Mad Hedge Technology Alerts!

Tesla’s (TSLA) recent underperformance is a canary in the coal mine of what could become of the global EV industry.

EV makers better watch out because the race to zero is coming for all of them.

It could be yet another tech industry captured by the Chinese. The Chinese are quickly rising up the food chain of technological capabilities and these new developments are sure to rattle the White House.

I remember years ago when the Chinese tried their best at smartphones, they were terrible, but fast forward to today, and now they compare close to the iPhone with much better pricing.

Now, the Chinese are coming after electric cars and I also remember touring EVs in China in 2007 and they again were pretty terrible.

However, fast forward to today, and yet again they have achieved major inroads in terms of quality and reach. BYD Company Limited (BYDDY) even produces something comparable to Tesla which is no small feat.

Tesla’s disappointing third-quarter deliveries highlight the panic state side where the first mover advantage has served CEO Elon Musk well but eroded lately.

Tesla sold 435,000 electric cars last quarter, while BYD sold 431,000 battery-powered electric cars over the same period.

Expect BYD to surge past Tesla in delivered electric cars soon because they have access to a vastly bigger market while the Chinese communist party is doing everything to ruin American corporate business in the Middle Kingdom.

BYD is already far ahead when it comes to total sales. Including hybrids, BYD sold over 800,000 cars last quarter, almost twice as much as Tesla.

The Chinese company sold 1.8 million cars last year, over 911,000 of which were BEVs. Tesla, which only sells BEVs, sold 1.3 million cars.

Musk had previously warned that planned upgrades to manufacturing plants around the world may lead to lower deliveries for the rest of the year.

Tesla is also facing sluggish demand, forcing it to launch aggressive price wars in both China and the U.S.

BYD has surged ahead of its competitors in China by selling more affordable electric vehicles, unlike the premium models sold by Tesla and other EV companies like Nio and XPeng. BYD recently unseated Volkswagen as China’s top-selling car brand.

The company is expanding outside of China and is now the top-selling EV brand in markets like Thailand, Israel, and Singapore. It’s even expanding into more developed markets like Japan and Europe.

Watch out for China’s BYD to hijack Western markets moving forward including Europe, Canada, the United States, and the UK.

It’s finally time to stop ignoring that China does a good job producing EVs and other hard-to-manufacture technology.

My guess is that China will also surpass the United States in semiconductor chip technology, although that will take longer to achieve.

The Pentagon has sounded the alarm bells after noticing huge improvements in chip know-how by the Chinese.

Competition is finally here for Musk after so many years of taking a free ride in the US and it’s about time. Now the rubber finally meets the road.

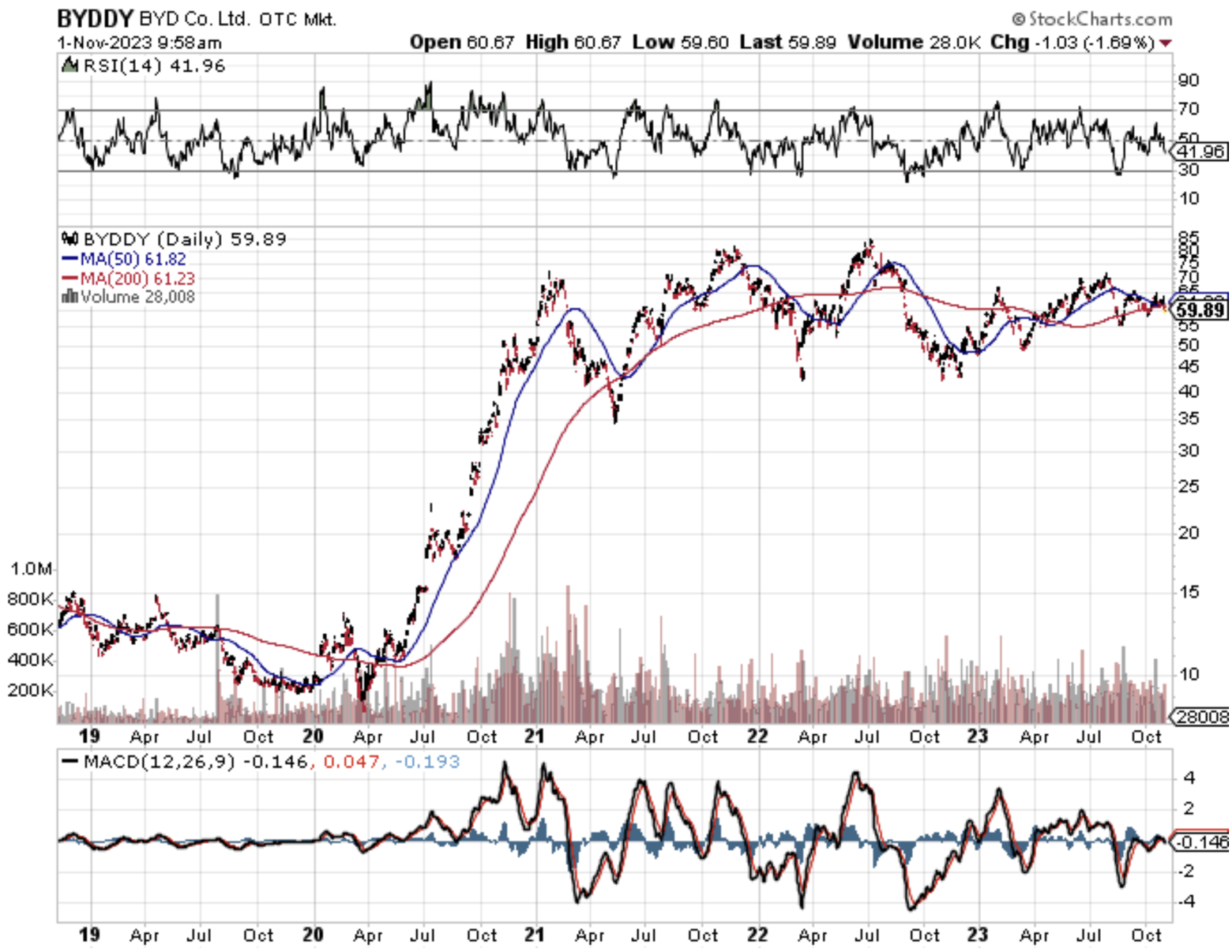

Readers with a high threshold of risk tolerance should look at BYD’s ADR (BYD) if shares experience a big dip then allocating a small portion of a portfolio to this equity makes sense.

Don’t forget there is now a high probability of Tesla losing its Shanghai factory in China once China seizes American businesses on the mainland. It doesn’t matter how much Musk kowtows to the communist party because this issue is far bigger than him or the EV business.

That threat has gone from almost 0 just recently to becoming somewhat plausible although still quite low. The tech world is accelerating at warp speed in 2023.

Mad Hedge Technology Letter

October 30, 2023

Fiat Lux

Featured Trade:

(WHY MEGACAP TECH IS THE ONLY SHOW IN TOWN)

(BIG TECH), (ETF), (COMPQ)

Megacap stocks continue to make hay when the sun shines in 2023.

The question is, why?

After all, many other great companies have arguably much better valuations, fundamentals, and affordable PE ratios.

Big tech stocks are expensive, yet buyers keep maneuvering to bid up the stock.

What gives?

The surge in the most hated sectors last year has been the main driver of this year’s stellar equity performance.

If we strip out tech, performance is actually negative if you can believe it.

The question is, why are professional managers seemingly chasing big tech like no other stocks exist?

The answer is more simplistic than you may think.

For investment managers, generating “alpha” is necessary to limit “career risk.”

If a manager underperforms their relative benchmark index for a time that is noticeable, they start to get in the firing line.

Currently, there are two drivers for the mega-capitalization stock chase. First, these stocks are highly liquid, and managers can quickly move money into and out without significant price movements.

The second is the passive indexing effect.

As investors change their investing habits from buying individual stocks to the ease of buying a broad index, the inflows of capital unequally shift into the largest capitalization stocks in the index.

Over the last decade, the inflows into exchange-traded funds (ETFs) have exploded.

That ETF issuance surge and the assets’ growth under management fuel the performance of the top 10 stocks. As we discussed previously:

Therefore, as investors buy shares of a passive ETF, the shares of all the underlying companies must be purchased.

Given the massive inflows into ETFs over the last year and subsequent inflows into the top-10 stocks, the mirage of market stability is not surprising.

Given stick high interest rates, inflation, and reversal of monetary liquidity post-pandemic, the risk of recession is higher than normal.

Higher interest rates, in particular, currently pose the largest threat to small and medium-sized companies.

The largest 10% of companies represent 62% of the overall non-financial market cap of the S&P 1500.

Smaller firms do not have the massive cash balances the megacap companies hold which puts them at a disadvantage.

As that debt wall of term loans hits over the next few years, higher borrowing costs are going to raise the risk of defaults and bankruptcies.

Tightening financial conditions have seen corporate bankruptcies rise by 71% since last year. If financial conditions are still elevated over the next few years, that bankruptcy risk increases markedly.

They weren’t able to lock into long-term loans at almost zero interest rates and pile it high in the money markets at variable rates.

Ultimately the pain for US small- and mid-cap companies will trigger the recession.

Portfolio managers must chase the market higher or potentially suffer career risk. Therefore, the easiest place to allocate cash is the mega-capitalization companies with low risk of bankruptcy or default and extremely high liquidity.

With the concentration of risk in a handful of stocks, the markets are set for a rather vicious cycle.

The concentration at the top keeps getting worse and I do believe we are one cycle away from the top 7 tech stocks comprising 35% of the total equity market.

It’s quite bizarre that something even remote could materialize, but that is where we stand where investors are looking for safety.

Throw in that most investors with a high net worth aren’t young, the tendency to go with a more conservative approach will shine through.

Funnily enough, tech investments in the big 7 constitute as conservative and it’s really true when I say that big tech has aged with its investor base.