When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 10:05:472018-11-05 10:24:35Trade Alert - (CRM) November 5, 2018 - TAKE PROFITS

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 09:52:422018-11-05 10:23:02Trade Alert - (TLT) November 5, 2018 - TAKE PROFITS

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 08:13:192018-11-05 08:13:19November 5, 2018 - MDT Pro Tips A.M.

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE MAD HEDGE FUND TRADER HITS A NEW ALL TIME HIGH),

(AAPL), (FB), (RHT), (GE), (VXX), (AMZN), (SPY), (IWM), (CRM)

I used to do a lot of skydiving from 20,000 feet. There’s nothing like a freefall, feeling the wind rip at your jumpsuit as you plunge towards the earth at terminal velocity of 125 miles per hour. In the beginning, the ground looks very far away. Then it suddenly gets very close, very fast.

I used to do this during the 1960s with WWII surplus silk parachutes with a “double L” cut. You hit the ground like a ton of bricks. Sometimes, we’d swing back and forth from the wings of the airplane before letting go just to have fun and freak out the pilot who had no chute.

Over time, you develop a very accurate sense of how fast the ground is approaching and when to pull the ripcord. If you’re wrong, you die.

That’s how I felt when markets went into freefall last Monday. However, after a half-century of trading, I have a highly developed sense of where the bottom is.

So, I piled on the “bet the ranch” longs in technology stocks and shorts in the bond market right at the absolute bottom. And to make sure everyone to a man got in, shares swooshed down one final time when rumors spread that Trump was escalating the trade war with China once again.

By Wednesday morning, the Mad Hedge Fund Trader model portfolio had booked its largest two day gain since the inception of this letter 11 years ago, some 12%. By miracle of miracles, we ended up positive for October, virtually the only one to do so in the entire hedge fund industry.

I would like to think that 50 years of toil in the markets is finally starting to pay off for me. The truth is, the harder I work, the luckier I get.

Stocks lost $2 trillion in market value in October, off 6.9%. Other than that, how was the play, Mrs. Lincoln? Tech took the worst hit in a decade, with many favorites down 20%-30%.

I am raising as much cash as I can ahead of the Midterm Elections tomorrow. Democrats seizing the House of Representatives is priced into the market already.

If the Republicans end up keeping the House, you can count on at least a 1,000-point rally in the Dow Average in the next few days as the door is now open for more tax cuts, more deregulation, and more deficit spending.

If the Democrats end up taking both the Senate and the House you can look for a 1,000 point drop in the Dow. That would bring on a huge “flight to safety” bid in the bond market and yet another opportunity to sell short at great prices.

Either way, I want more dry powder with which to take advantage of any extreme moves that may take place. “Extreme” seems to be the order of the day.

By the way, we are so far in the money with our remaining positions that even with a 1,000 point drop we should still reap the maximum profit with the November 16 option expiration in only 9 trading days.

Not that it matters, but October Nonfarm Payroll Report came in at a red-hot 250,000. The headline Unemployment Rate remained at a two-decade low at 3.7%. The Broader U-6 “Discouraged worker” unemployment rate fell 0.1% to 7.4%.

For the first time in yonks, no sector lost jobs last month. HealthCare added 36,000 jobs, Manufacturing 32,000 jobs, and Leisure & Hospitality 42,000 jobs.

However, the real blockbuster was that Average Hourly Earnings exploded to a 3.1% YOY rate, the highest in ten years. Yes, ladies and gentlemen, this is what inflation looks like, up close and ugly.

The number immediately knocked the wind out of the bond market taking it to a new low for the year. Yes, this is what double short positions in bonds are all about. I saw this coming a mile off.

The backdrop for the bond market is looking worse than ever. The budget deficit is about to break $1 trillion for the first time since the 2009 crash. Rising interest rates mean the government’s debt burden is about to grow by leaps and bounds, eventually becoming its largest expenditure.

The US Treasury is hitting the markets daily with massive new issuance, and the Chinese are dumping what US bonds they have to support the Yuan, now at a ten-year low. This is what Armageddon looks like in slow motion.

Last week was dominated by a China trade war that was on again, then off, then on one more time. The stock market ratcheted four-digit figures every time this happened.

Apple (AAPL) announced record profits yet again but countered with cautious forward sales guidance. Social media pariah Facebook (FB) delivered an earnings report beyond all expectations popping the stock $10.

IBM took over Red Hat (RHT) for $33 billion, the third largest merger in history. It’s too little too late for Big Blue as the stock falls on the news. It all reeks of a “Hail Mary.”

General Electric (GE) cut its dividend from 12 cents a share to one cent after reporting a breathtaking $22.8 billion loss. The Feds have opened a criminal investigation into accounting practices. This may define the final bottom in the stock. Take another look at those long-term LEAPS.

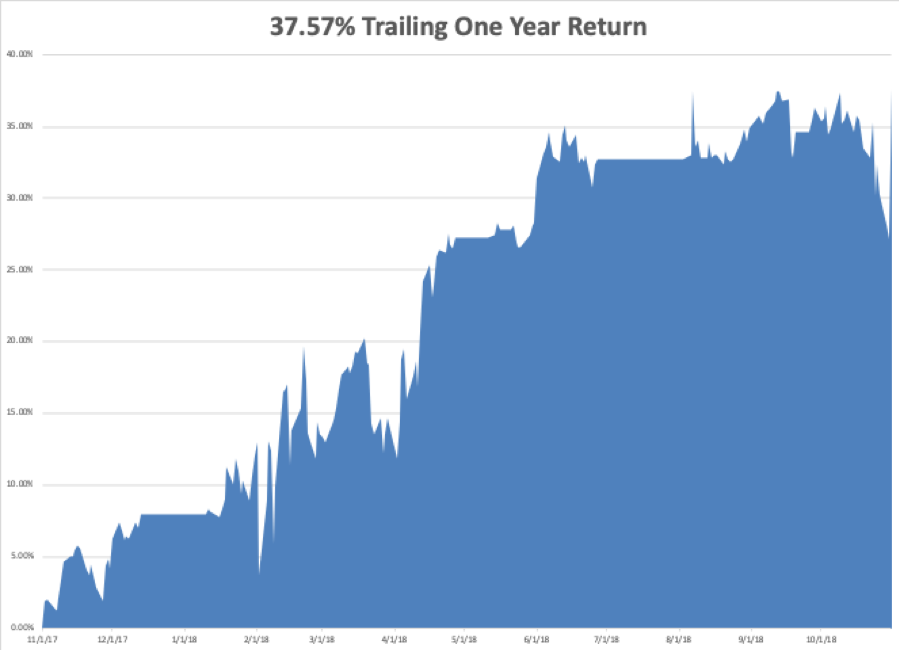

My year-to-date performance rocketed to a new all-time high of +33.17%, and my trailing one-year return stands at 37.57%. October finished at +1.24% and that includes an ill-fated -4.23% loss in the iPath S&P 500 VIX Short Term Futures ETN (VXX).

And this is against a Dow Average that is up a miniscule 1.9% so far in 2018. So far in November, we are up an eye-popping +3.54%.

Incredible as it may seem, the Mad Hedge Fund Trader has been up 18 consecutive months. That’s what you pay for and that’s what you’re getting. There’s nothing more fulfilling in life than making promises to friends, then delivering in spades.

As the market collapses, I scaled into longs in Amazon (AMZN), the S&P 500 (SPY), the Russell 2000 (IWM), and Salesforce (CRM). I used the flight to safety bid in the bond market to double up my short position there, and am kicking myself for not going triple weight.

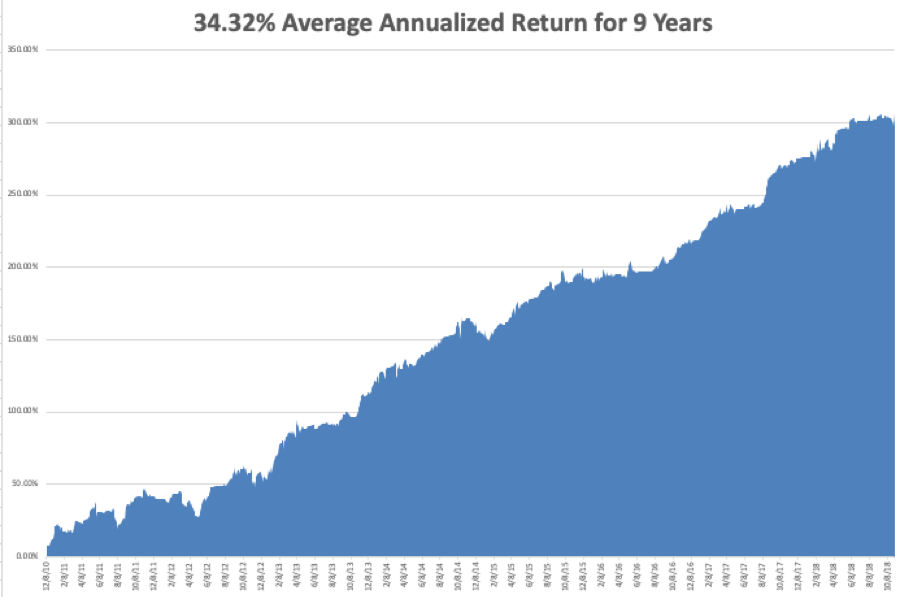

My nine-year return ballooned to 309.64%. The average annualized return stands at 34.72%.

All the BSDs are done reporting Q3 earnings and only a few tag ends are left to report. The carnage is over until we restart the cycle once again in February. In any case, economic data pales in comparison to the election in terms of market impact.

On Monday, November 5 at 10:00 AM, the ISM Manufacturing Index is out.

On Tuesday, November 6 is Election Day. Trading will be a subdued affair and the results will start coming out at 11:00 EST after the west coast polls close.

On Wednesday, October 24 we have the election aftermath to deal with. Up 1,000, down 1,000, or unchanged, who knows?

At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. The Federal Open Market Committee meets to discuss interest rates but will take no action.

On Friday, October 26, at 8:30 AM, the October Producer Price Index is out, an important read on inflation.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I made a massive amount of money personally in the October crash. I am going to plop down $150,000 and buy a brand new Tesla Model X for myself. The ashtrays are full on the old one, and besides, there is a tiny nick in the windshield from driving up to Lake Tahoe. I hear the new one has new “Summon” technology that allows it to drive into a parking lot by itself and drive around until it finds an empty space, then back into it, all untouched by human hands.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Knowing When You Hit the Ground is Crucial

My New Wheels

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/New-Wheels-nov5.png422564MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 05:31:312018-11-05 05:34:44The Market Outlook for the Week Ahead, or The Mad Hedge Fund Trader Hits a New All Time High

“If you put the federal government in charge of the Sahara Desert, in five years, there would be a shortage of sand,” said Nobel Prize-winning economist Milton Friedman.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/QOTD-nov5.png275412MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 05:30:322018-11-05 05:26:34November 5, 2018 - Quote of the Day

The biggest news of Apple’s earnings results was what Apple decided they will not do in the future – stop publishing iPhone unit sales.

I applaud CEO of Apple Tim Cook for putting this to rest because it is starting to get out of hand. The outbreak of criticism and grief targeted at Cook has to stop because analysts do not understand.

On one hand, it’s important to be aware of the metrics tech companies are judged on, but if analysts aren’t in tune to what these numbers mean in the bigger scheme of things, then it is irrelevant.

Apple is doing everything it can to turn into a software company. They are not interested in battling it out at the low-end of the totem pole because that path is a scrap down to zero margins.

Migrating up the value chain is something that management has identified, and this strategic shift should be met with rapturous celebrations.

Unit sales growth, gross payment value, and monthly views are all metrics that growth companies hold dear to their heart and a way to show to investors they are worth investing in regardless of the cash burn and cringeworthy operating margins.

Apple is way past that point if you haven’t noticed and should be focusing on how to monetize the existing base of customers.

Plain and simple, Apple is not a start-up growth company and taking away this reporting metric will help investors refocus on the real story at hand which is its core of software and services.

With software and services, profitability by way of innovative software offerings will be magnified and highlighted as the roadmap ahead.

As for the last batch ever of iPhone data, Apple has done a brilliant job, to say the least. They exceeded all expectations by smashing the average selling price (ASP) of iPhones at $793.

This is a monumental jump from $618 at the same time last year, a 28% YOY increase.

I did not say that Apple is the world’s best tech company at the Mad Hedge Lake Tahoe Conference, but I did say Apple is by far the highest quality company and this earnings report is a great example of that.

EPS routinely is beat and raised on a sequential basis.

Doubling down on the theme of quality is the revenue numbers from Japan which were up 34% YOY for a group of people who have the harshest view of quality control in the world.

Believe me, Japanese consumers have no desire to ever buy a Chinese smartphone.

The spike in ASPs was triggered by a flight to its collection of ultra-premium smartphones that has enthralled consumers. The ballooning ASP prices led iPhone revenue to spike 29% YOY to over $37 billion crushing the almost $30 million in quarterly revenue the prior year.

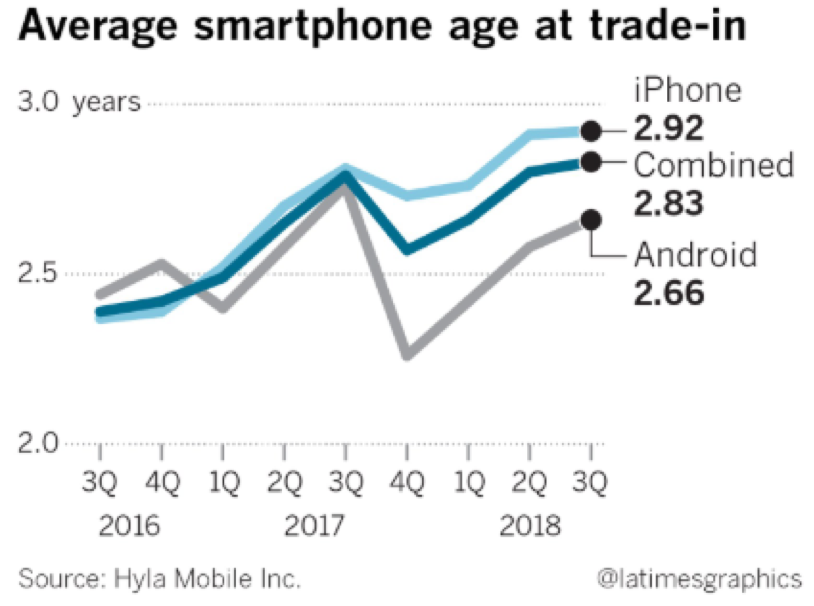

According to data from Hyla Mobile Inc., American iPhones traded in between July 1 and the end of September were 2.92 years old on average, up from 2.37 years old the same period two years earlier.

The reasons are two-fold.

Companies are producing better performing smartphones negating the need to impatiently upgrade right away.

The second reason is that they are just plain out pricey, and not everybody will have the dough to splurge on a new iPhone every year or two.

Thus, Apple has strategically placed itself in the correct manner by producing the best smartphone that customers will eventually adopt but carving out as much revenue while consumers are using their phones longer.

During this time, data usage has exploded as consumers are addicted to their smartphones and relying on a whole host of apps to complete their daily lives.

Apple would be stupid to not position themselves to capture this tectonic shift to more hourly data usage and breaking itself from the reliance of smart device revenue itself.

This is what other tech companies are doing like Roku, albeit at an earlier stage in their growth cycle.

In the future, smartphones will become obsolete replaced by something smaller, nimbler, and perhaps integrated with our brain or body or both.

Apple is also acutely aware that the bombardment of Chinese smartphones and the upward trend in the overall quality of these phones has siphoned off part of the iPhone market in specific segments of the world.

Thus, Apple has barely even touched the emerging markets of India that has been flooded by Chinese mid-tier phones without the branding power of Apple.

Apple doesn’t create these trends, they are merely stitching together smart decisions based upon them.

The next step is also a two-pronged proposition.

Apple needs a full-blown enterprise service based upon the cloud.

They can either buy one and they certainly have the cash to do so. Or they can develop one internally from scratch.

The second issue is that Apple also needs to widen its product service offerings that not only include an enterprise cloud option but also entertainment, news, sports, and everything else that could hook user’s attention and stick them to the iOS operating system until death.

Cementing users to the iOS operating system is the overall goal of all of this software infusion because if users start migrating over to the Android platform, it’s real game, set, and match for Apple as we know it.

Instead of myopic analysts focusing on “unit sales”, smart analysts should be focusing on whether what Apple is doing will tie future users to iOS or not.

I am happy with what I have seen so far but there can be a great deal of improvement going forward.

I think my 2-year-old nephew even knows that iPhone sales are maturing by now. This has not been a new story and I would call it poor reporting from a group of lazy-minded analysts.

It’s true that Apple rode the coattails of its miracle hardware products to a $1 trillion market cap. It was a magnificent achievement. I pat all who were involved on the back.

However, it’s clear as daylight that hardware is not what is going to propel Apple to a $2 trillion market cap.

Lost in all the smoke and mirrors is that revenue was up 20% YOY which is a staggering feat for a $1 trillion company.

Even more muddied in the rhetoric is that there has been minimal slowdown in China even after all the trade war jostling which is a miracle in its own right growing 16% YOY.

Software and services were up 27% YOY pulling in $10 billion and the Apple ecosystem has now reached 330 million paid subscribers, a growth of 50% YOY.

Paid subscribers are the most important metric to Apple now as it shows how many users are percolating inside their eco-system wielding their credit card around for software and services whether its maintenance spend or Apple pay.

Apple pay transaction volume tripled in the past year with four times the growth rate of FinTech player PayPal (PYPL).

Wearables still maintain broad-based growth climbing 50% YOY which is slightly down from the 60% YOY last quarter.

All of the wearables such as the amazing Apple Watch, AirPods, and Beats products have a nice supplemental effect to the Apple eco-system and is an over $10 billion business per year.

I am interested to see if Apple can make the quick pivot to an enterprise software company, and Apple’s announcement of Apple business manager, a method to deploy iOS devices at scale, had an initial sign up of 40,000 companies. Apple needs to bet the ranch on this direction and do it fast.

I would like to see Apple attack the enterprise market with zeal because there is a long runway for them to scale and the bulk of companies would welcome Apple products and services littered around their mobile offices.

The most important soundbite was by CFO of Apple Luca Maestri saying, “Given the increasing importance of our services business and in order to provide additional transparency to our financial results, we will start reporting revenue and total services beginning this December quarter.”

There you go…Apple explicitly saying they are the newest software company on the block that should go alongside the likes of Microsoft (MSFT).

The software theme will continue with the Mad Hedge Tech Letter because there are some real gems out there in the software landscape tied to the cloud.

As for Apple, the earnings report reaffirms my opinion that they just keep getting better and are magicians at adjusting to the current tech climate.

Wait for the stock to find some footing then it’s a definite buy, and for long-term holders, it’s a screaming buy.

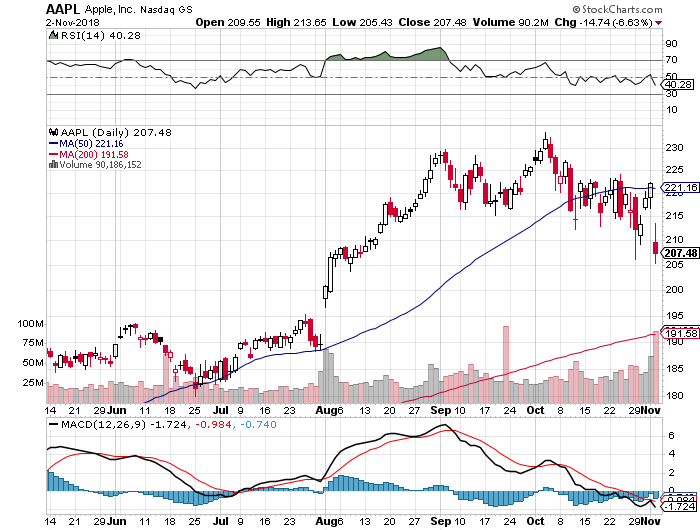

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/AAPL-chart-nov5.png606814MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 01:06:592018-11-02 17:11:08Get Ready for Another Bite of the Apple

“By giving people the power to share, we're making the world more transparent.” – Said Co-Founder and CEO of Facebook Mark Zuckerberg

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/Mark-Zuckerberg.png391272MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 01:05:012018-11-02 15:19:53November 5, 2018 - Quote of the Day

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-02 14:39:332018-11-02 14:39:33Trade Alert - (TLT) November 2, 2018 TAKE PROFITS

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.