Global Market Comments

March 28, 2019

Fiat Lux

Featured Trade:

(JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 25-26, 2019)

(THE REBIRTH OF THE MASTER LIMITED PARTNERSHIP),

(USO), (AMLP), (FPL), (MLPS), (MLPX)

Global Market Comments

March 28, 2019

Fiat Lux

Featured Trade:

(JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 25-26, 2019)

(THE REBIRTH OF THE MASTER LIMITED PARTNERSHIP),

(USO), (AMLP), (FPL), (MLPS), (MLPX)

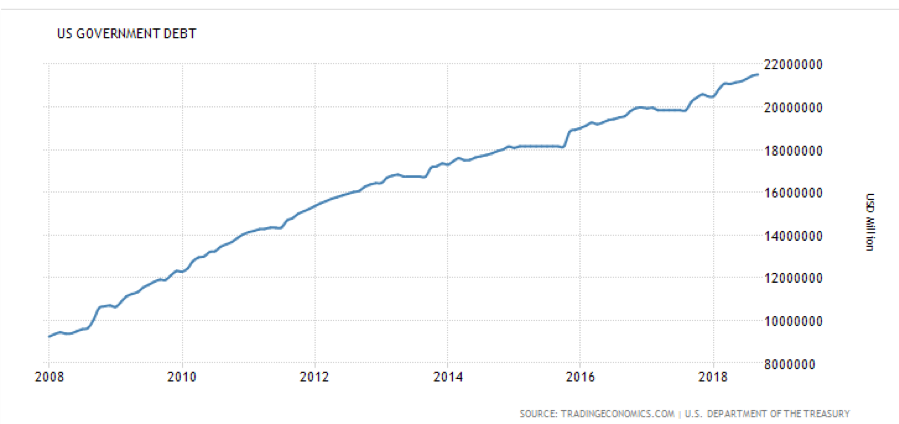

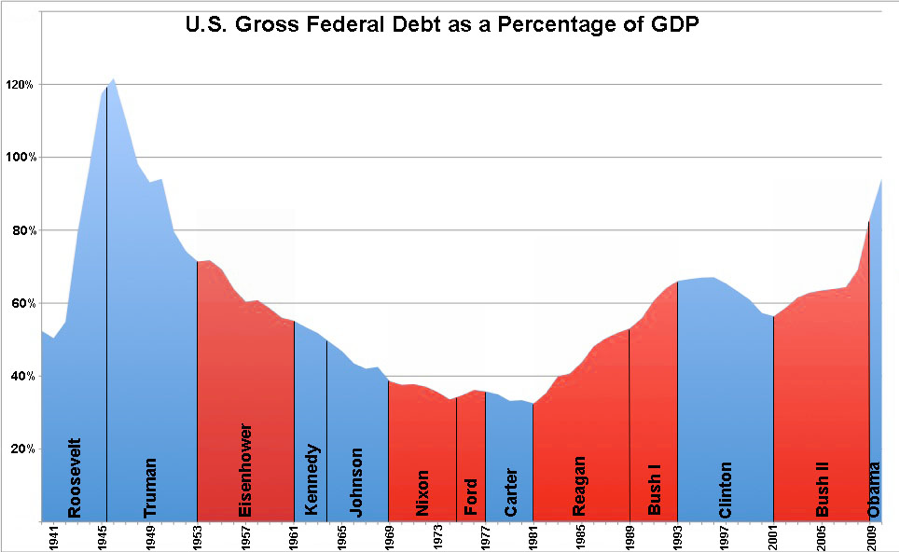

Not a day goes by without someone carping about the national debt to me which now stands at $21.6 trillion.

Since President Obama came into office on January 20, 2010, it skyrocketed.

Are we all going to hell in a handbasket? Eventually, yes.

While it is true that the national debt has increased by some $10 trillion over the past ten years, there is less than meets the eye.

Much less.

That includes the $4 trillion purchased by the Federal Reserve as part of its aggressive five-year monetary policy known as “quantitative easing”.

It also includes another $1 trillion of Treasury holdings by dozens of other federal agencies such as Fannie Mae, Freddie Mac, and Sallie Mae.

So, the net federal debt actually issued during Obama’s two terms is not $9 trillion, but $4 trillion.

That’s a big difference.

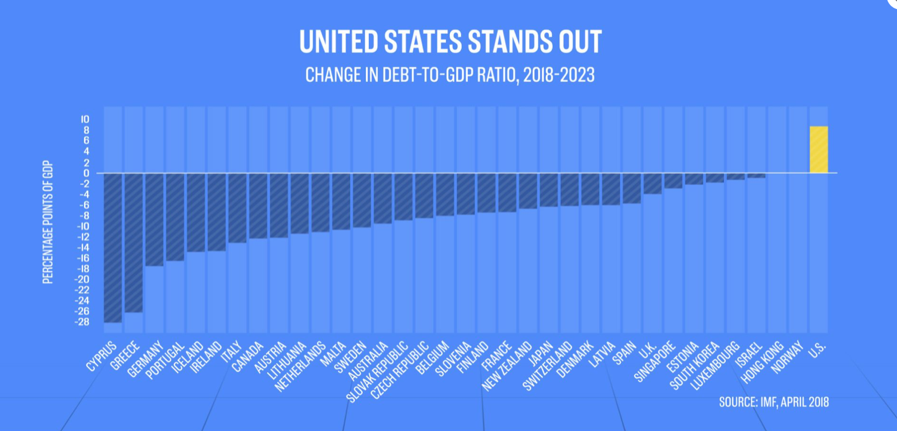

These numbers would make Obama one of the most fiscally conservative presidents in US history (see tables below).

And he pulled off this neat trick despite US tax revenues utterly collapsing in the aftermath of the Great Recession.

What the Treasury has in effect done is taken one dollar out of one pocket and put it in the other, 5 trillion times.

There has been no change in the nation’s true indebtedness or net worth as a result of these transactions.

In fact, these bonds were never even really issued. They only exist on a spreadsheet, on a server, on a mainframe, somewhere at 1500 Pennsylvania Avenue, NW, Washington DC.

And here is the real shocker.

The Treasury can cancel this debt at any time.

They can just decide to use one set of figures on the plus side of the balance sheet to offset an equal amount on the negative side, and poof, the debt is gone forever, and the national debt is suddenly only $16 trillion.

It wouldn’t even require an act of Congress. It could simply be carried out through a presidential order.

And we have seen a lot of those lately.

That would give America one of the lowest debt to GDP ratios in the industrialized world.

I actually recommended that the White House use this ploy to get around the last debt ceiling crisis.

All of this sounds nice in theory. But how would markets respond if this were the true state of affairs in the debt markets?

Ten-year US Treasury bond yields would stay stubbornly low around $3.10%.

Prices for marginal debt securities in emerging markets (ELD) would boom.

Am I ringing any bells here people? Do these sound like debt markets you know and love?

A half-century of trading has taught me to never argue with Mr. Market. He is always right.

By keeping its bonds, the Fed has a valuable tool to employ if it ever senses that real inflation is about to make a comeback without having to raise the overnight deposit rate.

It simply can raise bond market rates by selling some of its still considerable holdings.

“FED SELLS BOND HOARD.”

How do you think risk markets would take that headline? Not well, not well at all.

There are other reasons to keep the $5 trillion in phantom Treasury bonds around.

It assures that the secondary market maintains the breadth and depth to accommodate future large-scale borrowing demanded by another financial crisis, Great Recession, or war.

Yes, believe it or not, governments think like this.

I remember that these were the issues that were discussed the last time closing the bond market was considered.

That was at the end of the Clinton administration in 1999 when paying off the entire national debt was only a few years off.

But close down the bond market and fire the few hundred thousand people who work there, and it could take decades to restart.

This is what Japan learned in the 1960’s.

It took the Japanese nearly a half-century to build the bond infrastructure needed to accommodate their massive borrowings of today.

The Chinese are learning the same thing as they strive to construct modern debt markets from whole cloth. It is not an overnight job.

One of the most common questions I get from foreign governments, institutional investors, and wealthy individuals in my international travels is “What will come of America’s debt problem?”

The answer is easy. It will all go to debt heaven. It will disappear.

US government finances are now worsening at a pretty dramatic pace (see more charts and tables below).

The budget deficit has doubled from the Obama low of $450 billion to $900 billion in only two years. Debt has exceeded GDP for the first time since WWII. New government bond issuance is rocketing and will crush the market any day now.

However, there is a way out of the looming financial disaster.

A massive demographic tailwind kicks in during the 2020s as 85 million Millennials grow up to become big-time taxpayers.

In the meantime, the last of the benefit-hungry baby boomers finally die off, eliminating an enormous fiscal drag.

“Depends” and “Ensure” prices will crater.

The national debt should disappear by 2030, or 2035 at the latest. The same is true for the Social Security deficit. That’s when we next have to consider firing the entire bond market once more.

That is what happened to the gargantuan debt run up by the Great Depression, the Civil War, and the Revolutionary War.

Government debt always goes to debt Heaven either through repayment during the period of demographic expansion and economic strength, or via diminution of purchasing power caused by inflation.

That’s why we have governments to pull forward economic growth during the soft periods in order to even out economic growth and job creation over the very long term to accommodate population growth. Pulling forward growth during strong economies as the administration is now doing only ends in tears.

The French were the first to figure all this out in the 17th century. They were not the last.

History doesn’t repeat itself, but it certainly rhymes.

Global Market Comments

June 8, 2018

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE TUESDAY, JUNE 12, 2018,

NEW ORLEANS, LA, GLOBAL STRATEGY LUNCHEON),

(JUNE 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (TTT), (TBT), (AMLP), (IBB),

(SPY), (SDS), (SH), (GS), (BAC)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader June 6 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: What does the coming Kim Jong-un summit with North Korea mean for the market?

A: It means absolutely nothing for the market. The entire North Korean threat has been wildly exaggerated as a distraction from the chaos in Washington. So, you may get a one- or two-day rally if it's successful. If it's not expect a one- or two-day sell-off, but no more. Whatever North Korea agrees to, we will not see any follow through; they won't buy the Libyan model of denuclearizing North Korea for fear of their leader meeting the same end as Libya's Khadafy (i.e. being hunted and shot in a storm drain.) North Korea will never give up its nuclear weapons.

Q: What do you do at market tops?

A: Well, hopefully if you're reading this letter you're long up the wazoo, so you sell everything you have. Then, wait for a double top in the market (which is clear as day) and falling volume. You start looking at things like the ProShares Ultra Short S&P 500 ETF (SDS). That's the -2X version (there's the (SH), which is the -1X short S&P 500) and you just start buying outright puts on a lot of different things, particularly the overbought sectors of the market, which are generally pretty obvious. It's also good to look for a stock that has made a new high and has negative money flow.

Q: Why are the banks doing so poorly?

A: I believe they fully discounted all of this year's interest rate hikes last year when the stocks nearly doubled. We just talked about a technical setup; Goldman Sachs (GS), Bank of America (BAC), and other stocks had those bear setups. At this point, I believe they're coming down to a place of support and probably getting a decent dead cat bounce. They've had their sell-off, they had their run, and it was triggered by one of the best technical short setup patterns you'll see.

Q: Would you buy financials here?

A: Absolutely not. It's unclear why they're doing so badly, but I would not buy it with anyone's money. Their earnings growth is nowhere what you see with technology stocks.

Q: Is crude oil poised for the next leg up?

A: No, it's not. The oil game may be over if they rush to overproduce once again. It's clearly been artificially boosted to get the Saudi Aramco IPO done. After the end of the quota system, you can get oil back down to the $50s easily. I don't want to touch it here; if anything, I'm more inclined to buy it if we get down to the $50s, which would essentially be the February low.

Q: Is the U.S. dollar overbought here?

A: Yes. The dollar has had a great run all year, which is evident from the rising interest rates. It's done a 10% move up in a fairly short time, which is a lot for the foreign exchange market. It's way overbought; you could easily get a round of profit taking in the dollar, either going into or right after the next Fed interest rate hike in two weeks. I'm staying away from the currencies. There are too many better fish to fry in the equities.

Q: Can you expect Tech to keep going up after this next run?

A: Yes, I expect us to break out to a new high and give back some ground in a retest of the old high. The old high will then hold and then I expect a sort of slow grind up. Tech could well go up for the rest of 2018.

Q: If the S&P 500 is in a trading range, would you sell any rally?

A: Yes, but I'm going to wait for the rally to come to me; I'm not going to reach for any marginal trades. When the (SPY) gets to $280, I'll be looking very closely at the $285-$290 vertical bear put spread one or two months out. So, that peak should hold for the summer and you can make a good 25%-30% on that kind of spread.

Q: Would you buy Biotech here?

A: Yes, the chart setup here is looking very positive, and it's natural for people to rotate out of Tech to Biotech because the earnings growth is so dramatic. That's why I sent out a Trade Alert to buy the NASDAQ Biotechnology ETF (IBB) yesterday. They have been unfairly held back by fears of drug pricing regulation, which has nothing to do with biotech, but it affects their share prices anyway. But so far, it has been all talk from Trump and no action. I think he's busy with North Korea and the trade wars anyway.

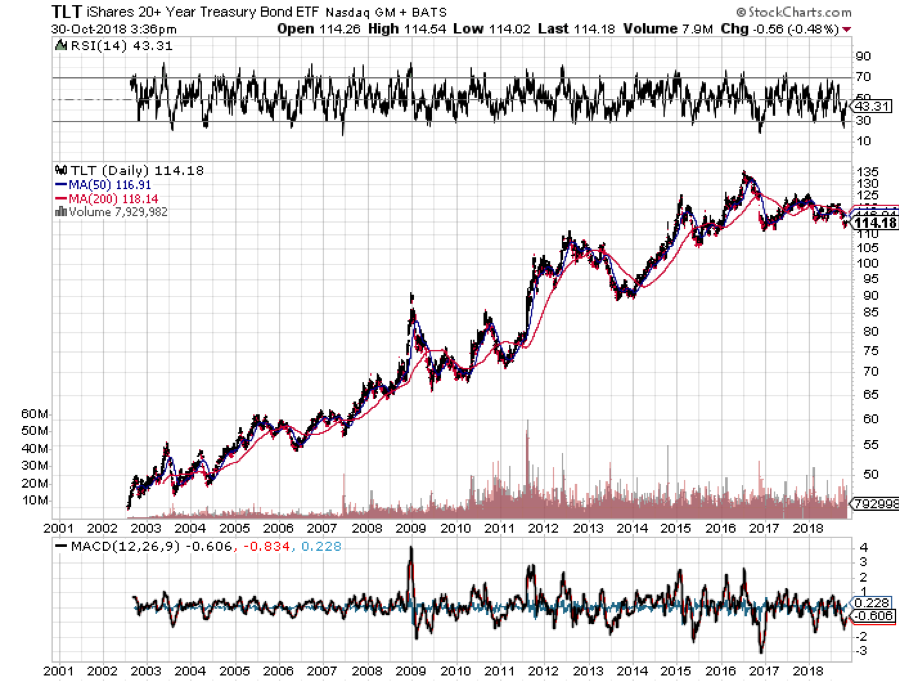

Q: My custodian won't let me sell short the United States Treasury Bond Fund (TLT) so I bought the ProShares Ultra Pro Short 20+ Treasury Fund (TTT). Is that alright?

A: You definitely want to be short the Treasury bonds market for the next several years going forward, so you have the right idea. If the 10-year U.S. Treasury bond yield jumps from 2.95% today to 4% in a year as I expect, that takes the (TLT) down from $119 to $97. If you can't make money shorting bonds in that environment you should consider another line of work.

The problem with these 3X leveraged funds is that the cost of carry is very high. In the case of the (TTT) it is three times the 3.0% 10-year bond coupon you are shorting plus a 1% management fee for a total of 10% a year. For that reason, the 3X funds are really only good for day trading. You run into a similar problem with the 2X (TBT). This is why I use non-leveraged put spreads or outright puts for this asset class.

Q: Why are we seeing strength in the Alerian master limited partnership (AMLP) when oil prices are falling, and interest rates are rising? Shouldn't it be going the other way?

A: How about more buyers than sellers? There are so many retirees out there desperate for yield they will take on inordinate amounts of risk to get it. With an 8.0% dividend yield you always have an underlying bid for this ETF. That's why we have been recommending this since April. An 8% dividend can cover up a lot of sins, even when interest rates are rising and oil prices are falling. Also, the U.S. is infrastructure constrained now that production is approaching 11 million barrels a day. That is great for the kind of energy projects (AMLP) finances.

Q: What's the next support price for NVIDIA (NVDA)?

A: With the stock going straight up there is little need for support. Our 2018 target is $300. If you recall, we have been recommending this cutting-edge GPU manufacturer since $68, and people have made fortunes. Those who bought long dated deep out-of-the-money leaps $100 out made 1,000% on this Trade Alert 18 months ago. That said, the 200-day moving average at $213 looks rock solid.

Good luck and good trading to all.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader