As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

You know how I love second helpings, especially when the sushi bar is involved. I especially like unagi, or cooked eel, which is said to be an oriental aphrodisiac.

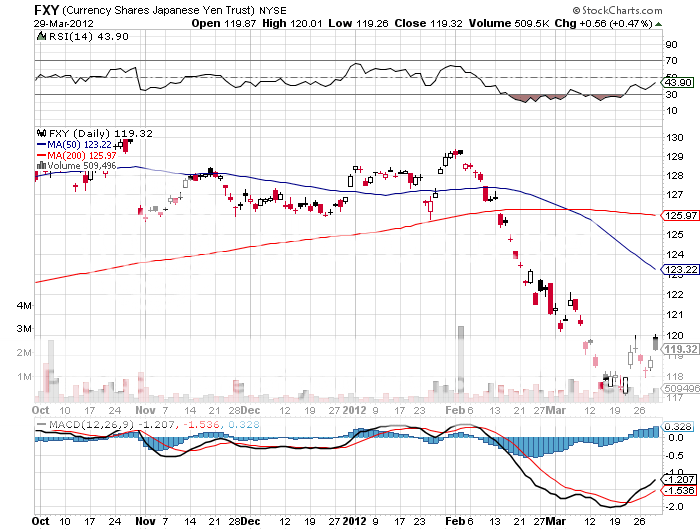

I am going to take advantage of Japan?s fiscal year end book closing on March 30 to reenter my short position of the Japanese yen. This is the one time a year when Japanese corporations suddenly repatriate yen back to Japan to beef up the cash on their books for their annual reports. Every year, this creates a quick boost to the yen against the US dollar which fades away in the following weeks like so much smoke.

Like everything else this year, the yen has had a straight line move since I put out my last call to sell the yen at the end of January. So while I made a nice profit on the first trade, I was never given another chance to reenter on the way down. Now I have that opportunity.

Since the yen bottomed on March 21, it has given back 25% of the move. Sure, I would prefer to get back in on the traditional one third pull back. But there are so few attractive trading opportunities out there right now that I am happy to jump the gun. If the yen strengthens more from here I will simply double up the position. This is a trade that I?ll be happy to live with for a while.

I have hammered away at the structural weakness of the Japanese economy ad nauseum for the past year. The one liner is that buyers of the country?s 1% yielding ten year bonds are dying off in droves, it has the world?s worst debt to GDP ratio, and labors under an Armageddon like demographic burden. It doesn?t help that they haven?t invested anything new since Godzilla ate the big screen. Sony (SNE) should have become Apple (AAPL). For those who wish to undertake a refresher course, please read the research pieces listed below:

* ?Momentum is Building for the Yen Shorts? on March 26 at http://madhedgefundradio.com/momentum-is-building-for-the-yen-shorts/

*? ?Nikkei Shows the Yen Move is Real? on February 20 at http://madhedgefundradio.com/nikkei-shows-the-yen-move-is-real/

*? ?Global Trading Dispatch Hits 64%, 11 Day Home Run on Yen Short? on February 13 at

http://madhedgefundradio.com/global-trading-dispatch-hits-64-11-day-home-run-on-yen-short/

*? ?Rumblings in Tokyo? on February 5 at http://madhedgefundradio.com/rumblings-in-tokyo/

*? ?Is This the Chink in Japan?s Armor?? on January 29 at http://madhedgefundradio.com/is-this-the-chink-in-japans-armor/

My preferred instrument here is the Currency Shares Japanese Yen Trust ETF (FXY) , where I will be buying the June, 2012 puts. At the very least, the (FXY) should make it back down to $117 in the near future, a price we visited just a week ago, which should give you a quickie 70%? return on the June $120 puts.

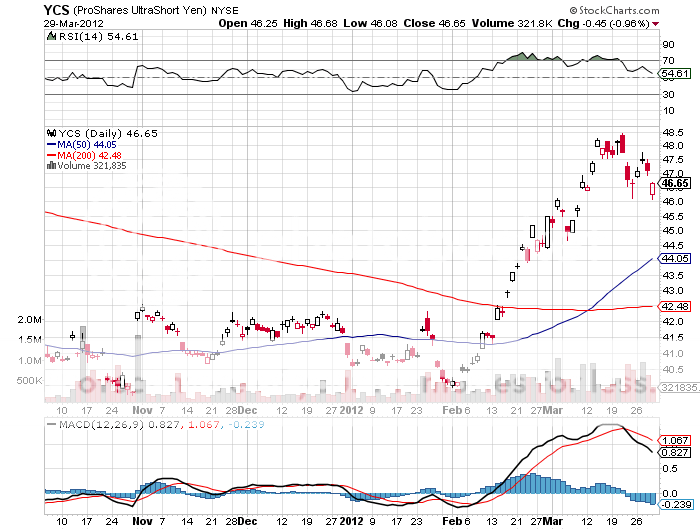

For those who are unwilling or unable to play in the options space, you can invest in the ProShares Ultra Yen Short ETF (YCS), a 2X leveraged bet that the yen falls against the dollar.

Do I hear Any Bids?

Japan?s Last Good Invention

This time I am going to start with the fundamental argument first, then follow up with the Trade Alert.

We are getting perilously close to a substantial pull back in global risk assets. While this has already started in commodities, the ags, oil, copper, and precious metals, we have yet to see the whites of their eyes in equities. I believe at these levels stocks are the planet?s most overvalued assets, at least on a short term trading basis. So I have begun more aggressively searching for plays that would benefit from substantial moves southward.

My personal preference is to gain downside exposure on small capitalization stocks. You can achieve this through buying put options on the Russell 2000 iShares ETF (IWM).

You have several things going for you in falling markets with this ETF. Small stocks are illiquid and therefore suffer the biggest pullback during market corrections. If Heaven forbid, double dip fears return this summer, small caps will fall the farthest and the fastest. They are most dependent on outside financing which rapidly dries up during times of economic distress.

You can see this clearly during last year?s summer swoon. The last time we thought the world was going to end, the (SPX) fell by 20% while the (IWM) plunged by 29.5%. This means that small cap stocks are likely to deliver 150% of the downside compared to big cap stocks. Making money then with shorts in the (IWM) was like shooting fish in a barrel.

You see this on the upside as well. Since the October, 2011 lows, the (SPX) leapt by 30% compared to a much more virile 38% move by (IWM). The (IWM) really does present the scenario where the smaller (or higher) they are, the harder they fall.

If you go into the options market you get this extra volatility at a discount. June at-the-money puts for the (SPY) carry an implied volatility of 15%, compared to 20% for the (IWM) puts. That means you get 50% more anticipated movement in the index for a premium of only 33%.

For those who wish to avoid options, you can buy the inverse ETF on the sector, the (RWM). But the liquidity for this instrument is a mere shadow of its upside cousin, the (IWM). You are better off shorting the (IWM) than buying the (RWM).

These Look Pretty Interesting

The handful of Chinese army officers I huddled with in the underground bunker all stared intently at their watches. Three, two, one, and then KABOOM! At exactly 12:00 noon, the blast of distant artillery sent a five inch shell screaming over our heads and exploded into the hill above us. The ground shook under our feet, causing dust to drift down from the concrete ceiling above us. It was 1976, and The People's Republic of China just let lose its daily symbolic protest against its errant rebellious province, known locally as the Republic of China, and to you and me, as Taiwan.

Fast forward 36 years later and the Middle Kingdom is sending salvos of money raining down on that prosperous island. Two years ago, China Mobile (CHL), the world's largest cell phone company, bought 12% of Far Eastone Telecommunications (4904.Taiwan). Although a small deal, it represented the first ever direct investment from China into Taiwan. The move triggered a takeover binge by big Chinese companies of their offshore cousins.

It was only a few years ago Taiwanese businessmen suffered long prison terms for just visiting, let alone investing in China, which they have done in a major, but surreptitious way, for 30 years. Readers of this letter are well aware of the long term attraction of both of these countries, which see GDP growth rates at a multiple of our own.

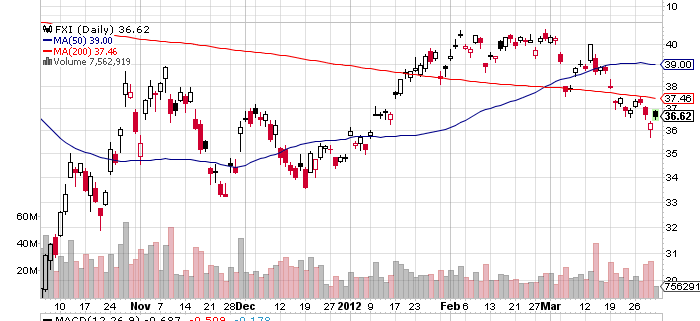

Closer ties between China and Taiwan auger well for the stock markets of the two high growth countries. The iShares MSCI Taiwan fund ETF (EWT) jumped by 17% in Q1, 2012. The iShares FTSE China 25 Index (FXI) has done less well, up 5%, as the country grapples with a temporarily slowing economy. At some stage, a country that is growing at four times our own rate, but at the same earnings multiple, will be a buy. But it appears not yet.

In the meantime, I guess that Beijing figured out that if you can't beat them, buy them. The proxy takeover bid is mightier than the sword.

?It's very difficult to navigate a business through a paradigm shift. You must hard wire your system to second guess all the time, questioning what is next, and then what is next. You've got to retain optionality for both investment portfolios and the business your run to navigate this well,? said Mohamed El-Erian, co-chairman of the bond house PIMCO.

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

A few years ago, I went to a charity fund raiser at San Francisco's priciest jewelry store, Shreve & Co., where the well-heeled men bid for dates with the local high society beauties, dripping in diamonds and Channel No. 5. Well fueled with champagne, I jumped into a spirited bidding war for one of the Bay Area's premier hotties, who shall remain nameless. She?s happily married to a tech titan now, and gentlemen don?t tell. Suffice it to say, she has a sports stadium named after her.

The bids soared to $10,000, $11,000, $12,000. After all, it was for a good cause. But when it hit $12,400, I suddenly developed lockjaw. Later, the sheepish winner with a severe case of buyer's remorse came to me and offered his date back to me for $12,000.? I said ?no thanks.? $11,000, $10,000, $9,000?? I passed.

The current altitude of the stock market reminds me of that evening. If you rode gold (GLD) from $800 to $1,900, oil, from $35 to $110, and Apple (AAPL) from $200 to $610, why sweat trying to eke out a few more basis points, especially when the risk/reward ratio sucks so badly, as it does now? I have a feeling that those who loaded up on stocks in March may develop the same sort of buyer?s remorse that I witnessed at Shreve?s.

I realize that many of you are not hedge fund managers, and that running a prop desk, mutual fund, 401k, pension fund, or day trading account has its own demands. But let me quote what my favorite Chinese general, Deng Xiaoping, once told me, ?There is a time to fish, and a time to hang your nets out to dry.?

At least then I'll have plenty of dry powder for when the window of opportunity reopens for business. So while I'm mending my nets, I'll be building new lists of trades for you to strap on when the sun, moon, and stars align once again.

See Any Similarity?

Time to Mend the Nets

ETF's are much more attractive than mutual fund competitors, with their notoriously bloated expenses and spendthrift marketing costs. You can't miss those glitzy, overproduced, big budget ads on TV for a multitude of mutual fund families. You know, the ones with the senior couple holding hands walking down the beach into the sunset, the raging bulls, etc? You are the sucker who is paying for these. Sometimes I confuse them for Viagra commercials.

I once did a comprehensive audit on a mutual fund, and a blacker hole you never saw. There were so many conflicts of interest it would have done Bernie Madoff proud. Any trainee assistant trader can tell you that more than 90% of all mutual fund managers reliably underperform the indexes, some grotesquely so. Published performance is bogus, they show a huge survivor bias, not including the hundreds of mutual funds that close each year. And there's always that surprise tax bill at the end of the year.

If there was ever an industry crying out for a fundamental restructuring, consolidation, price competition, and ultimately a whopping great downsizing, it is the US mutual fund industry. ETF's may be the accelerant that ignited this epochal sea change, with the number of mutual funds recently having shrunk from 10,000 to 8,000. It's still early days, with ETF's only accounting for 5-6% of trading volume, even though they have been around for a decade.

The Mutual Fund's Days Are Numbered