Mad Hedge Biotech and Healthcare Letter

January 23, 2025

Fiat Lux

Featured Trade:

(THE HARD TRUTH ABOUT THIS BIOTECH'S PIPELINE THAT WALL STREET DOESN'T GET)

(MRK), (AMGN), (AAPL)

Mad Hedge Biotech and Healthcare Letter

January 23, 2025

Fiat Lux

Featured Trade:

(THE HARD TRUTH ABOUT THIS BIOTECH'S PIPELINE THAT WALL STREET DOESN'T GET)

(MRK), (AMGN), (AAPL)

Earlier this month, while reviewing my biotech holdings during a layover at Chicago O'Hare, I got an interesting call from a long-time reader.

He was panicking about Merck (MRK) after seeing it trading near its 52-week lows, convinced the pharmaceutical giant was headed for trouble.

"Have you seen what Medicare negotiations did to Januvia?" he asked, referencing the 79% price reduction. "And Keytruda's patent expires in 2028!"

Here's the hard truth about this biotech's pipeline that Wall Street doesn't get: while everyone's fixated on Keytruda's patent cliff, Merck has quietly tripled their late-stage pipeline in just over three years.

We're talking more than 20 unique assets in late-stage development, plus another 50 in early stages.

The last time I saw this kind of pipeline expansion was during the early days of Amgen (AMGN), which turned out pretty well for investors who saw past the obvious.

Actually, Merck's current "crisis" also reminds me of the time I bought Apple (AAPL) right after Steve Jobs announced the iPhone. Everyone worried about the risk, while I saw the opportunity.

Merck just posted Q3 2024 numbers that would make most CEOs envious: revenue up 7% year-over-year to $16.7 billion.

Keytruda, their cancer blockbuster, grew 21% to $7.4 billion. Even their Animal Health division jumped 11%. These aren't the numbers of a company in trouble.

Speaking of investors, they've enjoyed a 126% total return over the past decade with Merck, despite more ups and downs than my last flight through turbulence.

The company's 5-year average Return on Equity sits at 25% (recently climbing to 28%), with Return on Invested Capital steady at 20%.

With a Weighted Average Cost of Capital around 8%, there's plenty of room for growth.

Yesterday, I was discussing these numbers with a former FDA commissioner (who shall remain nameless) over coffee.

He pointed out something fascinating: Merck's R&D spending is increasing alongside revenue growth. That's like a tech company doubling down on product development – exactly what you want to see in pharma.

For dividend hunters (and I know many of you are), Merck offers a 3.3% yield with a 7% five-year dividend growth rate.

The payout looks sustainable too, consuming 68% of earnings and 55% of free cash flow. It's not going to make you quit your day job, but it's better than the 1.4% you'll get from the S&P 500.

Looking at valuation, Merck trades at a P/E of 20.5, below its historical average of 22.3.

My own growth projections suggest a 13% annual rate going forward. Optimistic? Perhaps. But with their robust pipeline and near-term analyst projections, I've seen crazier things work out.

The company just announced a $15 billion share repurchase program, including plans to spend $7.5 billion over the next 12 months. When management puts that kind of money where their mouth is, I tend to pay attention.

Yes, Keytruda's patent cliff in 2028 is real. But so is Merck's late-stage pipeline of antibody-drug conjugates (ADCs) – think smart missiles in the war against cancer.

And unlike some biotechs, Merck has the financial muscle to weather any storm, with decreasing net debt and a solid cash position.

Remember what I always say about buying straw hats in winter? Merck right now is like finding a premium pharma stock in the discount bin.

Just like my friend who panicked and sold everything after the November 8 election (and missed the subsequent rally), sometimes the best opportunities come disguised as problems.

As for me, I'm looking at Merck as a potential long-term hold. The company's fundamentals remind me of other great turnaround stories I've traded successfully over the years.

With the healthcare sector currently out of favor and Merck trading near its 52-week lows, this might be one of those moments we look back on and wish we'd bought more.

And speaking of patents, maybe I should patent my strategy: “Buy great companies when everyone else is afraid.” Though I suspect Warren Buffett already beat me to that one.

Mad Hedge Technology Letter

January 13, 2025

Fiat Lux

Featured Trade:

(APPLE DROPS THE BALL)

(AAPL), (SAMSUNG), (CHINA)

Not only is Apple losing its edge, but they are failing miserably against the Chinese.

China, with its state-supported behemoths, is the bully on the playground and Apple can’t too diddlysquat.

Apple has been selling the same product for the past 13 years and the last iterations have been underwhelming, to say the least.

People don’t want to upgrade forcing them to elongate the refresh cycle.

It’s now so bad that Apple even ceded a 5% market share in the final quarter last year to Chinese competition.

Apple is also very late in integrating AI features signaling that Apple’s software game is behind the times and mediocre at best.

Apple risks falling behind quickly and the Chinese have really nailed the consumer tech and muscled into this industry.

They are poised to dominate EVs and smartphones and other value-added tech in the upcoming years.

They plan to seize the moment and squeeze American companies out of the way for good.

Samsung also has been going through a disastrous downcycle after their Android flagship phone peaked a few years ago.

This new trajectory is a slippery slope and if Apple goes on the cost-cutting path, there will be little talent left to innovate out of this problem.

The iPhone slipped a point to 18% worldwide market share in 2024.

Apple marked a 2% sales decline for the full year, at a time when the wider market grew 4% globally.

China’s smartphone makers are all developing their own in-house AI tools and agents, including services that can perform tasks on a user’s behalf.

Samsung also gave up its share to faster-growing Android device makers from China, led by Xiaomi and Vivo. Apple marked a 2% sales decline for the full year.

The situation paints a picture of the non-Chinese smartphone markets in a world of hurt.

I believe that Apple and Samsung have nobody to blame, but themselves as those years of forced technological know-how transfer are coming back to bite them where it hurts.

My friends’ kids have these new Chinese smartphones and I can tell you that I was surprised about how good they perform.

They are run on Android, which is very different from IoS, but they are premium.

German car companies are also feeling this bitter pill as Chinese companies have taken their own technology and implemented it in a more affordable way.

In aggregate, this latest news is a bad omen for Apple’s earnings season.

They are barely jumping over a lower bar and that will keep happening until something major is revamped in the product lineup.

I believe any steep sell-off would be a nice opportunity to execute a short-term trade, but those years of buying and holding Apple until eternity are gone.

Readers must really nitpick what this company is doing because management presides over a dull model and their China business is falling apart as we speak all while they helped the local Chinese competition over many years take market share with forced technological transfers.

Not a good look and things could get worse as we move deeper into the year.

Mad Hedge Biotech and Healthcare Letter

December 31, 2024

Fiat Lux

Featured Trade:

(SOMETIMES WALL STREET GETS IT WRONG)

(BMY), (AAPL), (MRK)

Sitting in my stateroom aboard the Coral Princess, about 200 miles off Mexico's west coast, I found myself chuckling at the market's reaction to Bristol-Myers Squibb’s (BMY) latest developments. Sometimes Wall Street reminds me of my old physics professor - brilliant but occasionally missing the forest for the quantum trees.

Here's what caught my attention: BMY's stock has outperformed the broader market by +15% since July, yet still trades at a measly 7.91x forward P/E while its sector peers strut around at 20.53x. It's like finding a Ferrari in a used car lot, priced like a Corolla.

The cynics, of course, point to the patent cliff. "What about Eliquis in 2026? Opdivo in 2028?" they ask, wringing their hands. But that's exactly where it gets interesting.

Just earlier this month, BMY announced FDA approval for Opdivo Qvantig - their new subcutaneous version that cuts treatment time from 30 minutes to 5 minutes. If you've ever spent time in cancer treatment centers like I have, you know those 25 minutes make a world of difference.

BMY's commercial team expects this version to capture 75% of Opdivo's business, with 30-40% of patients switching from IV. That's not just convenience - it's strategic patent life extension.

Speaking of strategy, let's talk about their growth portfolio, which has quietly expanded 20% year-over-year and now represents 48.7% of their business.

Remember when Apple (AAPL) transformed from computers to mobile devices? BMY is pulling a similar pivot, just without the flashy keynotes.

Take their $14 billion Karuna acquisition. Their newly approved schizophrenia treatment, Cobenfy, targets a market projected to hit $15.23 billion by 2034. The timing here is masterful - monetization starts in early 2025, well before the patent cliffs hit.

Meanwhile, they're cleaning up their balance sheet faster than a neat freak with a new vacuum. They've already slashed $4.31 billion in debt this year, with plans to cut $10 billion by 2026.

Their free cash flow has grown to $13.8B, up 18.1% sequentially. At this rate, they'll have plenty of dry powder for more strategic moves.

But here's what really makes me scratch my head: while everyone's fixated on the patent cliff, BMY has quietly added 8 new oncology registrational trials in the past year. Their oncology trio - Opdivo, Yervoy, and Opdualag - is growing at 7.6% year-over-year.

Sure, Merck's (MRK) Keytruda is the 800-pound gorilla with $25 billion in sales, but BMY's playing a different game - diversification with shots on goal across multiple therapeutic areas.

Now, I'm not suggesting you back up the truck tomorrow morning. The stock might see some pressure after the January 3, 2025 ex-dividend date, possibly testing support at $51 or even $48. But with a 4.45% dividend yield and a valuation at half its historical average, patient investors might find this an interesting entry point.

Speaking of timing - Wall Street's greatest fortunes were made by investors who saw value where others saw problems. Right now, most analysts are staring at BMY's patent cliff like deer in headlights.

Meanwhile, I'm seeing a company with a 4.45% dividend yield, a growth portfolio expanding at 20% annually, and a valuation that's practically begging to double.

As I wrap this up from somewhere off the Mexican coast (where I'm supposedly on vacation but can't help analyzing stocks between rounds of Monopoly), I'm reminded of something I learned in my decades of trading: The crowd is usually looking through the wrong end of the telescope.

While they're zoomed in on 2026's patent expirations, they're missing the transformation happening right now in front of their eyes.

Maybe that's why I've averaged +50% returns for over a decade - I tend to look where others don't. BMY just might be one of those opportunities that makes next year's Christmas gift to my subscribers an even bigger winner than this year's +75.25% return.

Now, if you'll excuse me, my banjo needs tuning, and I have a Monopoly empire to build. But remember - in both board games and markets, the best players are always thinking three moves ahead. BMY's management certainly is.

Global Market Comments

December 26, 2024

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN)

Global Market Comments

December 23, 2024

Fiat Lux

Featured Trade:

(A BUY WRITE PRIMER)

(AAPL)

Mad Hedge Technology Letter

December 13, 2024

Fiat Lux

Featured Trade:

(THE AI TRAIN KEEPS CHUGGING)

(DELL), (AAPL), (NVDA)

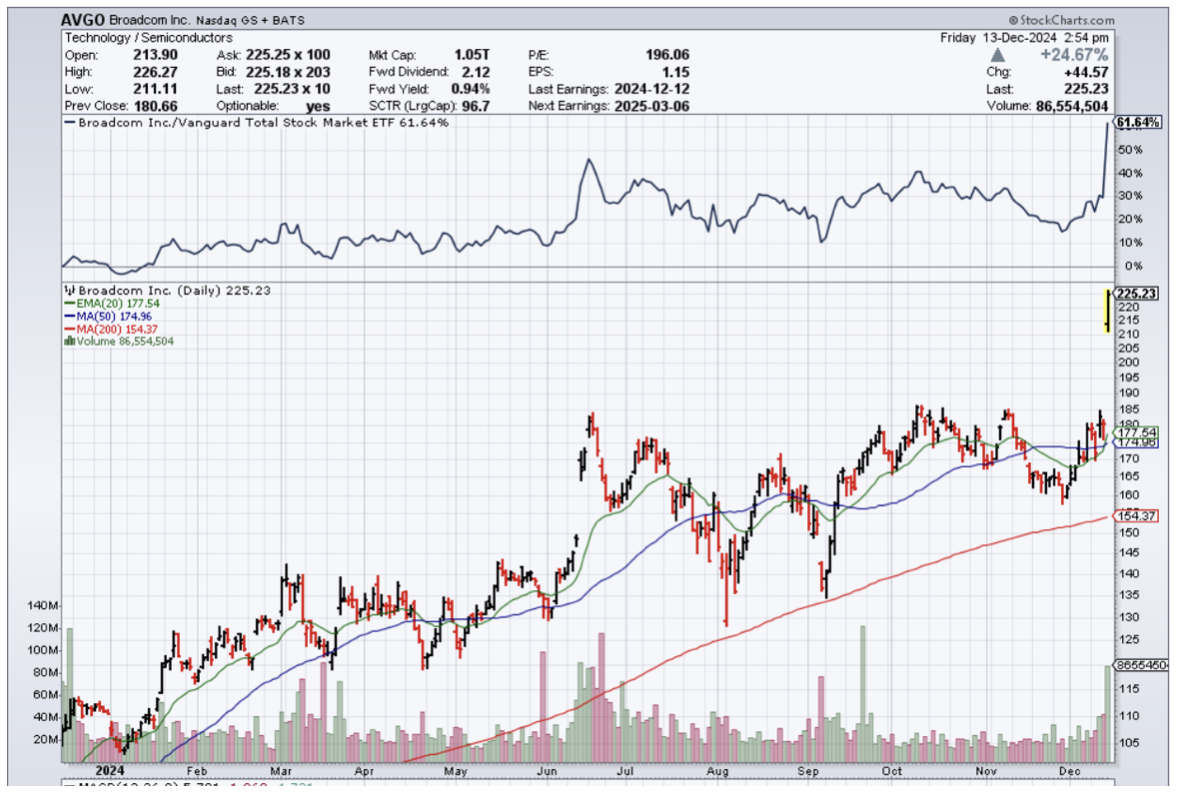

If anyone needs another AI data point, the tech market just delivered us a juicy one with an outstanding earnings call with Broadcom (AVGO) and its CEO Hock Tan.

The AI enterprise build-out has been developing in full-force and investors are pouring money into the foundation of the AI future.

That is currently where the AI profits currently lie.

The software companies have missed out on that profit in the short-term, but since many are also involved in the AI infrastructure spend, they can turn to their investors and ask for a mark-up in owned shares.

This won’t always be the case, and I do believe we are fast reaching an inflection point where shareholders will demand more from their capital and not just more AI data centers and more modern AI semiconductor chips.

I am talking about meaningful revenue growth directly tied to AI spend – we don’t have that yet.

At some point, there needs to be an application from all of this money spent and return on capital.

In the meantime, Mr. Market is cheering the success of AVGO and the stock is up 25% today at the time of this writing signaling investors will continue to back this AI infrastructure spend into 2025 and possibly beyond.

Broadcom CEO Hock Tan said the company expects its custom AI chips will generate between $60 billion and $90 billion in revenue over the next three years from its three existing hyperscaler customers, whom the company did not name. Tan reiterated his belief that each of the three hyperscalers will deploy 1 million clusters of its custom AI chips called XPUs by 2025.

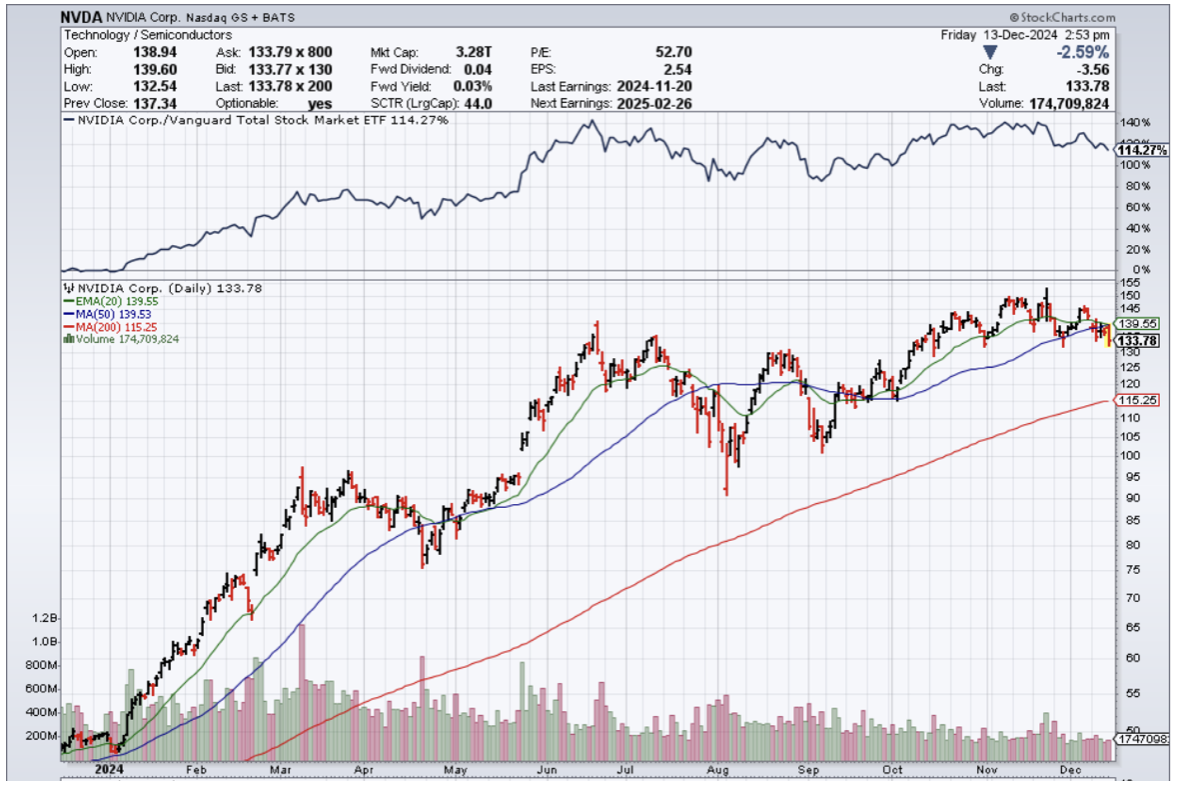

Apple is reportedly working with Broadcom to develop an AI server chip. The move by tech giants to make their own server chips is meant to cut costs and scale back their reliance on Nvidia’s (NVDA) GPUs (graphics processing units).

That trend is reflected in the industry at large. The AI chip market is set to grow 74% in 2025, while the semiconductor market overall is projected to grow just 12% next year.

We are seeing this type of binary divergence in tech firms like Dell and Oracle.

Many of these legacy tech companies are attempting to wean themselves from a legacy business that is expanding in the low single digits.

From a technical perspective, any dip to the $200 level will be a strong buy for AVGO.

I believe they continue to pivot into the AI infrastructure build while partnering with companies that can aid this type of success.

They will continue to invest in products related to AI, mainly chips, which will be installed in a wide array of businesses like data centers, consumer electronics like smartphones and laptops, and electric vehicles.

AVGO has been a hot company for quite a while, and even though not quite an Nvidia, I do believe AVGO stock is a solid backup option for tech investors looking for some diversification.