Global Market Comments

May 2, 2024

Fiat Lux

Featured Trade:

(THE UNITED STATES OF DEBT)

(TLT)

Global Market Comments

May 2, 2024

Fiat Lux

Featured Trade:

(THE UNITED STATES OF DEBT)

(TLT)

SAN MATEO, CA – May 1, 2024 – Franklin Templeton, a global investment management leader, today announced a groundbreaking collaboration with Microsoft to develop a state-of-the-art financial AI platform. This transformative initiative will reshape the financial services landscape, blending Franklin Templeton's investment expertise with Microsoft's cutting-edge AI technology. The platform promises to redefine personalized client experiences and streamline operations within the financial industry.

Transforming Financial Services Through AI

The collaboration marks a significant turning point in how financial institutions leverage artificial intelligence. By harnessing Microsoft's Azure AI services—including Azure OpenAI Service (GPT-4 model), Azure AI Search, and Azure AI Document Intelligence—Franklin Templeton will be uniquely positioned to create a platform tailored to the specific needs of the financial industry.

"The future of how we work with clients to best meet their desired investment outcomes will require strong technological resources," said Jenny Johnson, President and CEO of Franklin Templeton. "The newly introduced platform we are developing is specifically tailored for investment management, leveraging the full range of Microsoft's AI resources, as a key driver of investment success."

The aim is to create an AI-driven system that delivers unparalleled personalization, enhanced risk management, and superior investment strategies. Franklin Templeton expects to provide its clients with highly tailored investment insights and recommendations, optimizing portfolios in response to rapidly shifting market conditions.

The Promise of Personalized Services

A crucial focal point of this partnership is offering a seamless, highly personalized experience for every client. The AI platform will analyze vast amounts of client data – including risk tolerance, financial goals, and investment preferences – to deliver customized advice and portfolio solutions.

"This partnership is not simply about harnessing AI; it's ultimately about human connection and better client experiences," said Satya Nadella, Chairman and CEO of Microsoft. "Microsoft's technology will allow Franklin Templeton to offer truly individualized financial solutions, helping people achieve their goals with the insight and agility that the market demands."

Unlocking Operational Efficiency

Beyond personalized client experiences, the new financial AI platform promises to redefine operational efficiency within Franklin Templeton. The platform is expected to automate routine tasks such as data analysis, report generation, and compliance monitoring. By streamlining these processes, Franklin Templeton's investment professionals will have more time for high-value activities like client consultation and strategic decision-making.

This enhanced efficiency, enabled by AI, is poised to boost productivity and reduce costs, ultimately resulting in a more focused and streamlined operational model for Franklin Templeton.

A Collaboration Focused on Innovation

The Franklin Templeton-Microsoft partnership marks a convergence of two industries committed to innovation and transformation. Franklin Templeton's deep understanding of financial markets complements Microsoft's leading expertise in cloud computing and artificial intelligence. The synergy is expected to catalyze further advancements in financial services.

Analysts predict this groundbreaking collaboration will inspire similar partnerships across the industry, paving the way toward broader AI adoption in a traditionally conservative sector.

Responsible AI Integration

Given the critical and sensitive nature of financial services, the partnership places a strong emphasis on responsible AI principles. Both Franklin Templeton and Microsoft have pledged to prioritize transparency, explainability, and fairness in the development and deployment of AI solutions.

The companies acknowledge that earning and maintaining trust is crucial to the success of their efforts. Clients will have clear insights into how their data is used to power AI-driven recommendations, with continuous communication around the processes.

A Vision for the Future of Finance

The Franklin Templeton-Microsoft alliance heralds a new era in financial services: one where AI empowers a deeply personalized client experience, optimizes complex processes, and ultimately drives better investment outcomes.

"We strongly believe the collaboration with Microsoft is essential to Franklin Templeton’s strategic commitment to leveraging technology to drive investment success for our clients while simplifying the complexity of wealth management," commented Johnson.

Mad Hedge Technology Letter

May 1, 2024

Fiat Lux

Featured Trade:

(THE BIG RETAILER DIVING INTO FINTECH)

(WMT), (PYPL)

The takeaway I get from Walmart’s (WMT) push into fintech is that fintech is becoming mighty crowded in the short-term and this trend most likely won’t change anytime soon.

Walmart has been one of the big companies trying to beef up online commerce so it’s no surprise that wants to marry up this initiative with an in-house digital payment mode.

It could be that sometime in the near future that the likes of PayPal, Klarna, and Affirm who don’t have their e-commerce platform will be muscled out of this digital payment space.

Walmart’s in-house fintech startup One has begun offering buy now, pay later loans for big-ticket items at some of the retailer’s more than 4,600 U.S. stores.

The move puts One raises the question of whether major retailers need the help of outside payment apps.

Right now, Affirm, the BNPL leader has been the exclusive provider of installment loans for Walmart customers since 2019.

One is a mobile one-stop shop for saving, spending, and borrowing money.

Affirm helped the WMT generate $648 billion in revenue last year.

Ironically enough, offerings from both One and Affirm are available at checkout, and loans from either provider are available for purchases starting at around $100 and costing as much as several thousand dollars at an annual interest rate of between 10% to 36%.

Electronics, jewelry, power tools, and automotive accessories are eligible for the loans, while groceries, alcohol, and weapons are not.

One’s no-fee approach is especially relevant to low- and middle-income Americans who are “underserved” financially.

One could generate roughly $1.6 billion in annual revenue from debit cards and lending in the near term, and more than $4 billion if it expands into investing and other areas, according to Morgan Stanley

Walmart can use its scale to grow One in other ways. It is the largest private employer in the U.S. with about 1.6 million employees, and it already offers its workers early access to wages if they sign up for a corporate version of One.

Fintech players including Block’s Cash App, PayPal, and Chime dominate account growth among people who switch bank accounts and have made inroads with Walmart’s core demographic.

The three services made up 60% of digital player signups last year.

One has the great advantage of being majority-owned by a company whose customers make more than 200 million visits a week.

It can offer them enticements including 3% cashback on Walmart purchases and a savings account that pays 5% interest annually, far higher than most banks, according to customer emails from One.

One has access to Walmart’s sizable and sticky customer base, the largest in retail and that is worth a lot right there.

It’s entirely feasible that Walmart keeps growing its digital platform and in-house fintech app to somewhat look like a tech company in a few years.

I’ve written a few times about how Walmart is mimicking many of the best practices from the great tech companies and who knows, they might even employ a cloud division to take care of its own data and warehouse operations.

The day where outsourcing much of the data to software companies is very much over for big companies like WMT who are making deep inroads and investment into their tech prowess.

WMT’s stock has always been given that non-tech premium and I believe that will slowly change around as the growth rates start to pick up.

WMT is one of those American companies that are strongly positioned to do well in inflationary times and picking up all the $100,000 per year white collar professionals is a massive victory as they figure out ways to monetize this higher spend base.

This is a great company to buy on any dip and hold long term.

“The most terrifying words in the English language are: I'm from the government and I'm here to help.” – Said Former US President Ronald Reagan

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

( THE YEN IS FACING A DILEMMA)

May 1, 2024

Hello everyone,

Welcome to May, and what could be a continuation of the market behaviour we saw in April. The market is in the doldrums about what the Fed might say on Wednesday. Investors are already interpreting and theorizing possible outcomes, hence putting the market on the back foot.

As we wait to decipher the Fed’s stance on the road ahead, let’s look at what Bank of America thinks about this market correction.

According to the firm, investors should not panic. Instead, they should use the downside movement as a promising entry point before the market swings back to the green this summer.

It’s that ‘buy on the low, sell on the high’ idea. Most of the reluctance to buying at these times comes from the mindset: ‘But, what if the market (or stock) goes lower?’ Answer: you buy in small parcels at different levels, average in.

That’s how I approach the market. Take what the market gives you.

During election years, headwinds in April and May can be expected. But this is mostly temporary. Seasonality supports buying the dip prior to a summer rally. Volume indicators for the S&P 500 are suggesting a pause ahead of upsides in the summer.

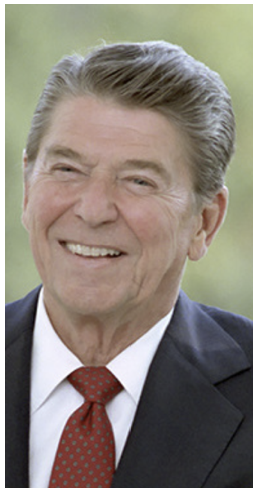

Why is the Japanese Yen cratering?

The Japanese stock market has been rallying over the past few years. From its Covid-induced low in 2020, the Nikkei has run to a record high of over 38,000. That gallop has even outdone the U.S. S&P500 over the same period.

Japan’s previous three decades saw stagnant performance and low economic growth. Now in 2023/2024, we see Japan’s stock market entering a new era of strength, but alongside this strength, the Japanese Yen has collapsed.

On Monday morning the Yen briefly touched 160, a 34-year low compared to the U.S. dollar. However, in what may have been the Bank of Japan's intervention, the dollar dived below 157 in a heartbeat not long after the low was reached. In January 2023 the Yen was sitting at 129. So, what gives?

The Yen’s collapse can mostly be explained by the rising U.S. interest rates. The currency’s fortunes are mostly tied to expected interest rate differentials. In other words, the Yen will fluctuate in accordance with the anticipated difference between the interest rates in Japan and other parts of the world, most particularly the U.S.

So, when the U.S.’s interest rates are higher than Japan’s, it puts pressure on the yen. And the reasons for this are twofold. Firstly, due to Japan’s low interest rates, the yen is often used in the so-called “carry trade.” This means investors can borrow at a low interest rate to invest in an asset with a higher return. So, you might see a fund manager borrowing yen and investing it in a higher-yielding foreign instrument, pocketing the difference.

The interest rate differentials between Western powers and Japan also impact investment and hedging in Japan’s $4.2 trillion portfolio of overseas assets. When Japanese investors see that interest rates are far higher in other developed nations, they’ll often increase their investment in these overseas assets, pulling down the yen. Hence the rising interest-rate differential between the U.S. and Japan has become quite a dilemma for the yen over the past few years.

In the short to medium term, there is little likelihood of change here for JPY/USD. With the resilient U.S. economy and inflation showing signs of accelerating, many believe the Fed is unlikely to cut interest rates soon, which will see the yen remaining at the mercy of developments, particularly in the U.S.

But the tide will eventually turn. U.S. and European central banks will eventually cut their respective interest rates, lessening the painful interest-rate differential for Japan.

Bank of America argues that the Bank of Japan may hike rates in the third quarter, and the U.S. could cut rates. This would then pave the way for yen appreciation.

QI Corner

Cheers,

Jacquie

Global Market Comments

May 1, 2024

Fiat Lux

Featured Trade:

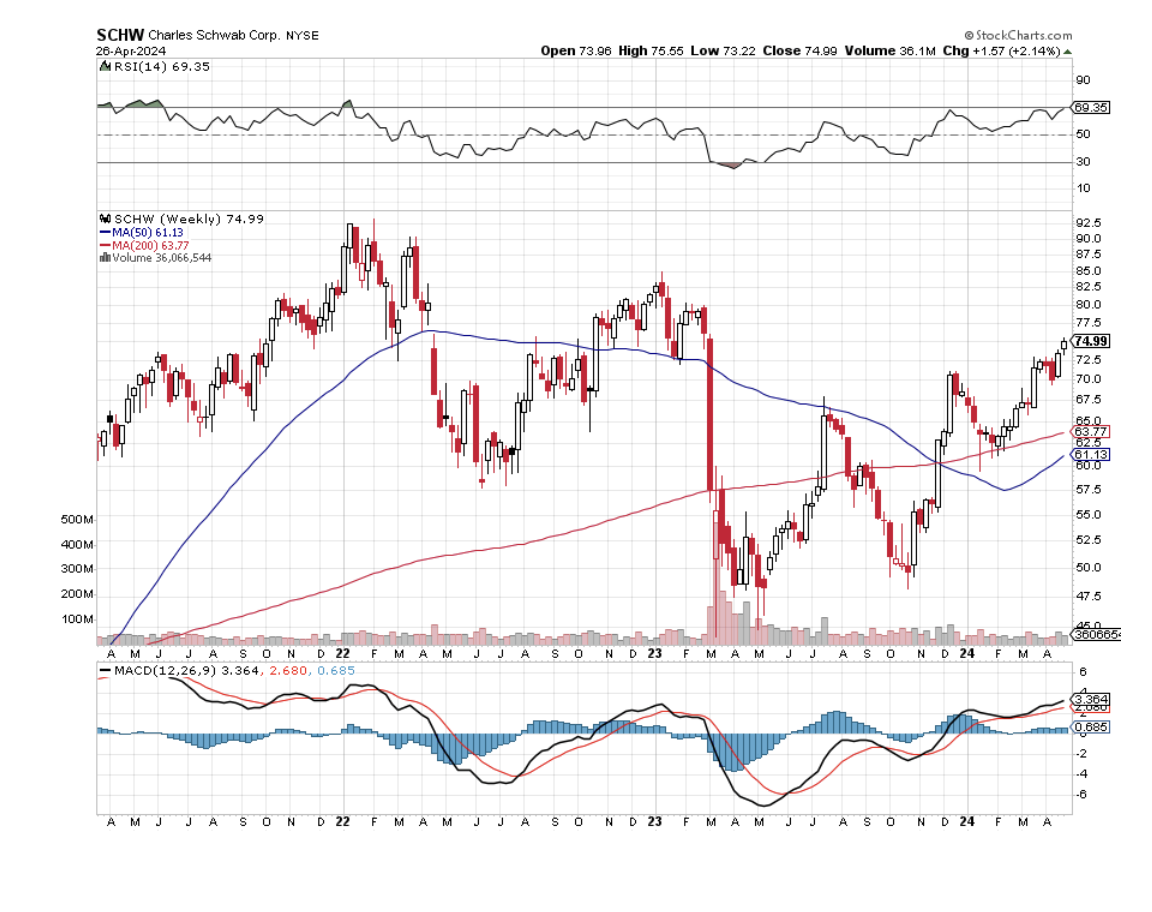

(SEVEN REASONS TO BUY CHARLES SCHWAB),

(SCHW), (TLT), (GS), (MS), (C), (BAC),

(TESTIMONIAL),

(TAKING A BITE OUT OF STEALTH INFLATION)

Looking for a financial to add to your tech-heavy portfolio?

I think the nimble investor can pick up shares of online broker Charles Schwab (SCHW) and gain an outsized return.

That’s assuming that the current correction in the stock market remains in single digits, and doesn’t explode into a full-blown bear market.

There are many things that can go right with (SCHW).

Of the major online brokers, Charles Schwab pays the highest tax rate. With the least amount of international business, it is unable to hide billions of dollars tax-free offshore, as do (GS), (MS), (BAC), and (C).

It therefore pays the highest tax rate of the major financials and will be the most to benefit from any tax cut, if and when that ever happens.

Big funds have been soaking up the stock all year.

That leads to the second play. With the smallest amount of international earnings, the company will suffer the least from a coming weak US dollar.

With 90-day US Treasury bill ticking at 5.39% this morning, the greenback will almost certainly remain strong for a few more months. Once the cuts start, look out below.

Since financials are the one sector most sensitive to interest rates, (SCHW) should do well when rates fall.

At a 4.70% ten-year yield, we are closer to the bottom in all fixed-income yields than the 2020 top at 0.32%.

Personally, I don’t think the ten-year will go any lower than 5.10% in this cycle.

Here is the fourth reason to pick up some (SCHW).

When my New American Golden Age resumes, stock markets will rise threefold and volumes will explode.

The retail investor will make a long-awaited return to investing in equities.

Ever wonder why your online brokers keep disappearing?

Why TradeMonster get taken over by Option House, which then was swallowed by E-Trade?

It’s the major players making bets that financials will become the top-performing sector of the next decade. Always follow the big money.

This makes Charles Schwab a takeover target.

And if Schwab doesn’t get bought out, it will benefit from reason number six, a huge concentration of the industry that will finally allow commissions to RISE instead of fall, as they have over the last four decades.

Reduced competition always leads to higher profits. If you’re not convinced look no further than the airline business.

Charles Schwab originally sprang from a well-written newsletter from the 1960s and is now both a bank and brokerage firm, based in San Francisco, California.

It was founded in 1971 by Charles R. Schwab and was one of the earliest discount brokerage houses. It is now one of the largest brokerage firms in the United States.

The company provides services for individuals and institutions that are investing online.

(SCHW) offers an electronic trading platform for the trade of common stocks, preferred stocks, futures contracts, exchange-traded funds, options, mutual funds, and fixed-income investments.

It also provides margin lending and cash management services. The company also provides services through registered investment advisers.

It is not cheap, with a price-earnings multiple of 31, but it does offer a dividend of 1.33%.

This is a market that is all about expensive stocks getting more expensive, which cheap stocks (retail) get cheaper.

(SCHW) total market capitalization stood at $110 billion at the end of trading yesterday.

Of course, there’s the seventh reason to buy the shares of Charles Schwab.

I have the box next to the one owned by (SCHW) founder and CEO Charles Schwab himself at the San Francesco Opera House.

At the intermission for the season opener for Puccini’s Turondot, I asked him what he thought about the price of his shares here.

All he would say was “I’m not selling”, and gave me a wink.

The last time I bet on a wink like that, I got a double in the shares.

That’s good enough for me.

Dear John,

I loved your trades this year!

10% plus in a day? I’ll take as many of those as you can dream up.

And pulling this off in this boring market is incredible.

After reading BS and extreme negativity in my other newsletters all day long, you are a breath of fresh air.

Keep them coming.

David

Austin, Texas