my guns. None of the money from earlier easings made it into the sectors of the economy that they were attempting to target, like housing and construction. All it did was create bubbles in liquid and fungible global asset prices.

I think the Fed has figured this out by now. If a policy fails twice, then why repeat it a third time? If quantitative easing is truly well and done for good, how will the risk markets respond when they figure this out? The mother of all hangovers could be a safe bet.

Since we?re talking about Europe, good job on the Oscars, France! With Jean du Jardin in ?The Artist?, you won best picture and best actor. It is perhaps ironic that it was for a silent film. Is The Academy trying to tell you something, or what? Sorry, but I can?t resist a good cheap shot, especially when a foreigner takes away the prizes from California?s most illustrious industry. If my amphibious followers want to throw rotten tomatoes at me in person, please buy tickets to my July 17 Paris strategy lunch by clicking here.

Well Said, France!