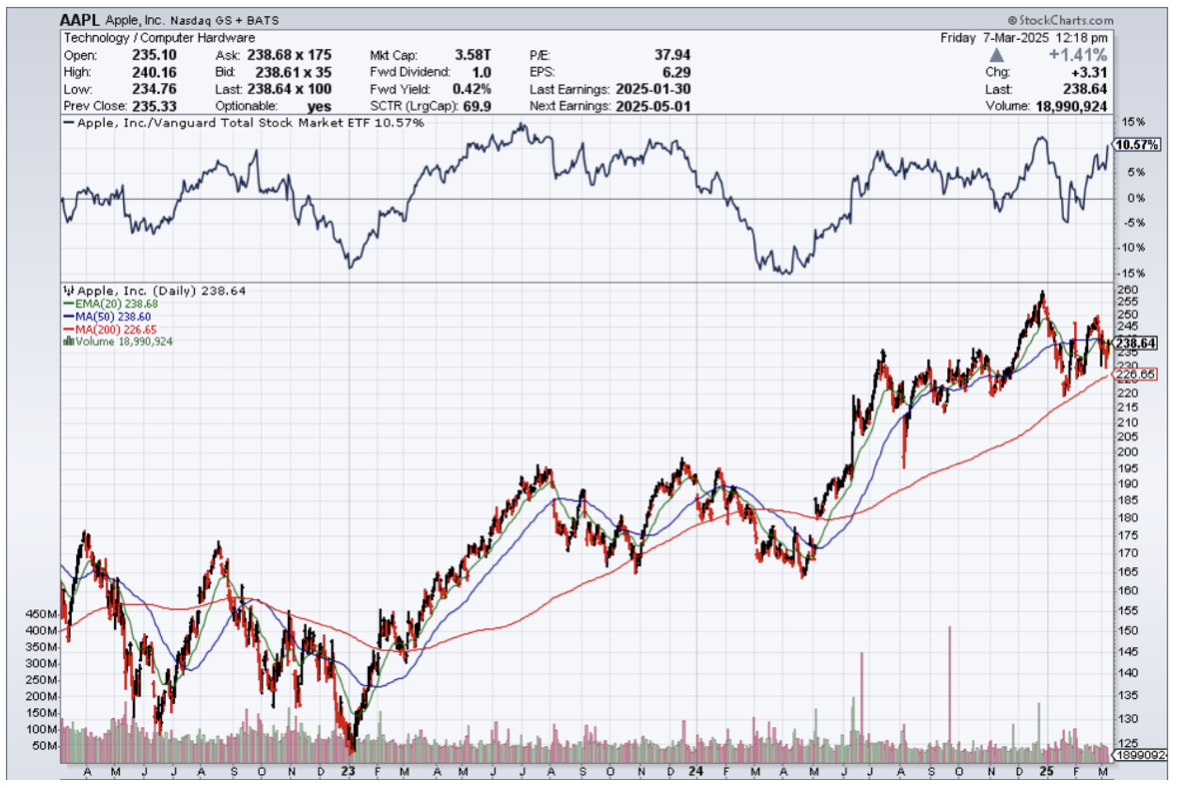

Not only is Apple losing its edge, but they are failing miserably against the Chinese.

China, with its state-supported behemoths, is the bully on the playground, and Apple can’t too diddlysquat.

Apple has been selling the same product for the past 13 years, and the last iterations have been underwhelming, to say the least.

People don’t want to upgrade, forcing to elongate of the refresh cycle.

It’s now so bad that Apple even ceded 5% market share in the final quarter last year to Chinese competition.

Apple is also very late in integrating AI features, signaling that Apple’s software game is behind the times and mediocre at best.

Apple risks falling behind quickly, and the Chinese have really nailed the consumer tech and muscled into this industry.

They are poised to dominate EVs, smartphones, and other value-added tech in the upcoming years.

They plan to seize the moment and squeeze American companies out of the way for good.

Samsung also has been going through a disastrous down cycle after their Android flagship phone peaked a few years ago.

This new trajectory is a slippery slope, and if Apple goes on the cost-cutting path, there will be little talent left to innovate out of this problem.

The iPhone slipped a point to 18% worldwide market share in 2024.

Apple marked a 2% sales decline for the full year at a time that the wider market grew 4% globally.

China’s smartphone makers are all developing their own in-house AI tools and agents, including services that can perform tasks on a user’s behalf.

Samsung also gave up share to faster-growing Android device makers from China, led by Xiaomi and Vivo. Apple marked a 2% sales decline for the full year.

The situation paints a picture of the non-Chinese smartphone markets in a world of hurt.

I believe that Apple and Samsung have nobody to blame but themselves, as those years of forced technological know-how transfer are coming back to bite them where it hurts.

My friends’ kids have these new Chinese smartphones, and I can tell you that I was surprised about how good they perform.

They are run on Android, which is very different from IoS, but they were premium.

German car companies are also feeling this bitter pill as Chinese companies have taken their own technology and implemented it in a more affordable way.

In aggregate, this latest news is a bad omen for Apple’s earnings season.

They are barely jumping over a lower bar, and that will keep happening until something major is revamped in the product lineup.

I believe any steep sell-off would be a nice opportunity to execute a short-term trade to the upside, but those years of buying and holding Apple until eternity is gone.

Readers must really nitpick what this company is doing because management presides over a dull model, and their China business is falling apart as we speak, all while they helped the local Chinese competition over many years take market share with forced technological transfers.

Surprisingly, the stock has done well during the tariff rhetoric and has trudged along sideways while other stocks have really felt the full brunt of the trade escalation.

If we get a smooth patch, I would advocate for a tactical trade to the upside in AAPL.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-07 14:02:522025-03-07 16:44:08Apple Looking To Find Its Mojo

Some asset classes are reflecting the fact that we are already in a full-blown recession, while others are not. In case Iam wrong and we DO go into a recession, knowing how to sell short stocks will be a handy skill to have.

It will become essential to be knowledgeable about all the different ways to add downside protection.

While you are all experts in buying stocks, selling them short is another kettle of fish.

I, therefore, think it is timely to review how to make money when prices are falling. I call it Short Selling School 101.

I don’t think we are going to crash to new lows from here, maybe drop only 10% at worst. So some of the most aggressive bearish strategies described below won’t be appropriate.

If you have big positions in single stocks, like Apple (AAPL), you can execute the same kind of strategy. Selling short the Apple call options to hedge an existing long in the stock looks like the no-brainer here. You should sell one option contract for every 100 shares you own.

There is nothing worse than closing the barn door after the horses have bolted or hedging after markets have crashed.

No doubt, you will receive a wealth of short-selling and hedging ideas from your other research sources and the media right at the next market bottom.

That is always how it seems to play out, great closing the barn doors after the horses have bolted.

So I am going to get you out ahead of the curve, putting you through a refresher course on how to best trade falling markets now, while stock prices are still rich.

I’m not saying that you should sell short the market right here. But there will come a time when you will need to do so.

Watch my Trade Alerts for the best market timing. So here are the best ways to profit from declining stock prices, broken down by security type:

Bear ETFs

Of course, the granddaddy of them all is the ProShares Short S&P 500 Fund (SH), a non-leveraged bear ETF that is supposed to match the fall in the S&P 500 point for point on the downside. Hence, a 10% decline in the (SPY) is supposed to generate a 10% gain in the (SH).

In actual practice, it doesn’t work out like that. The ITF has to pay management operating fees and expenses, which can be substantial. After all, nobody works for free.

There is also the “cost of carry,” whereby owners have to pay the price for borrowing and selling short shares. They are also liable for paying the quarterly dividends for the shares they have borrowed, around 2% a year. And then you have to pay the commissions and spread for buying the ETF.

Still, individuals can protect themselves from downside exposure in their core portfolios by buying the (SH) against it (click here for the prospectus). Short-selling is not cheap. But it’s better than watching your gains of the past seven years go up in smoke.

Virtually all equity indexes now have bear ETFs. Some of the favorites include the (PSQ), a short play on the NASDAQ (click here for the prospectus ), and the (DOG), which profits from a plunging Dow Average (click here for the prospectus).

My favorite is the (RWM) a short play on the Russell 2000, which falls 1.5X faster than the big cap indexes in bear markets (click here for the prospectus).

Leveraged Bear ETFs

My favorite is the ProShares Ultra Short S&P 500 (SDS), a 2X leveraged ETF (click here for the prospectus). A 10% decline in the (SPY) generates a 20% profit, maybe.

Keep in mind that by shorting double the market, you are liable for double the cost of shorting, which can total 5% a year or more. This shows up over time in the tracking error against the underlying index. Therefore, you should date, not marry, this ETF, or you might be disappointed.

3X Leveraged Bear ETF

The 3X bear ETFs, like the UltraPro Short S&P 500 (SPXU), are to be avoided like the plague (click here for the prospectus).

First, you have to be pretty good to cover the 8% cost of carry embedded in this fund. They also reset the amount of index they are short at the end of each day, creating an enormous tracking error.

Eventually, they all go to zero and have to be periodically redenominated to keep from doing so. Dealing spreads can be very wide, further adding to costs.

Yes, I know the charts can be tempting. Leave these for the professional hedge fund intraday traders for which they are meant.

Buying Put Options

For a small amount of capital, you can buy a ton of downside protection. For example, the April (SPY) $182 puts I bought for $4,872 on Thursday allows me to sell short $145,600 worth of large cap stocks at $182 (8 X 100 X $6.09).

Go for distant maturities out several months to minimize time decay and damp down daily price volatility. Your market timing better be good with these because when the market goes against you, put options can go poof and disappear pretty quickly.

That’s why you are reading this newsletter.

Selling Call Options

One of the lowest risk ways to coin it in a market heading south is to engage in “buy writes.” This involves selling short call options against stock you already own but may not want to sell for tax or other reasons.

If the market goes sideways or falls, and the options expire worthless, then the average cost of your shares is effectively lowered. If the shares rise substantially, they get called away, but at a higher price, so you make more money. Then you just buy them back on the next dip. It is a win-win-win.

Selling Futures

This is what the pros do, as futures contracts trade on countless exchanges around the world for every conceivable stock index or commodity. It is easy to hedge out all of the risk for an entire portfolio of shares by simply selling short futures contracts for a stock index.

For example, let’s say you have a portfolio of predominantly large-cap stocks worth $100,000. If you sell short 1 September 2021 contract for the S&P 500 against it, you will eliminate most of the potential losses for your portfolio in a falling market.

The margin requirement for one contract is only $5,000. However, if you are short the futures and the market rises, then you have a big problem, and the losses can prove ruinous.

But most individuals are not set up to trade futures. The educational, financial, and disclosure requirements are beyond mom-and-pop investing for their retirement fund.

Most 401Ks and IRAs don’t permit the inclusion of futures contracts. Only 25% of the readers of this letter trade the futures market. Regulators do whatever they can to keep the uninitiated and untrained away from this instrument.

That said, get the futures markets right, and is the quickest way to make a fortune if your market direction is correct.

Buying Volatility

Volatility (VIX) is a mathematical construct derived from how much the S&P 500 moves over the next 30 days. You can gain exposure to it by buying the iPath S&P 500 VIX Short-Term Futures ETN (VXX) or buying call and put options on the (VIX) itself.

If markets fall, volatility rises, and if markets rise, then volatility falls. You can, therefore, protect a stock portfolio from losses through buying the (VIX).

I have written endlessly about the (VIX) and its implications over the years. For my latest in-depth piece with all the bells and whistles, please read “Buy Flood Insurance With the (VIX)” by clicking here.

Selling Short IPOs

Another way to make money in a down market is to sell short recent initial public offerings. These tend to go down much faster than the main market. That’s because many are held by hot hands, known as “flippers,” don’t have a broad institutional shareholder base.

Many of the recent ones don’t make money and are based on an as-yet unproven business model. These are the ones that take the biggest hits.

Individual IPO stocks can be tough to follow to sell short. But one ETF has done the heavy lifting for you. This is the Renaissance IPO ETF (click here for the prospectus). As you can tell from the chart below, (IPO) was warning that trouble was headed our way since the beginning of March. So far, a 6% drop in the main indexes has generated a 20% fall in (IPO).

Buying Momentum

This is another mathematical creation based on the number of rising days over falling days. Rising markets bring increasing momentum, while falling markets produce falling momentum.

So, selling short momentum produces additional protection during the early stages of a bear market. Blackrock has issued a tailor-made ETF to capture just this kind of move through its iShares MSCI Momentum Factor ETF (MTUM). To learn more, please read the prospectus by clicking here.

Buying Beta

Beta, or the magnitude of share price movements, also declines in down markets. So, selling short beta provides yet another form of indirect insurance. The PowerShares S&P 500 High Beta Portfolio ETF (SPHB) is another niche product that captures this relationship.

The Index is compiled, maintained, and calculated by Standard & Poor's and consists of the 100 stocks from the (SPX) with the highest sensitivity to market movements, or beta, over the past 12 months.

The Fund and the Index are rebalanced and reconstituted quarterly in February, May, August, and November. To learn more, read the prospectus by clicking here.

Buying Bearish Hedge Funds

Another subsector that does well in plunging markets is publicly listed bearish hedge funds. There are a couple of these that are publicly listed and have already started to move.

One is the Advisor Shares Active Bear ETF (HDGE) (click here for the prospectus). Keep in mind that this is an actively managed fund, not an index or mathematical relationship, so the volatility could be large.

Oops, Forgot to Hedge

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/Wile-E.-Coyote-TNT.jpg365496april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-06 09:02:482025-04-07 20:37:51A Refresher Course at Short Selling School

With both market technical and fundamentals going to hell in a handbasket, it’s time to take a refresher course on “Buy Writes.”

I have advised followers to dump the positions they are dating and only keep the ones they are married to. It’s worth enduring a 30% drawdown in a high-quality name to capture a 300% profit over the long term.

If you sell an Amazon (AMZN) or Alphabet (GOOGL) now, I guarantee you that you’re not going to be able to buy them back at the bottom. For a start, when these do bottom out, the universal advice is to sell them because the world is ending….again.

There is always a way to make money in the stock market. Get the direction right, and the rest is a piece of cake.

But what if the market is going nowhere, trapped in a range, with falling volatility? Yes, there is even a low risk, high return way to make money into this kind of market, a lot like the one we have now.

And that’s the way markets work. It’s like watching a bouncing ball, with each successive bounce shorter than the previous one. Thank Leonardo Fibonacci for this discovery (click herefor details).

Which means a change in trading strategy is in order. The free lunch is over. It’s finally time to start working for your money.

When you’re trading off a decade low its pedal to the metal, full firewall forward, full speed ahead, damn the torpedoes. Your positions are so aggressive and leveraged that you can’t sleep at night.

Some four years into the bull market, not so much. It’s time to adjust your trades for a new type of market that continues to appreciate, but at a slower rate and not as much.

Enter the Buy Write.

A buy write is a combination of positions where you buy a stock and also sell short options on the same stock against the shares at a higher price, usually on a one-to-one basis.

“Writing” is another term for selling short in the options world because you are, in effect, entering into a binding contract. When you sell short option, you are paid the premium and the buyer pays, and the cash sits in your brokerage account, accruing interest.

If the stock rallies, remains the same price, or rises just short of the strike price you sold short, you get to keep the entire premium.

Most buy writes take place in front month options, and the strike prices are 5% or 10% above the current share price. I’ll give you an example.

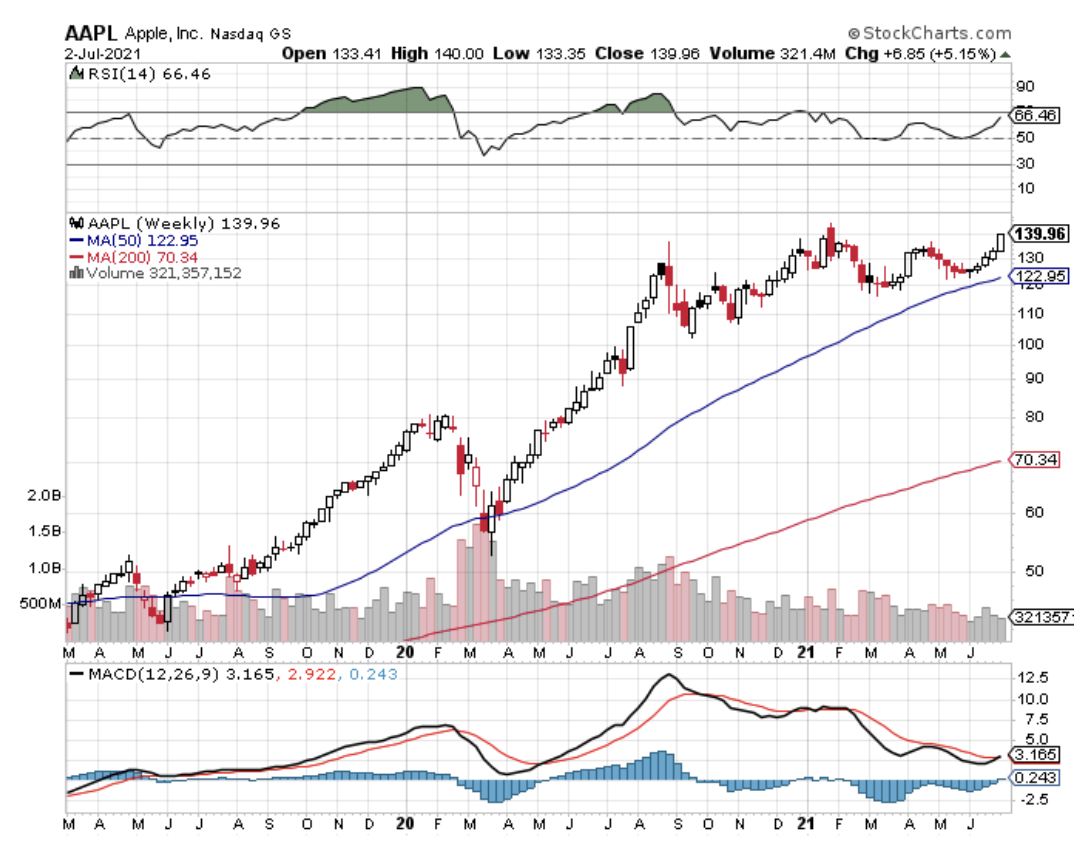

Let’s say you own 100 shares of Apple (AAPL) at $140.You can sell short one August 2021 $150 call for $1.47. You will receive the premium of $147.00 ($1.47 X 100 shares per option). Remember, one option contract is exercisable into 100 shares.

As long as Apple shares close under $150 at the August 20 option expiration, you get to keep the entire premium. If Apple closes over $150, you automatically become short 100 Apple shares. Then, you simply instruct your broker to cover your short in the shares with the 100 Apple shares you already have in your account.

Buy writes accomplish several things. They reduce your risk, pare back the volatility of your portfolio, and bring in extra income. Do these write, and it will enhance the overall performance of your portfolio.

Knowing when to strap these babies on is key. If the market is going straight up, you don’t want to touch buy writes with a ten-foot pole as your stock will be called away, and you will miss substantial upside.

It’s preferable to skip dividend-paying months, usually March, June, September, and December, to avoid your short option getting called away mid-month by a hedge fund trying to get the dividend on the cheap.

You don’t want to engage in buy writes in bear markets. Whatever you take in with option premium, it will be more than offset by losses on your long stock position. You’re better off just dumping the stock instead.

Now comes the fun part. As usual, there are many ways to skin a cat.

Let’s say that you are a cautious sort. Instead of selling short the $150 strike, you can sell the $155 strike for less money. That would bring in $79 per option. But your risk of a call away drops, too.

You can also go much further out in your expiration date to bring in more money. If you go out to the January 18, 2022, expiration, you will take in a hefty $6.67 in option premium, or $667 per option. However, the likelihood of Apple rising above $150 and triggering a call away by then is far greater.

Let’s say you are a particularly aggressive trader. You can double your buy-write income by doubling your option short sales at the ratio of 2:1. However, if Apple closes above $150 by expiration day, you will be naked short 100 shares of Apple.

It is likely you won’t have enough cash in your account to meet the margin call for selling short 100 shares of Apple, so you will have to buy the shares in the market immediately. It is something better left to professionals.

How about if you are a hedge fund trader with a 24-hour trading desk, a good in-house research department, and serious risk control? Then you can entertain “at-the-money buy writes.”

In the case of Apple, you could buy shares and sell short the August 20 $140 calls against them for $4.45 and potentially take in $4.45 for each 100 Apple shares you own. Then, you make a decent profit if Apple remains unchanged or goes up less than $4.45.

That amounts to a $3.18% return in 34 trading days and annualizes out at 26%. In bull markets, hedge funds execute these all day long, but they have the infrastructure to manage the position. It’s better than a poke in the eye with a sharp stick.

There are other ways to set up buy wrights.

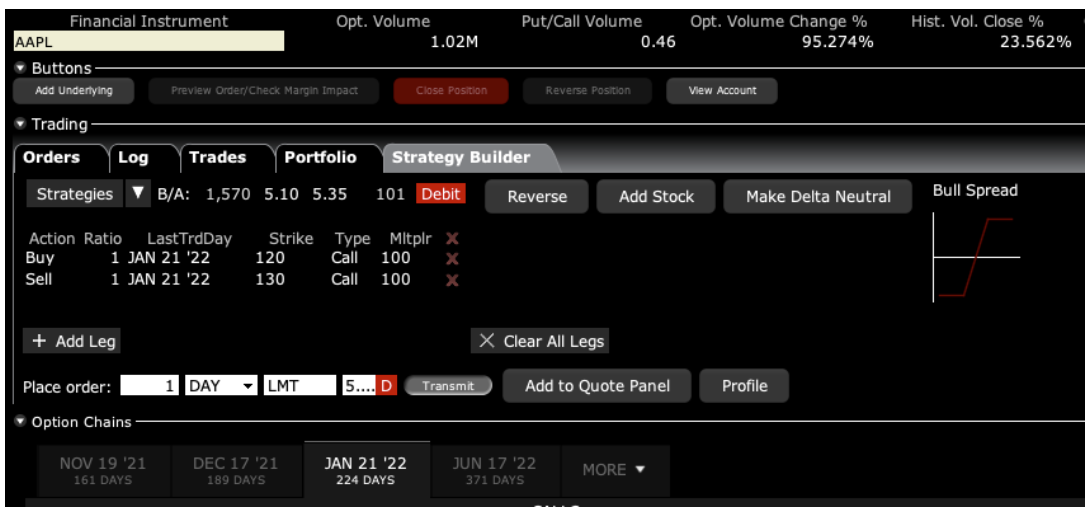

Instead of buying stock, you can establish your long position with another call option. These are called “vertical bull call debit spreads” and are a regular feature of the Mad Hedge Trade Alert Service. “The “vertical” refers to strike prices lined up above each other. The “debit” means you have to pay cash for the position instead of getting paid for it.

How about if you are a cheapskate and want to get into a position for free? Buy one call option and sell short two call options against it for no cost. The downside is that you go naked short if the strike rises above the short strike price, again triggering a margin call.

Here is my favorite, which I regularly execute in my own personal trading account. Buy long-term LEAPS (Long Term Equity Anticipation Securities) spreads like I recommended three weeks ago with the (AAPL) January 21 $120-$130 vertical bull call spread for $5.20.

On Friday, it closed at $7.21, up 38.65%.

This is a bet that one of the world’s fastest-growing companies will see its share unchanged or higher in seven months. In Q1, Apple’s earnings grew by an astonishing 35% to $23.6 billion. Sounds like a total no-brainer, right?

If I run this position all the way to expiration, and I probably will, the total return will be ($10.00 - $5.20 = $4.80), or ($4.80/$5.20 = 92.31%) by the January 21, 2022, option expiration. This particular expiration benefits from the year-end window dressing surge and the New Year asset allocation into equities.

Whenever we have a big up month in the market, I sell short front-month options against it. In this case, that is the August 20 $150 calls. This takes advantage of the accelerated time decay you get in the final month of the life of an option, while the time decay on your long-dated long position is minimal.

Keep in mind that the deltas on LEAPS are very low, usually around 10%, because they are so long-dated. That means your front month short should only be 10% of the number of shares owned through your LEAPS in order to stay delta-neutral. Otherwise, you might get hit with a margin call you can’t meet.

After doing this for 53 years, it is my experience that this is the best risk/reward options positions available in the market.

To make more than 92.31% in seven months, you have to take insane amounts of risk or engage in another profession, like becoming a rock star, drug dealer, or Bitcoin miner.

I’m sure you’d rather stick to options trading, so good luck with LEAPS.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/01/john-california-eagles.png297377Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2025-03-04 09:02:462025-03-04 12:46:22A Buy Write Primer

A $599 cheaper iPhone with worse features is clearly a sign that Apple (AAPL) is on its way down from peak innovation.

This new cheap phone won’t save the company, but the company doesn’t really need saving.

The company is on auto-pilot mode. Let me explain.

At this point, CEO Tim Cook has done the calculations and he has decided that the company doesn’t need to innovate.

Apple needs to milk its subscriber base whom are famously loyal to its ecosystem.

Apple users are the least likely to just jump ship and switch to the Android ecosystem.

Cook knows that which is why he can push through annual increases in service charges.

Apple’s balance sheet is also another key part of the story and Cook will wield it with extreme efficacy through shareholder returns.

It could be true that we are past the stage of Apple delivering big growth numbers.

That looks to be a thing of the past.

Now, competing with China on cheaper phones is a massive step back and it won’t flow through to the bottom line.

It’s easier to argue that this phone will cannibalize sales of Apple’s more expensive phones.

We have arrived at this point and it is sad for most technologists.

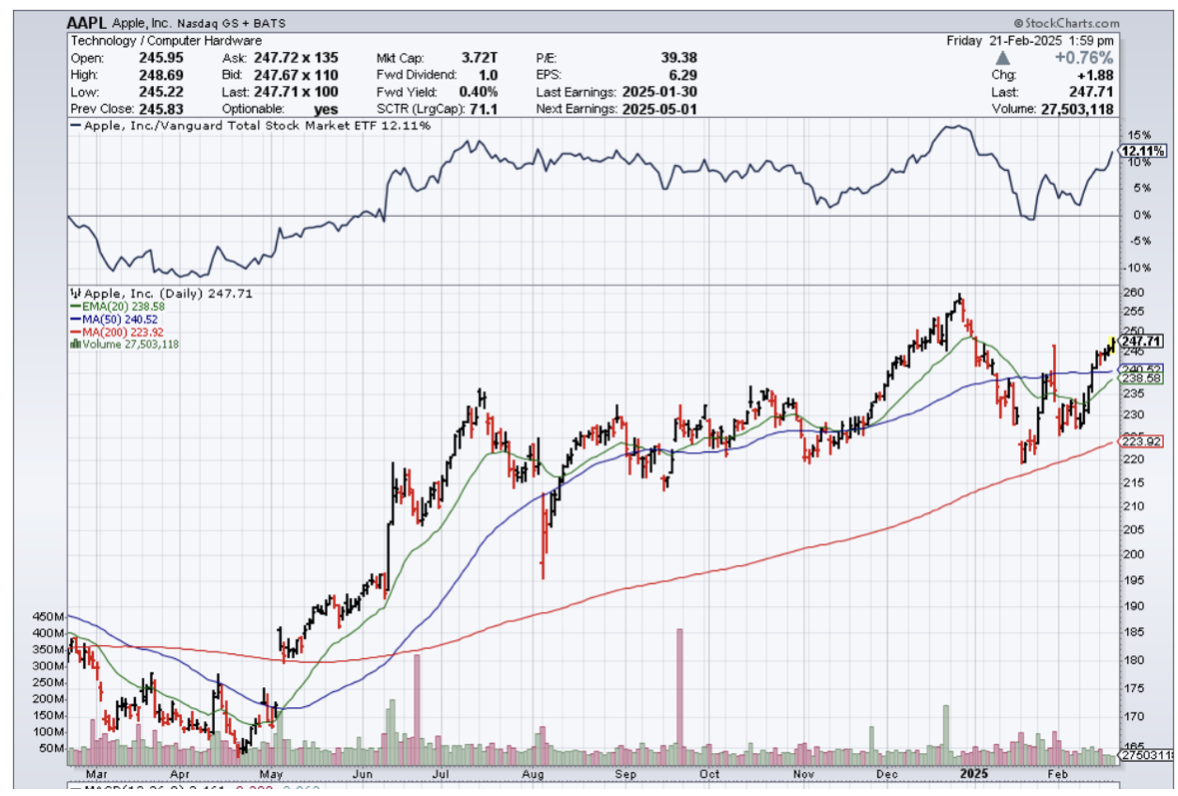

Apple AAPL expanded the iPhone 16 family with the launch of a cheaper iPhone 16e version powered by the latest A18 chip and supporting Apple Intelligence.

iPhone 16e is available in a 6.1-inch display size and has the best battery life ever on this display size offered by Apple. The iPhone 16e, available from Feb. 28, will cost $599 compared with $799 for iPhone 16 and $999 for iPhone 16 Pro.

Although iPhone sales decreased 0.8% year over year to $69.14 billion in the first quarter of fiscal 2025, Apple saw better iPhone 16 sales in those regions where Apple Intelligence was available. iPhone’s active installed base grew to an all-time high and saw a record level of upgrades in the reported quarter. The iPhone was a top-selling model in the United States, Urban China, India, the U.K., France, Australia and Japan.

AAPL maintained its lead over Samsung for the second consecutive year, with a market share of 23% compared with the latter’s 16%. Xiaomi trailed both Apple and Samsung with 13% market share. Global smartphone shipments increased 7% year over year to $1.22 billion units in 2024.

Apple has more than 1 billion paid subscribers in its ecosystem and the focus is entirely on them. There are only 8 billion people on this planet and Apple has decided it is not worth going after the other 7 billion.

If they haven’t adopted an Apple phone or tablet then this last cheap phone is the last chance. Even then, the reason they most likely haven’t adopted an Apple device is because they cannot afford it.

Apple shares are down 1% this year at the time of this writing and I still believe this is a buy-the-dip stock even with a weakening business model.

Apple knows they can withstand earnings whenever they want by just increasing their dividend.

Another headwind is that Apple is not one of the leaders in AI and shareholders will wait to see how that plays out.

Buy the dip in Apple, but don’t hold it long-term.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-02-21 14:02:582025-02-21 15:03:08The Affordable iPhone From Apple

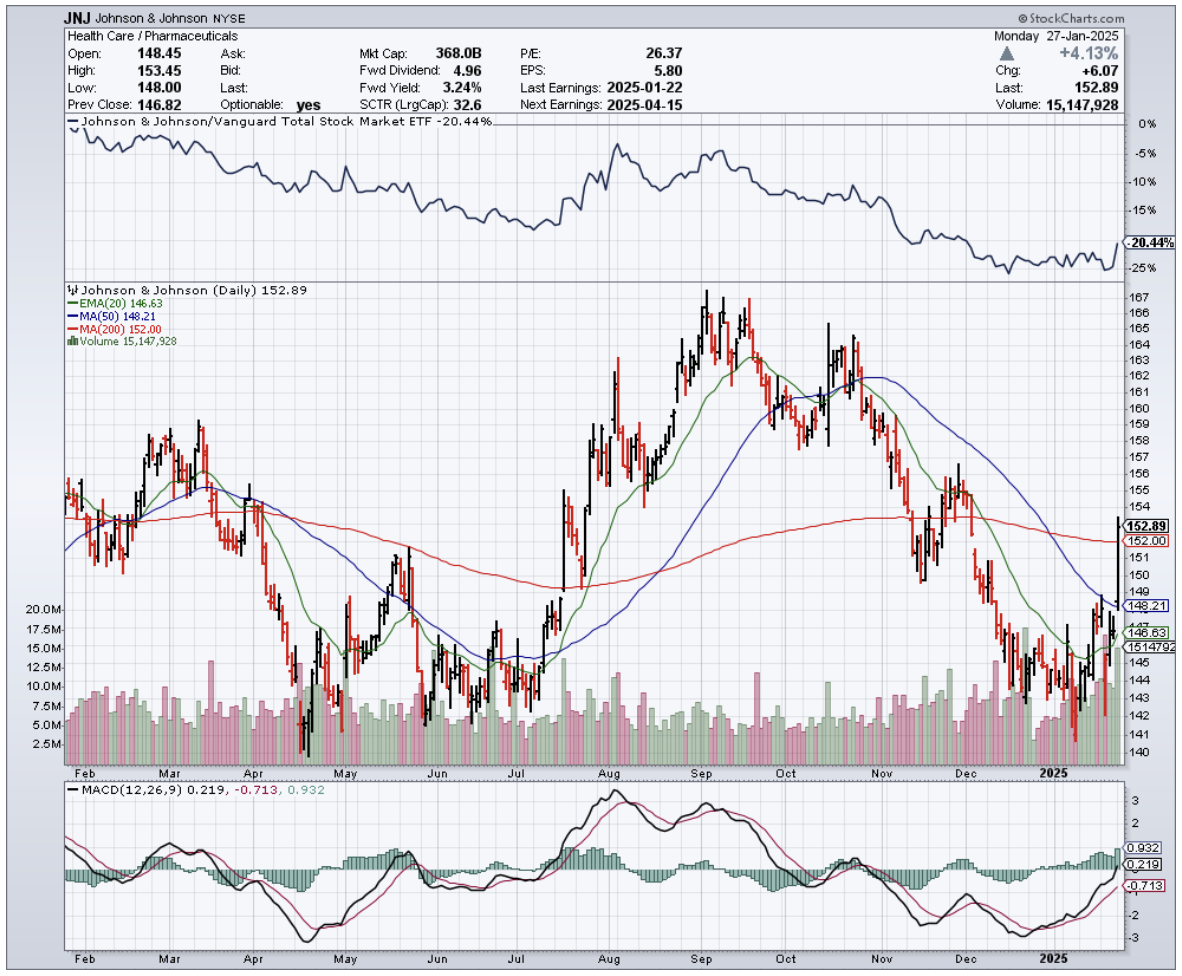

I had to laugh when I saw Johnson & Johnson's (JNJ) Q4 earnings hit my screen earlier this month.

Here we have Wall Street wringing its hands over a slight revenue miss, sending shares down 3.5%, while management is busy plotting its path to pharma industry dominance.

The numbers tell an interesting story.

Q4 revenues grew 5.3% (or 5.7% on an adjusted operational basis) to $22.5 billion. Wall Street got the vapors because earnings came in at $1.41 per share, well below their $2.04 consensus.

Reminds me of the time analysts completely missed Apple's (AAPL) transformation into a services company.

For the full year 2024, JNJ delivered 4.3% sales growth (5.4% operational) to $88.8 billion, with earnings per share landing at $5.79, or $9.98 adjusted after swallowing a $(0.67) hit from acquired IPR&D charges.

Not too shabby for a company in transition.

Looking into 2025, management is guiding for 2.5-3.5% operational sales growth ($90.9-91.7 billion) and adjusted operational EPS of $10.75-$10.95.

That's 8.7% growth at the midpoint, though they're careful to hedge around legal proceedings and acquisition costs.

And here's where it gets interesting.

During last week's JP Morgan Healthcare Conference, CEO Joaquin Duato was practically bouncing in his chair about their drug pipeline. Let's look at what's got him so excited.

Darzalex, their multiple myeloma superstar, raked in $11.67 billion in 2024, up 20%.

The new kid Carvykti exploded 93% higher to $963 million. Tecvayli landed $550 million in its rookie year.

Depression med Spravato jumped 56% to hit the magic $1 billion mark. Tremfya, their Stelara successor, grew 17% to $3.7 billion.

Speaking of Stelara – there's the elephant in the room.

JNJ's crown jewel is losing patent protection, already showing up in Europe with a >12% sequential decline in Q4 to $2.35 billion. Expect a 30% "haircut" this year.

But here's what Wall Street is missing: JNJ saw this coming years ago.

They just dropped $14.6 billion on Intracellular Therapies, mostly debt-funded (they can afford it with only $31.3 billion in long-term debt and $19.98 billion in cash).

This brings them Caplyta, an antipsychotic med with blockbuster potential that's already approved for schizophrenia and bipolar disorders.

The medical device business isn't sitting still either.

Q4 worldwide revenues jumped 6.7% year-on-year. While Surgery was flat at $2.5 billion and Orthopedics grew a modest 2.5% to $2.32 billion, Vision popped 9% to $1.3 billion.

But the real story? Cardiovascular surged 24% to $2.1 billion. Those Shockwave and Abiomed acquisitions are looking pretty smart right about now.

For the year, MedTech grew 4% to $31.56 billion. Operating margins slipped a bit – Innovative Medicines down from 42% to 39.4%, MedTech from 23.7% to 21.6%.

Late-stage pipeline products nearing approval should ease R&D expenses in 2025, just as JNJ gears up for its next growth phase.

The foundation looks rock solid - $19.98 billion in cash, $31.3 billion in long-term debt, 2025 adjusted EPS guidance of $10.75-$10.95, and that reliable $1.24 quarterly dividend.

But forget the current numbers - the real money's in what's coming next.

Here's what the market is missing: JNJ is promising 5-7% compound annual growth between 2025-2030, with ten drugs hitting $5+ billion in annual sales by decade's end.

Sound ambitious? Maybe. But they've got the pipeline to back it up – from immunology stars nipocalimab and icotrokinra to neuroscience contenders seltorexant and aticaprant, plus oncology plays like TAR-200 for bladder cancer.

I've seen this movie before with AbbVie (ABBV), which navigated the loss of $20+ billion Humira without missing a beat.

And JNJ looks even better positioned - their pharma division is targeting $58 billion in 2024 revenues, which would make them the biggest player in Big Pharma, ahead of Pfizer (PFE), AbbVie (ABBV), Roche (RHHBY), AstraZeneca (AZN), Sanofi (SNY) and Novartis (NVS).

The only real wildcard? That pesky talc litigation.

JNJ's latest move – spinning the lawsuits into Red River Talc LLC and filing for bankruptcy – could cap the damage at $8.5 billion. They claim 75% of claimants are on board, with a court ruling expected this month.

So, what's my take? I think JNJ's 2025 will be a "reset" year, especially the first half. But just like buying straw hats in winter, there might be an opportunity here for patient investors. Management says the back half will be stronger, setting up 2026 for what could be a very interesting guidance call.

While the market frets about Stelara's patent cliff, smart money is quietly building positions. That's why I'm maintaining my stand to buy the dip.

After all, sometimes the best trades are the ones that make you a bit uncomfortable at first. And if you're worried about patent cliffs, just ask any AbbVie shareholder how that worked out for them.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-01-28 12:00:202025-01-28 12:23:27Ready, Reset, Go

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.