Global Market Comments

July 1, 2013

Fiat Lux

Featured Trade:

(MAD DAY TRADER IS NOW FOR SALE),

(AUGUST 1 MYKONOS, GREECE STRATEGY LUNCHEON),

(BE CAREFUL WHO YOU SNITCH ON),

(COULD YOU QUALIFY TO BECOME A US CITIZEN?)

I am pleased to announce that the The Mad Day Trader is now for sale, my first major upgrade to your service.

While the Global Trading Dispatch focuses on investment over a one week to six-month time frame, Mad Day Trader will exploit money-making opportunities over a ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.

Mad Day Trader uses a dozen proprietary short-term technical and momentum indicators to generate buy and sell signals. These will be sent to you by text message and email for immediate execution. During normal trading conditions, you should receive three to five alerts a day.

As with our existing service, you will receive ticker symbols, entry and exit points, targets, stop losses, and regular real time updates. At the end of each day, a separate short-term model portfolio will be sent to you and posted on the website.

The new service will generate long and short selling signals for a range of widely traded exchange traded funds (ETF?s). These include stock indexes (SPY), bonds (TLT), (TBT), foreign exchange (FXY), (FXE), (FXA), commodities (CU), (CORN), energy (USO), (UNG), and precious metals (GLD), (SLV). There is also a special focus on the leading hot stocks of the day. This will be followed up with a series of educational webinars that will be an important resource for the serious trader.

The Mad Day Trader service will be provided out of Chicago by my old friend and industry veteran, Jim Parker. Jim is a 40-year veteran of the financial markets and has long made a living as an independent trader in the pits at the Chicago Mercantile Exchange.

Jim has worked his way up from a junior floor runner to advisor to some of the world?s largest hedge funds. We are lucky to have him on our team and gain access to his experience, knowledge, and expertise. You will not find a better man in Chicago to look after your positions.

I have been following his alerts for the past five years, and his impeccable market timing has become an important part of the ?unfair advantage? that I provide readers. The time has finally come to offer Mad Day Trader as a stand-alone product.

A trading service with this degree of success and sophistication normally costs $20,000 a year. As a client of The Mad Hedge Fund Trader, you can purchase Mad Day Trader alone for $2,000 a year or $699 a quarter. Or you can buy it as a package together with Global Trading Dispatch, which we call Global Trading Dispatch PRO, for $4,000 a year, a 20% discount to the full retail price.

Existing subscribers to the Global Trading Dispatch are invited to upgrade their subscription to include both products. Just send an email to Nancy at customer support at support@madhedgefundtrader.com.

She will calculate the remaining value of your current subscription and give you a full credit towards the new one-year Global Trading Dispatch PRO subscription. She will then send you instructions on where to send a check. As no two amounts will be the same, our store is unable to handle personalized orders.

Part of the deal is that I want to hear from you on how we can evolve Mad Day Trader to make it more user friendly and coherent to better meet your needs. Sometimes, a couple of old warhorses like us forget how much our specialized language is incomprehensible to the outside world. Just send us an email with suggestions to support@madhedgefundtrader.com.

Come join John Thomas for lunch at the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting on the Greek island of Mykonos in the Aegean Sea on Thursday, August 1, 2013. A three-course lunch will be followed by a PowerPoint presentation and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, foreign currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $259.

The lunch will be held at major resort hotel on the south shore of the island, which can be found by steering a course of 120 degrees 99 nautical miles from the port of Piraeus. Just make sure you don?t run aground on the island of Andros on the way, as the tides can be treacherous. The pirates on Mykonos have already been dealt with. Moorings can be made available for private visiting yachts offshore. I will email more details with your purchase confirmation.

Bring your broad brimmed hat, sunglasses, and plenty of SPF 50 suntan lotion. You will need them. The Greek islands are cooking hot this time of the year. The dress is casual. Those not wishing to view the clothing optional beach can have a chair with its back to the sea. Accompanying spouses and significant others will be free to bill drinks to my personal account as my guest. Together we will plot the future of western civilization.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store.

Buried in the recently passed Dodd-Frank financial reform bill are massive financial rewards for turning in your boss. The SEC is hoping that multimillion dollar rewards amounting to 10%-30% of sanction amounts will drive a stampede of whistle-blowers to their doors with evidence of malfeasance and fraud by their employers.

If such rules were in place at the time of the settlement with Goldman Sachs (GS), the bonus, in theory, could have been worth up to $500 million. Wall Street firms are bracing themselves for an onslaught of claims, legitimate and otherwise, by droves of hungry gold diggers looking for an early retirement.

Don?t count on this as a get rich quick scheme. Government hurdles to meet the requirement of a true stoolie can be daunting. The standard of evidence demanded is high, and must be matched with the violation of specific federal laws. Idle chit chat at the water cooler won?t do. Litigation can stretch out over five years, involve substantial legal costs, and often lead to a non-financial settlement with no reward.

Having ?rat? on your resume doesn?t exactly look good either. Just ask Sherron Watkins, the in house CPA who turned in energy giant Enron?s Ken Lay, Andy Fastow, and Jeffrey Skilling just before it crashed in flames. Nearly a decade later, Sherron earns a modest living on the lecture circuit warning of the risks of false accounting, and whistle-blowing.

The coming Fourth of July celebration brings back memories of my late wife?s campaign to become an American citizen, who originally came from Japan.

Part of the process required a verbal quiz about US history and government. Our family spent a year energetically prepping her, with nightly grilling?s over dinner about the most obscure details of our independent form of government. She took cram courses and read a dozen prep books. By the time the test day came, she was a veritable constitutional law scholar, and any one of us could have qualified for a seat on the Supreme Court.

I drove her up to the Federal Building in Santa Rosa, California with the greatest trepidation. As the interviewing officer entered, the tension in the room was so thick, you could cut it with a knife. There were only three questions. No. 1: what colors are in the American flag (answer: red, white, and blue). No. 2: who was the first general of the US army? (Answer: George Washington). What are the three branches of government? (Answer: legislative, executive, and judicial).

I was stunned. All that work and she gets a test that a child could pass. Two months later we were in an auditorium on San Francisco?s posh Nob Hill with 1,500 others to be sworn in, which by tradition is led by an English applicant.

In 2008, the feds revamped the test to make it a little harder. Here are some sample questions. No. 1: who wrote the Articles of Confederation? (Answer: Alexander Hamilton). No 2: how many seats are in the House of Representatives? (Answer: 435 voting, six nonvoting). No. 3: How many amendments are there to the Constitution? (27)

Whoa! I?m not sure I could pass this test. Just as my SAT scores are probably too low to get into a decent school today, I?m not sure that I could meet the standard to become a citizen either. But over one million immigrants did last year.

Global Market Comments

June 28, 2011

Fiat Lux

(NOTICE TO SUBSCRIBERS

TAKING OFF FOR EUROPE)

My tux and white dinner jacket are packed, the hotels are booked, and the limo is waiting outside. The Cessna is fully fueled and the flight plan filed. I am taking off for my annual European Strategy Luncheon Tour.

Along the way I will be meeting with other hedge fund managers, senior government officials, CEO?s at major banks and Fortune 500 companies, large institutional investors, and a Nobel Prize winner or two. Getting out into the real world and soaking up new data and opinions in invaluable in shaping my own global view, and your performance benefits from it. Since I don?t stumble across these people in my living room, I have to seek them out.

After pit stops in Chicago and New York, I?ll board the Cunard Line?s Queen May II at the Brooklyn Cruise Terminal to take residence in the owner?s suite. As we pass over the wreck of the Titanic on the second day out, we?ll throw a bouquet of flowers as a mark of respect.

In London I?ll catch William Shakespeare?s A Midsummer Night?s Dream at the Globe Theater, spend an evening at the Royal Ballet, and visit the Royal Academy of Arts Summer Exhibition. At least one morning will find me catching an old-fashioned straight razor shave at the Jermyn Street Barbers, and topping up my supply of business shirts at Turnbull & Asser.

The cheese trolley at the Michelin restaurant is to die for. For accommodations I?ll be staying at the ever reliable, if not Spartan, British Navy Officers Club. You know, the place where Horatio Nelson used to drink with his junior officers?

I?ll then board the Orient Express for Venice, where the dinner is black tie only. Hopefully, there won?t be any murders this time. If a new Brioni suit and pair of Gucci shoes throw themselves upon me while I stroll through the Galleria in Milan I may be unable to resist.

In Geneva I?ll be consulting with the representatives of several Middle Eastern royal families while they vacation in the Alps. One afternoon will be devoted to taking the paddle wheel steamer on Lake Geneva to the Chateau de Chillon in Montreux where Lord Byron used to live, sipping fine Swiss white wines along the way.

The grand finale will be my annual assault on the Matterhorn at Zermatt, which at 14,692 feet, is higher than anything we have in the continental US. After training all year for this, it?s now or never. I spend my evenings there at public steam baths where, afterwards, I roll around in the snow and beat myself with birch branches. It is invigorating, to say the least.

I will be traveling with my laptop and keeping touch with the markets. While 18th century Internet service is passable, the bandwidth can be snail like. So unless I see something extraordinary, I will cut back on new Trade Alerts. After running up a 36% return in six months, and beating 99% of the hedge funds in the industry, I deserve a break. I need to spend some time alone on a mountaintop, communing with the spirits, attempting to discover the new long-term market trends through the mist.

While on the road, I will continue writing my newsletter, giving you my daily dose of market insight. I will also be re-running some of my favorite research pieces from the past. This is to expose my thousands on new subscribers to the golden oldies, and to remind the legacy readers who have since forgotten them. I will be back in San Francisco in mid August, glued to my screens once again for another year of toil. In the meantime, please feel free to email me.

Mad Day Trader, Jim Parker, will be putting the pedal to the metal to get his new product off the ground, and will be working straight through the summer.

In the meantime, I shall be raising a glass to all of you at dinner, the loyal readers of The Diary of a Mad Hedge Fund Trader. Salute! Prost! And Cheers! Thanks for making this letter a huge success!

If you want to take the opportunity to meet me in person, please find my strategy luncheon schedule below. To purchase tickets for the luncheons, please go to my online store at http://madhedgefundradio.com/ and click on ?STRATEGY LUNCHEONS?, and the city of your choice.

New York City - July 2

London, England - July 8

Amsterdam, Netherlands - July 12

Berlin, Germany - July 16

Frankfurt, Germany - July 19

Portofino, Italy - July 25

Mykonos, Greece - August 1

Zermatt, Switzerland - August 9

I?ll Meet You on Top

Global Market Comments

June 27, 2013

Fiat Lux

Featured Trade:

(UPDATED 2013 STRATEGY LUNCHEON SCHEDULE),

(THE BITTER MEDICINE FOR THE STATES),

(THE FALLING MARKET FOR KIDS),

(HOLLYWOOD CASHES IN ON WALL STREET TROUBLES)

Come join me for lunch for the Mad Hedge Fund Trader?s Global Strategy Updates, which I will be conducting throughout Europe during the summer of 2013. A three-course lunch will be followed by a PowerPoint presentation and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store at http://madhedgefundradio.com/ and click on ?STRATEGY LUNCHEONS?.

New York City - July 2

London, England - July 8

Amsterdam, Netherlands - July 12

Berlin, Germany - July 16

Frankfurt, Germany - July 19

Portofino, Italy - July 25

Mykonos, Greece - August 1

Zermatt, Switzerland - August 9

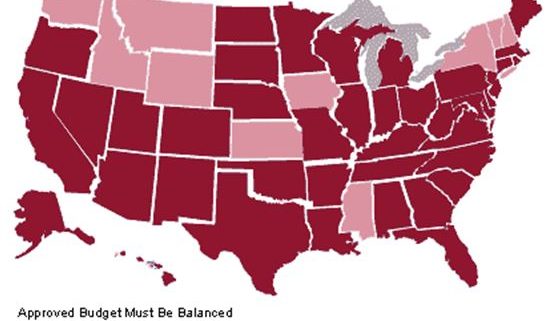

On a map, it appears that the United States is made up of 50 states. The fiscal reality is that we have 20 Portugal?s, 15 Italy?s, 10 Ireland?s, 3 Greece?s, and 2 Spain?s.

In the aftermath of the Great Recession, state GDP?s saw the sharpest drop since 1981. States shoveled money out of the economy nearly as fast as the Obama administration shoveled it in. During the bubble, the states wildly overestimated revenues, thought they were richer than they really were, and bulked up on social services as if the party would go on forever.

As a result, spending grew faster than the economy for many years, especially when it came to building new prisons. Because of the ephemeral nature of property and stock gains, that movie now has to run in reverse, and state services have to shrink down to what they can afford.

During the last two recessions, state and local governments hired, easing some of the pain at the local level. Not this time. Teachers, policemen, and firemen have been laid off with reckless abandon, the oldest and most expensive usually targeted to go first.

Entitlements, primarily state employee pension payments, are going to have to be the top priority, which in many cases now exceed those in the private sector. The headache is so huge that it is mathematically impossible for any tax increase to address the shortfall alone. No action at all brings slower economic growth and fewer jobs. This is all one reason why I am pounding the table for a long-term growth rate of 2%-2.5% which the financial markets have only recently started to embrace.