(MARKET OUTLOOK FOR THE WEEK AHEAD, or IRAN WAR SETS MARKETS ON FIRE),

(USO), (GLD), (SLV), (TLT), (GS), (FCX),(XOM), (PFE), (BMY), (PFE),(XLF), (IWM), (TAB), (NVDA), (DGE.L), (IBM), (DHI), (AMD)

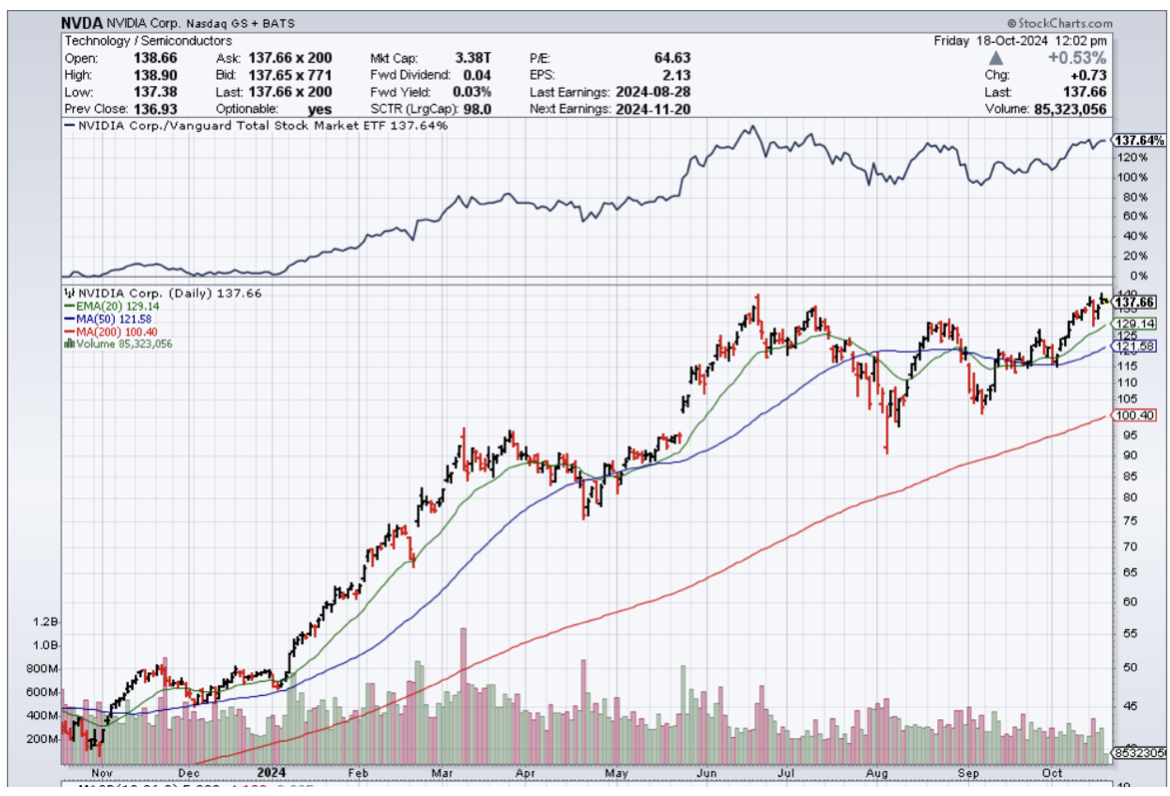

If you thought that AI chips had reached the high water mark, then you are entirely wrong.

Nvidia has been one of the only games in town, and that is a strong sign of a first-mover advantage.

In fact, the ecosystem could benefit if several chip companies could rise to the occasion to infuse that extra bit of supply.

Nvidia is on record, saying they can’t meet demand.

Well, we have finally reached the next phase of the AI chip story, and that is the next company stepping up to the plate.

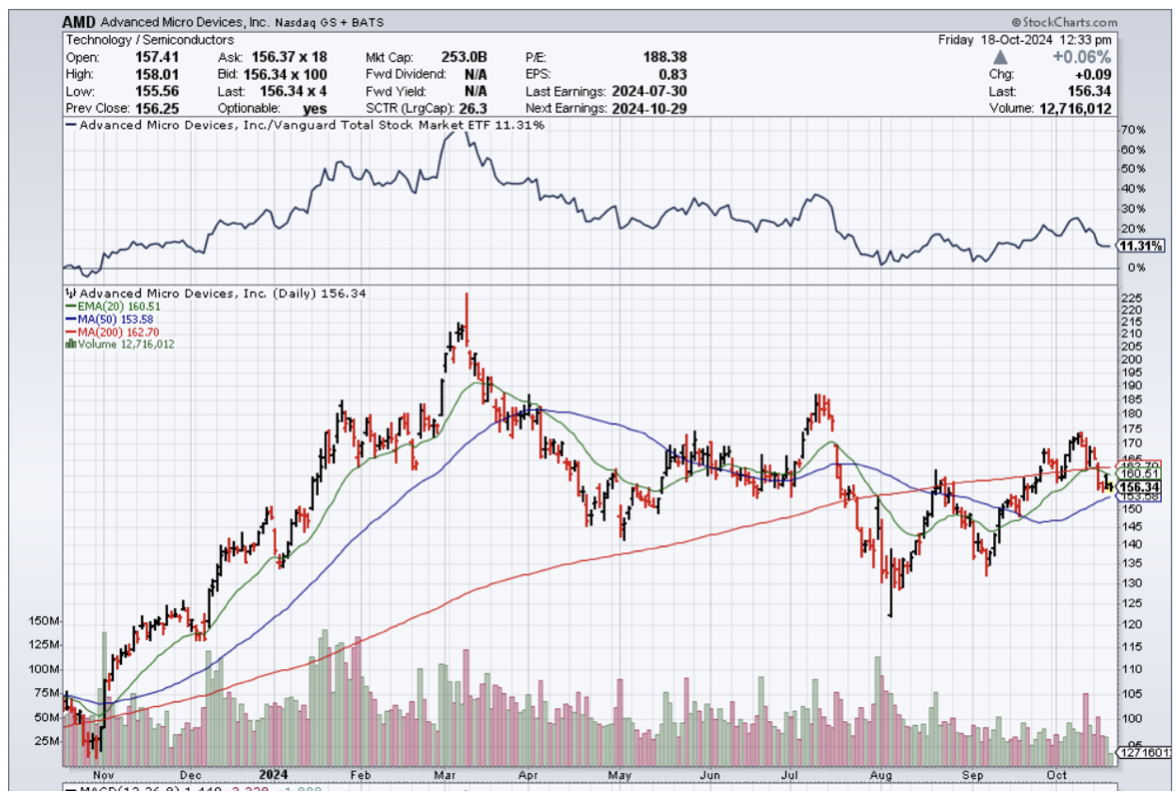

AMD (AMD) has been working furiously to get into the AI GPU game, and it appears as if their harvest is just around the corner.

For the past 18 months, Nvidia (NVDA) has dominated the GPU industry with a ball-busting market share of up to 98%.

Nvidia's H100 GPU set the benchmark for AI training and AI inference.

The H100 is still a sizzling product today, and Nvidia continues to struggle with supply constraints because demand is so high from leading AI companies like OpenAI, Amazon, Microsoft, and more.

Those supply challenges have opened the door for competitors like Advanced Micro Devices to swoop out of nowhere. The company announced its own data center GPU called the MI300X at the end of 2023, which was specifically designed to compete with the H100. So far, it has lured in some of Nvidia's top customers, including Microsoft, Oracle, and Meta Platforms.

AMD forecasts the MI300 series will propel its GPU revenue to a record $4.5 billion in 2024 - an estimate that has already been raised twice.

Nvidia still is the champion - it started shipping its new H200 GPU earlier this year, which is capable of performing AI inference at nearly twice the speed of the H100.

Nvidia is now focused on its latest Blackwell chip architecture, which paves the way for the biggest leap in performance so far. The new GB200 NVL72 system is capable of performing AI inference at a whopping 30x the pace of the equivalent H100 system.

AMD is preparing to ship another new GPU next year called the MI350X, offering a staggering leap in performance of 35x compared to CDNA 3 chips like the original MI300X.

Advanced Micro Devices has explicitly said the MI350X will compete directly with Nvidia's Blackwell chips.

Nvidia plans to ramp up shipments of Blackwell GPUs during its fiscal 2025 fourth quarter.

A 114% increase year over year in data center revenue is what it looks like on the balance sheet for AMD.

Developing artificial intelligence (AI) software wouldn't be possible without data centers and the powerful graphics processing chips (GPUs) inside them.

This is where we stand – at the beginning of an AI-induced supercycle in technology stocks.

AMD is clearly the 2nd horse in the race that will pick up market share on Nvidia.

This could easily turn into a duopoly of GPU chip companies, and readers would be ignorant to not apply this knowledge a trading regimen.

Wait for a substantial dip to buy into AMD shares.

You’ll regret it if you don’t, especially long-term.

Last weekend, I had dinner with one of the oldest and best-performing technology managers in Silicon Valley. We met at a small out-of-the-way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables.

The service was poor and the food indifferent, as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information I had to promise the utmost in confidentiality. If I mentioned his name you would say “Oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on these lowest-of-margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third-party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer, who once in, buys more services.

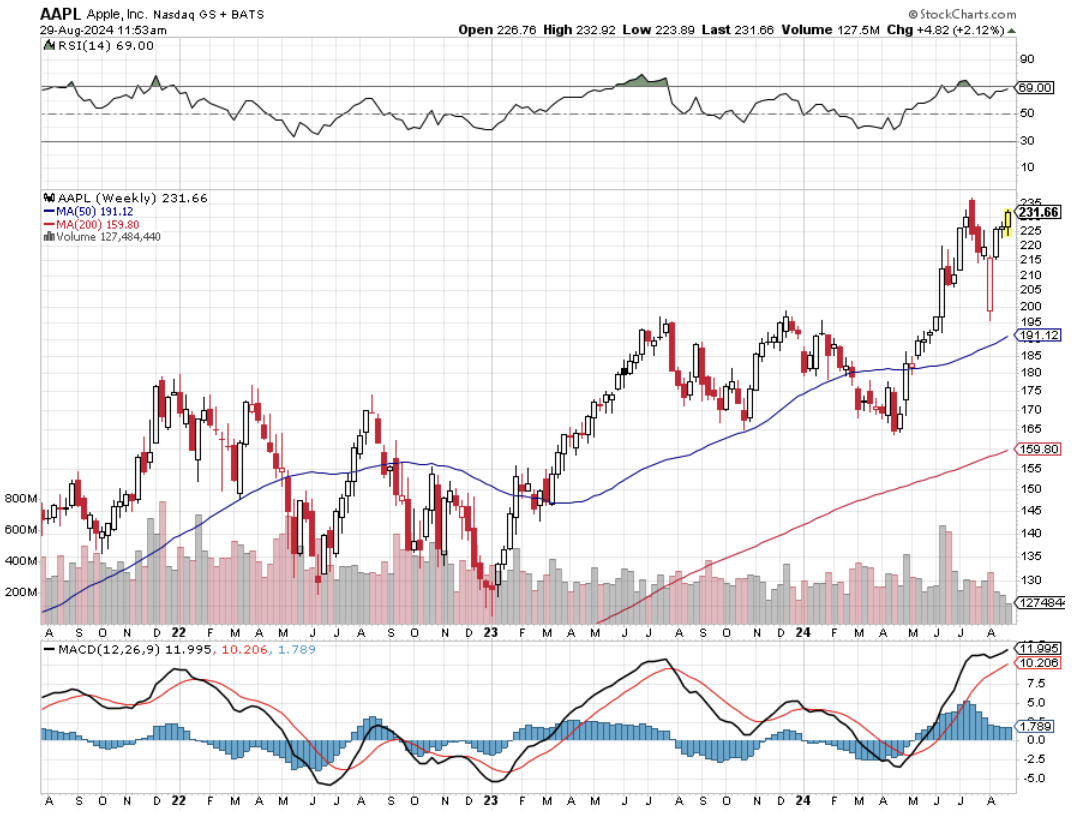

Apple (AAPL) is his second holding, the next AI stock. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 25X over the last several years. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third-party services. The cream on top is that Apple is at the very beginningof an enormous replacement cycle for its installed base of over one billion phones. Moving from up-front sales to a lifetime subscription model will also give it a boost.

Half of these are more than four years old and positively geriatric in the tech world. More than half of these are outside the US. 5G will add a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over-the-top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 21 Emmys this year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world. Tech growth will accelerate in 2021 and 2022.

5G will enable better Internet coverage for everyone and will increase the competitiveness of telecom companies. Factory automation will be another big area for 5G, as it is reliable and secure, and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government-threatened breakups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies of its own, views big American tech companies simply as a source of revenue through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Meta (META) control 70% of the advertising market, which is inherently a slow-growing market, expanding at 5% a year at best. (META)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised the value of tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings it is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract service revenues from their cars, like Apple has. Tesla will grow revenues by 30%-50% a year for the next two or three years. They should sell several million of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. However, interest rates are much lower. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

When rates rise in a year or so tech stocks may have to come down. They have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your shortlist for LEAPS to buy at the coming market bottom.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/09/oakland-fire-dept.png408608april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-29 09:02:202024-08-29 14:30:47Seven Tech Stocks to Buy at the Next Market Bottom

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.