Regular readers of this letter are well aware of my fascination with demographics as a market driver.

They go a long way towards explaining if asset prices are facing a long-term structural headwind or tailwind.

The great thing about the data is that you can get precise, high quality numbers 20, or even 50 years in advance. No matter how hard governments may try, you can?t change the number of people born 20 years ago.

Ignore them at your peril. Those who failed to anticipate the coming retirement of the baby boomer generation in 2006 all found themselves horribly long and wrong in the market crash that followed shortly.

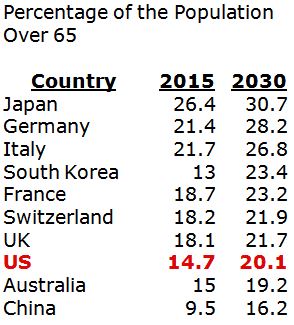

The Moody?s rating agency (MCO) has published a report predicting that the number of ?super aged? countries, those with more than 7% of their population over the age of 65, will increase from three to 13 by 2020, and 34 in 2030.

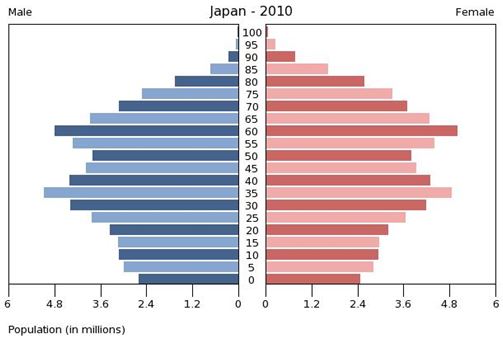

Currently, only Japan (26.4%) (EWJ), Italy (21.7%) (EWI), and Germany (EWG) are so burdened with that number of old age pensioners. France (EWQ) (18.7%), Switzerland (EWL) (18.2%), and the UK (EWU) (18.1%) are about to join the club.

The implication is that the global demographic dividend the world has enjoyed over the last 40 years is about to turn into a tax, a big one. The consequence will be lower long-term growth, possibly by 0.5%-1.0% less than we are seeing today.

This is what the bond market may already be telling us with its unimaginably subterranean rates for its long term bonds (Japan at -0.13%! Germany at 0.14%! The US at 1.75%!).

Traveling around Europe last summer, I was struck by the number of retirees I ran into. It certainly has taken the bloom off those topless beaches (I once saw one great grandmother with a walker on the beach in Barcelona).

For the list of new entrants to the super aged club, see the table below.

This is all a big deal for long-term investors.

Countries with inverted population pyramids have lots of seniors saving money, spending very little, and drawing hugely on social services.

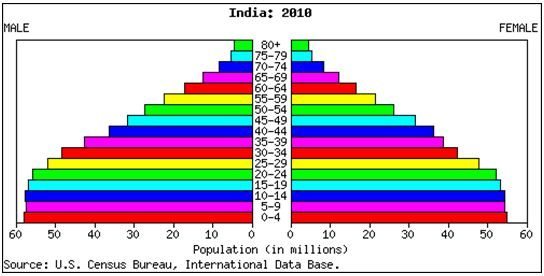

For example, in China, the number of working age adults per senior plunges from 6 in 2020, to 4.2 in 2030, to only 2.6 by 2050!

Financial assets do very poorly in such a hostile environment. Your money doesn?t want to be anywhere near a country where diaper sales to seniors exceed those to newborns.

You want to bet your money on countries with positive demographic pyramids. They have lots of young people who are eager to work and to spend on growing families, drawing on social services little, if at all.

Fewer seniors to support keeps tax and savings rates low. This is all great for business, and therefore, risk assets.

Be careful not to rely solely on demographics when making your investment decisions. If you did that, you would have sold all your American stocks in 2006, had two great years, but then missed the tripling in markets that followed.

According to my friend, noted demographer Harry S. Dent, Jr., the US will not see a demographic tailwind until 2022.

When building a secure retirement home for yourself, you need to use all the tools in your toolbox, and not rely just on one.

A demographic headwind does not permanently doom a country to investment perdition.

The US is a prime example, where a large number of women joining the labor force, high levels of immigration, later retirement ages, and lower social service payouts all help mitigate a demographic drag.

A hyper accelerating rate of technological innovation also provides a huge cushion.

You Want to Invest in This Pyramid?

...Not This One

https://www.madhedgefundtrader.com/wp-content/uploads/2015/06/Lady-Raspberries-e1434408537142.jpg291400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-05-11 01:06:022016-05-11 01:06:02The Cost of an Aging World

Malls are dying. Commerce is moving online at breakneck pace. Investing in retail is a death wish.

No less a figure than Bill Gates, Senior told me that in a decade malls would only be inhabited by climbing walls and paintball courses, and that was a decade ago.

Except it didn?t quite work out that way. Some malls are playing out Mr. Gates? dire forecast. But others are booming. It turns out that there are malls, and then there are malls.

There is one big kicker here that no one is noticing except me. If my prediction that this is not a low interest rate decade, but a low interest rate century turns out to be correct, then mall REIT?s with their high yields are the ?BUY? of the century.

Let me expand a bit on my thesis.

Technology is moving forward at an exponential rate. As a result, product performances are improving dramatically, while costs are falling. While commodity and energy prices are rising, they are but a tiny fraction of the cost of production.

In other words, DEFLATION IS HERE TO STAY!

The nearest hint of real inflation won?t arrive until the 2020?s when Millennials become big spenders, driving up the cost of everything.

We also have the most dovish Federal Reserve in history. Until my former economics professor Janet Yellen sees ?the whites of inflation?s eyes? she?ll limit interest rate hikes to a quarter point a year, if that. That?s until we go into the next recession, when US rates will go negative.

So with that issue decided, let's go back to the REIT thing. Real Estate Investment Trust?s are a creation of the Internal Revenue Code, which gives preferential tax treatment for investment in malls and other income generating properties.

There are 1,100 malls in the United States. Some 464 of these are rated as B+ or better and are concentrated in the biggest spending parts of the country (San Francisco, Beverly Hills, Greenwich, CT, etc).

Trading and investing for a half century, I have noticed that most mangers are backward looking, betting that existing trends will continue forever. As a result, their returns are mediocre at best and terrible at worst.

Truly brilliant managers make big bets on what is going to happen next. They are constantly on the lookout for trend reversals, new technologies, and epochal structural changes to our rapidly evolving modern economy.

I am one of those kinds of managers.

These are not your father?s malls. It turns out the best quality malls are booming, while second and third tier ones are dying the slow painful death that Mr. Gates outlined.

It is all a reflection of the ongoing American concentration of wealth at the top. If you are selling to the top 1% of wealth owners in the country, business is great. If fact, if you cater to the top 20%, things are pretty damn fine.

You can see this in the top income producing tenants in the ?class A? malls. In 2000, they comprised J.C. Penney, Sears, and Victoria?s Secret. Now Apple, L Brands, and Foot Locker are sought after renters. Put an Apple store in a mall, and it is golden.

And what about that online thing?

After 20 years of online commerce, the business has become so competitive that profit margins have been beaten to death. You can bleed yourself white watching Google Adwords empty out your bank account. I know, because I?ve tried it.

Many online only businesses are now losing money, desperately searching for that perfect algorithm that will bail them out, going head to head against the geniuses at Amazon.

I open my email account every morning and find hundreds of solicitations for everything from discount deals on 7 For All Mankind jeans, to the new hot day trading newsletter, to the latest male enhancement drug (although why they think I need the latter is beyond me).

Needless to say, it is tough to get noticed in such an environment.

It turns out that the most successful consumer products these days have a very attractive tactile and physical element to them. Look no further than Apple products, which are sleek, smooth, and have an almost sexual attraction to them.

I know Steve Jobs drove his team relentlessly to achieve exactly this effect. No surprise then that Apple is the most successful company in history, and can pay astronomical rents for the most prime of prime retail spaces.

It turns out that ?Clicks to Bricks? is becoming a dominant business strategy. A combination of the two is presently generating the highest returns on investment in retail today.

People start out by finding a product online, and then going to the local mall to try it on, touch it , and feel it.

Research shows that two thirds of Millennials prefer buying their clothes and shoes at malls. Once there, the probability of a serendipitous purchase is far great than online, anywhere from 20% to 60% of the time.

This explains why pure online businesses by the hundreds are rushing to get a foothold in the highest end malls.

Immediate contact with a physical customer give retailers a big advantage, gaining them the market intelligence they need to stay ahead of the pack. In ?fast fashion? retailers like H&M and Uniqlo, which turn over their inventories every two weeks, this is a really big deal.

There?s more to the story. Malls are not just shopping centers, they have become entertainment destinations. With an ever increasing share of the population chained to their computers all day, the demand for a full out-of-the-house shopping, dining, and entertainment family experience is rising.

Notice how Merry Go Rounds have started popping up at the best properties. Imax Theaters are spreading like wildfire. And yes, they have climbing walls too. I have not seen any paintball courses yet, but the guns and accessories are for sale.

This is why all of the highest rated malls in the country are effectively full. If you want space there you have to wait in line. REIT managers pray for tenant bankruptcies so they can jack up rents on the next incoming client, or pivot their strategy towards a new retail niche.

Malls are also in the sweet spot in the alternative energy game. Lots of floor space means plenty of roof space. That means they can cash in on the 30% federal investment tax credit for solar roof installations. Some malls in sunny states are net power generators, effectively turning them into mini local power utilities.

Fortunately for we investors, we are spoiled for choice in the number of securities we can consider. Many have a return on investment of 9-11%, a portion of which is passed on to the end investor.

There are now 25 REIT?s in the S&P 500. The sector has become so important that the ratings firm is about to create a separate REIT subsector within the index.

According to NAREIT.com (click here for the link at https://www.reit.com/nareit ), these are some of the largest mall related investment vehicles in the country:

Simon Growth Property (SPG) is the largest REIT in the country, with 241 million square feet in the US and Asia. It is a fully integrated real estate company which operates from five retail real estate platforms: regional malls, Premium Outlet Centers, The Mills, community/lifestyle centers and international properties. It pays a 3.17% dividend.

Macerich Co. (MAC) is a California based company that is the third largest REIT operator in the country. It has been growing though acquisitions for the past decade. It pays a 3.53% dividend.

Taubman Centers, Inc. (TCO) runs a national network of malls in some of the priciest zip code in the country. Properties include th

e Beverly Center in Los Angeles, Stamford Town Center in Stamford, CT, and the Fair Oaks mall in Fairfax, VA. It was established by the late Alfred Taubman of Sotheby?s fame. It pays a 3.41% dividend.

Mind you, REIT?s are not exactly risk free investments. To get the high returns you take on more risk. We remember how disastrously the sector did when the credit crunch hit during the 2009 financial crisis. Many went under, while others escaped by the skin of their teeth.

There are a few things that can go wrong with malls. Local economies can die, as exemplified by Detroit. Populations age, shifting them out of a big spending age group.

These are all highly leveraged companies, so any prolonged rise in interest rates could be damaging. But as I pointed out before, there is little chance of that in the near future.

The bottom line here is that we are seeing anything but the death of the mall. It just depends on the mall.

All in all, if you are looking for income and yield, which everyone on the planet is currently pursuing, then picking up some REIT?s could be one of your best calls of the year.

See You At the Mall

https://www.madhedgefundtrader.com/wp-content/uploads/2016/04/Mall-e1461879279977.jpg303400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2016-04-29 01:06:372016-04-29 01:06:37Death of the Mall

Circulating among Europe's top global strategists this spring, visiting their corner offices, camping out in their vacation villas, or cruising on their yachts, I am increasingly hearing about a new investment theme that will lead markets for the next 20 years: The Second American Industrial Revolution.

It goes something like this.

You remember the first Industrial Revolution, don't you? I remember it like it was yesterday.

It started in 1775 when a Scottish instrument maker named James Watt invented the modern steam engine.? Originally employed for pumping water out of a deep Shropshire coalmine, within 32 years it was powering Robert Fulton's first commercially successful steamship, the Clermont, up the Hudson River.

The first Industrial Revolution enabled a massive increase in standards of living, kept inflation near zero for a century, and allowed the planet's population to soar from 1 billion to 7 billion. We are still reaping its immeasurable benefits.

The Second Industrial Revolution is centering on my own neighborhood of San Francisco. It seems like almost every garage in the city is now devoted to a start up.

The cars have been flushed out onto the streets, making urban parking here a total nightmare. These are turbo charging the rate of technological advancement.

Successes go public rapidly and rake in billions of dollars for the founders overnight.? Thirty-year-old billionaires are becoming commonplace.

However, unlike with past winners, these newly minted titans of industry don?t lock their wealth up in mega mansions, private jets, or the Treasury bond market.

They buy a Tesla Model S-1 (TSLA), and then reinvest the rest of their windfall in a dozen other startups, seeking to repeat a winning formula.

Many do it.

Thus, the amount of capital available for new ideas is growing by leaps and bounds. As a result, the economy will benefit from the creation of more new technology in the next ten years than it has seen in the past 200.

Computing power is doubling every year. That means your iPhone will have a billion times more computing power in a decade. 3-D printing is jumping from the hobby world into large-scale manufacturing. In fact, Elon Musk's Space X is already making rocket engine parts on such machines.

Drones came out of nowhere, and are now popping up everywhere.

And don?t get me started on virtual reality. Ever wanted to date Cybil Shepherd or Nicole Kidman? How about both, at the same time? The possibilities boggle the mind.

It is not just new things that are being invented. Fantastic new ways to analyze and store data, known as ?big data? are being created.

Unheard of new means of social organization are appearing at breakneck speed, leading to a sharing economy. Much of the new economy is not about invention, but organization.

The Uber taxi service has created $65 billion in market capitalization in only five years, and is poised to replace UPS, FedEx, and the US Postal Service with ?same hour? intracity deliveries.?Now they are offering ?Uber Eats? in my neighborhood, which will deliver you anything you want to eat, hot, in ten minutes!?

Airbnb is arranging accommodation for 1 million guests a month, including 120,000 in Brazil for last year?s World Cup. They even had 189 German guests staying with Brazilians. I bet those were interesting living rooms on the final day! (Germany won).

As for me, I am planning my own all Airbnb trip to Europe next summer. It should be interesting.

And you are going to spend a lot of Saturday nights at home alone if you haven?t heard of Match.com, eHarmony.com, or Badoo.com.

Biotechnology (IBB), an also-ran for the past half-century, is sprinting to make up for lost time. The field has grown from a dozen scientists in my day 40 years ago, to several hundred thousand today.

The payoff will be the cure of every major disease, like cancer, Parkinson?s, heart disease, AIDS, and diabetes, within ten years. Some of the harder cases, such as arthritis, may take a little longer. Soon, we will be able to manipulate our own DNA at will.

The upshot will be the creation of a massive global market for these cures, generating immense profits. American firms will dominate this area, as well.

Energy is the third leg of the innovation powerhouse. Into this basket you can throw in solar, wind, batteries, biodiesel, and even ?new? nuclear.? The new Tesla home battery will be a game changer. Visionary, Elon Musk, is ramping up to to make tens of millions of these things.

The message to big oil is that Elon sold 400,000 of his new Tesla 3?s in just two weeks, and that is for a car that won?t be delivered for two more years.

Use of existing carbon based fuel sources, such as oil and natural gas, will become vastly more efficient. Fracking is unleashing unlimited new domestic supplies at costs that are falling at an incredible rate.

Welcome to ?Saudi America.?

The government has ordered Detroit to boost vehicle mileages to an average 55 miles per gallon by 2025. The big firms have all told me they plan to beat that deadline, not litigate it, a complete reversal of philosophy.

Coal will be burned in impoverished emerging markets only, before it disappears completely. Energy costs will drop to a fraction of today?s levels, further boosting corporate profits.

If you thought the Internet was big, free energy will have a far greater impact on the global economy.

Coal will die, not because of some environmental panacea, but because it is too expensive to rip out of the ground and transport around the world when all of the costs are factored in.

Seven years ago, I used to get two pitches for venture capital investments a quarter, if any. Now, I am getting two a day. I can understand only half of them (those that deal with energy and biotech, and some tech, where I have a background).

My friends at Google Venture Capital are getting inundated with 20 a day each! How they keep all of these stories straight is beyond me. I guess that?s why they work for Google (GOOGL).

The rate of change for technology, our economy, and for the financial markets will accelerate to more than exponential.

It took 32 years to make the leap from steam engine powered pumps to ships, and was a result of a chance transatlantic trip by Robert Fulton to England, where he stumbled across a huffing and puffing steam engine.

Such a generational change is likely to occur in 32 minutes in today?s hyper connected world, and much shorter if you work on antivirus software (or write the viruses themselves!).

The demographic outlook is about to dramatically improve, flipping from a headwind to a tailwind in 2022. That?s when the population starts producing more big spending Gen Xer?s and fewer oversaving and underproducing baby boomers. This alone should add at least 1-2% a year to GDP growth.

China is disappearing as a drag on the US economy. During the nineties and the naughts, they probably sucked 25 million jobs out of the US.

With an ?onshoring? trend now in full swing, the jobs ledger has swung into America?s favor. This is one reason that unemployment is steadily falling. Joblessness is becoming China?s problem, not ours.

The consequences for the financial markets will be nothing less than mind boggling. The short answer is higher for everything. Skyrocketing earnings take equity markets to the moon.? Multiples blast off through the top end of historic ranges. The US returns to a steady 4% a year GDP growth in the 2020's.

What am I bid for the Dow Average (INDU), (SPY), (QQQ) in 2030? Did I hear 300,000, a 17-fold pop from today?s level? Or more?

Don?t think I have been smoking the local agricultural products in arriving at these numbers. That is exactly the gain that I saw during 1982 to 2000, when the stock average also appreciated 17 fold, from 600 to 10,000.

Th

ey?re playing the same movie all over again. Except this time, it?s on triple fast forward.

There will also be commodities (DBA) and real estate booms. Even gold (GLD) gets bid up by emerging central banks bent on increasing their holdings to western levels.

I tell my kids to save their money, not to fritter it away day trading now, because anything they buy in 2020 will increase in value tenfold by 2030. They?ll all look like geniuses, like I did during the eighties.

After that, I will be 78, and it will be up to them to figure out what is going to happen next.

What are my strategists friends doing about this forecast? They are throwing money into US stocks with both bands, especially in technology (XLK), biotech (IBB), and energy (XLE).

That?s why the market bounced back so hard from the 10% correct in Q1.

This could go on for decades.

Just thought you?d like to know.

It?s Amazing What You Pick Up on These Things!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/John-Thomas7.jpg305378Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-28 01:06:092016-04-28 01:06:09The Second American Industrial Revolution

In my never-ending search for my readers for ?ten-baggers,? or investments that will rise in value tenfold over the foreseeable future, I keep circling back to the solar industry.

Tesla founder Elon Musk never does anything small.

Last year he announced the first ever, economical home battery electrical storage system, which he calls the Powerwall.

The device will enable your roof-mounted solar panels to supply power to your home 24 hours a day, not just when the sun is shining.

It is an innovation on the scale of Thomas Edison?s invention of the light bulb in 1879, or the launch of the Internet in 1969, in terms of the long-term impact on our economy.

Shifting the source of a third of our power supply is a big deal.

You may recall that the early investors in these earlier transitions made fortunes, General Electric (GE) in Edison?s case, and Netscape that spun out of the early Internet days.

Today, General Electric is the only company that has remained in the Dow Average for the past 100 years. So, investors take note.

During the day, the panels will charge up the battery mounted on your garage wall, which is about the size of a big screen TV. At night, you can then run your home off battery power.

Alternatively, you can engage in what is known in the industry as ?load shifting.? Charge your battery at night when you can buy electricity for as little as 4 cents a kilowatt hour, and sell it back to your local utility during a power demand surge the next afternoon for as much as 50 cents a kWh.

Buy low, sell high, it works for me!

And what is the cost of the miracle technology?

Only $3,000 for a 7 kWh battery or $3,500 for the 10 kWh version for energy hogs, like me, who has to charge a Tesla Model S-1 every day, soon to be two.

You can also include as immediate customers for this new product sports addicts, who watch multiple games on ESPN 24/7, paranoids who keep the lights on all night and indoor pot farmers, whose energy needs are said to be prodigious. Of course, the military will be another big consumer.

I ran some numbers on the possibilities for the Powerwall and they are mind-boggling.

The average home in the US has 2,500 square feet, which uses 7,000 kWh per year, or 19 kWh per day. The current cost for this power will be around $2,000 a year, depending where you live, more in California, and less in Texas, Oklahoma, and North Carolina.

A solar/ battery combination for such a home should cost about $14,000, including installation, the panels, the inverter, and all the gizmos. Net out the alternative energy investment tax credit of 30% (IRS Form 5695 http://www.irs.gov/pub/irs-pdf/f5695.pdf ), and your cost falls to only $10,500.

That means your power savings will cover the cost of your solar investment in a mere 5 years, compared to the present 7 or 8 years. After that, your home will have free electricity for another 20 years, as the life of these systems is usually 25 years.

Make the investment, and the value of your home rises, by $2 for every dollar spent, or so local real estate agents tell me.

You also will be guaranteed against any future power rate increases, an absolute certainty. America?s power grid is currently in a woeful state of disrepair, with much of the hardware 50 years old, or more.

The demands on the power industry are also about to take a quantum leap forward, as millions of consumers buy electric cars. Tesla plans to ramp up production of vehicles from 40,000 units last year to 500,000 by 2020, when the $35,000, 300 mile range Tesla 3 achieves mass production.

Some of my over-the-horizon-thinking hedge fund friends believe that figure could hit 15 million by 2030.

Add to that new, competing electric models produced by every other major carmaker, and that?s a lot of juice that will be needed. As a result, electric power utilities will probably have to endure more structural changes to their business model than any other industry.

Trillions of dollars are needed to modernize it, and all of that is going to come out of your pocket, but only if you remain an existing power customer.

Indeed, I have already been notified by my own utility, Pacific Gas and Electric Company (PGE), that I am due for two consecutive 7% price increases over the next two years.

The battery will also provide a backup power supply for home for when the grid crashes. Twice in the last two decades I have lost a freezer full of venison, pheasants, quail, trout, and salmon that I hunted and fished when storms knocked out power, for a week each time.

The Powerwall prices are so low that they beat the cost of a conventional backup diesel or gasoline generator.

They will also wipe out most of the existing back up battery industry, as Tesla?s advantages gained through massive economies of scale are enormous. Musk is talking about producing billions of batteries.

The Powerwall is a game changer for the solar industry, which has long been hobbled by the limitation that it could only supply power for 12 hours a day, and less in the winter, depending on your latitude.

It certainly gives a shot in the arm for the solar industry, which I have been banging the table about for years. My favorite is Solar City (SCTY). Other names to look at are First Solar (FSLR) and SunPower (SPWR), which manufactures my own solar panels.

It also casts Musk?s own Tesla (TSLA) in a new light. It is no longer just a car company, but a comprehensive energy solution. Musk has already made one of the largest capital investments in history to build a $5 billion ?Giga? factory near Reno, Nevada.

Much of that plant?s production has already been pre sold, and I understand that the decision has already been made to build a second one. Wow!

Musk explains that the world consumes 20 trillion kWh per year of electricity.

In the US, 1/3 of our fossil fuel consumption goes to transportation, and another 1/3 generates electric power, which is the equivalent to consuming 225 billion gallons of gasoline per year (or 8 billion barrels of oil per year, or 22 million barrels a day).

His goal is nothing less than to largely substitute those fossil fuel uses with solar energy, cutting our fossil fuel consumption by 2/3.

I guess there is no point in setting the bar low.

Meet the Next Light Bulb

https://www.madhedgefundtrader.com/wp-content/uploads/2015/05/Tesla-e1430771145520.jpg224400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-20 01:06:582016-04-20 01:06:58The Solar Missing Link is Here!

Of the 200 million Americans who possess financial assets, probably all of them own Apple (AAPL), either directly through a trading account, or indirectly though an ETF (it is a massive 11.67% of the PowerShares QQQ), public or private pension fund.

So to say that traders are on pins and needles ahead of the upcoming quarterly earnings report would be an understatement.

A year ago, Apple issued one of the most perfect reports in the history of capitalism.

It blew away even the most optimistic forecasts, announcing earnings per share of $2.33, versus a consensus expectation of $2.16, and $1.75 last quarter.

The firm earned $13.6 billion in profits on $58 billion in gross profits, the largest quarterly profit in world history.

The company sold a staggering 61.2 million iPhones during the three-month period, 4 million more than expected. Insignificant iPad sales dropped from 13.9 to 12.6 million units. MacBooks were in line at 4.6 million units.

No mention was made whatsoever of problems with a strong dollar.? The company now sits on an unbelievable $194 billion in cash, the equivalent of the GDP of a medium sized country.

Most importantly, Apple expanded its share buy back program to $200 billion. The big question now is, will Apple buy another company, or a whole country?

Wow!

Since then the stock has been grinding sideways in the most tedious manner imaginable. It was a classic ?Buy the rumor, sell the news? set up.

Which leads many shareholders to ask if, now that the stock is owned by every taxi driver, elevator operator , and shoe shine boy in the country (now I?m showing my age!), are we headed for another 45% selloff, much like the last time the stock peaked out in 2012?

Certainly, the grounds for concern are out there.

There are now no new blockbuster products coming out until we see the iPhone 7 in September 2016.

There are supply chain worries, as the global manufacturing network is now absolutely mammoth.

Some analysts are nervous about quality control, especially regarding new products like the Apple watch, which should sell an eye popping 30 million units this year.

However, I think this time it?s different.

While you weren?t looking, Apple has turned into a China play. No, they aren?t suddenly eating dim sum with chopsticks at corporate headquarters in Cupertino.

The Middle Kingdom, in short order, has become the firm?s largest grower of its earnings. This is a good thing. Last year saw an 80% growth of sales there. China is expected to become the largest market for Apple products this year.

What?s more, the ballistic growth there is expected to continue. Walk down the street in Shanghai these days, and you are amazed by how many people are speaking or texting into their iPhones, real and fake ones alike.

In fact, they have become the primary means through which people access the Internet there.

No doubt, this is due to Apple?s special relationship there with China Mobile (CHL), which now offers iPhone owners a great deal for their cell phone service. Did I mention that (CHL) has a staggering 750 million customers?

The iWatch is now viewed as the gateway for the sales of as many as 1.2 million future third party developed apps, the number iTunes offers now.

Apple Pay looks to replace Visa and Master Card at some point in the future. Apple TV is still lurking out there in the background.

We?ll learn more about all of this at the next developers conference in San Francisco in June.

All of this leads me to believe that there is far more fundamental support in terms of new products and business lines for the company than we saw during the last cycle.

There is also more distance in the rear view mirror since the passing of Steve Jobs. Successor Tim Cook has since proved himself as a world-class leader.

It turned out the timing for the company to transition from a founder-tyrant to a cutting edge administrator-manager was perfect. You don?t need to hold your breath anymore.

At least the stock market thinks so.

Therefore, I expect to see a $1 trillion market capitalization for Apple sometime in 2018, well up from today?s $602 billion. I think that means you need to use the current dip to load up on the stock.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/05/Apple-Logo.jpg305234Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-11 01:06:352016-04-11 01:06:35What To Do About Apple

It looks like the cyber security sector is about to take off like a rocket once again. There could be another 25%-50% in it this year.

The near destruction of Sony (SNE) by North Korean hackers last November has certainly put the fear of God into corporate America. Apparently, they have no sense of humor whatsoever north of the 38th parallel.

As a result, there is a generational upgrade in cyber security underway, with many potential targets boosting spending by multiples.

It's not often that I get a stock recommendation from an army general. However that's exactly what happened the other day when I was speaking to a three star about the long-term implications of the Iran peace deal.

He argued persuasively that the world will probably never again see large-scale armies fielded by major industrial nations. Wars of the future will be fought online, as they have been, silently and invisibly, over the past 15 years.

All of those trillions of dollars spent on big ticket, heavy metal weapons systems are pure pork designed by politicians to buy voters in marginal swing states.

The money would be far better spent where it is most needed, on the cyber warfare front. Needless to say, my friend shall remain anonymous.

The problem is that when wars become cheaper, you fight more of them, as is the case with online combat.

A little known fact is that during the Bush administration, the Chinese military downloaded the entire contents of the Pentagon's mainframe computers at least seven times.

This was a neat trick because these computers were in stand alone, siloed, electromagnetically shielded facilities not connected to the Internet in any way.

In the process, they obtained the designs of all of out most advanced weapons systems, including our best nukes. And what have they done with this top-secret information?

Absolutely nothing.

Like many in senior levels of the US military, the Chinese have concluded that these weapons are a useless waste of valuable resources. Far better value for money are more hackers, coders and servers, which the Chinese have pursued with a vengeance.

You have seen this in the substantial tightening up of the Chinese Internet through the deployment of the Great Firewall, which blocks local access to most foreign websites.

Try sending an email to someone in the middle Kingdom with a gmail address. It is almost impossible. This is why Google (GOOG) closed their offices there years ago.

My awareness of this comes from several Chinese readers complaining to me that they are unable to open my Trade Alerts or access their foreign online brokerage accounts.

As a member of the Joint Chiefs of Staff recently told me, "The greatest threat to national defense is wasting money on national defense."

If wars are now being fought online, then investing in national defense has actually come to mean investing in cyber security.

And although my brass-hatted friend didn't mention the company by name, the implication was that I need to go out and buy Palo Alto Networks (PANW) right now.

Palo Alto Networks, Inc. is an American network security company based in Santa Clara, California just across the water from my Bay Area office. The company's core products are advanced firewalls designed to provide network security, visibility and granular control of network activity based on application, user, and content identification.

Palo Alto Networks competes in the unified threat management and network security industry against Cisco (CSCO), FireEye (FEYE), Fortinet (FTNT), Check Point (CHKP), Juniper Networks (JNPR), and Cyberoam, among others.

The really interesting thing about this industry is that there are no real losers. That's because companies are taking a layered approach to cyber security, parceling out contracts to many of the leading firms at once, looking to hedge their bets.

To say that top management has no idea what these products really do would be a huge understatement. Therefore, they buy all of them.

This makes a basket approach to the industry more feasible than usual. You can do this through buying the $435 million capitalized PureFunds ISE Cyber Security ETF (HACK), which boasts Cyberark Software (CYBR), Infoblox (BLOX) and FireEye (FEYE) as its three largest positions. (HACK) has been a hedge fund favorite since the Sony attack.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/03/john-thomas-01.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-03-24 01:06:432020-04-06 15:28:31Cyber Security is Only Just Getting Started

There is no better sight to a hungry trader than blood in the water.

?Buy them when they?re cryin? is an excellent investment strategy that always seems to work.

There are rivers of tears being shed over the banking industry right now.

Federal Reserve officials openly told investors that after the December ?% rate hike that they would continue to do so on a quarterly basis. Only weeks later, a collapse in the stock market shattered this scenario to smithereens.

I doubt we?ll see any more Fed action in 2016.

This caught investors in bank shares wrong footed in a major way.

But wait! It gets worse!

Among the largest holders of American bank shares are the Persian Gulf sovereign wealth funds, including those for Saudi Arabia, Kuwait, Oman, Qatar, and the United Arab Emirates, my old stomping grounds. Pieces of me are still there.

The collapse in oil prices (USO) has put their budgets in tatters and they now have to sell stock to fund wildly generous social service programs. The farther Texas tea drops, the more shares they have to sell, and at $26 a barrel they have to sell bucket loads.

Had enough? There?s more.

The junk bond market (JNK) and oil company shares are suggesting that up to half of all American oil companies will go bankrupt sometime this year, mostly small ones. It all depends on how long oil stays under $40.

Unfortunately, the oil industry has been the most prolific borrower from banks for the last decade. The covenants on many of these loans require borrowers to pump and sell oil to meet interest payments NO MATTER THE PRICE! It?s a perfect formula for maxing out production and selling into a hole.

So fear of widespread energy defaults has also been dragging down bank shares as well.

Some of the moves so far in this short year have been absolutely eye popping. Bank of America (BAC) has plunged 31% from its recent high, while Citibank (C) is down 32% and JP Morgan is off 19%. Basically, they all had a terrible year just in the month of January.

Bank shares have been beaten so mercilessly that they are approaching levels last seen at the nadir of the 2009 financial crisis.

Except that this time, there is no financial crisis, not even the hint of one. For the past seven years, banks have been relentlessly raising capital, reducing leverage, and growing BIGGER.

They proved last time that they were too big to fail. Now they are REALLY too big to fail. Default rates aren?t even a fraction of what we saw during the bad old days. Energy industry borrowing is only a tenth the size of bank home loan portfolios going into the crisis.

Blame the Dodd-Frank financial regulation bill, which requires banks to hold far more capital In US Treasury bonds (TLT) than in the past, which by the way, are doing spectacularly well.

Blame ultra cautious management.

Whatever the reason, Big US banks are now solid as the Rock of Gibraltar.

Which means I?m starting to get interested. Interest rates don?t go down forever, nor does the price of oil. And scares about loan defaults are being wildly exaggerated by the media, as always.

But there is more than one way to skin a cat.

All of these companies issue high yield preferred stock with exceptionally high dividends. For example, Bank of America issued 6.2% yielding paper as recently as October. It is paying something like 8% now.

Since these securities are stock, you get to participate in price appreciation when the panic subsides. A guaranteed 8% return, plus the prospect of substantial capital appreciation? Sounds like a pretty good deal to me.

Google bank preferred shares and you will find an entire world out there of specialist advisors, dedicated newsletters and even day trading and hedging recommendations.

One thing to keep in mind here is that you should only buy ?non callable? paper. This prevents issuers from stealing your paper when better times return to cut their interest payouts.

There is another way to play this beleaguered sector.

You can buy the iShares S&P US Preferred Stock Index Fund ETF (PFF), which owns a basket of preferred stocks almost entirely made up of bank shares. As of today it was yielding 5.62%. To visit the fund?s website, please click link: https://www.ishares.com/us/products/239826/ishares-us-preferred-stock-etf.

Time to BUY?

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/ATM-Crash-e1454593247769.jpg299400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-04 01:08:092016-02-04 01:08:09Perfect Storm Hits the Banks

I was just about to don my backpack and head out for my evening hike when I caught a phone call from Tokyo.

The Bank of Japan had just announced they were implementing negative interest rates for the first time in history. The Japanese yen (FXE), (YCS) was in free fall and the stock market (DXJ) was soaring.

Note to self: don?t ever answer the phone just as I?m heading out the door. Good-bye hike, hello another inch on my waistline.

However, bank stocks were getting destroyed, as they would now have to pay money to the central bank to accept deposits, as they already do in Europe and Switzerland.

The overnight trading in S&P 500 (SPY) futures jumped from unchanged to up 100 points. It looked like January was going to go out with a bang. This could be the mother of all month end window dressings.

It really was a day for moves that made no sense. Bonds (TLT) rose with stocks on the hopes that any Fed interest rate hikes for this year will be cancelled. That?s like dogs and cats laying together.

Gold (GLD) rose modestly, even though the prospect of more quantitative easing anywhere in the world should have caused it to crater.

The US dollar was robust (UUP), just when you?d think that lower for longer interest rates should weaken it. I guess it?s a case of being the best house in a bad neighborhood.

Oil (USO), the main driver of all process for the past six months, was strangely unchanged for a change.

It was really one of those days when you wanted to hurl your empty beer cans at the TV, throw up your hands, and cry.

Personally, I don?t think US risk markets are out of the woods yet. We can?t escape the reality that earning multiples for American companies are falling.

You have to ask the question of what do negative interest rates really mean for the global economy? Hint: none of the answers are good.

Blame it on a Fed tightening cycle, which has just been shifted from second gear back to first. Blame it on a decade long GDP growth rate, which is stuck at 2%. That is caused by demographic headwinds that we can do nothing about.

Whatever the reason, stocks are not headed straight up from here. I think we are just squeezing out the shorts for the umpteenth time. They could all be cleaned out by the time the (SPY) hits $195.

Then it will be back to the low end of our new, violent range, probably just above $182.

Surprise!

https://www.madhedgefundtrader.com/wp-content/uploads/2016/01/Bank-of-Japan-e1454176764535.jpg227400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-01 01:07:452016-02-01 01:07:45Bank of Japan Bombshell Boosts Markets

Suddenly, the consolidation turned into a correction and maybe even a bear market.

A crucial part of trading a crash is knowing what to do at the bottom. Don?t worry. You?ll receive a flurry of text alerts from me right when that happens.

Many individual investors simply run to the bathroom and lock the door, hoping nobody knocks on the door for a couple of days.

Worse, they dump every stock they have. That?s what makes market bottoms.

Trades that once seemed impossible can now get done, provided you use limit orders.

Let me get this right. Stocks are crashing because:

1) The Federal Reserve isn?t going to raise interest rates anymore. 2) The price of oil has dropped 84% in five years. 3) Commodities have reached multi-decade lows. 4) The US dollar has suddenly stabilized. 5) Investors are yanking money from abroad and pouring it into the US on a flight to safety trade because it is the only place they can obtain a positive return, especially in stocks.

May I point out the screamingly obvious right here?

These are all reasons for 90% of US companies that borrow money and consume energy and commodities to increase earnings and to boost their share prices.

Only the 10% that derive revenues from ripping oil and commodities out of the ground should get hurt here.

Of course the market doesn?t know that. It is anything but rational when we hit big triple digit declines. There was only one direction on, and that was OUT.

And that is where you make your money

Margin clerks rule supreme, squeezing every bit of leverage out of their clients they can find.

The Dow and (SPY) are already posting large negative numbers for 2016.

Of course, I saw all of this coming a mile off.

I have been banging drums, pulling fire alarms, shooting off flare guns, and otherwise warning readers that the technical situation for the market was terrible ever since I went 100% into cash in December.

When the breakdown appeared imminent, I shot out Trade Alerts to sell short the S&P 500 (SPY) in size as fast as I could write them. And I started buying outright (SPY) puts for the first time in ages.

As a result of these sudden tactical moves, my model-trading portfolio has been keeping its head above water all month, up 2%. The Dow Average is off by a nausea inducing -10.7% at today?s low.

Yes, yes! All the hard work and research is paying off!

Ignore my musings at your peril!

What is even more stunning is that these declines are occurring in the face of US macro economic numbers that are going from strength to strength. The blockbuster December nonfarm payroll report of 292,000 is the real writing on the wall.

Housing, which accounts for about one third of the US economy, has been on fire. I?m sorry, but if you can?t find a parking space at Target, there is no recession.

Another crucial leg of the US economy, auto manufacturing, has been in overdrive. Auto sales are at a record 18 million annual rate, and some summer production shut downs have been cancelled.

That is, everywhere except Volkswagen.

With two of the most important legs firing on all cylinders, it?s clearly not about the economy, stupid!

There certainly hasn?t been a geopolitical event to justify moves of this magnitude.

As far as I can tell, Hitler has not invaded Poland, nor have the Japanese attacked Pearl Harbor.

Sure, there is whining about China, which has the Shanghai Index approaching the 2,900 level once again, down 40% from the top.?

Which leads me to believe that all of this is nothing more than a temporary hiccup. A BIG Hofbrauhouse kind of hiccup, but a hiccup nonetheless.

In a zero interest rate world, stocks only have to fall back from a price earnings multiple of 18 to 15 to flush out a ton of buying, and they will have done just that when the (SPY) hits $174.

THAT IS MY LINE IN THE SAND.

If nothing else, corporate buybacks should reaccelerate here, which could reach $1 trillion in 2016. Some 75% companies exit their quiet period by February 5 and can resume buying.

That could signal an interim market bottom.

The great thing about this selloff is that the best quality companies have fallen the most. This has been a function of the heavy sovereign wealth fund selling the bridge oil deficits.

After all, when share prices are in free fall, you have to sell what you can, not what you want to. It is only human to realize profits rather than incur losses, so quality has been trashed.

I am therefore going to give you a list of ten of my favorite stocks to buy at the bottom, highlighting the sectors that will lead us into a yearend rally.

The themes here are home builders, consumer discretionary, autos, solar, old technology, and international. I?m sorry, but the entire interest sensitive sector is on hold for the rest of the year, thanks to likely Fed inaction.

Watch out, because when I sense that the market has burned itself out on the downside, the Trade Alerts are going to be coming hot and heavy.

You have been forewarned!

Read ?em and weep with joy!

10 Stocks to Buy at the Bottom

Lennar Homes (LEN) Home Depot (HD) Microsoft (MSFT) General Electric (GE) Tesla (TSLA) Apple (AAPL) First Solar (FSLR) Palo Alto Networks (PANW) Wisdom Tree Japan Hedged Equity (DXJ) Wisdom Tree Europe Hedged Equity (HEDJ)

Finally, All the Hard Work is Paying Off

https://www.madhedgefundtrader.com/wp-content/uploads/2015/07/John-Thomas5-e1437678792272.jpg299400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-21 01:06:152016-01-21 01:06:15Ten Stocks to Buy at the Bottom

With great fanfare, congress passed a blockbuster $1.8 trillion spending bill in December. President Obama hastily signed the bill into law the next day.

Barley noticed was a measure included in the bill, which extends the 30% investment tax credit for alternative energy investments by five more years, until the end of 2021.

Barely, that is, unless you owned solar stocks.

Since the intention to include this pet democratic program started leaking out in November, shares of the entire industry doubled in value.

Solar City (SCTY) rocketed by 136%. First Solar (FSLR) soared by 81%. Even the normally quiescent Guggenheim Solar ETF (TAN) gained an impressive 28%.

Since then, these shares have given up a big chunk of their gains, thanks to the ongoing stock market correction. Better look hard at this group. They could become one of the top performers this year.

In exchange for the solar extension, the president agreed to permit oil exports for the first time in 40 years. The fact that the country has run out of storage and already has 50 filled takers sitting offshore in the Gulf of Mexico makes this an easy move.

House Minority leader, Nancy Pelosi, my local congressperson, told me the republicans were willing to ?Give away the store? to get the export measure through.

It seems that the Koch Brothers, the republican party?s largest donors and funders of global warming deniers, wanted to use the oil export measure as the means to offshore the entire US petrochemical industry.

It is headed for emerging nations, where labor is cheaper, taxes are lower, and regulation nil. That means the loss of tens of thousands of US jobs, many in California, over which Pelosi complained.

Pelosi complaining about the loss of petrochemical jobs? It?s proof that if you live long enough, you see everything.

Whatever jobs the Golden State loses here, it will make back with solar, big time. Industry analysts estimate that the five-year extension is worth a STAGGERING $125 BILLION IN ADDITIONAL SALES!

That is a multiple of the entire solar industry?s current total annual sales.

What?s more, this is five years during which the solar industry can dramatically improve panel output efficiencies, inverters, designs, and cut costs (remember that the cost of labor and regulation, about half the cost of a solar installation, is still rising).

Solar is already close to grid parity on costs now. It is even competitive in Texas. It will be substantially cheaper in five years.

During the same time, the cost of grid power will keep rising continuously, thanks to rising capital cost of replacing aging infrastructure.

I?m not saying you should rush out and buy solar today. But when the bull market resumes later this year, this group should be at the top of your list.

As for me, I am already getting estimates for a doubling of my existing solar roof system to accommodate the charging of my second Tesla, the Model X.

To learn all the ins and outs of buying and installing a solar roof system for you self, please read ?How to Buy a Solar System? by clicking here.

Better Bring Some More Panels

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/John-Thomas-Solar-Panal-e1444422199491.jpg296400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-19 01:08:582016-01-19 01:08:58The Game Changer for Solar

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

...Not This One

...Not This One