(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or MY LONG COMMUTE), (SPY), (TLT), (QQQ), (IWM), (AAPL), (AXP), (BAC), (KO), (CVX), (BRK/B), (XOM), (SLB), (NFLX), (NVDA), (AMD), (MU), (INTC), ($VIX), (GOOGL), (AAPL), (TSLA), (XLP), (XLI)

Below please find subscribers’ Q&A for the January 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Sarasota, Florida.

Q:What would I recommend right now for my top five stocks?

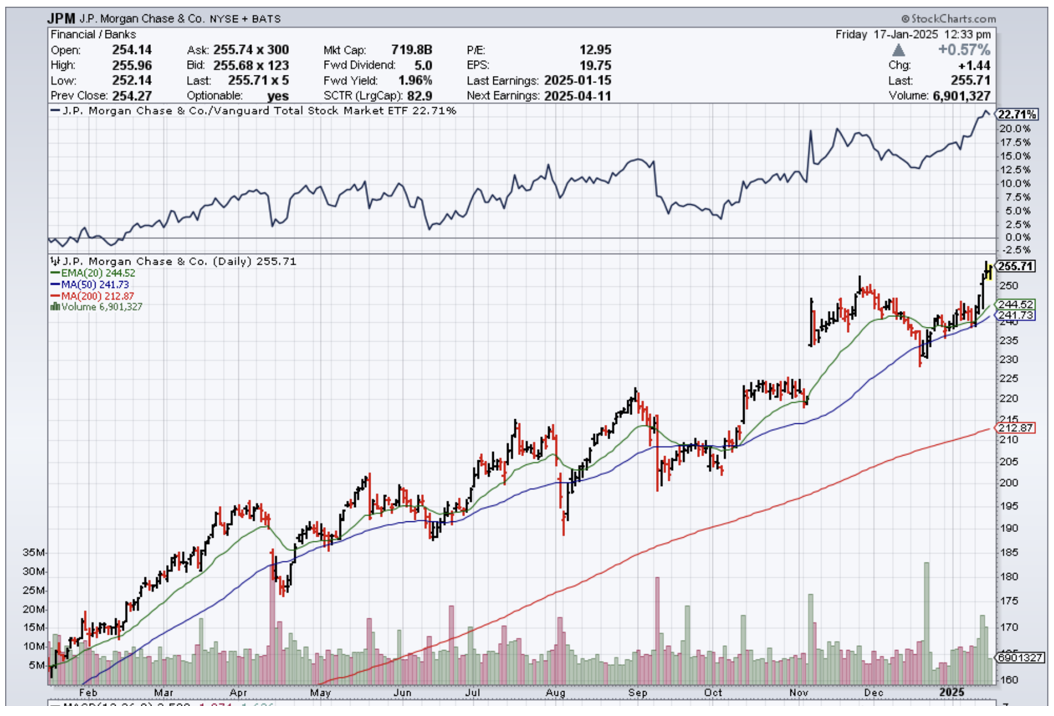

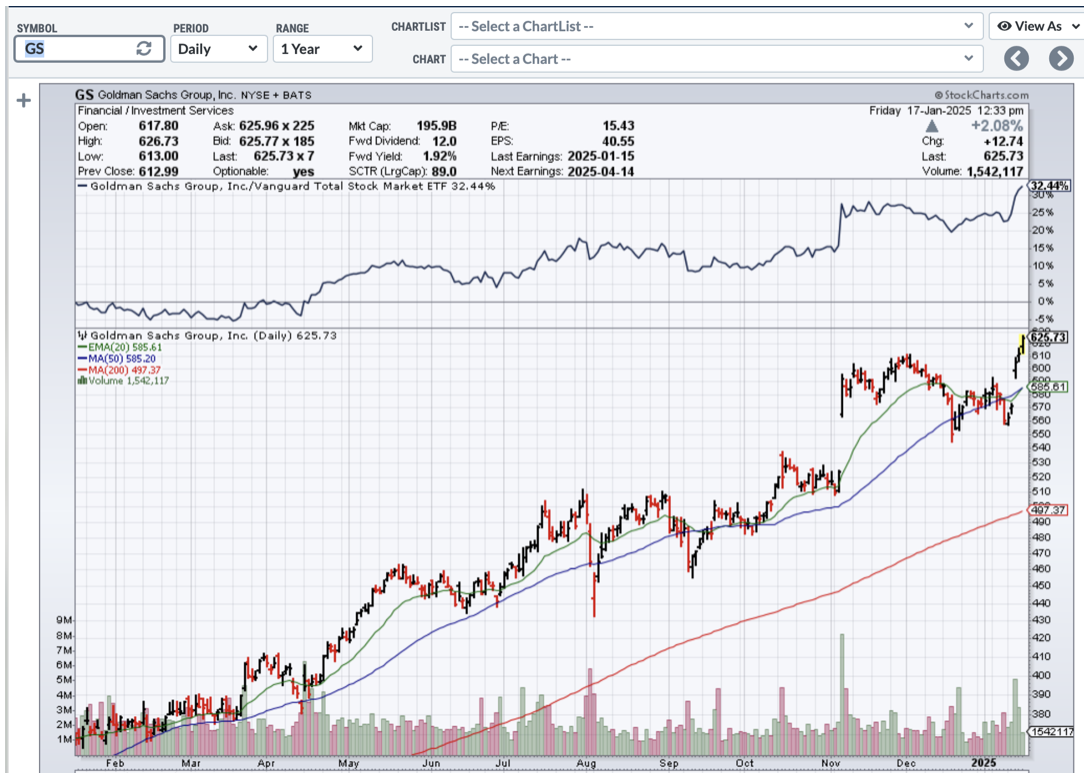

A: That’s easy. Goldman Sachs (GS), Morgan Stanley (MS), JP Morgan (JPM), Citibank (C), and Bank of America (BAC). There's five right there—the top five financials that are coming out of a decade-long undervaluation. A lot of the regional banks, which are also viable, are still trading to discount the book value, which all the financials used to trade out only a couple of years ago. Of course, JP Morgan's reaching a two-year return of around double, but the news just keeps getting better and better, so buy the dips. Buy every sell-off in financials and you will be a happy camper for the year.

Q: What do you think about Robin Hood (HOOD)?

A: Well, the trouble with Robinhood is it’s very highly dependent on crypto volumes. If you think crypto is going to go higher and volumes will increase, this is a great play. However, you get another 95%, out-of-the-blue selloff in crypto like we had three years ago and Coinbase (COIN) will follow it right back down again. On the last downturn, there were concerns that Coinbase would go under, so if you can hack the volatility, take a shot, but not with my money. I have the largest banks in the country that are about to double again; I would much rather be buying LEAPS in that area and getting anywhere from 100% to 1000% percent returns on a 2-year view—much more attractive risk-reward for me. And they pay a dividend.

Q: How do you define a 5% correction?

A: Well, if you have a $100 stock and it drops $5, that is a 5% correction.

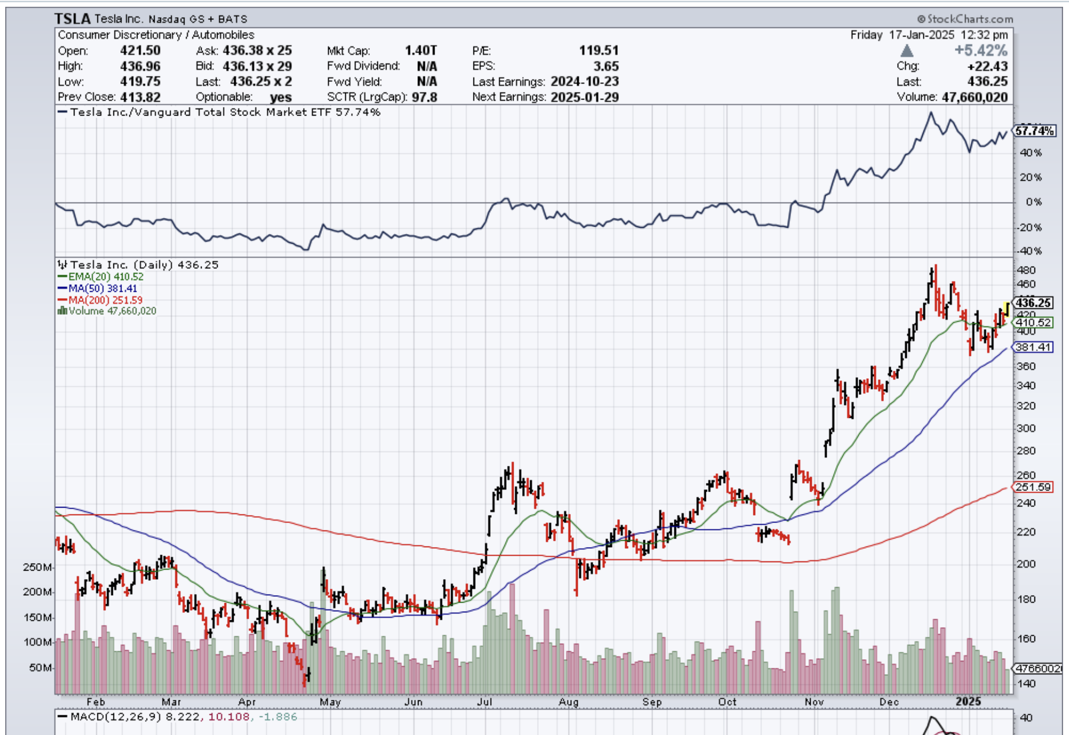

Q: Can you please explain what Tesla 2X leverage actually means and is it a way to trade Tesla as an alternative?

A: I steer people away from the 2Xs because the tracking error is really quite poor. You only get 1.5% of the upside, but 2.5 times the downside over time. These are more day trading vehicles. They take out huge fees, and huge dealing spreads—it's a very expensive way to trade. Far cheaper is just to buy Tesla (TSLA) stock on margin at 2 to 1, and there your tracking error is perfect, your fees are much lower, and you just have the margin interest rate to pay on the position, which is 6% a year or 50 basis points a month. No reason to make the ETF people richer than they already are. They keep coining these products—1x, 2x, 3x long shorts on every one of the high volume stocks, and it sucks a lot of people in, but it's higher risk, lower returns for the amount of money you're risking as far as I'm concerned. So that's the way to do it.

Q: What are your projections for Nvidia (NVDA)?

A: I think not just Nvidia, but all of the big tech is going to be kind of trading in a sideways range for a while, maybe 6 months, and then we get an upside breakout if you get the earnings breakout, which we are all expecting. AI is still in business, and still growing gangbusters. There are always a lot of Cassandra's out there saying that we're going to crash anytime, and I just don't see it. I know a lot of these people, I'm in touch with a lot of the companies, I see Beta releases of all products, the consumer products, and…the slowdown just ain't happening, I'm sorry. And I've been through a lot of these tech booms over the last 40 years, and this is only showing signs of just getting started.

Q: How come Tesla (TSLA) is up and down $30 every couple of days?

A: Number one, it is the most actively traded stock in the market right now. It has implied volatility on the options of 70%, which is really the highest in the market of any individual stock. That just creates immense amounts of trading by options traders, volatility traders, by call writing, and 2x and 3x ETF long and short players. All of the financial engineering and new products that we see all gravitate toward the high volume stocks like Nvidia, Tesla, and Apple because that's where the money is being made. Some days Tesla accounts for 25% of all the market trading. Financial engineers go where the action is, where the volume is, where the customer demand is.

Q: Why do you expect only 5% to 10% corrections if the Fed rate cuts get completely priced out?

A: I don't expect the Fed to keep cutting interest rates. We should get another rate cut this year, and that may be it for the year. If inflation comes back (and of course, all of the new administration’s policies are highly inflationary) it’s just a question of how long it takes for it to hit the system.

Q: Do you believe I should hold all of my municipal bonds (MUB) with 10-year call protection at 4.75%?

A: On a tax-adjusted basis, I would say yes. You know, stock markets may peak and deliver a zero return, and in that situation, muni bonds are very attractive. The nice thing about bonds is that you hold on to maturity—you get 100% of your money back. With stocks, that is not always the case. Stocks you have to trade because the volatility can be tremendous. And in fact, what I do is I keep all of my money in one year Treasury bills. Last time I did this, which was in September, I locked in a one-year return for 5%.

Q: Would you prefer to buy deep in the money and put spreads on top of any rally?

A: Absolutely yes. If this is a real trading year, you not only buy the dips, you sell the rallies. We did almost no real selling last year. We really only did it in June and July because the market essentially went straight up, except for two hickeys. This could be the year of not only call sprints but put spreads as well. You just have to remember to sit down when the music stops playing.

Q: You say buy the dips; what would your dip be in JP Morgan (JPM)?

A: Well lower volatility stocks by definition have smaller drawdowns. JP Morgan (JPM) is one of those, so I'd be very happy to buy a 5% dip in JP Morgan. If it drops more, you double the position on a 10% pullback. Higher volatility stocks like Tesla—I'm really waiting for 10% or 20% corrections. You saw I just bought a 22% correction twice in Tesla with it down 110 points. One of those trades is at max profit right now and the other one has probably made half its money since yesterday. That is the game. The amount of dip you buy is directly related to the volatility of the stock.

Q: Should you let your cash go uninvested?

A: Yes, never let your cash go uninvested just sitting as cash. Your broker will take that money and put it in 90-day T-bills and keep the money for himself. So buy 90-day T-bills as a cash management tool—they're paying about 4.21% right now— and you can always use those as collateral under my positions on margin.

Q: Is Home Depot (HD) a buy on the LA reconstruction story?

A: I would say no, Los Angeles is probably no more than 5% of Home Depot's business—the same with Lowe's (LOW). A single city disaster is not enough to move the stock for more than a few days, and the fact is: Home Depot is mostly dependent on home renovation, which tends not to happen during dead real estate markets because, you know, it takes the flippers out of the market. It really needs lower interest rates to get Home Depot back up to new highs.

Q: Do you expect a big market move at the end of the day when the Fed makes its announcement?

A: The market has basically fully discounted the move on January 28, and if anything happens, there'll probably be a “sell on the news.” So, I expect we could give up a piece of the recent performance on the announcement of the Fed news.

Q: Should we expect trade alerts for LEAPS coming from you?

A: Absolutely, yes. However, LEAPS are something you really only want to do on down moves. If we don't get any, we'll just do the front-month call spreads. You can still make 10%, 20% a month just concentrating on financial call spreads.

Q: What would have happened to our accounts if we kept the (TLT) $82-$85 iShares 20+ Year Treasury Bond ETF (TLT) call spread and it went all the way down to $82?

A: The value of your investment goes to zero. Of course, it was declining at a very slow rate, and the $80: you might have gotten a bounce off the $85 level. But if the inflation number had come in hot, as had all other economic data of the last month, then you could have easily gotten a gap down to $82 and lost your entire investment, because two days is not enough time to expiration to recover that 3-point loss. And that's why I stopped out yesterday.

Q: Didn't David Tepper buy China (FXI)?

A: With both hands last September, yes he did. And my bet is he got out before he got killed. I mean, that's what hedge funds do. He probably got out close to cost, and you likely won't see him promoting China again anytime in the near future.

Q: I have June 530 puts on the S&P 500, should I get rid of them?

A: Yes, I don't see a big crash coming. You probably paid a lot going all the way out to June, and it's probably not worth hanging on to. Put spreads are the better way to go—that cuts your cost by two-thirds and those you only want to put on at market tops.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.