Mad Hedge Technology Alerts!

In a world where natural disasters and global war has never been more common, there is one tech company whose fortunes are directly correlated in this types of chaos.

The tech firm and stock is Palantir (PLTR).

They specialize in disaster management software and even can sign contracts to prevent disaster management.

They apply unique software to deliver the best solutions for those they service, whether it is the U.S. military, a Fortune 500 company, or a state government looking at how to best allocate scarce resources during a torrid hurricane.

PLTR knows what to do, when to do it, and in what doses, and in 2024, that is a potent cocktail that has seen the company sign contract after contract.

It was only just a few months ago when PLTR was green lighted for a $99.8 million contract to extend access to the Maven Smart System to all military branches, including the U.S. Army, Air Force, Navy, Space Force, and Marine Corps.

The pact is a five-year firm-fixed price contract from the Army Combat Capabilities Development Command Army Research Laboratory aims to streamline access to current Maven Smart System capabilities, which utilize advanced artificial intelligence and machine learning.

Work is expected to enhance coordination between strategic and tactical operations, allowing the military to make informed decisions and fast actions.

Terms of the contract include support for AI-enabled battlespace awareness, global integration, force management, contested logistics, joint fires, and targeting workflows.

Combat vehicles from every military department will be outfitted by Maven to help them make the best decisions on the ground in real time.

The U.S. military and PLTR are also a common operational piece as part of its response efforts to aid in Hurricane Helene relief.

Maven specializes to facilitate battle space awareness, global integration, contested logistics, joint fires, and targeting workflows, but is being deployed to aid in the hurricane relief efforts.

While common operational tools and data systems have been used for disaster relief in the past, this marks the first time the Maven capability has been used for a hurricane.

The military is working to feed the data it is gathering directly to FEMA and other first responders. That includes general mapping data and data from various sensors that provide insights into things like road closures, communications, force movements, and which areas have yet to be serviced.

The system can also help with logistics by bringing in that data so that in real-time, based on the point of need and survey data from FEMA, food, water, medical supplies, or other goods can be reallocated to the best locations to serve citizens.

I’m not the one to wish ill on the populace, but it is almost a fact that the percentages of calamities that include natural disasters and kinetic wards have increased a great deal during the past 4 years.

There is not a company better positioned to take advantage of this through their best of breed software.

One thing I must note, management often dilutes shares by giving themselves vested shares, the stock tends to sell off big when these executives sell shares.

Wait for a big dip to jump in and ride the volatility higher.

Mad Hedge Technology Letter

October 9, 2024

Fiat Lux

Featured Trade:

(SQUEEZING COMPETITION)

(GOOGL)

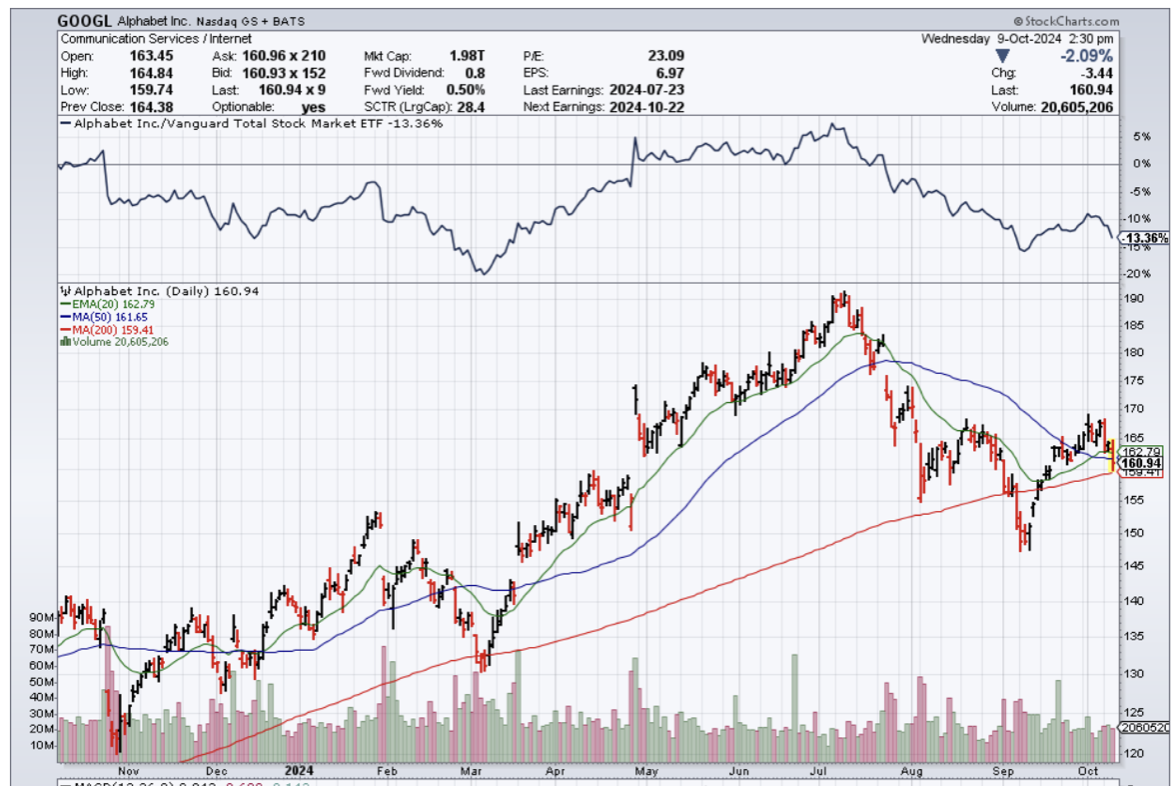

Regulators are inching closer to Mag 7, and that has major ramifications for the trajectory of tech stocks.

It has been a time coming for tech as they have turned from market darlings to quasi-monopolies.

Look at your daily life, and it is hard to get away from some of these services like Google.

That is why the US Justice Department said in a new court filing that it may break up of Google (GOOGL).

Its anti-competitive practices have made it hard for smaller companies to add to the American economy.

It seems as if Google has benefited too much from its success.

Naturally, Google did not agree.

That makes sense because executives at Google would be crazy to want to break itself up simply because they can extract larger compensation when presiding over the current model.

People like the CEO Sundar Pichai have no incentive to splinter the company into many different divisions.

He simply would get paid less, and he would finally have to compete harder.

The move by DOJ also sends a signal to other tech giants currently facing antitrust cases from DOJ and other Washington regulators as part of a wide-ranging effort by the Biden administration to rein in what it views as anticompetitive behavior across a number of industries.

The case against Google targeting its dominance in search resulted in a landmark decision and concluded Google illegally monopolized the online search engine market and the market for search text advertising.

The judge concluded that Google’s agreements with browser providers and devices powered by Google’s Android operating system stifled rivals from entering and growing within the markets.

Google pays as much as $26 billion per year to maintain its position on mobile devices such as Apple (AAPL) and Samsung smartphones.

The DOJ could also ask the judge to force Google to share the data that it uses to refine its search algorithms with rival browsers and search providers and limit the company's dominance over search text ads.

DOJ suggested the judge should also consider blocking Google from illegally monopolizing related markets, in addition to the search and search text advertising markets.

It may ask the judge to force Google to give websites more ability to "opt out" of "any Google-owned artificial-intelligence product."

Forcing Google to reveal its algorithms would be devastating to the business model.

Everyone would know their secrets, and other big tech could take anything usable and inject it into their own algorithms.

Algorithms are the secret sauce to many tech companies, and it will only become more valuable when infused by AI.

In the medium term, this caps any upside to Google shares.

In the short-term, I could see a bounce back after the bad news is priced in.

In the long term, if standalone divisions of Google’s businesses are created, like the ad and search business, being unshackled from old management could make some of these parts into new growth companies.

The unprofitable parts like Waymo might get terminated.

It would be sink or swim time because management isn’t going to prop up anything wasteful.

It would be good for the tech market as a whole, add more value, and deliver more equal competition, which the Feds are set out to do.

Either way, the breaking up of Google is more like a marathon and not a spring, but tech now has to wake up to existential threats that were never there before.