Below please find subscribers’ Q&A for the May 29 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Since Elon Musk is raising tons of money for his AI startup called xAI, will this impact Tesla’s (TSLA) stock price?

A: Yes, it's a very positive move for Tesla because anytime Elon Musk raises money anywhere in his network, it takes the need off of him to sell Tesla shares for cash. And I think his xAI will be the next trillion-dollar company, and SpaceX is in front of it as another trillion-dollar company. Those stocks, he can sell any time and raise a lot of money, but the other two are still private companies. We can't buy them yet unless we buy some of the public vehicles offered by venture capitalists like Ron Baron who has heavy positions in both Tesla and SpaceX. So, no direct plays yet on these companies, but no doubt when they become incredibly valuable, he'll take them all public and become the richest man in the world two or three times over. So yes, that is a positive.

Q: Where do you think (TLT) will be in the next few months?

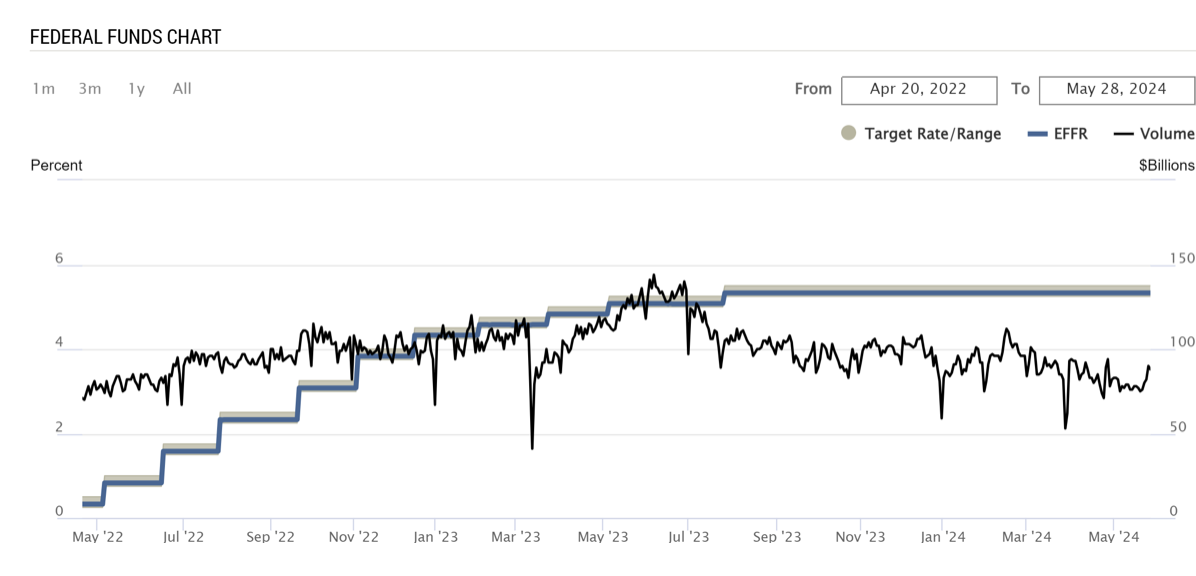

A: In a narrow trading range. I think we're basically in a $86 to $91 trading range, and we'll go nowhere until we get clarification on Fed interest rate cuts. At the rate the economy is slowing, we may get one in September, and even if the Fed doesn't cut, the rest of the world will, including Japan, Europe, Great Britain, and so on. So we may get our interest rates dragged down here by foreign countries that all have much weaker economies than the US.

Q: Should I keep buying big tech stocks after Nvidia's (NVDA) blowout earnings?

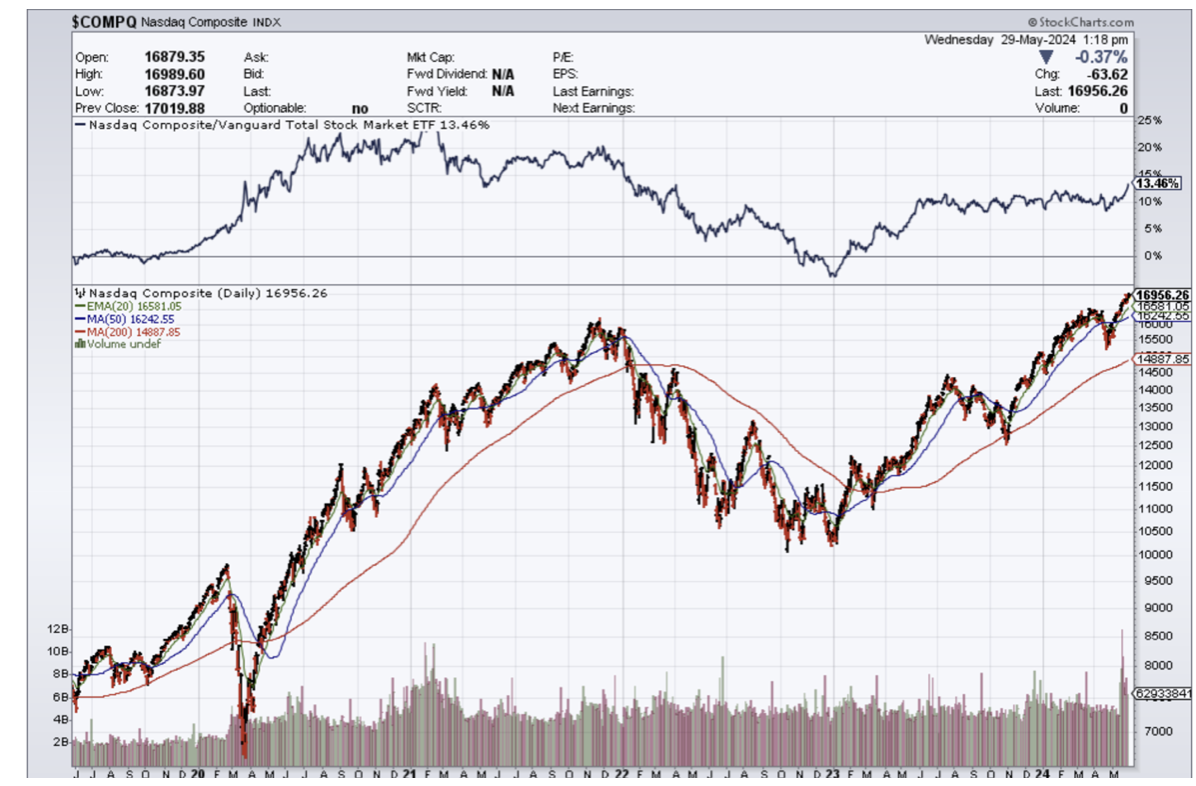

A: Well, if you recall back in the ancient times of April, Nvidia had a 20% sell-off, and most of the tech stocks were down at least 10%. So, I would wait for the next 20% sell-off of Nvidia not only to buy Nvidia but all other big tech stocks as well, because it basically is a big tech story and will continue for the rest of the year like that. So we're really looking to buy dips among the big tech winners, and those would include Amazon (AMZN), Meta (META), Microsoft (MSFT), and so on.

Q: How long can the US economy go without a recession?

A: Five years. The way our economic cycle works is after a long period of growth, companies get overconfident, over-invest, create excessive capacity in the markets for everything, and that leads to a crash and a recession, deflation, and lower interest rates. So even if we don't get major moves in the (TLT) upside now, you always will over the long term get interest rates going back to 2 or 3% for the 10-year so it’s a great long-term hold. That is the economic cycle—that's what creates bear markets and it’s known as “Boom and Bust”. Long may it live because that’s where we traders earn our crust of bread. But this time may be different. We may go longer than 5 years because AI is still in its infancy, still rolling out, and the number of companies making actual profits in AI will go from 3 to 300 over the next five years.

Q: I'm looking to buy gold in an investment account (GLD). Would you do that now, if so, what would you recommend?

A: I would recommend GLD (SPDR Gold Trust) because the metals are still outperforming the miners, miners being held back by the inflation rates unique to the mining industry, which are much higher than the 3.3% for the general economy. And if you want to add a little more spice to your portfolio, buy some silver (SLV) because it is rising at three times the rate of gold thanks to Chinese speculation. You might buy some copper while you're at it too—it's moving almost as fast as gold is.

Q: Which big tech firm is next to issue a dividend?

A: That's an easy answer, it's Netflix (NFLX). But there's a more important question out here— Which is the next tech stock to issue a stock split? And guess what the answer is? Netflix again, which needs to declare both a dividend and a stock split. It's at an all-time high, has a very high share price, and over time, stocks that split deliver double the performance of the S&P 500. So, the mere announcement will suck in a lot of new retail investors as we just saw with Nvidia (NVDA), where we got a $250 move on the split announcement. So, watch your splits, and in fact, I'm going to be devoting a major piece of next Monday's newsletter to splits and how to play them.

Q: Why has the stock market been so strong this year when interest rates are high?

A: The answer to that is AI. We are still in the very early days of AI, and as I mentioned earlier, only three companies are making money from AI right now. That's Nvidia (NVDA), Microsoft (MSFT), and Google (GOOG). That number will increase as AI moves down the food chain and everybody starts using it, including you and me. I view the AI development as similar to 1995 when all of a sudden we got Netscape, a navigator that made the Internet available to the public, Dell Computers (DELL), and Microsoft (MSFT) software all at once hitting the market and creating the online economy essentially from scratch. Something of that magnitude is what the stock market is discounting now. Think of it in terms of the revolutionary new technologies of 1995, which means we have another 5 or 6 years to go, and that's why the stock market is so strong.

Q: Should I invest in Berkshire Hathaway (BRK/B), or do you think their magic will run out soon?

A: I don't think their magic will ever run out. Of course, the day that Warren Buffett dies it'll be down 10%, but then you'll want to buy it with both hands because Warren has already replaced himself with a first-class management team who is carrying on his strategy. Any selloffs in Berkshire you get this summer, go in there and buy the calls, the call spreads, the stock, the LEAPS, and the kitchen sink. Still a great long-term BUY, and I see $500 either late this year or next year in (BRK/B).

Q: I'm a member of IM Academy.

A: Oh my gosh. I would let your membership expire, except you're probably on auto-renewal, and the only way to stop your subscription is to call your credit card company and ask them to block the billings. That is the problem with these predatory financial newsletters, they're impossible to get out of, even when they promise refunds anytime.

Q: Are there any Chinese stocks you like now?

A: No, but the highest quality stock in China is Alibaba (BABA). It's basically a combination of Amazon and PayPal in China, but you still have a very high political risk investing in anything in China. The currency is very weak, so better fish to fry is my opinion. And I tend to avoid countries suffering from demographic implosions.

Q: Should we buy (TLT) now or wait?

A: I would wait until we get some upside momentum going and we complete a few more downside tests.

Q: What's the best place to put cash in the summer?

A: The answer is always good old 90-day US Treasury bills. They are still paying 5.25%.

Q: What are your thoughts on PayPal (PYPL)?

A: I'm avoiding that sector because of over-competition crushing profit margins; that has been a problem for a couple of years now. Don't confuse “gone down a lot” with cheap.

Q: Which oil companies are the best to invest in right now?

A: You can buy Exxon Mobil (XOM) for the high dividend and the sheer size of the company. My second is Occidental Petroleum (OXY), because Warren Buffett owns 25% of the company, has shrunk the float, and that has a result in magnifying any moves up in the stock. Also, I somewhat admire Warren Buffett's stock-picking ability. And of course, I’ve been following the California company OXY since 1970, back when it was run by Armand Hammer, a friend of Vladimir Lenin, so my connections with the company go back a very long time.

Q: Do you like DuPont (DD) for the three-way split?

A: I do, but DuPont has a major problem looming with lawsuits over the PFAS chemicals—those are the forever chemicals which are all over the country, all over the food supply, and cause cancer. So that could be sort of like a Johnson & Johnson-type liability problem with the talcum powder. So again…why look for trouble? Buying a stock facing that kind of liability could be another tobacco situation.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Bob Dylan was right: "The times they are a-changin'". And for Pfizer (PFE), those changing times mean navigating a post-pandemic world and a looming patent cliff. Can they rise to the challenge, or will they be singing the blues?

Pfizer hardly needs an introduction. Founded 175 years ago in 1849 and publicly listed in 1942, Pfizer boasts a market cap of over $160 billion, with highly liquid options trading against its equity.

However, this stock has been on a bit of a rollercoaster lately.

With revenues exceeding $240 billion between 2021 and 2023, largely from vaccines and cancer treatments sold in over 200 countries, Pfizer's reach is undeniable.

But after hitting a record high of $61.71 a share in December 2021, it's taken a nosedive – more than a 50% drop.

So, what gives? Well, it's mostly a combo of waning demand for their Covid-19 products and the dreaded patent cliff looming over some of their top-selling drugs.

At the moment, Pfizer's portfolio paints a mixed picture, with some drugs shining brightly and others facing a cloudier future.

Their pneumonia vaccine duo, Prevnar 13 and 20, remains a reliable workhorse, raking in $6.4 billion in FY23, a 3% increase. With Prevnar 20's patent secure until 2033, it's a safe bet for continued success.

Eliquis, the blood thinner co-marketed with Bristol-Myers Squibb (BMY), is also holding its own, bringing in a respectable $6.7 billion in FY23, up 5%. However, the looming threat of generic competition in 2028 could put a damper on its future prospects.

On the other hand, Vyndaqel, a combination heart and nerve drug, has been a true standout, boasting a remarkable 36% jump in revenue to $3.3 billion in FY23.

Doctors have embraced it for treating a heart condition called ATTR-CM, but its patent situation remains uncertain with a potential expiration in 2024, unless Pfizer's extension to 2028 is approved.

Not all is rosy in Pfizer's garden though.

Comirnaty, their COVID-19 vaccine, may still be pulling in a hefty $11.2 billion in FY23, but it's a far cry from its FY22 peak. Sales have plummeted 70%, and those booster shots aren't exactly flying off the shelves anymore.

As for Paxlovid, the once-promising COVID-19 treatment, this drug has suffered an even more dramatic fall from grace, with revenue crashing 92% to $1.3 billion in FY23. To add insult to injury, Uncle Sam returned a staggering 6.5 million treatment courses.

Meanwhile, Ibrance, their breast cancer treatment, is also feeling the heat, with sales down 6% to $4.8 billion in FY23. It's facing tough competition overseas and its patent is set to expire in 2027, adding further pressure on its future performance.

To make matters worse, several other Pfizer blockbusters – Inlyta, Xeljanz, and Xtandi – are also staring down the barrel of patent expiration in the next few years.

This looming patent cliff poses a significant challenge for Pfizer, as these drugs have been major contributors to their revenue stream.

The company will need to rely on its pipeline of new drugs and strategic acquisitions to offset the potential losses and maintain its position as a leading player in the pharmaceutical industry.

Does that mean, then, that the $43 billion Seagen acquisition in December 2023 could become a lifeline for Pfizer?

Facing a double whammy of declining blockbuster sales and the looming patent cliff, Pfizer isn't sitting idly by. Seagen brings a fresh arsenal of patent-protected cancer-fighting drugs to the table, including three promising antibody-drug conjugates (ADCs).

Two of these, Adcetris for Hodgkin lymphoma and Padcev for urothelial cancer are already showing blockbuster potential, having raked in $751 million and $479 million, respectively, in the first nine months of 2023, despite the acquisition's timing.

But Pfizer's ambition doesn't stop there.

With five new therapies and six label expansions slated for oncology alone by 2026, they're banking on biologics like ADCs to fuel their growth.

They predict these cutting-edge treatments will surge from 6% to 60% of their cancer revenues by 2030, potentially yielding eight new blockbusters.

For now, Seagen's arrival is a much-needed boost to their oncology sales, which dipped 4% to $11.6 billion in FY23, even with Seagen's $120 million contribution in the final weeks of the year.

While the Seagen acquisition helps Pfizer tackle its goals of dominating oncology and fueling pipeline innovation, it's not the whole picture.

Pfizer's got a few other tricks up its sleeve: maximizing new product performance, trimming costs, and playing the capital allocation game to keep shareholders happy.

They're even planning a $3 billion spending spree from late 2023 through 2024, aiming for a cool $4 billion in annual cost savings. Talk about tightening the belt while expanding the empire.

Speaking of empires, Pfizer's 4Q23 results were a bit of a wake-up call.

Earnings per share (EPS) tanked to $0.10 (non-GAAP) on revenue of $14.2 billion, a far cry from the $1.14 EPS and $24.3 billion revenue of the previous year.

For the full year, EPS dropped a whopping 72% to $1.84 (non-GAAP), with revenue down 42% to $58.5 billion.

But, if you ignore those pesky Covid-19 products (Comirnaty and Paxlovid), the top line actually grew a bit – 8% in Q4 and 7% for the whole year.

Just remember, that Paxlovid revenue reversal in Q4 wasn't pretty, slashing both GAAP and non-GAAP EPS by $0.54.

Fast forward to Q1 2024, and Pfizer's numbers were a bit more cheerful, at least compared to what the analysts expected.

Non-GAAP EPS came in at 82 cents, a solid 30 cents above the consensus.

Revenue did fall 19.5% year-over-year to $14.9 billion, but even that beat estimates by $900 million.

Management's still sticking to their FY2024 guidance of $58.5 billion to $61.5 billion in revenue and $2.15 to $2.35 in non-GAAP EPS. We'll see if they can deliver.

That Seagen deal wasn't cheap, though, adding a hefty $31 billion to Pfizer's debt pile. As of March, they had about $12 billion in cash and marketable securities against over $61 billion in long-term debt. Yikes.

Still, management's determined to keep raising those quarterly dividends, now up to $0.42 a share in early 2024. That's a lot, considering it ate up 91% of their non-GAAP earnings in FY23 and is projected to gobble 78% in FY24.

With all that debt, don't expect any more stock buybacks in 2024. Pfizer's taking a break from that game, just like they did last year.

Despite Wall Street's lukewarm reception to Pfizer's patent cliff strategy, it's important to remember that this pharmaceutical giant is far from down for the count.

So, sure, Pfizer's 2023 revenue took a 42% nosedive compared to 2022, but let's not forget: over 620 million people worldwide still rely on their meds.

They actually scored nine FDA approvals, sold more pharmaceuticals than anyone else on the planet, and they're not sitting idly by while their product sales decline. Clearly, they're making moves.

The current bargain-basement price of Pfizer's stock, trading at a P/E of 10.4 on FY25E EPS, coupled with a juicy 5.9% yield, might just be the cherry on top for savvy investors willing to bet on the company's ability to navigate these turbulent times. Whether they can pull it off is anyone's guess, but at this price, it might be worth a gamble.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-05-30 12:00:302024-05-30 11:33:31Scaling The Cliff

In a move that has sent shockwaves through the artificial intelligence (AI) landscape, Elon Musk's xAI startup has secured a staggering $6 billion in a Series B funding round. This substantial investment propels the company forward in its quest to compete with major players in the rapidly evolving AI industry, most notably OpenAI, the creator of ChatGPT. The funding, backed by prominent investors such as Andreessen Horowitz and Sequoia Capital, represents a significant step forward for xAI, which was founded just last year.

Musk's History in AI: A Complicated Relationship

Elon Musk, the visionary entrepreneur behind Tesla and SpaceX, has a complex history with AI. He co-founded OpenAI in 2015 but departed in 2018 due to disagreements over the company's direction. Musk has since been vocal about his concerns regarding AI's potential risks, advocating for ethical and responsible development. With the launch of xAI, Musk aims to steer the course of AI innovation while ensuring alignment with human values and safety considerations.

The Rise of xAI: A New Contender Emerges

Despite its relative newness, xAI has already made significant strides in the AI domain. It has introduced the Grok chatbot, designed to integrate seamlessly with the X platform, formerly known as Twitter. The chatbot has garnered attention for its advanced capabilities, including long context understanding and image recognition. With the recent infusion of capital, xAI is poised to accelerate its research and development efforts, potentially leading to groundbreaking breakthroughs in AI technology.

The AI Race: Competition Heats Up

The AI landscape has become increasingly competitive, with a slew of startups vying for dominance alongside established players like OpenAI and Google. Microsoft's substantial investment of approximately $13 billion in OpenAI and Amazon's backing of Anthropic with $4 billion underscores the high stakes involved in the race for AI supremacy. xAI's substantial funding now positions it as a formidable contender, armed with the resources to potentially disrupt the status quo.

xAI's Strategy: A Focus on Safety and Ethics

While the specifics of xAI's strategy remain under wraps, the company has emphasized its commitment to building safe and beneficial AI systems. Musk has repeatedly voiced concerns about the potential risks of unchecked AI development, including the possibility of AI surpassing human intelligence and posing existential threats. xAI aims to mitigate these risks by prioritizing transparency, accountability, and ethical considerations in its AI research and development.

The Impact of xAI: A Game Changer in AI?

The emergence of xAI as a well-funded and ambitious player in the AI race holds the potential to reshape the industry in several ways. Firstly, it could accelerate the pace of innovation, as xAI's deep pockets and talented team of researchers push the boundaries of what is possible with AI. Secondly, xAI's emphasis on safety and ethics could set a new standard for responsible AI development, influencing the practices of other companies in the field. Finally, xAI's focus on integrating AI with social media platforms like X could revolutionize the way users interact with and consume information online.

Challenges Ahead: Navigating Complex Terrain

While xAI's prospects appear bright, it faces significant challenges in its pursuit of AI dominance. The company must navigate complex technical, ethical, and regulatory landscapes. Developing cutting-edge AI models requires substantial resources, expertise, and time. Ensuring the safety and alignment of these models with human values poses a significant challenge, given the potential for unintended consequences and biases. Additionally, evolving regulatory frameworks around AI could impose constraints on xAI's operations and development.

The Future of xAI: A Promising Outlook

Despite the challenges, xAI's substantial funding and Musk's ambitious vision make it a company to watch in the AI space. The company's emphasis on safety and ethics could set a positive precedent for the industry, fostering a more responsible and sustainable approach to AI development. If xAI succeeds in achieving its goals, it could usher in a new era of AI innovation, one that prioritizes the well-being of humanity alongside technological advancement.

The Global Implications of xAI's Rise

The rise of xAI and the intensifying AI race have significant global implications. AI has the potential to transform industries, economies, and societies on a global scale. It could lead to increased productivity, efficiency, and innovation in various sectors, ranging from healthcare and education to manufacturing and transportation. However, it could also exacerbate existing inequalities, displace jobs, and pose security risks if not managed responsibly. The international community must work together to ensure that AI development proceeds in a way that benefits all of humanity, rather than exacerbating existing problems.

The Role of Government and Regulation in AI

The rapid advancement of AI technology has raised important questions about the role of government and regulation in shaping its development. Some experts advocate for a light-touch approach, allowing companies to innovate freely while relying on self-regulation and ethical guidelines. Others argue for more stringent regulations to mitigate potential risks and ensure that AI is used for the benefit of society as a whole. Striking the right balance between fostering innovation and protecting public interest is a complex challenge that requires careful consideration and collaboration between policymakers, industry leaders, and civil society.

The Ethical Imperative of AI Development

As AI becomes increasingly powerful and pervasive, the ethical implications of its development become ever more pressing. Issues such as bias, discrimination, transparency, and accountability must be addressed head-on to ensure that AI systems are fair, equitable, and trustworthy. The development of AI should be guided by a strong ethical framework that prioritizes human values, dignity, and well-being. This requires a collaborative effort between researchers, developers, policymakers, and the public to create a shared understanding of the ethical challenges and opportunities presented by AI.

Conclusion

The race for AI supremacy is in full swing, and xAI's substantial funding has catapulted it into the spotlight as a major player. With Elon Musk at the helm and a commitment to safety and ethics, xAI has the potential to disrupt the industry and set a new standard for responsible AI development. The company's progress will be closely watched by industry insiders, policymakers, and the public alike, as it navigates the complex challenges and opportunities presented by the rapidly evolving field of artificial intelligence.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2024-05-29 16:46:002024-05-29 16:46:00Elon Musk's xAI Raises $6 Billion to Challenge OpenAI in Fierce AI Race

Rates will stay higher for longer and the higher income bracket will carry the US economy through any conflict with short-term inflation.

What does that mean for tech stocks?

It will trend higher for longer.

Sure, US rates will stay elevated, but tech stocks have proven they are tough to keep down with elevated inflation.

Most who buy tech stocks have done very well financially in the past 18 months.

There is a high likelihood that higher rates won’t affect their purchasing power to buy more tech stocks.

I do admit a big chunk of Americans are missing out on buying tech stocks at these current prices – I don’t diminish that.

The big spenders have utilized their 3% fixed mortgage to hunker down and continue to spend on devices, software, EVs, and other tech.

This clearly means that 5% isn’t the real neutral rate that the Fed is looking for and I view this rate as a relatively loose fiscal policy that is allowing high-income Americans to splurge on more tech products.

Don’t forget that these are the same stockholders that are reaping increasing tech dividends, higher-tech stocks, and generous shareholder returns.

Further evidence is that the $2 trillion in quantitative tightening along with a 5% Fed Funds rate has resulted in the S&P index rising 37%.

That’s not supposed to happen if rates are high above the neutral rate.

What the Fed gets wrong is that the neutral rate has moved significantly higher when we consider the trillions that were printed for the pandemic programs and stimulus checks.

The additional amount of fiat paper floating around chasing a limited amount of goods results in the neutral rate being somewhere closer to 8-10% and that development gets missed by the Fed.

Therefore, 5% Fed Funds rates are “high” and a lot higher than 0%, but the wealthy have now used this rate as a tailwind to progress their financial goals.

Wealthy households right now can earn upwards of 4.5% in a high-yield savings account, see their tech portfolios go up 20% in a year, and are watching the value of their real estate holdings surge higher.

Given the amount of wealth concentrated among a handful of US households and the skew on the income distribution in the US, just about any change in monetary policy will be regressive, advantaging those with more at the expense of those with less.

Tuesday's consumer confidence reading — while registering a three-month high — was far from a clear-cut judgment from Americans that things are looking up, economically speaking.

If the Fed holds at 5% and fails to erect rates closer to 8%, tech stocks will grind higher.

Rates would need to be at a nominal number that would give pain to higher-income buyers.

My personal view is that the Fed will stand pat at 5% interest rates and the Nasdaq should perform well in this scenario.

If we get talk of 6 or 7%, tech stocks will produce a minor pullback delivering another fabulous opportunity to buy.

The other piece here is Nvidia delivering stellar earnings and that should keep the shine on high-quality tech stocks when the market sets up to make the next move.

My bet is any dip will be bought ferociously and any “dip” could turn out to be more of a sideways time correction before we rip higher.

This is also why Nvidia is close to 81% above its 200-day moving average and boasts a current $2.7T valuation.

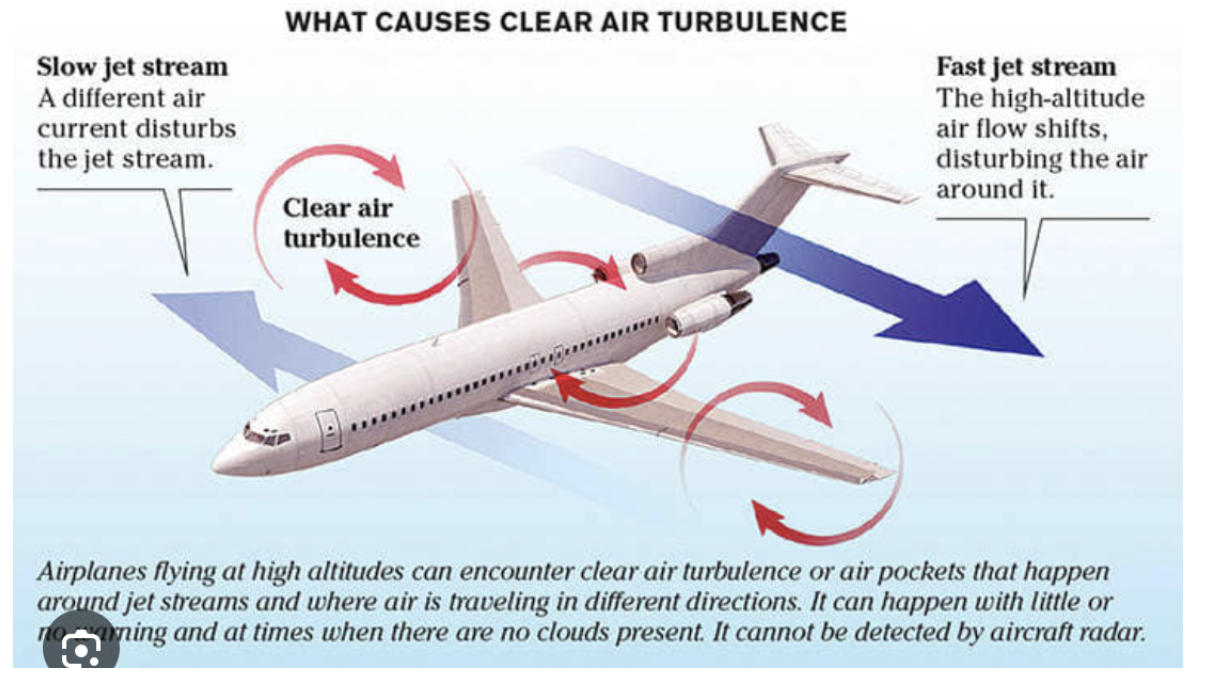

(BUCKLE UP WHEN FLYING - CLIMATE CHANGE MAY BE INCREASING CLEAR-AIR TURBULENCE)

May 29, 2024

Hello everyone,

Scientists at Reading University in the UK have studied clear-air turbulence.

Their research shows that severe turbulence has increased by 55% between 1979 and 2020 on a typically busy North Atlantic route.

Scientists have found that changes in wind speed at high altitudes due to warmer air from carbon emissions have played a role.

Prof. Paul Williams, an atmospheric scientist at the University of Reading has co-authored a decade-long study in this area.He argues that the focus should be on investing in improved turbulence forecasting and detection systems to prevent the rougher air from translating into bumpier flights in the coming decades.

Flight routes in the USA and North Atlantic have seen the largest increases in turbulence.Europe, the Middle East, and the South Atlantic also have seen significant increases in turbulence.

Prof Williams explained that increased turbulence was due to greater wind shear – or differences in wind speed – in the jet stream, a strong wind system blowing from west to east, about five to seven miles above the Earth’s surface.Williams further shows that it exists largely due to the difference in temperature between the world’s equator and poles.

While satellites can’t see the turbulence, they can see the structure and the shape of the jet stream, allowing it to be analysed.

Radar can pick up turbulence from storms, but clear-air turbulence is almost invisible and hard to detect.

We all know that turbulent flights are uncomfortable, but they can also cause injuries for those on the flight.Severe turbulence is very rare, but clear-air turbulence can come out of the blue when passengers are not belted in.

It is sensible to keep your seat belt fastened all the time, unless you are moving around.

The financial costs for airlines can be huge.The aviation industry loses between $150 and $500 million in the US alone annually because of turbulence, including wear and tear on aircraft.There is also an environmental cost, as pilots burn up fuel avoiding the turbulence when they can.

A case in point is the Singapore Airlines flight (SQ321) from London to Singapore on May 21.About 10 hours into the flight when the staff were serving breakfast, the airline hit severe clear air turbulence passing over the Irrawaddy Basin (Myanmar).The crew requested an emergency landing at Bangkok airport as one of the passengers had died.At least 50 people were injured including two crew members and a toddler.All were admitted to a hospital in Bangkok; some had serious injuries.More than 20 were admitted to ICU with spinal injuries.(Many people were obviously not wearing their seatbelts).

On Sunday, May 26 a Qatar Airways flight from Doha to Dublin experienced clear air turbulence but managed to land safely in Ireland.12 people were injured and eight were taken to hospital.

In August 2023 a Delta flight hit severe turbulence about 40 miles outside of Atlanta catapulting passengers out of their seats.Another incident involving an Allegiant Air flight last July that was flying from North Carolina to Florida.One passenger described the experience like being in “The Matrix.”

NASA is working on a way to detect clear-air turbulence.

The technology, under development at NASA’s Langley Research Centre and involving government, university and private sector experts, anticipates using ground-mounted infrasonic microphones that can pick up ultralow frequencies produced by turbulence -possibly as far as 300 miles away.

Such microphones could provide an early warning for what’s known as “clear-air turbulence,” the top cause of inflight injuries and fatalities, according to researchers at the University of Reading.

Clear air turbulence differs from other forms of turbulence in several ways, and it can occur without warning at altitudes of 20,000 to 40,000 feet.The unstable air masses can be as much as 100 miles wide and 300 miles long, and they often are found just above the jet stream core, researchers say.

Turbulence is expected to get worse as the world warms.

Prof. Williams and his team at the University of Reading project that the frequency of clear-air turbulence events will double by 2050 and that the intensity of such events will increase by as much as 40%.

The NASA research effort could make flight crews, passengers, and aircraft more resilient to that future.

Market Update

The summer season is almost upon us.A retracement is imminent in the DOW and S&P500 in line with retracements in the metals sector and Bitcoin & crypto in general as well.

S&P500 – expecting a pullback to 5221 or as far as 5140.

DOW – looking for trendline support around 37810 price point.A lower price point would be 37000.

US tech 100 – looking for consolidation now towards the 18450-price level.18085 possible support level before a further rally in the tech sector.

GOLD- looking for a correction back towards the 2275 price range and potentially as low as 2220.Subsequent profit targets for further highs sit at 2482 and 2689.

SILVER – expecting retracement towards 3050.Following correction, the metal will rally toward the longer-term target of 3470.

US dollar –expecting a short-term rise in the USD basket towards 10800 before a decline to the 10,000-price zone.So, you should be looking to short the US dollar in 4-6 weeks and buy the EURO, POUND Sterling, and Australian dollar.

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.