Mad Hedge Technology Alerts!

Mad Hedge Technology Letter

November 22, 2024

Fiat Lux

Featured Trade:

(PICK YOUR SPOTS)

(NVDA), (TSLA), ($COMPQ)

Mad Hedge Technology Letter

November 20, 2024

Fiat Lux

Featured Trade:

(THE FUTURE IS HERE)

(NO CODE)

The future is here.

No code or low code will bring a raft of new innovative tech companies to market, and we are in the early innings of this transformative development.

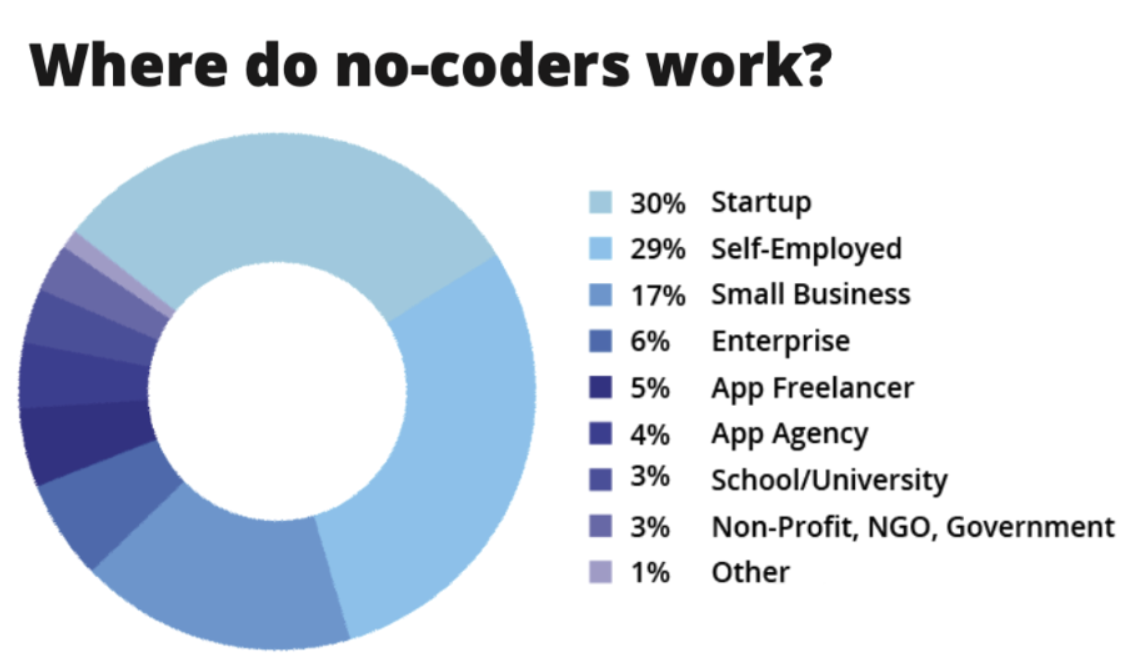

What is no code?

No-code is an approach to designing and using applications that requires zero coding or knowledge of programming languages.

This type of software hits us at a perfect time when the home office is beginning to become ubiquitous.

The self-service movement that empowers business users will support the creation, manipulation, and employment of data-driven applications.

If we turn back the pages of history, companies needed an army of software programmers to develop even the measliest application.

That was then, and this is now.

Fast forward to today, and automated technology doesn’t only include cutting-edge industries like automotive cars but also software on laptops that can be rejigged by individual entrepreneurs.

That’s right, one person with no coding experience will be able to design, develop, and offer a real-life application with meaningful business value without the help of expert programmers.

The research data backs up my thesis with research firms projecting a 23% increase in the global market for this type of technology.

During the pandemic, low-code/no-code tools saw steady growth due to their effectiveness in addressing some of tech’s most complicated challenges.

The essential need to digitize workflows and enhance customer and employee experiences will be a boost to the efficiency of commercial and operational teams.

No-code platforms have evolved from just facilitating mundane tasks to making it possible for a broader range of business employees to truly own their automation and build new software applications with no coding while increasing organizational capacity.

A few risks that larger companies might consider is that even for remote developers building new applications, governance is paramount.

IT staff will need to install guardrails in place and have those built into low-code/no-code platforms to maintain consistent levels of security across the organization.

Cybersecurity solutions need to be integrated into this workflow by training every employee at the organization on security behavior and using compartmentalization and limited access to prevent opportunities for mistakes.

Hard landings are hard to recover from, and some can be crippling to the business model.

For no-code companies, harmonizing workflows is a key requirement for success.

In a low-code/no-code organization, departments should be able to work without silos and communicate freely across functions.

Elevated performance enabled by low-code/no-code tools will mean that the number of useful apps hurling toward the marketplace will be more and merrier than ever before.

Higher performance will no doubt usher in a new renaissance of efficiency and even better performance.

This also puts a 3 or even 4-day workweek squarely in play.

Many of the best tech minds in the world have supported the concept of working smarter instead of working harder.

A low code/no-code standard will allow for these achievements to take place.

The cratering of costs to start and run a tech firm is affected, too.

Deploying startup capital to pay for other expenses will make it easier for successful incubation.

This will ultimately mean that this new type of tech company will need to embrace the fusion of IT and business staff, empowering them with composable applications to speed up the time to market for new solutions.

Low-code/no-code APIs and other tools are enabling companies to integrate new applications into their existing tech stack in a more seamless manner with a lift-and-shift approach vs a rip-and-replace.

At the entrepreneur level, individuals will be able to harness the technology to build $100 million companies with a snap of the fingers when it wasn’t possible to do it before.

This is finally a chance for the little guy to recapture their moxie in the vast and sometimes overwhelming business world.