It’s not that they shouldn’t be a company - I’ve seen worse ideas cut up on the drawing board - but I don’t see how they will ever become successful.

They probably should have invested in Bitcoin before it blew up to $65,000 because that was the last savior before tech companies realized they couldn’t just roll over debt anymore.

SFX’s lack of competitive advantage is worrisome, and they haven’t done enough to differentiate themselves amongst competition.

For a company fighting for relevancy, they have made some boneheaded mistakes.

They recent hired a new CEO Elizabeth Spaulding with no apparel experience - she was only a consultant with Bain and has never run a company in her life.

For one, customers don’t receive a great sales price on the clothes. Unless keeping the entire box (5 items), they won't get a discount. They also won't find any coupons online for Stitch Fix.

For many tech companies that preach the freemium model, Stich Fix is asking customers to pay a premium for clothing upfront without proof of a brand premium, and I believe that is turning off a lot of potential customers.

A tech company with decelerating revenue for 6 straight quarters is a red flag.

If you are a bargain bin fanatic, the sight of SFIX’s service will turn you off.

Stitch Fix claims the average price of items is around $70, but that the items can cost anywhere between $20 and $400.

You can set price ranges for each category, but that doesn't mean your stylist will always follow those instructions.

Pigeonholing oneself as a luxury service but hoping to scale broadly and fast like a tech company is counterproductive.

Many Americans simply won’t pay up to $500 for a 5-piece set of clothing no matter who is styling it.

This sounds like a service for a computer programmer in San Francisco with a $200,000 annual salary--which isn’t a bad thing, but it will fail to scale.

Just as important, there is quite robust competition that undercuts SFIX such as Amazon (AMZN) Prime Wardrobe.

Amazon Prime Wardrobe is an exclusive program just for Prime members. This service gives users the chance to have chosen clothing items shipped to their home for them to try on before buying. The difference here is that the user selects the item which, for me at least, makes sense instead of SFIX blindly shipping clothes that aren’t ok’d. I just don’t think a “stylist” can get it right more than half the time. You only pay for what you keep and you have 7 days to make up your mind.

The biggest head scratcher is the $20 SFIX styling fee if you don't keep anything.

Seriously, what is that about?

If you hate their expert stylish decisions, you get blamed for it and pay $20 for nothing! Shouldn’t it be SFIX paying the user $20 for failed style sense?

And this is without even mentioning the pain of resending the clothes!

The inferior business model explains why the stock has gone from $120 fifteen months ago to under $3 per share today.

Don’t bet on a reversion to the mean trade as well, there are so many better stocks out there.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/07/stitch.png9701390Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-28 15:02:062022-12-29 09:40:37Stitched Up By Its Own Poor Decisions

Automation is taking place at warp speed displacing employees from all walks of life.

Next could be you!

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the $250 billion annually that banks spend on technological development in-house which is second highest after the traditional tech giants.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up around 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. banking sector getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

Gutting bank jobs will naturally occur in the call centers first, because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificially engineered algorithm.

The wholesale integration of automating the back-office staff isn’t contained to the rudimentary part of the staff.

The front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

The front-office staff has already felt the brunt of downsizing with purges carried out from 2022 representing a twelfth year of continuous decline.

Front-office traders and brokers are being rapidly replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30% and the accumulation of hordes of data will advance the marketing effort into a potent, multi-pronged, hybrid cloud-based, and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 100,000 employees in 2022.

Even Europe’s banking jewel Credit Suisse is on the brink of collapsing and in need of a bailout.

Don’t tell your kid to get into banking, because they will most likely be feeding on scraps at that point.

An interesting tech stock that integrates financial payments is Square (SQ) which has given back its entire pandemic performance.

As US interest rates are expected to peak and go down in 2023, I recommend dollar cost average into this stock at bargain basement prices.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-21 14:02:452023-01-02 20:08:33Fin-Tech Automation and Banking

Dealing with the Cloud works, and for every relevant tech company, this division serves as the pipeline to the CEO position.

If this isn’t the case for a tech company, then there’s something egregiously wrong with them!

Take Andy Jassy - he is the mastermind behind Amazon’s (AMZN) lucrative cloud computing division and was the man who succeeded company founder Jeff Bezos.

He was rewarded this important position based on his performance in the cloud and faces a daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon almost 30 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Cloud 101

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

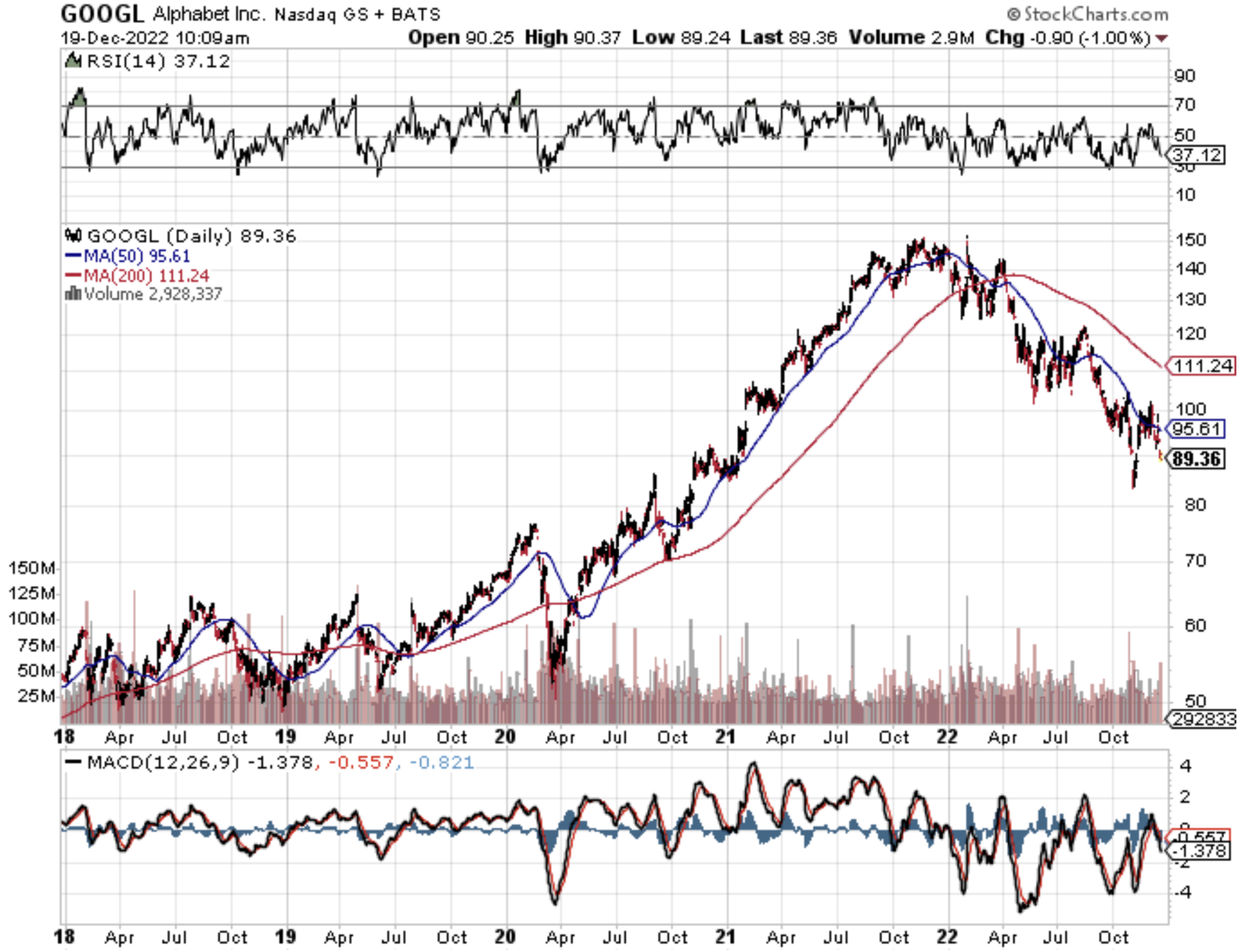

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at anytime from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them working remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

The cloud is where you want to be.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-19 16:02:582023-01-02 16:48:34Go Straight To The Top With The Cloud

We have now collapsed 16% from the January high. Buyers are few and far between, with one day, 5% crashes becoming common.

By comparison, theMad Hedge Fund Trader is up a nosebleed 88.48% during the same period.

The Harder I work, the luckier I get.

Go figure.

It makes you want to throw up your hands in despair and throw your empty beer can at the TV set.

Let me point out a few harsh lessons learned from this most recent meltdown and the rip-your-face-off rally that followed.

Remember all those market gurus claiming stocks would rise every day for the rest of the 2022?

They were wrong.

This is why almost everyTrade Alert I shot out this year have been from the “RISK OFF” side.

“Quantitative Tightening”, or “QT” is definitely not a stock market-friendly environment.

We went into this with big tech leaders, including Apple (AAPL), Amazon (AMZN), Google (GOOG), and Microsoft (MSFT), all at or close to all-time highs.

The other lesson learned this year was the utter uselessness of technical analyses. Usually, these guys are right only 50% of the time. This year, they missed the boat entirely. After perfectly buying the last top, they begged you to dump shares at the bottom.

In 2020, when the S&P 500 (SPY) was meandering in a narrow nine-point range, and the Volatility Index (VIX) hugged the $11-$15 neighborhood, they said this would continue for the rest of the year.

It didn’t.

When the market finally broke down in January, cutting through imaginary support levels like a hot knife through butter ($35,000?, $34,000? $33,000?), they said the market would plunge to $30,000, and possibly as low as $20,000.

It didn’t do that either.

If you believed their hogwash, you lost your shirt.

This is why technical analysis is utterly useless as an investment strategy. How many hedge funds use a pure technical strategy? Absolutely none, as it doesn’t make any money on a stand-alone basis.

At best, it is just one of 100 tools you need to trade the market effectively. The shorter the time frame, the more accurate it becomes.

On an intraday basis, technical analysis is actually quite useful. But I doubt few of you engage in this hopeless persuasion.

This is why I advise portfolio managers and financial advisors to use technical analysis as a means of timing order executions, and nothing more.

Most professionals agree with me.

Technical analysis derives from humans’ preference for looking at pictures instead of engaging in abstract mental processes. A pictureis worth 1,000 words, and probably a lot more.

This is why technical analysis appeals to so many young people entering the market for the first time. Buy a book for $5 on Amazon and you can become a Master of the Universe.

Who can resist that?

The problem is that high-frequency traders also bought that same book from Amazon a long time ago and have designed algorithms to frustrate every move of the technical analyst.

Sorry to be the buzzkill, but that is my take on technical analysis.

Hope you enjoyed your cruise.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/John-Thomas.png391368Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-09 10:02:272022-12-09 11:57:05Why Technical Analysis Never Works

Wage growth is too strong to even think about pivoting – that was the takeaway from the latest jobs report.

Granted, tech firms have been firing employees left and right, but that can be contextually misleading.

Essentially, tech firms overhired during the government lockdowns and in most cases are only now cutting back to a headcount that reflects the same number as around a year or 2 ago.

The sensationalist headlines are riveting, but going two steps forward and one step back isn’t really a big deal.

The overarching theme of wage growth in white collar jobs means that the leftover tech workers are handsomely paid and possess a lot of leverage.

Since 2020, many tech workers jumped ship or were poached for a 50% pay rise.

Those gaudy wages have tapered off somewhat in technology as the sector slows down, but in many cases, workers don’t care if their 2023 salary is “frozen” after a 50% increase the prior year.

In fact, many of the recent tech firings were either the weakest of a specific team or the "last in, first out" type of hire and fire.

Employers added 263,000 jobs in November and the unemployment rate held steady at 3.7%.

For the three months through November, average hourly earnings rose at a 5.8% annualized rate, the Labor Department said Friday.

Strong demand for labor and high inflation is triggering the formation of a wage-price spiral.

To be honest I am not surprised by the most recent data.

A 3.75% Fed Funds rate is still ultra-accommodative.

How do I know that?

Tech firms are still borrowing massive amounts of borrowed funds at cheap rates.

Amazon (AMZN) sold investment-grade bonds for general corporate purposes, its second offering this year.

The bond deal is $8 billion of senior unsecured bonds in as many as five parts.

The longest portion of the offering, a 10-year security, yields 1.15% over US Treasuries.

Big tech is still tapping the debt markets for its operations and it’s the smart thing to do with a Fed Funds rate at 3.75%.

Amazon isn’t the only one.

Essentially, any big tech corporate stalwart with a strong balance sheet would be an idiot not to take out debt at these levels.

The iPhone company Apple also tapped the debt markets just in August.

Apple sold $6.5 billion in four parts as the tech giant increasingly looks to return cash to shareholders.

The longest portion of the offering, a 40-year security yields 0.92% above US Treasuries.

Proceeds from the sale are earmarked for general corporate purposes, including share repurchases, dividend payments, funding for capital expenditures, and acquisitions.

Although I am not privy to discussions at an operations level at Apple and Amazon, I do believe some of these billions will be used to pay staff higher wages which in turn will fuel higher inflation.

It takes money to stay on top and instead of allowing the best talent at Apple and Amazon to walk for bigger raises, firms have been stumping up the cash.

I expect wage growth to continue to exhibit strong numbers in 2023.

Without crushing the jobs market, inflation will regress somewhat but then take off again in the back half of 2023.

It all means we are range bound as we juxtapose slower rate hikes with deteriorating earnings forecasts.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-02 15:02:202022-12-15 00:01:17Accommodating Tech Corporations

I love doing presentations to small businesses in my free time, partly to stay in touch with the pulse of the industry’s minnows that have the unenviable task of fighting uphill against the behemoths.

It’s bad enough that the tech giants have scaled locally turning one’s local playground into a disadvantage.

The presentation is aptly titled "Content is King... But Only Through One’s Ownership" where the same parallels are explored and unpacked for my audience.

Proprietary Content – must be yours and you must own it on your own turf - your blog, your vlog, your app, and so on, it goes for everything.

Repurposing content on other platforms as a supplement to your own is one thing, but the moment you adopt an enemy platform as your main platform, that’s your coup de grâce.

SMEs (small businesses enterprise) believe it’s plausible to work with the higher-ups, but don’t forget the higher-ups have every incentive to cut you off from the fountain of youth.

One could say the best skill big tech has today is undermining its competition.

Facebook doesn’t allow posting content that criticizes Facebook, have you ever wondered why?

Website innovation has ground to a halt because of the PageRank algorithm from Google - everybody is making websites the same, a top nav, descriptive text, a smattering of images, and a handful of other elements arranged similarly.

Google’s algorithms and the self-regulating nature of its ecosystem have perverted the chance to have a unique online experience.

Most internet users have discovered that most websites don’t work well and the execution is lousy.

Silicon Valley now has a monopoly on websites.

Because websites are the key to building businesses, Silicon Valley is now using the concept of websites and their position as de-facto moderators to prevent others from developing proper websites, killing off the competition.

Alphabet is notorious for ranking in-house products at the top of page one of any Google search.

Amazon has followed the same practice by sticking its in-house brands at the top of any Amazon search on Amazon.com.

Websites are used to give businesses a chance.

What’s next?

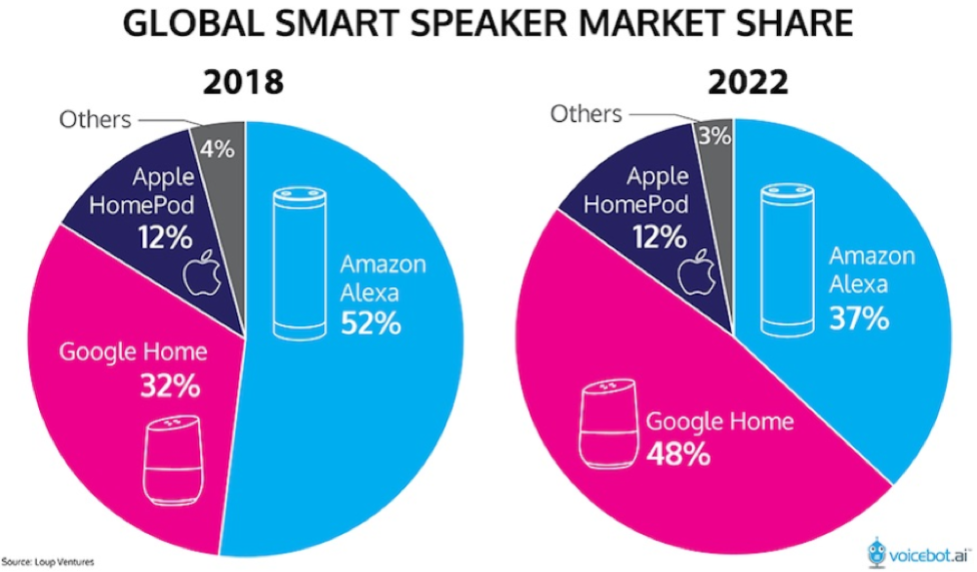

Once we migrate the lion’s share of content to voice platforms over the next 15 years, Google Home, Apple HomePod, or Amazon Alexa could easily choose to remove Joe’s Furniture Moving Business information because they aren’t following arbitrary “policies.”

Big tech will be the gatekeepers of all global information, business, and development in the world and we will need to satisfy their algorithms to get our own content uploaded on their voice platforms.

And because of the nature of voice, users cannot see what else is out there, users will only hear what these companies tell us offering an outsized opportunity to manipulate the user experience generating more dollars for these powerful platforms.

As we inch towards the day the US Central Bank will drop the Federal Funds rate, minus Facebook, readers must load up the truck and pile into these monopolistic tech stocks.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/11/speakers.png485570Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-16 14:02:062022-12-02 03:21:13Content is King

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.