Amazon (AMZN) is invading the healthcare sector, wielding its far-reaching online presence and countless distribution warehouses to dominate the market.

Leveraging its ability to offer quick shipping to practically all locations, Amazon has transformed into a grab-anything-and-everything-possible business.

Now, it has set its sights on the healthcare and prescription sector. In fact, it has been attempting to infiltrate this segment since 2018 when it acquired PillPack.

The only limitation of that deal was that customers still had to get prescriptions from their doctors to avail of the PillPack service.

However, Amazon’s not the only one seeing the potential of this sector.

Following the difficulties it encountered in cornering the market, the e-commerce giant collaborated with fellow Wall Street titans Berkshire Hathaway (BRK.A) (BRK.B) and JPMorgan (JPM). Together, the three companies launched a service they called “Haven.”

Unfortunately, the venture eventually fell apart, and they canceled the deal altogether.

Despite that unfortunate end, Amazon refuses to back down on its vision. Recently, it decided to take another stab at the venture with a rebranding, giving birth to AmazonCare.

The goal is to offer assistance to customers in booking doctor appointments and receiving prescriptions online.

Undeniably, any business endeavor with Amazon’s backing will make waves in any industry. Nonetheless, this new venture could still be a tough sell.

For now, the company's strength is hoping to use the “Amazon effect” to sway members into signing up and using AmazonCare as well.

Surprisingly, Amazon finds itself facing an unlikely challenger in this pursuit: CVS (CVS).

Like Amazon, Berkshire, and JPMorgan, CVS has also recognized the potential of this market.

Unlike Amazon’s partners, CVS has decided to invest to become a frontrunner in terms of dominating the same sector and eventually taking advantage of this rapidly expanding total addressable market.

Instead of following the track of its fellow healthcare providers, such as UnitedHealth (UNH) and Anthem (ANTM), CVS has opted to change its angle of attack in the hopes of gaining more market share and reaping higher profits.

CVS is putting to good use its over 9,900 stores and distributions as means to establish better connections and rapport with customers.

After all, statistics indicate that approximately 80% of American citizens live less than 10 miles from a CVS branch.

This offers CVS a competitive advantage in terms of proximity to its customers. That is, it offers a unique convenience as it serves as the ever-present “corner stores” in practically every city.

Leveraging the locations, CVS has set up about 1,500 branches into “HealthHubs” by the end of 2021.

Basically, HealthHubs serve as emergency care clinics found inside CVS stores, providing customers with easy access to convenient and even cheaper after-hours health checkups.

Aside from this feature, a growing number of CVS stores are starting to get set up to be able to ship medicines or any other products ordered online, while other branches are being eyed as potential UPS drop-off points.

This setup will transform several branches into convenient “mini” distribution centers.

CVS has broken out of its “boring corner drugstore” image following its decision to target a more lucrative and massive healthcare sector.

It started the ball rolling when it acquired Aetna for $69 billion—a decision that so many investors disapproved of at that time.

Until recently, the market has largely ignored CVS because of the debt it incurred from the Aetna deal.

However, the tides had turned when investors finally realized that the drugstore giant had been efficiently and effectively executing a brilliant strategy all this time.

With Aetna under its wing, CVS has been granted access to a multitude of healthcare and managed care benefits availed by more than 23 million members. The sheer number of subscribers transformed the company into the third-biggest health insurer in the United States—next only to decades-long established providers Anthem and UnitedHealth.

Riding this momentum, CVS has been aggressive in revamping its image and expanding its services.

This is another massive market since CVS already has roughly 35 million digital customers subscribed to its CVS app.

These users are all ordering products and other prescriptions from CVS. Integrating Teladoc’s services to the mix would be a surefire way of boosting its membership and adding a lucrative revenue stream.

Keep in mind that the global market for telehealth services is projected to expand somewhere between $300 billion to $700 billion by 2028—and that’s a conservative estimate.

Overall, CVS can only be described as a company striving to become a unique business that offers a range of products that no one else in the industry provides.

Although it’s improbable that it’ll sustain a monopoly in these services, CVS has been gradually transforming and growing into an almost unbeatable force in the industry by leveraging its strengths in an effective and logical method.

Moreover, it has evolved from a stodgy drugstore into an early tech adopter and a revolutionary business that can stand to challenge the likes of Amazon.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-03 19:00:022022-02-15 22:41:17A 'Boring' Business Resisting the 'Amazon Effect'

The 14% selloff year to date in tech shares finally met its match when Microsoft (MSFT) soothed us with its most recent quarterly performance.

It’s starting to feel like a broken record, but this world belongs to 5 large Silicon Valley tech companies and for the rest of the other few hundred publicly listed companies, we are just living in their world.

And it just so happens that if anybody or anyone is anointed as the savior to save this market from capitulating, it has to be the heavy lifters and we are getting validation from the strongest of cloud/enterprise companies.

Just as resonating, MSFTs positive quarter draws yet one more line in the sand for Mr. Market, offering us support and offering us evidence this could morph into a short-term bottom.

Even more salient, this is even deeper evidence that the software sector is the cream of the crop in tech and their strategic position is only getting stronger.

The thing that these guys have that is critical in today’s economic environment is tinged with inflation headwinds — pricing power.

Starting in March, Microsoft is pushing through an MSFT 365 price hike and consumers and businesses will see their monthly bill go up a few bucks.

According to Microsoft, those increases will apply globally with local market adjustments for certain regions.

And it’s not that 365 is MSFT's cutting edge division, it’s just another example of how MSFT can raise prices and consumers have no other choice but to comply because, at this point, 365 is a utility.

Sure, you can find a substitute, but it wouldn’t be as good of a product.

It was a record quarter, driven by the continued strength of the Microsoft Cloud, which surpassed $22 billion in revenue, up 32% year over year. We are living through a generational shift in our economy and society. Digital technology is the most malleable resource at the world's disposal to overcome constraints and reimagine everyday work and life.

Anyone who bet the ranch on the cloud and enterprise is happy they bet the ranch on it.

MSFT's earnings were just a giant confirmation of how tech won’t be knocked off its perch as the apex warrior, not only in the Nasdaq index but the broader market.

The stock market has been a tech market for quite a few years and that can’t be ignored or discounted.

Fundamentally, the foundations of profitable tech stocks have never been healthier, and they are extracting more of the pie than ever.

Then as we hear nonstop about the upcoming metaverse project and its entryways through gaming, MSFT is so on top of that new development that they will put all other companies to shame.

Granted, there are other heavyweights like Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL) that MSFT must take measures of to see if they are pushing ahead with something they are unaware of, but all is good is Redmond, Washington.

As data volumes and transactions increased over 100% year over year, MSFT has a grip on what’s going on and can quickly pivot to anything that’s worth it with its army of high-quality developers.

MSFT’s ubiquitous fingerprints are everywhere with even over 90% of Fortune 500 companies using Teams Phone this past quarter highlighting the deep penetration into the richest corners of corporate America.

My overarching point is that MSFTs products aren’t just a one-trick pony ala Facebook.

More than half of customers have four or more MSFT workloads, up 75% year over year, underscoring MSFTs end-to-end differentiation.

On a short-term trading basis, traders must adopt tech winners with robust balance sheets, and this must be looked at as a dealbreaker or deal winner of sorts.

In a world that is clamoring for quality tech names, it’s no time to allocate your hard-earned savings into Podunk technology.

Once the macro washout fades, pile into MSFT!

What I am saying is that there is a great deal of the market to plain out avoid, and don’t get caught up in those lemons.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-26 16:02:342022-01-30 00:40:29MSFT Digs Us Out of a Hole

Popular nostrum has it that earnings will save the stock market.

The strength of corporate America time and time again is on display to show investors how high short-term growth follows through.

Anytime the Nasdaq enters a little rut, earnings bail us out and the next move is usually higher for tech shares.

Well, wait a second, things are different this time.

The bad news now is that confirmation of solid fundamentals during the upcoming earnings season, won’t make the Nasdaq index go higher.

The market is pricing in business as usually for the largest 5 tech stocks which are really the only ones that matter.

Internally, the rest of tech has been deeply damaged by this January sell-off and we are talking about 8-9% one-day sell-offs for the small cap tech growth and I haven’t even mentioned the peak to trough underperformance which is much worse.

Larger cap Enterprise and Cyber Security stocks still boast solid foundations and are going down less than the meme stocks, shelter-at-home stocks, and the best of the rest tech stocks.

Basically, we need to get through earnings because there is minimal upside for tech stocks as investors peruse through a lack of short-term catalysts.

We are stuck in a ditch where monetary and fiscal policy has been set dead straight against an environment of potentially appreciating tech stocks.

Until that changes, I don’t envision a snappy reversal apart from a dead cat bounce to sell into.

Chasing growth in a low-interest rate environment gave us an overshoot to the upside and now that is all working in reverse.

And for the big FANG stocks outperforming small cap, it just means shares are performing better than tech growth because they command lower volatility due to stronger balance sheets.

Resilience to indiscriminate selling is currency in today’s trading world.

Nothing wrong with growth, but they are what they are, so much so that if you cannot generate profitability now, sell-offs are indicative of their poor strategic position among bigger tech.

The carnage under the hood is stark today with Snap stock cratering after the social media company’s shares were downgraded amid risks to revenue growth and tough competition from rival TikTok.

Snap’s headwinds result from a weakening business profile stemming from IDFA headwinds, difficult [year-over-year comparisons] from stellar growth in 2020-21, and increasing competition from TikTok.

IDFA is a serious thorn in the side for the android-based systems of Google as well as for Facebook.

IDFA is Apple minimizing the reach of data harvesting platforms by turning off their data reach and these modifications by Apple (AAPL) to rules for advertising on mobile apps have forced companies like Snap to lower guidance.

When it reported quarterly earnings last October, Snap revealed that the impact on its advertising business could be long lasting and now we are experiencing that.

The IDFA issues could cut growth rates by half as these social media firms have been unable to remedy its loss of reach in digital advertising.

Snap has the unenviable position to not only be behind Google and Facebook, but they are also the next company to be upended by TikTok that has really come on the last few years.

TikTok has supplanted Snap as the go-to social media platform for teens and young adults.

In a rising interest rate environment, the best of the rest like Snap gets punished for not being the best of class.

Snap shares are down over 200% from its peak and threatening to close in on 300% in the red.

Snap represents the fortunes for the marginal tech stocks that rely on growth and that is not working in 2022.

Although not as loss-making as other tech growth, SNAP has been fairly pigeonholed as the tech you don’t want to own now.

It’s a dangerous position to fill in times of the VIX spiking to 30.

The problems don’t stop there with TikTok really threatening Snap’s position and the momentum signaling that Snap is prepared for a deeper slowdown than initially expected.

Snap’s foothold is strongest in the 13-34-year-old range in the U.S., Canada, the U.K., France, Australia, and the Netherlands, but TikTok’s audience is the most similar to Snap’s which means it puts both Snap’s user face time spent and ad dollars at risk.

From a monetary standpoint, digital advertisers will start to play off ad competition between TikTok and Snap, resulting in discounted ad revenue per unit which will narrow margins moving forward.

Not being able to command the prior ad premium is a stinging blow to Snap who thought they were in the driving seat to the third position behind Google and Facebook, but it shows that being a tech minnow is a harrowing experience and fending off toxicity is part of the playbook just to survive.

Head to higher waters in this volatile environment.

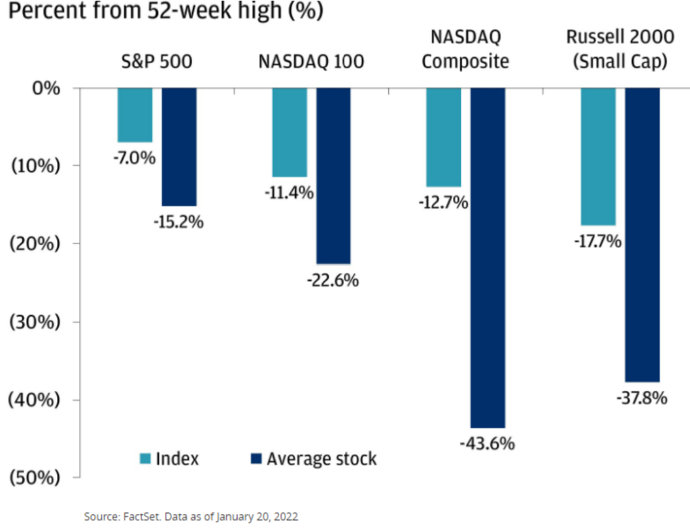

https://www.madhedgefundtrader.com/wp-content/uploads/2022/01/percent-52weeks.png528690Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-24 15:02:442022-01-29 01:13:22Best of the Rest Gets Slaughtered

(MARKET OUTLOOK FOR THE WEEK AHEAD, or PARACHUTING WITHOUT A PARACHUTE), (AAPL), (SPY), (MSFT), (TLT), (TBT), (TDOC), (NFLX), (DIS), (VALE), (FCX), (USO), (JPM), (WFC), (BAC), (TSLA), (AMZN), (NVDA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-24 09:04:462022-01-24 16:50:43January 24, 2022

It has been the worst New Year stock market opening in history.

After a two-day fake-out to the upside, stocks rolled over like the Bismarck and never looked up. NASDAQ did its best interpretation of flunking parachute school without a parachute, posting the worst month since 2008.

Markets can’t hold on to any rally longer than nanoseconds, and the last hour of the day has turned into one from hell.

What is even more confusing is that stocks are now trading like commodities, with massive one-way moves, while commodities, like oil (USO), copper( FCX), and iron ore (VALE) have resumed a steady grind up.

We had a lovefest going on here at Incline Village, Nevada for Technology and Bitcoin researcher Arthur Henry has been staying with me for the week to plot market strategy.

Once the market showed its hand, I sold short Microsoft (MSFT), which elicited torrents of complaints from readers. Then Arthur sold short Netflix (NFLX), inviting refund demands. Then I sold short Apple (AAPL), prompting accusations of high treason. Then Arthur sold short Teledoc (TDOC). There wasn’t a lot of talking, but frenetic writing and emailing instead.

Followers cried all the way to the bank.

In a mere two weeks, the price earnings multiple for the S&P 500 plunged from 22X to 20X. A lot of traders were only buying stock because they were going up. Take out the “up” and Houston we have a problem.

The entire streaming industry seems to have gone up in smoke and ex-growth practically overnight. Netflix (NFLX) delivered a gob smacking 29.5% swan dive in the wake of disappointing subscriber growth forecasts. Walt Disney (DIS), which ate the Netflix lunch, was dragged down 10% through guilt by association.

It is often said that the stock market has discounted 12 of the last six recessions. It is currently pricing in one of those non-recessions. What we are seeing is a sudden growth scare of the first order.

Despite last week’s carnage, stocks are still the most attractive asset class in the world, offering a potential 10% return in 2022. The problem is that they may make that 10% profit starting from 10% lower than here.

Despite all the red ink, big tech stocks are still on track to see a 30% earnings growth this year, and they account for a hefty 28% of the market.

Let’s look at Apple’s past declines for guidance on this meltdown.

Steve Jobs’ creation gave back 60% in the 2008 Great Recession, 34% during the 2015 growth scare, 48% during the great 2018 Christmas collapse, and 28% in the 2020 pandemic crash. So, the good news is that you won’t get killed by this selloff, you’ll just lose an arm and a leg. But they’ll grow back.

Remember, it’s always darkest just before it goes completely black. This correction is survivable, although it may not seem so at the moment.

It does vindicate my 2022 view that the first half will be about survival and that big money can be had in the second half.

So far, so good.

The Market is De-Grossing Big Time. That means cutting total market exposure and selling everything, regardless of stock or sector. The market is discounting a recession and bear market that isn’t going to happen, which occurs often. When it ends in a few weeks, interest rate sensitives, especially the banks, will bounce back hard, but tech won’t. Buy (JPM), (WFC), and (BAC) on bigger dips.

The Bond Collapse Goes Global, with German 10-year bunds going positive for the first time in three years, up 40 basis points in a month. Yes, inflation is finally hitting the Fatherland, home of post-WWI billion percent inflation. Eurozone inflation just topped 5%, well above its 2% target. British inflation hit a 30-year high. The move has lit a fire under all Euro currencies. Methinks the down move in (TLT) has more to go.

Fed to Raise Rates Eight Times, says Marathon Asset Management. That’s what will be needed to curb the current runaway inflation now at 7.0% and still rising. Personally, I think it will be 12 quarter-point increments to peak out at a 3 ¼% overnight rate. Any more and Powell might bring on a recession.

NASDAQ is Officially in Correction, down 10%, in the wake of poor performance this month. It’s the fourth one since the pandemic began two years ago. Tesla (TSLA), Amazon (AMZN), and NVIDIA (NVDA) have been leading the swan dive, all felled by rapidly rising interest rates. This could go on for months.

Weekly Jobless Claims Hit 286,000, a four-month high, as omicron sends workers fleeing home.

Goldman Sachs (GS) Gets Crushed, down 8%, on disappointing earnings. Tough market conditions are fading trading volumes while 2021 bonuses were through the roof. The move is particularly harsh in that buyers were flooding in right at support at the 200-day moving average.

China GDP (FXI) Grows 8.1% YOY but is rapidly slowing now, thanks to Omicron. China was first in and first out with the pandemic but is getting hit much harder in this round. That has prompted new mass lockdowns which will make out own supply chain problems worse for longer. In Chinese, “lockdown” means they weld your door shut, unlike here. Harsh, but it works.

Oil (USO) Hits Seven-Year High, as inventories hit a 21-year low. No new capital is entering the industry, crimping supplies as old fields play out. The threat of a Russian invasion of the Ukraine is prompting advance stockpiling. Russia is the world’s second-largest oil exporter.

Existing Homes Sales Hit a 15-Year High, at 6.12 million, the best since 2006. December fell 4.6%. Extreme inventory shortage is the issue, with only 910,000 homes for sale at the end of the year, an incredibly low 1.8-month supply. You can’t find anything on the market now, to buy or rent. The median price of a home sold in December was $358,000, a 15.8% gain YOY.

Bitcoin (BITO) Crashes, decisively breaking key support at $40,000. Non-yielding assets of every description are getting wiped. Bail on all crypto options plays asap.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my January month-to-date performance bounced back hard to 5.05%. My 2022 year-to-date performance also ended at 5.05%. The Dow Average is down -6.12% so far in 2022.

Once stocks went into free fall, I piled on the short positions as fast as I could write the trade alerts, including in Microsoft (MSFT), Apple (AAPL), and a double short in the S&P 500 (SPY). I also increased my shorts in the bond market (TLT) to a triple position. When prices became the most extreme, when the Volatility Index (VIX) hit $30, I bought both (SPY) and (TLT).

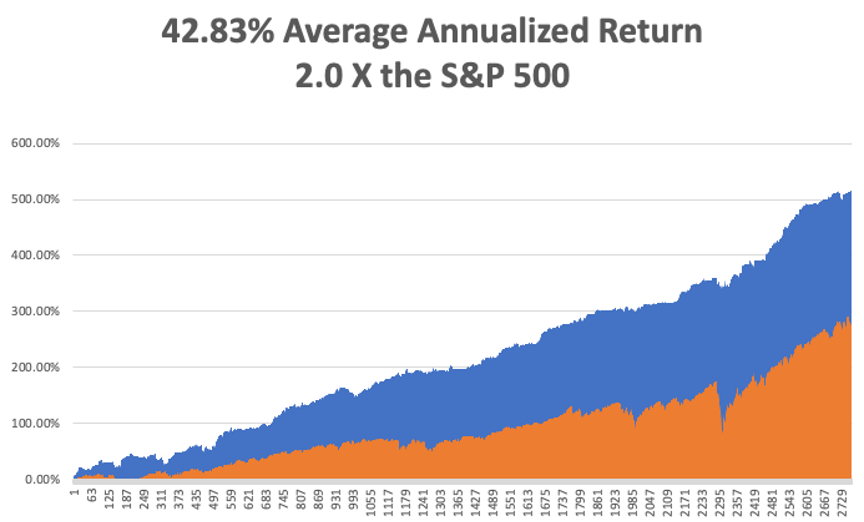

If everything goes our way, we should be up 14.26% by the February 18 options expiration.

That brings my 12-year total return to 517.61%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.82% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 71 million and rising quickly and deaths topping 866,000, which you can find here.

On Monday, January 24 at 6:45 AM, The Market Composite Flash PMI for January is out. Haliburton (HAL) reports.

On Tuesday, January 25 at 6:00 AM, the S&P Case Shiller National Home Price Index for November is released. American Express (AXP) reports.

On Wednesday, January 26 at 7:00 AM, the New Home Sales for December are published. At 11:00 AM The Federal Reserve interest rate decision is announced. Tesla (TSLA), Boeing (BA), and Freeport McMoRan (FCX) report.

On Thursday, January 27 at 8:30 AM the Weekly Jobless Claims are disclosed. We also get the first look at US Q4 GDP. Alaska Air (ALK) and US Steel (X) report.

On Friday, January 28 at 5:30 AM EST US Personal Income & Spending is printed. Caterpillar (CAT) reports. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I drove up to visit my pharmacist in Incline Village, Nevada, I warned him in advance that I had a question he never heard before: How good is 80-year-old morphine?

He stood back and eyed me suspiciously. Then I explained in detail.

Two years ago, I led an expedition to the South Pacific Solomon Island of Guadalcanal for the US Marine Corps Historical Division (click here for the link). My mission was to recover physical remains and dog tags from the missing-in-action there from the epic 1942 battle.

Between 1942 and 1944, nearly four hundred Marines vanished in the jungles, seas, and skies of Guadalcanal. They were the victims of enemy ambushes and friendly fire, hard fighting, malaria, dysentery, and poor planning.

They were buried in field graves, in cemeteries as unknowns, if not at all left out in the open where they fell. They were classified as “missing,” as “not recovered,” as “presumed dead.”

I managed to accomplish this by hiring an army of kids who knew where the most productive battlefields were, offering a reward of $10 a dog tag, a king's ransom in one of the poorest countries in the world. I recovered about 30 rusted, barely legible oval steel tags.

They also brought me unexploded Japanese hand grenades (please don’t drop), live mortar shells, lots of US 50 caliber and Japanese 7.7 mm Arisaka ammo, and the odd human jawbone, nationality undetermined.

I also chased down a lot of rumors.

There was said to be a fully intact Japanese zero fighter in flying condition hidden in a container at the port for sale to the highest bidder. No luck there.

There was also a just discovered intact B-17 Flying Fortress bomber that crash-landed on a mountain peak with a crew of 11. But that required a four-hour mosquito-infested jungle climb and I figured it wasn’t worth the malaria.

Then, one kid said he knows the location of a Japanese hospital. He led me down a steep, crumbling coral ravine, up a canyon and into a dark cave. And there it was, a Japanese field hospital untouched since the day it was abandoned in 1943.

The skeletons of Japanese soldiers in decayed but full uniform laid in cots where they died. There was a pile of skeletons in the back of the cave. Rusted bottles of Japanese drugs were strewn about, and yellowed glass sachets of morphine were scattered everywhere. I slowly backed out, fearing a cave-in.

It was creepy.

I sent my finds to the Marine Corps at Quantico, Virginia, who traced and returned them to the families. Often the survivors were the children or even grandchildren of the MIAs. What came back were stories of pain and loss that had finally reached closure after eight decades.

Wandering about the island, I often ran into Japanese groups with the same goals as mine. My Japanese is still fluent enough to carry on a decent friendly conversation with the grandchildren of their veterans. It turned out I knew far more about their loved ones than they. After all, it was our side that wrote the history. They were very grateful.

How many MIAs were they looking for? 30,000! Every year, they found hundreds of skeletons, cremated in a ceremony, one of which I was invited to. The ashes were returned to giant bronze urns at Yasakuni Ginja in Tokyo, the final resting place of hundreds of thousands of their own.

My pharmacist friend thought the morphine I discovered had lost half of its potency. Would he take it himself? No way!

As for me, I was a lucky one. My dad made it back from Guadalcanal, although the malaria and post-traumatic stress bothered him for years. And you never wanted to get in a fight with him….ever.

I can work here and make money in the stock market all day long. But my efforts on Guadalcanal were infinitely more rewarding. I’ll be going back as soon as the pandemic ends, now that I know where to look.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

True MIAs, the Ultimate Sacrifice

My Collection of Dog Tags and Morphine

My Army of Scavengers

Dad on Guadalcanal (lower right)

https://www.madhedgefundtrader.com/wp-content/uploads/2022/01/dog-tags-morphine.png428570Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-24 09:02:122022-01-24 16:51:22The Market Outlook for the Week Ahead, or Parachuting Without a Parachute

Tech has led the way to the downside as the macro picture sours in the short term.

Valuations have come down from the nosebleed levels and now is the time to pick and choose where to allocate capital for the next leg up in tech.

Avoiding growth tech is something that should be stapled to your bedpost, loss-making companies won’t be able to compete with more established revenue models.

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Here are the names of five of the best stocks to slip into your portfolio in no particular order when we find a bottom.

Remember, tech ALWAYS comes back.

Apple

Steve Job’s creation is weathering the gale-force storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software service tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $200 billion in shares by the end of 2021. Get into this stock while you can, as entry points are few and far between.

Oh, and their 5G phone is selling like hotcakes. Some one billion need to be replaced to bring consumers into the new high speed 5G world.

Amazon (AMZN)

This is the best company in America, hands down, and commands 5% of total American retail sales or 49% of American e-commerce sales. The pandemic has vastly accelerated the growth of their business.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then, oozing innovation, and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2021 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter -- and that is a good thing.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies, especially retailers.

Microsoft is also on the vanguard of the gaming industry and deals like the $86 billion purchase of Activision (ATVI) mean that it will be difficult for another company to loosen MSFTs stranglehold at the top of the gaming ladder.

Alphabet (GOOGL)

Alphabet and Facebook boast a strong duopoly of ad technology. Alphabet generated 80% of its revenue from Google's advertising services in 2020. Google's non-advertising businesses (including subscriptions and hardware) accounted for 12%, while another 7% came from Google Cloud.

Alphabet's total revenue rose 13% in 2020, even as the pandemic throttled the growth of Google's advertising business in the first half of the year. The growth of Google Cloud throughout the year also cushioned that blow.

Google's advertising business recovered in the second half of the year, and Alphabet's operating margin expanded from 21% in 2019 to 23% in 2020. Its diluted earnings per share (EPS) also grew 19%.

In the first nine months of 2021, Alphabet's revenue rose 45% year over year as Google's advertising and cloud business grew in tandem.

Its array of different businesses like LinkedIn, YouTube, and Google Maps means this revenue pipeline is as fertile as can be.

Google’s robust balance sheet will protect itself from any downtrend in business that they might ever suffer.

Tesla (TSLA)

The influential EV leader has really surged ahead of the competition during the pandemic.

Demand for its product is off the charts as they delivered 184,800 Model 3 and Model Y cars in the first quarter, beating expectations and setting a record for Tesla.

However, the company also said it produced none of its higher-end Model S sedans or Model X SUVs for the period ending March. It delivered 2,020 older Model S sedans and Model X SUVs from inventory.

Supply chain issues are likely to remain a challenge for Tesla this year as many EV makers are having a hard time sourcing semiconductor chips.

Tesla is now aiming to produce 2,000 Model S and X vehicles per week later this year.

The company said Monday it expects more than 50% vehicle delivery growth in 2021 overall, which implies minimum deliveries of around 750,000 vehicles this year.

This stock is a must-buy when tech reverses.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-21 14:02:342022-01-28 23:41:59Five Tech Stocks to Lap Up at the Bottom

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-19 15:04:062022-01-19 16:22:47January 19, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.