Global Market Comments

January 7, 2022

Fiat Lux

Featured Trades:

(JANUARY 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(IWM), (RUA), (TSLA), (NVDA), (USO), (TBT), (ROM), (SDS), (ZM), (AAPL), (FCX), (HOOD), (BRKB)

Global Market Comments

January 7, 2022

Fiat Lux

Featured Trades:

(JANUARY 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(IWM), (RUA), (TSLA), (NVDA), (USO), (TBT), (ROM), (SDS), (ZM), (AAPL), (FCX), (HOOD), (BRKB)

Below please find subscribers’ Q&A for the January 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: What’s a good ETF to track the Russell 3,000 (RUA)?

A: I use the Russell 2,000 (IWM) which is really only about the Russell 1500 because 500 companies have been merged or gone bankrupt and they haven't adjusted the index yet. This is the year where value plays and small caps should do better, maybe even outperforming the S&P500. These are companies that do best in a strong economy.

Q: Should I focus on value dividends growth, or stick with the barbell?

A: I think you have to stick with the barbell if you’re a long-term investor. If you’re a short-term trader, try and catch the swings. Sell tech now, buy it back 10% lower. Keep financials; when they peak out you, dump them and go back into tech. It’ll be a trading year, but if a lot of you are just indexing the S&P500 or doubling up through a 2x ETF like the ProShares ultra S&P 500 (SSO), it may be the easiest way to go for this year.

Q: Will higher rates sabotage tech, particularly smaller companies?

A: They’ve already done so with PayPal (PYPL) down 44% in six months—I’d say that’s sabotaged. Same with Square (SQ) and a lot of the other smaller tech companies. So that has happened and will continue to happen a bit more, but we’re really getting into the extreme oversold levels on a lot of these companies.

Q: Should we cash out on the iShares 20 Plus Year Treasury Bond ETF (TLT) summer 150/155 put spread LEAPS?

A: No, because you haven't even realized half of the profit in that yet since there is so much time value left in those options. As long as you stay below $150 in the (TLT), which I'm pretty sure we will, you will get your full 100% profit on that position. On the six month and one year positions, they don’t really move very much because they have so much time value in them. Once you get into the accelerated time decay, which is during the last 3 months before expiration, they catch like a house on fire. So, if you're willing to keep a safe long-term position, this thing will write you a check every day for the next six months or a year to expiration. I know we have absolutely everybody in these deep in the money TLT puts; some people even did $165-$170’s—you know, my widows and orphans crowd—and they are doing well, but not as much as if you’d had a front month.

Q: What scares you most for the next 12 months?

A: Another variant that is more fatal than either Delta or Omicron. Unlikely, but not impossible.

Q: Do you expect Freeport McMoRan (FCX) to break out to the upside?

A: I do, I did the numbers over the vacation for copper production to meet current forecast demands for electric vehicle production. Global copper has to increase 11 times, and that can’t be done, so prices are going to have to go up a lot. One of my concerns with these lofty EV projections (that even I make) is that there aren’t enough commodities in the world to make all these cars with the current infrastructure. And you’re not going to find a replacement for copper—it's just too perfect of an electrical conductor. So, that means higher prices to me—you increase demand 11 times on a stable supply, and it takes 10 years to bring a new copper mine online.

Q: Do you have any open trades?

A: No, and one reason is that I figured they would probably crash the market on the last trading day of the year, which they did. If I had positions, they would have crushed them on the last year and my performance. And all hedge fund traders do this; they try to go 100% cash at the end of the year to avoid these things. And whatever you lost on Friday you made back on Monday morning at the expense of last year's performance. But you have to wait 15 months to get paid on today's performance, and, that is the reason I do that. So, looking for higher highs to sell, lower lows to buy.

Q: Should I be buying NVIDIA (NVDA) and Tesla (TSLA) on the dip?

A: Absolutely yes, but Tesla's prone to 45% corrections—we had one last year and the year before—and Nvidia tends to have 25% corrections. So yes, NVIDIA could well be the stock of the decade, but you don’t want to buy it right now. It’s starting to lose steam already.

Q: Will ProShares Ultra Technology (ROM) be under pressure?

A: Keep your position small now, take some profits, look to buy on a bigger dip. If the big techs drop 10%, (ROM) will drop 20% and get you below $100.

Q: Do you offer trade alerts on small caps for short term traders?

A: No, because you can’t execute those trades. A lot of them are just so illiquid, you can’t even trade one share unless you want to pay a huge spread. Keep in mind, when I worked at Morgan Stanley (MS), I covered the Rockefeller Foundation, the Ford Foundation, George Soros, Paul Tudor Jones, the government of Abu Dhabi, California State Pension Fund, and a lot of other huge funds; and the last thing they’re interested in is short term trades for the small-cap stocks. So, I don't really know much about those, but they tend to change the names every year anyway. And it really is a beginner trader type area because the volatility is so enormous. You can get 10x moves one day going to zero the next. It is also an area full of scams, cons, and pump and dump schemes.

Q: What is your advice when it comes to the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Short term, take the profits—you just got a $14 point rally in your favor. Short term traders, take profits on bonds here, cover your shorts. Long term investors keep it, the cost of carry is only about 4% right now, not that high, so I would keep it for a great year-end move for 2.5% yields on the ten-year.

Q: I hate oil (USO) because it’s going to zero. Should I keep trading in it?

A: Very few are nimble enough to trade oil, it’s really an insider’s game. No new capital is moving into the oil industry and oil companies themselves won’t invest in their own businesses anymore.

Q: Would you put on a new position on the iShares 20 Plus Year Treasury Bond ETF (TLT) today?

A: No, you don’t sell short things after they move down $14 points. You put them on before that. If I were to do a short-term trade in (TLT) I would be a buyer, I’d maybe buy it for a countertrend rally of maybe $4 or $5 points.

Q: What should I do with my FCX 2023 LEAP?

A: There is enough time on it, so I would keep running it along as is—don’t get greedy. Keep the LEAPS you have and you should do well by it.

Q: Could the iShares 20 Plus Year Treasury Bond ETF (TLT) bottom out in the near term?

A: Yes, it could, on a short-term basis. $141 is the nine-month low for the (TLT), so a great place to take short term profits. (TLT) is right now at $142.56, so we’re approaching that $141 handle closely. Every technical trader on the market’s going to cover their shorts on the $141 or $142 handle, so just congratulate yourself going into this move short, and take the money and run. You take every $14 point move in your favor in the (TLT); and let it rally 5 points and then reestablish, that’s how you trade.

Q: Do you think there will be a delay in the first interest rate hike due to COVID?

A: Yes, Jay Powell is the ultra-dove—any excuse to delay rate hikes, he’ll do it. And the way you’ll know is he’ll delay the end of other things which you don’t see, like daily mortgage bond purchases, daily US Treasury purchases, and other backdoor forms of QE. We’ll know well in advance if he’s going to raise or not by March or even June. We watch this stuff every day, we talk to people at the Fed every week. And remember, the Treasury Secretary Janet Yellen is a good friend of mine, I get a good handle on these things; this is why 99% of my bond trades make money.

Q: What if I have the $135-$140 put spread in January?

A: Sell it now, take what you can, take the hit; because that’ll expire at zero unless we break down to new lows on the (TLT) in the next ten days or so. That's not a good bet, especially on top of a $14 point drop. Capture what you can on that one and keep the cash for a better entry point. That’s exactly what I did—I sold all my January positions yesterday no matter what they were, because when you get to two weeks to expiration the moves become random.

Q: Do you think inflation will last longer than expected?

A: No, I think it will last shorter than expected because I think at least half of the inflation rate, if not more, are caused by supply chain problems which will end within the next six months, and therefore lead to the over-order problem that I was talking about earlier.

Q: What’s your outlook on energy this year?

A: It could go higher. On the way to zero, you’re going to have several double, tripling’s, even 10x increases in the price of oil, like we saw in the last 18 months. We went from negative numbers to 80, and what happens is oil becomes more volatile as the supply becomes more variable, that's a natural function. But trading this is not for non-professionals.

Q: Since sector rotation is happening, do you think we should sell all tech positions?

A: Short term yes, long term no. Tech will still lead with earnings, and even if they have a bad five months coming, they have a terrific long-term view. For the last 30 years, every sale of tech has been a mistake, especially in Apple (AAPL). So if you’re a trader, yes, you should have been selling since November. If you’re a long-term investor, keep them all.

Q: Is the ProShares UltraShort S&P 500 (SDS) a good position to buy up when the market timing index goes into sell territory?

A: Yes it is, and that will probably work better this year than it did last year because narrow range volatile markets are much more technically oriented than straight-up markets or long term bull markets. Pay close attention to those markets, you could make a lot of money trading them.

Q: Do Teslas have good car heaters for climates up North in -25 or -30?

A: You plug them in. When it gets below zero you actually get a warning message on your Tesla app telling you to plug it in, and then the car heats itself off of the power input. Otherwise, if you get to below zero, the range on the car drops by half. If you have a 300-mile range car like I do and then you freeze it, it drops to like 150 miles. In Tahoe, I keep my car plugged in all the time when I'm not using it, just to keep it warm and friendly.

Q: Is Zoom (ZM) a good buy here?

A: No, I think they’re going to keep punishing these overpriced small cap techs like they have been. We’re a long way from value on small tech. That was a 2020 story.

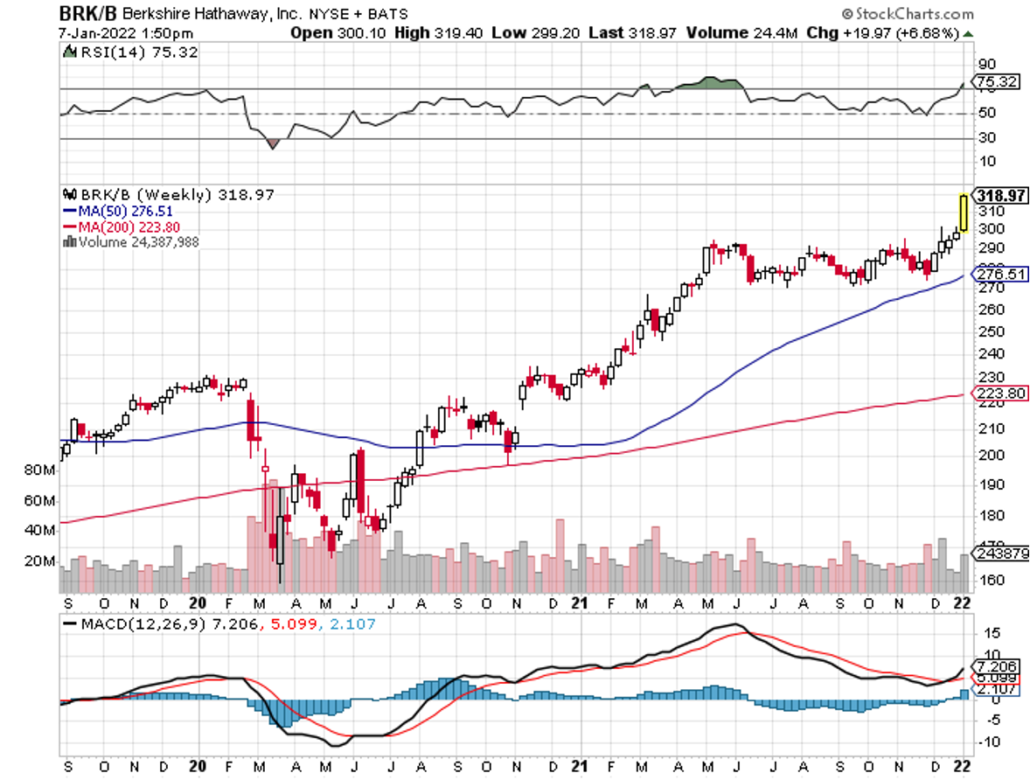

Q: What about Berkshire Hathaway (BRKB)?

A: Berkshire Hathaway is doing a major breakout because they own financials up the wazoo and they’re all breaking out. And YOU should be long up the wazoo on these things because I’ve been recommending them for the last 4 months.

Q: What do you think of Robinhood (HOOD)?

A: Robinhood I like long term, but it is high risk, high volatility. It is down 78% from the IPO so it is busted. Kind of tempting down here, but again, all the non-earning overvalued stocks are getting their clocks cleaned right here; I'm not in a rush to get involved.

Q: When you enter a LEAP, is the straight call or call spread?

A: It’s a call spread. You finance the high cost of one-year options by selling short a call option against it further out of the money. And that way you can get enormous leverage for practically nothing, 10 or 20 times in some cases, depending on how you structure the strikes.

Q: Best stock to play Copper?

A: Freeport McMoRan (FCX). I’ve been recommending it since it was $4.00.

Q: Oil is the pain train until EVs actually take over.

A: That’s true, and they haven’t. EVs have about a 6% market share now of new car sales worldwide, but that could rapidly accelerate given all the subsidies that EVs are getting. Also, we have many future recessions to worry about, during which oil could easily drop 290% like it did last year. If you can hack that kind of volatility, go for it, but I find better things to do quite honestly. And I think my next oil trade will be a short, especially if we go over $100.

Q: What about Bitcoin?

A: It could go sideways in a range for a while. If we can’t hold the 200-day, we’re going back down to the high 30,000s, where we were at the start of the year—we could give up the entire year of 2021. Bitcoin also suffers from rising interest rates since they don’t yield anything.

Q: Is this recorded?

A: Yes, the webinar recording goes out in about 2 hours. Log into the madhedgefundtrader.com website and go to my account, where you’ll find it with all the different products you’ve purchased.

Q: I just closed out my (TLT) 150 put option for the biggest single trade profit in my life; I just made 20% of my annual salary alone today. Thank you, John!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 3, 2022

Fiat Lux

Featured Trade:

(NEW VIDEO UPDATE ON EXECUTING A VERTICAL BULL CALL DEBIT SPREAD),

(AAPL)

Automation is taking place at warp speed displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the direct capital of $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. bank jobs getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificially engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

Front-office staff has already felt the brunt of downsizing with purges carried out from 2018 representing an eighth year of continuous decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30% and the accumulation of hordes of data will advance the marketing effort into a smart, multi-pronged, hybrid cloud-based and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies like PayPal and Square are chomping at the bit and even tech companies like Amazon and Apple have started tinkering with new financial products.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 63,036 employees in 2019, more than 10x higher the number of U.S. financial job losses and that has continued in 2020 and 2021.

In a sign of the times, the European outlook has turned demonstrably negative with Deutsche Bank announcing layoffs of 40,000 employees through 2023 as it scales down its investment banking business.

Germany banks are also passing on the burden of negative interest rates to their clients.

A recent survey by Deutsche Bundesbank shows that 58% of banks are charging all savers negative interest rates while others only target wealthy and corporate clients.

If the U.S. dips into negatives rates in the future, expect the same nasty effect on job force cuts that Europe has experienced.

Either way, don’t tell your kid to get into banking, because they will most likely be feeding on scraps at that point.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

Global Market Comments

December 24, 2021

Fiat Lux

Featured Trade:

(TRADING THE NEW APPLE IN 2022),

(AAPL),

(TESTIMONIAL)

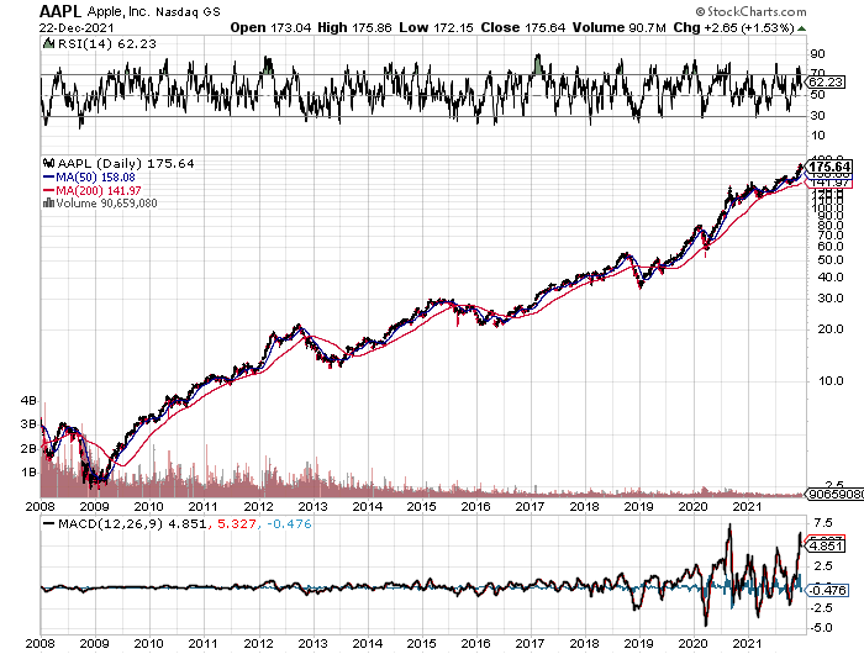

Not a day goes by when someone doesn’t ask me about what to do about Apple (AAPL).

After all, it is the world's largest publicly-traded company at a $2.1 trillion market capitalization. It is the planet’s most widely owned stock. Almost everyone uses their products in some form or another.

It buys back more of its own stock than any other company on the planet. Oh yes, it is also one of Warren Buffet’s favorite picks and one of his biggest holdings.

So, the widespread adulation is totally understandable.

Apple is a company with which I have a very long relationship. During the early 1980s, I was ordered by Morgan Stanley to take Steve Jobs around to the big New York Institutional Investors to pitch a secondary share offering for the sole reason that I was one of three people who worked for the firm who was then from California.

They thought one West Coast hippy would easily get along with another. Boy, were they wrong, me in my three-piece navy blue pinstripe suit and Steve in his battered Levi’s. It was the worst day of my life.

Steve was not a guy who palled around with anyone. He especially hated investment bankers, like me.

I last got into Apple with my personal account when the company only had four weeks of cash flow remaining and was on the verge of bankruptcy. I got in at $7, which on a split-adjusted basis today is 25 cents. I still have them. In fact, my cost basis in Apple is less than the 88 cents annual dividend now.

Today, some 200 Apple employees subscribe to the Diary of a Mad Hedge Fund Trader looking to diversify their substantial holdings. Many own Apple stock with an adjusted cost basis of under $5. Suffice it to say, they all drive really nice Priuses.

So I get a lot of information about the firm far above and beyond the normal effluent of the media and stock analysts. That’s why Apple has become a favorite target of my Trade Alerts over the years.

And here is the great irony: Nobody would touch the stock with a ten-foot pole at the end of 2018. Since then, Apple has rallied 274%, creating more market cap in a year than any company in history.

Here’s why. Apple was all about the iPhone which then accounted for 75% of its total earnings. The TV, the watch, the car, iPods, the iMac, and Apple Pay were all a waste of time and consumed far more coverage than they are collectively worth.

The good news is that iPhone sales are subject to a fairly predictable cycle. Apple launches a major new iPhone every other fall. The share price peaks shortly after that. The odd years see minor upgrades, not generational changes.

Just like you see a big pullback in the tide before a tsunami hits, iPhone sales are flattening out between major upgrades. This is because consumers start delaying purchases in expectation of the introduction of the new iPhone, more power, gadgets, and gizmos.

So during those in-between years, the stock performance was disappointing. 2018 certainly followed this script with Apple down a horrific 30.13% at the lows. Maybe it’s a coincidence, but the previous generation in Apple shares in 2015 brought a decline of, you guessed it, exactly 29.33%.

But Apple is a much bigger company this time around, and well-established cycles tend to bring in diminishing returns. It’s like watching the declining peaks of a bouncing rubber ball.

This is not your father’s Apple anymore. Services like iTunes and the new Apple+ streaming service are accounting for an even larger share of the company’s profits. And guess what? Services companies command much higher multiples than boring old hardware ones. It’s the old questions of linear versus exponential growth.

Here’s the next new play. Autonomous driving looks to be a huge business for Apple, possibly a $1 trillion a year business. After all, Tesla is already charging $8,000 for the upgrade and it only works on freeways. My bet is that they sell autonomous consoles to legacy Ford (F) and General Motors (GM).

An easing of trade relations with China under a new Biden administration will bring a new spring to Apple’s step, where sales have recently been in free fall. Their new membership lease program promises to deliver a faster upgrade cycle that will allow higher premium prices for their products. That will bring larger profits.

A decade ago, I ran into a local school teacher who, after 30 years of slaving away with your brats, was unable to retire because, with only $100,000 saved, she was too poor to do so. All her money went to expensive California rent and to Blue Cross since her district had no health insurance plan.

I told her to place her entire life savings into Apple. Her financial advisor told her she was nuts. Her friends told her she was crazy. Her mother said she should disown me.

Where is that school teacher today? She just bought a $3 million beachfront home on Hawaii’s Kona Coast. She sold her Apple shares for $7.3 million. I know because I just received a nice Christmas card from her attached to a two-pound box of See’s candy, my favorite.

Who said teaching didn’t pay!

It all adds up to keeping Apple as a core to any long-term portfolio.

Just thought you’d like to know.

I Heard They are Diversifying

Mad Hedge Technology Letter

December 17, 2021

Fiat Lux

Featured Trade:

(LOOKING FORWARD TO TECH IN 2022)

(FB), (NVDA), (AAPL), (MSFT), (AR), (VR)

Another pandemic year is on the verge of being in the books and we need to look yonder to 2022 and what it can offer.

Now that billions are being poured into the project, it’s not weird to say that advanced technology and the arteries and ventricles surrounding it, will all lead to developing this new world called the Metaverse.

The metaverse is a hypothesized iteration of the Internet, supporting persistent online 3-D virtual environments through conventional personal computing, as well as virtual and augmented reality headsets.

And I am not saying this is a new thing just to be cool, analyzing thousands of earnings reports, it’s clear that companies are deploying human capital around gaining a slice of this future Metaverse.

This idea is so prominent that Facebook (FB) changed its name to Meta to signal its commitment to this new technology.

Next year will be the year that we get closer to the real deal — a fully functioning Metaverse even if it might just be a beta version.

And it’s not just Facebook, Apple (AAPL), and Microsoft (MSFT) and the rest are in it too with Nvidia’s (NVDA) chips serving as a building block of the Metaverse.

Naturally, related technologies will be of great importance, and I can easily see a greater surge in augmented reality (AR) interest.

People should also keep a close eye on the introduction of Meta's internet-of-VR.

The idea of the metaverse and an advanced VR world must be seen through the prism of the pandemic which has forced us to become digital first even if many of us aren’t native digital users.

Many of us have had to learn on the go, for instance, download that Zoom video conferencing software or upgrade our home office.

This torrent of internet usage has its pitfalls like explosive growth in cyberattacks, making cybersecurity more important than ever.

Cybersecurity will no longer be seen as an “added extra” by organizations and will be built into the DNA of any and every IT system, from supply chains to infrastructure and devices.

Our reliance on internet leads nicely into 2022 becoming the year when 5G became mainstream.

We are edging towards that point where we need that extra speed to harness our work devices and to wield them in the most efficient and optimal way.

Many of you have had to upgrade data packages, build robust infrastructure into your home office and I don’t mean just buying a better office chair.

This could see the rise of “digital cities” along with new smart mobility services such as autonomous vehicles and 5G connected bicycles. We could also see a rise in private 5G networks for businesses in manufacturing and logistic sectors.

A new era of private connection for businesses will be launched, enabling greater data-driven insights and real-time business decisions.

2022 will see businesses continue to neglect the traditional office and many companies will be at best — hybrid.

We might start seeing companies go bankrupt because they can’t convince any workers to show up in physical form.

It’s already happening to the workers I talk to where limited remote working opportunities when interviewing for new jobs is a deal-breaker.

Next year is also when we finally see artificial intelligence on steroids.

The explosion of AI-powered gadgets, apps, websites, and tools is here for 2022.

It'll become harder to differentiate chatbots from human customer support agents. Other products such as future content recommendations on social media and streaming websites are likely to come from an AI rather than traditional data analysis.

The Internet of Things, AI, and automation will aid businesses to fill gaps created by the labor shortage while optimizing staff. In retail and hospitality, this will take the form of self-serve kiosks, autonomous order fulfillment, and AI-enabled drive-thrus, all freeing people up for higher-skilled roles.

Ultimately, an explosion of data requirements will offer complex challenges to firms that must manage large amounts of data.

This goes triple for many companies still struggling to fully digitize.

Although it’s hard to visualize, our reliance on technology will keep growing and the winners will be the ones who can harness these new technologies to supercharge their financial profiles.

It’s not that I am boring, but the companies leading the new stage of digital technologies are the biggest and richest of Silicon Valley, and I would rather ride the bandwagon with them than try the sexy contrarian play, especially with higher interest rates hurting start-up culture.

Global Market Comments

December 17, 2021

Fiat Lux

Featured Trade:

(DECEMBER 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(FCX), (FCI), (TLT), (TBT), (BITO), (AAPL), (AMZN), (T), (TSLA), (BABA), (BLOK), (MSTR), (COIN)

Below please find subscribers’ Q&A for the December 15 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: With interest rates going up, would it make sense to short heavily indebted companies as a class?

A: Yes it does; those would be old-line industrials and auto companies with very heavy debts. Technology companies essentially have no debt unless they’re startups. So yeah, that’s a good idea; unless of course inflation is peaking right now, which it may be if you solve these supply chain problems, and it becomes evident that retailers overordered to beat the supply chain problems and now have a ton of excess inventory they can’t meet—then the inflation plays will crash. So, not a low-risk environment right now. No matter where you look, you’re screwed if you do, you’re screwed if you don't. So that is an issue to keep in mind.

Q: What do you think of Freeport McMoRan (FCX) short-term?

A: Short term, (FCX) only sees the Chinese (FXI) real estate crisis, which is getting worse before it gets better and could bring a complete halt to all known construction in China. The government is forcing the real estate companies there to run at losses in order to bring the bottom part of their society into the middle class with houses in third and fourth-tier cities. Long term, as annual electric car production goes from a million cars a year to 25 million cars a year and each car needs 200 lbs. of copper, we have to triple world production practically overnight to accommodate that. That can’t happen, therefore that means much higher prices. If you’re willing to take some pain, picking up freeport McMoRan in the low $30s has to be the trade of the century.

Q: Do you see a Christmas rally or a bigger correction?

A: Rally first. Once we get the Fed out of the way today, we could get our Christmas rally resumed and go to new highs by the end of the year. But, January is starting to look a little bit scary with all the unknowns going forward and massive long positions. January could be okay as hedge funds put positions back on in tech that they’re dumping right now. If they don’t show up…Houston, we might have a problem.

Q: Thoughts on the iShares 20 Plus Year Treasury Bond ETF (TLT) Dec 2022 $150-$155 vertical bear put spread?

A: Since I'm in low-risk mode, I would go up $5 or $10 points and not be greedy. Not being greedy is going to be one of the principal themes of 2022 therefore I’m recommending that people do the $160-$165 or even the $165-$170, which still gives you a 30% return in a year, and I think next year this will be seen as a fabulous return.

Q: What about the $100,000 target for Bitcoin (BITO) by the end of the year?

A: That’s off the table thanks to the Fed tightening and Omicron triggering a massive “RISK OFF” and flight to safety move. Non-yielding instruments tend not to do well during periods of rising interest rates, so gold along with crypto is getting crushed.

Q: What will happen in the case of a black swan event in early 2022, like Russia invading Ukraine?

A: Market impact for that would be a bad couple of days, a buying opportunity, and then you’d want to pile into stocks. Every geopolitical event that’s happened in the last 20 years has been a buying opportunity for stocks. Of course, I would feel bad for the Ukrainians, but it’s kind of like Florida seceding from the US, then the US invading Florida to take it back, and the rest of the world not really caring. Plus, it doesn’t help that their heavily nationalist post-coup government has some fascist tendencies. However, we could get global economic sanctions against Russia like an import/export embargo, which would hurt them and destroy their economy.

Q: Will the European natural gas shortage continue?

A: Yes because the Europeans are at the mercy of the Russians, who have all the gas and none of the economy. Therefore, they can export as much or as little as they want, depending on how much political control they’re trying to exert in Europe.

Q: Apple Inc. (AAPL) price target?

A: Well, my price target for next year was $200; we could hit that by the end of the year if we get a rally after the Fed meeting.

Q: 33% of the population is in collection status with personal debt, credit cards, etc—is that a harbinger of a 2008 crash?

A: No, it is a harbinger of excess liquidity, interest rates being too low, and lenders being too lax. However, we aren’t at the level where it could wipe out the entire economy like with defaulting on a third of all housing market debt in 2008.

Q: What should I do with my call spreads for Amazon.com, Inc. (AMZN)?

A: Well, November would have been a great sell. Down here, I’d be inclined to hold onto the spreads you have, looking for a yearend rally and a new year rally. But remember, with all these short-dated plays risk is rising, so keep that in mind.

Q: What do you think of AT&T Inc (T)?

A: The whole sector has just been treated horrifically; I don’t want to try to catch a falling knife here even though AT&T pays a 10% dividend.

Q: What about quad witching day?

A: Expect a battle by big hedge funds trying to push single stocks options just above or below strike prices. It’s totally unpredictable because of the rise of front-month trading, which is now 80% of all options trading with the participation of algorithms.

Q: Is the Alibaba Group Holding Limited (BABA) $230-$250 LEAP in June 2023 worth keeping?

A: I would say yes, I think the Chinese will come to their senses by then, and all the Chinese tech plays will double, but there’s no guarantee. That is still a high-risk trade.

Q: Does the US have an opportunity to export petroleum products?

A: The answer is yes, we are already a net energy exporter thanks to fracking. But, it is a multi-year infrastructure build-out to add foreign export destinations like Europe, which hasn’t bought our petroleum since WWII. Right now, almost all of our exports are going to Asia. No easy fixes here.

Q: Is Tesla Inc (TSLA) a buy at 935 down 300 in change?

A: Not yet; 45% seems to be the magic number for Tesla correction. We had one this year. And Elon Musk hasn’t quit selling yet, although I suspect he’ll end his selling by the end of the year because he’ll have met all his tax obligations for the year. He has to sell these options before they expire and are rendered useless. So that is what’s happening with Tesla, Elon Musk selling. And can you blame him? He almost worked himself to death making that company, time to spend some money and have a good time, like me.

Q: What if your Chinese company gets delisted?

A: Try to get out before it is delisted. Otherwise, the domicile moves to Hong Kong and you’ll have to sell equivalent shares there. I don’t know what the details of that are going to be, but the Chinese companies are trying to force companies to delist from the US and list in Hong Kong so they have complete control over what's going on. Also, I never liked these New York listings anyway because the disclosures were terrible, with Cayman Island PO Boxes and so on…

Q: Is the ProShares UltraShort 20+ Year Treasury (TBT) a good long-term position to hold?

A: It is to an extent—only if you expect any big moves up in interest rates, which I kind of am. This is because the cost of carry for (TBT) is quite high; you have to pay double the 10-year US Treasury rates, which is double 1.45% or about 2.90%, and then another management fee of 1%, so you have kind of a 4% a year headwind on that because of cost. Remember, if you’re short a bond, you’re short a coupon; if you’re double short a bond you’re short twice the coupon and you have to pay that and they take it out of the share price. But, if you’re expecting bonds to go down more than 4%, you’ll cover that and then some and I think bonds could drop 10-20% this year.

Q: What’s the difference between GBTC and BITO?

A: Nothing, both are Bitcoin plays that are tracking reasonably well. I prefer to go with the miners—the Bitcoin providers, that’s a selling-shovels-to-the-gold-miners play. They tend to have more volatility than the underlying Bitcoin, so that’s why I’m in (BLOK) and (MSTR) when I’m in it.

Q: What’s the best way to buy Crypto?

A: If you really want to buy Crypto directly, the really easy way is to go through one of the top crypto brokerage houses, and we’ve recommended several of those. Coinbase (COIN) is the one I’m in. It literally takes you five minutes to set up an account and you can instantly buy Bitcoin linked to your bank account.

Q: What are the fees like for Coinbase?

A: The fees at (COIN) are exorbitant only if you’re buying $10 worth of Bitcoin. If you’re buying like $1 million worth, they’re much, much smaller. But I recommend you start at $10 and work your way up as I did, and sooner or later you’ll be buying million-dollar chunks of Bitcoin which then double in three months, which happened to me this year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader