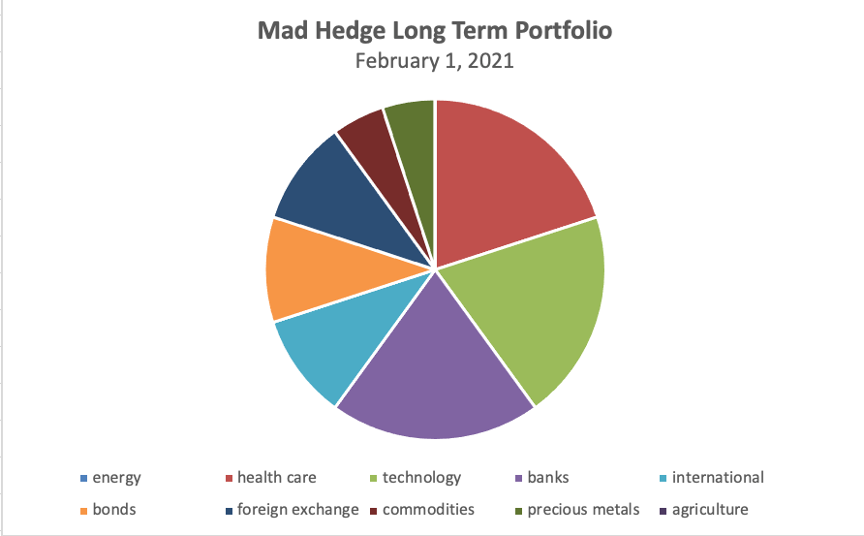

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on July 21, 2020. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted below.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

Changes

I am cutting back my weighting in biotech from 25% to 20% because Celgene (CELG) was taken over by Bristol Myers (BMY) at a 110% profit compared to our original cost. We also earned a spectacular 145% gain on Crisper Therapeutics (CRSP). I’m keeping it because I believe it has more to run.

My 30% weighting in technology also gets pared back to 20% because virtually all of my names have doubled or more. These have been in a sideways correction for the past six months but are still an important part of any barbell portfolio. So, take out Facebook (FB) and PayPal (PYPL) and keep the rest.

I am increasing my weighting in banks from 10% to 20%. Interest rates are finally starting to rise, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, add in Morgan Stanley (MS) and Goldman Sachs (GS), which will profit enormously from a continuing bull market in stocks.

Along the same vein, I am committing 10% of my portfolio to a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis, so go read Global Trading Dispatch.

I am keeping my 10% international exposure in Chinese Internet giant Alibaba (BABA) and the iShares MSCI Emerging Market ETF (EEM). The Biden administration will most likely dial back the recent vociferous anti-Chinese stance, setting these names on fire.

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). The Aussie has been the best performing currency against the US dollar and that should continue.

Australia will be a leveraged beneficiary of the synchronized global economic recovery, both through strong commodity prices and gold which has already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

As for precious metals, I’m baling on my 10% holding in gold (GLD), which delivered a nice 20% gain in 2020. From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

Yes, in this liquidity-driven global bull market, a 20% return is just not enough to keep my interest. Instead, I add a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles.

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/long-term-portfolio.png536864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-02 10:02:032021-02-02 10:37:30My Newly Updated Long-Term Portfolio

My daughter needed a desk so she could go to high school from her bedroom. So, I drove around Northern Nevada to get the perfect piece, visiting Reno, Sparks, Carson City, and Minden. It is one of the most conservative parts of the country, probably 90% republican.

What I saw was amazing.

There were Biden/Harris signs everywhere. Yes, there will still some Trump signs, but they were in a definite minority. Four years ago, you only saw Trump signs. The rare Clinton/Kaine sign was full of bullet holes, torn down, or copiously marked with offensive graffiti.

I thought, hmm, there must be a trade here.

We seem to be on the verge of massive changes in the US economy. Get in front of them and you’ll make a fortune. Lag behind, and you’ll be seen driving an Uber cab.

Technology undoubtedly led the decade, bringing in a 30% annual return since 2009. Industrial and other domestic stocks brought in no more than 12%. The “Roaring Twenties” could bring the reverse.

Technology will continue to do OK. Ever falling prices and greater service is a tough business model to beat. But let’s face it, none of these things are cheap. Apple (AAPL) going from a 9X multiple to 45X?

Industrials could be playing a massive catch up game initiating a new supercycle as they did from 2000-2010 when tech lagged in the wake of the Dotcom Bust.

This switch is made easier by the fact that most big industrial companies are now de facto technology ones. They all now use advanced cloud software, sophisticated robots, and state of the art distribution systems. Caterpillar (CAT) even has a 290-ton dump truck that drives itself like a giant Tesla (TSLA)!

Many of these companies I have covered for nearly 50 years, when they last belonged to the Nifty Fifty. So, for me, it’s a matter of dusting off my old research, seeing who is left, and giving them a modern spin. The great thing about these stocks is that many pay decent dividends.

I’ll give you a short list of where to buy the dips.

Banks – JP Morgan (JPM), Bank of America (BAC)

Railroads – Norfolk Southern (NSC), Union Pacific (UNP)

Credit Cards – Visa (V), Master Card (MA)

Couriers – FedEx (FDX), UPS (UPS)

Consumer Discretionary – International Paper (IP)

Hmm, a market where everything goes up. I like it! Dow 120,000 here we come!

Trump ordered all Stimulus Negotiations to cease, and then changed his mind six hours later. Clearly, the president has given up on the election and wants the next administration to inherit a Great Depression. Or is this Covid-19 talking? It’s the perfect scorched earth strategy. Write off another 2 million small businesses. Down ticket republican candidates will be beaten like a red-headed stepchild. Stocks plunged 600, with airlines in free fall, then bounced 700.

Jay Powell REALLY wants a stimulus package, claiming the economy desperately needs fiscal help to maintain a recovery or face a prolonged depression. “The risks of overdoing it seem, for now, to be small,” the central bank chief told the National Association for Business Economics. Are his pleas falling on deaf ears in Washington? Trump just gave our Fed governor the middle finger salute.

Share Buybacks vaporized T\this year and will be miniscule next year, with companies whose earnings have been crushed by the pandemic not participating. The ban on bank share buybacks imposed by the Fed continues. This has been the largest portion of net stock buying for the past decade. The good news is that foreign investors stepped in as big buyers in 2020, taking the indexes to new highs.

Apple to announce new 5G iPhone this week. The release came a month late, thanks to the pandemic. Scheduled for October 13, the event is called “High Speed”. Apple’s biggest sales quarter in history has just begun. Buy dips in (AAPL).

The Election is Noise and its best to focus on the bull market that has just begun, says JP Morgan. Record fiscal stimulus and quantitative easing in the face of near-zero interest rates create a perfect storm in favor of equities. The best stock to own going into the October 13 Prime Day?

Weekly Jobless Claims edged down to 840,000, still missing 200,000 from California, due to an upgrading computer system. California stopped reporting data so they can rebuild the antiquated computer system of the Employment Development Department, which has been breaking down due to overwhelming demand. Some 26.5 million workers are now claiming unemployment benefits.

Banks are making record trading profits on the back of the US Treasury market where volume has exploded. Even though there has been little net movement in prices in six months, the two-way bets have been enormous. It helps to have a massive home refi boom, incredible QE, and a government that is printing new debt like there’s no tomorrow.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch maintained a new all-time high last week by staying 100% in cash. I was just as grateful for having no positions on the up 600-point days as I was on the down 600-point days. Safe to say that I will be an increasingly more aggressive buyer on ever smaller dips.

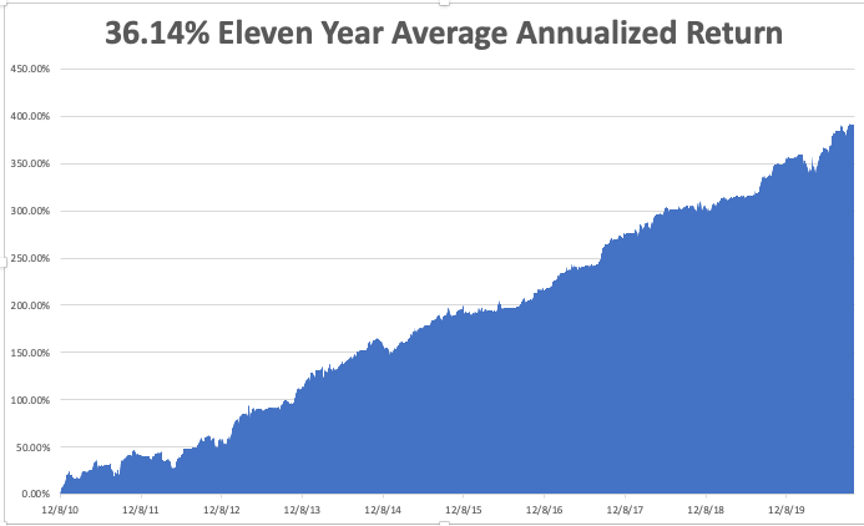

That keeps our 2020 year-to-date performance at a blistering +35.46%, versus a gain of 0.5% for the Dow Average. That takes my eleven-year average annualized performance back to +36.14%. My 11-year total return stood at new all-time high of +391.37%. My trailing one-year return dropped to +44.26%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 210,000, which you can find here.

On Monday, October 12 at 8:30 AM EST, the government is closed for Columbus Day so there will be no data releases, even though the stock market is open.

On Tuesday, October 13 at 9:00 AM EST, the US Inflation Rate for September is out.

On Wednesday, October 14, at 8:30 AM EST, The Producer Price Index for September is released. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, October 15 at 8:30 AM EST, the Weekly Jobless Claims are announced. We also get the Empire State Manufacturing Index.

On Friday, October 16, at 8:30 AM EST, US Retail Sales are printed. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I eventually found the perfect desk on Craigslist Reno. It was from the 1930s and had once occupied the office of the Metropolitan Life Insurance Company of New York, complete with two inkwells.

The company logo was prominently displayed in its wrought iron legs. When the Metropolitan modernized its offices in the 1950s, it sold off its furniture, which has been in circulation in the antique market ever since.

I told the seller, who had just moved from the east coast, of my amazing connection with the company. My Uncle Ed spent three years on a Navy destroyer in the Pacific during WWII. Enlistees in the 1940s were required to take out life insurance policies before they went off to war.

When Ed passed away a few years ago, I went through his papers and what did I find but a life policy from the Metropolitan Life Insurance Company for $1,000.

Ever the history buff, I called the company to find out if the policy was worth anything 70 years later. It turned out to have a cash value of $100,000, which they paid out immediately. I divided the money among my mom’s 20 grandchildren to pay for their college educations. Several now have PhDs. Got to love that compounding of interest.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Bring on the Roaring Twenties

https://www.madhedgefundtrader.com/wp-content/uploads/2020/10/table-and-lamp.png382286Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-10-12 09:02:572020-10-12 09:35:17The Market Outlook for the Week Ahead, or Back to the Nifty Fifty

Banks have certainly been the red-headed stepchild of equity investment in 2020.

While technology shares have rocketed by two, three, and four-fold, banks have remained mire in the muck, down 35% on the year while the S&P 500 is up 6%.

However, all that is about to change.

Banks have become the call option on a US economic recovery. When the economic data runs hot, banks rally. When it’s cold, they sell-off. So, in recent months bank share prices have been flat-lining.

You have to now ask the question of when the data stay hot, how high will banks run?

There also is a huge sector rotation issue staring you in the face. Where would you rather put new money, stocks at all-time highs trading at ridiculous multiples, or a quality sector in the bargain basement? Big institutions have already decided what to do and are buying every dip.

Banks certainly took it on the nose with the onset of the pandemic. Interest rates went to zero and loan default rates soared, demanding a massive increase in loan loss provisions.

Much more stringent accounting rules also kicked in during January known as “Current Expected Credit Losses.” That requires banks to write off 100% of their losses immediately, rather than spread them out over a period of years.

Then in June, the Federal Reserve banned bank share buybacks and froze dividends to preserve capital in expectation of more loan defaults.

So what happens next?

For a start, fall down on your knees and thank Dodd-Frank, the Obama era financial regulation bill.

Banks carped for years that it unnecessarily and unfairly tied their hands by limiting leverage ratios to only 10:1. Morgan Stanley reached 40:1 going into the Great Recession and barely made it out alive, while ill-fated Lehman Brothers reached a suicidal 100:1 and didn’t.

That meant the banks went into the pandemic with the strongest balance sheets in decades. No financial crisis here.

Thanks to government efforts to bring the current Great Depression to a quick end, generous fees have been raining down on the banks from the numerous loan programs they are helping to implement.

And trading profits? You may have noticed that options trading volume is up a monster 95% so far in 2020 and increased by a positively meteoric 120% in August. That falls straight to the banks’ bottom lines. If you’re wondering why your online trading platform keeps crashing, that’s why.

I list below my favorite bank investments using the logic that during depressions, you want to buy Rolls Royces, Teslas, and Cadillacs at deep discounts, not Volkswagens, Fiats, or Trabants.

JP Morgan (JPM) – Is the crown jewel of the sector, with the best balance sheet and the strongest customers. It has over reserved for losses that are probably never going to happen, stowing away some $25 billion in the last quarter alone.

Morgan Stanley (MS) - Brokerage-oriented ones like Morgan Stanley (MS) and Goldman Sachs (GS) are benefiting the most from the explosion in stock and options trading. I’ll pick my former employer (MS), where I once accounted for 80% of equity division profits, as (GS) is still mired in the aftermath of the $5 billion Malaysia scandal.

Bank of America (BAC) - is another quality play with a fortress balance sheet.

Citigroup (C) – Is the leveraged play in the sector with a slightly weaker balance sheet and more aggressive marketing strategy. It seems like they’re always trying to catch up with (JPM). This week’s revelation of a surprise $900 million “operational loss” and the penalties to follow knocked 13% of the share price. This is the high volatility play in the sector.

And what about Wells Fargo (WFC), you may ask, the cheapest bank of all? Unfortunately, it still has to wear a hair suit because of its many regulatory transgressions, before, during, and after the financial crisis so I’ll give it a miss. Oh, and Warren Buffet is selling too.

The One

https://www.madhedgefundtrader.com/wp-content/uploads/2020/08/jpm-bank.png508936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-16 09:02:002020-09-16 09:14:43The Bull Case for Banks

Six months into the quarantine, I feel like I’ve been under house arrest with no visiting privileges. And if I go outside for even a few minutes, I have to inhale the equivalent of a pack of cigarettes as I am surrounded by three monster fires. All I can say is that I’m getting a heck of a lot of work done.

We are in the middle of a 20-year move in the Dow Average from 6,500 to 120,000. We have just completed a fourfold move off the 2009 bottom. All that remains is to complete a second fourfold gain by 2030.

The move is being driven by hyper-accelerating technology on all fronts. The first half of this move was wrought with constant fear and disbelief. The second half will be viewed as a new “Golden Age” and a second “Roaring Twenties.” The euphoria of July and August were just a foretaste.

And here is the dilemma for all investors.

The Dow has just pulled back 6.1% from the all-time high of 29,300 to 27,500. Should you be buying here, keeping the eventual 120,000 target in mind? Or should you hold back and wait for 26,000, 25,000, or 24,000?

The risk is that if you lean out too far to grab the brass ring, you’ll fall off your horse. By getting too smart attempting to buy the bottom, you might miss the next 93,000 points.

And now, I’ll make your choice more complicated.

The president has recently whittled away at his deficit in the polls, however slightly, typical of the run-up to the November elections. That increases the uncertainty of the election outcome and increases market volatility (VIX). Ironically, the better Trump does, the lower stocks will fall. So, if you do hang out for the lower numbers you might actually get them, and then more.

That puts the 200-day moving averages in play, not only for the major indexes but for single stocks as well. That could take Apple (AAPL) from a high of $137 to $80, a Tesla down from a meteoric $500 to $300.

Hey, if this were easy, your cleaning lady would be doing this for a tiny fraction of the pay.

Did I just tell you the market may go up, down, or sideways? I sound like a broker.

The 200-day moving averages are definitely in play. The 200-day moving average for the Dow Average is 26,298, down an even 10% from the high for the year. The technology-heavy S&P 500 could fall as much as 14% to its 200-day at 3,097.

Don’t bet against the Fed as Tuesday’s 700-point rally in the Dow Average sharply reminded traders. Don’t bet against the global scientific community either. That’s why I am fully invested and within spitting distance of a new all-time high. After a pre-election low, the market will soar to new highs. Even if Trump loses the election, quantitative easing and fiscal stimulus will continue as far as the eye can see.

The elephant unwinds. Softbank dumped $718 million worth of technology call options deleveraging in a hurry. (NFLX), (FB), and (ADBE) were the targets according to market makers. They still own $1.66 billion worth of long positions in call options. Softbank’s position has grown so large that even my cleaning lady and gardener know about them.

The Tesla bubble popped, down a record 22% in one day after traders learned it would NOT be added to the S&P 500. Tesla approached my medium-term downside target of down 40%, or $300 a share. It seems too much of its earnings were coming from non-recurring EV subsidies from the Detroit carmakers. With a peak market cap for an eye-popping $450 billion, it’s probably the largest company ever turned down from the Index.

Google ditched Irish office space, putting on ice a plan to rent additional office space for up to 2,000 people in Dublin. The retreat from global office space continues. The company was close to taking 202,000 sq ft (18,766sq m) of space at the Sorting Office building before the virus hit.

AstraZeneca halted their vaccine trial after a patient fell ill. It’s not clear if the vaccine killed off the phase 3 trial volunteer, a preexisting condition felled them, or an unrelated illness hit. The company was developing the “Oxford” vaccine, which had been the best hope for developing Covid-19 immunity. It definitely creates a pause for the headline rush to develop a vaccine. Notice the tests are being held in South Africa where patients have little legal recourse. Keep buying (AZN) on dips.

“Skinny” failed, tanking the Dow Average by 450 points. A Republican Senate failed to provide even $500 billion to support a COVID-19-ravaged economy. There will be no more stimulus until a new administration takes office. Until then, unemployment will remain in the high single digits, tens of thousands of small businesses will fail, and home foreclosures will explode. The stock market cares about none of this, as it is dominated by large, heavily subsidized companies.

Nikola crashed, down 33%, in response to a damning report from a noted short-seller. They don’t have a truck, they lack a claimed hydrogen fuel source, and the founder is milking the company for every penny he can. It’s all hype, thanks to endless quantitative easing. None of the Tesla wannabees are going anywhere. General Motors (GM), which just bought 11% of the company, has egg on its face. With a market cap of $20 billion, Nikola is this year’s Enron. Sell short (NKLA) on rallies.

US inflation jumped, with the Consumer Price Index up 1.3% YOY in August, compared to only 1% in July. Soaring used car prices accounted for the bulk of the gain. More proof that the economy lives. Is this the beginning of the end or the end of the beginning?

Goldman Sachs moved global stocks to “overweight”. They’re preparing for the post-pandemic world. Cyclical “recovery” stocks like banks will take the lead. It fits in nicely with my view of a monster post-election rally and a Dow 120,000 by 2030.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch clocked its second blockbuster week in a row, thanks to aggressively loading up on stocks at the previous week’s bottom (JPM), (C), (AMZN). My long in gold (GLD) looked shinier than ever. I bet the ranch again on a massive short in the US Treasury bond market (TLT) which paid off big time. My short position in the (SPY) is looking sweet.

My only hickey was an ill-fated long in Apple (AAPL), which I stopped out of at close to cost. Notice that I am shifting my longs away from tech and toward domestic recovery plays.

You only need 50 years of practice to know when to bet the ranch.

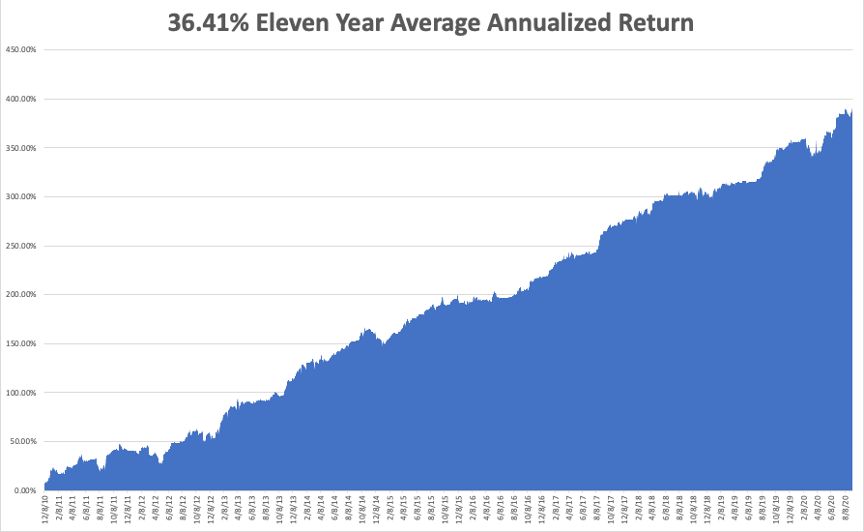

That takes our 2020 year-to-date back up to a blistering 35.51%, versus -2.93% for the Dow Average. September stands at a robust 8.96%. That takes my 11-year average annualized performance back to 36.41%. My 11-year total return has reached to another new all-time high at 391.42%. My trailing one year return popped back up to 58.13%.

It will be a dull week on the data front, with only the Federal Reserve Open Market Committee Meeting drawing any attention.

The only numbers that really count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, September 14 at 11:00 AM US Inflation Expectations are released.

On Tuesday, September 15 at 8:30 AM EST, the New York Empire State Manufacturing Index for September is published. A two-day meeting at the Federal Reserve begins.

On Wednesday, September 16, at 8:30 AM EST, September Retails Sales are printed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out. At 2:00 the Fed announces its interest rate decision, which will probably bring no change.

On Thursday, September 17 at 8:30 AM EST, the Weekly Jobless Claims are announced. Housing Starts for August are also out.

On Friday, September 18, at 8:30 AM EST, the University of Michigan Consumer Sentiment is announced. At 2:00 PM The Bakers Hughes Rig Count is released.

As for me, the Boy Scout camporee I was expected to judge and supervise this weekend was cancelled, not because of Covid-19, but smoke. This will certainly go down in history as the year from hell.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/09/john-golden-nugget.png492656Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-14 04:02:132020-09-14 05:41:27The Market Outlook for the Week Ahead, or the 200-Days are in Play

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHY CASH IS STILL TRASH),

(JPM), (AAPL), (AMZN), (V), (TLT), (SPY), (GOOGL),

(BAC), (C), (FCX), (VIX), (VXX), (TSLA), (FB)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-08 09:04:422020-09-08 11:09:58September 8, 2020

This is no more than a 10%-15% correction typical for long term bull markets.

Sure, we saw every technical indicator known to man scream “SELL” in the run-up to the recent market top. There were other factors at play as well.

The bulk of the buying focused on only the top six stocks, more concentrated than seen during the Dotcom Bubble Top in 2000.

There really was only one buyer. That would be my friend Masayoshi Son’s Softbank (SFTBY). He bought $4 billion worth of big tech call options in the run-up to the top with an exercise value of $30 billion. When he started to sell last Monday, the market for these options vaporized and stocks plunged.

The fact that both Apple (AAPL) and Tesla (TSLA) shares split the same day also defined a market top that I have been warning readers about for weeks.

This is all in the face of the incredible reality that 50% of all S&P 500 (SPY) stocks are down over the past two years. It really has been a stock picker’s market with a turbocharger.

And this isn’t just any old bull market. We are in fact 11 ½ years into a bull market that started in March 2009 that has another decade to run. We have completed the first 400% gain. What lies ahead of us is another stock market increase of 400%, taking us up to 120,000 in the Dow Average by 2030.

And this is a bull market that has suffered plenty of 10%-15% corrections since its inception. The one that began in Thursday is no different. The sole exception to this analysis was the COVID-19-induced 37% meltdown that began in February. That little event only lasted six weeks.

For you see, the fundamentals have not changed one iota. No, I’m not talking about earnings, valuations, or sales growth. That is so 20th century.

No, I’m referring to the only fundamental that counts in the 21st century: Liquidity.

And liquidity isn’t shrinking, it is in fact increasing. That includes the unprecedented expansion of quantitative easing by the Federal Reserve, massive deficit spending by the US government, and zero interest rates, which Fed governor Jay Powell has promised us will continue for another five years.

During the last Dotcom Bubble top, the FAANGs and Tesla (TSLA) did not even exist. Apple was just coming out of its flirtation with bankruptcy and Amazon (AMZN) had just barely gone public. Google (GOOGL) and Facebook (FB) were still but glimmers in their founders’ eyes.

Except now we have a new bullish fundamental to discount: a Biden win in November. Since Biden decisively pulled ahead in the polls in May, the stock market has risen almost every day. He is 4%-10% ahead in every battleground state poll.

Even if Trump were to win every red and red-leaning state accounting for 163 electoral college votes, plus all 63 votes from toss-up states (AZ, NC, IA, FL, GA, OH), he would still lose the election, where 270 votes are needed to win. Just THAT is a 1:100 event, on the scale of Harry Truman’s historic 1948 compact, and Trump is no Harry Truman.

So what of Biden wins?

You can count on the $3 trillion stimulus bill passed by the House in March to go through, which primarily allocates money to keep states and local municipalities from firing policemen, firemen, and teachers.

Next to come are another $3 trillion in infrastructure spending. And I absolutely know from past experience that markets love this kind of stuff. It enhanced liquidity even more.

As I say, cash is still trash, and it may remain so for years.

The Top is in, with a horrific two-day 1,500-point selloff in the Dow Average ($INDU) coming out of the blue on no news and signaling the end of the current rally. Whatever went up the most is now going down the most as the Robinhood traders flee in panic. This was long overdue. Margin calls are running rampant.

Volatility (VIX) soared to $38, up 70% in two days, meaning that we may be close to the end of this correction. The (SPX) is down 24 points, 6.7% from the Wednesday high. The last (VIX) peak was at $44 in June and $80 in March. Time to start buying stocks for a yearend rally? Look at the banks.

Was Apple (AAPL) really up 400%? Did Tesla gain 500%? You might be fooled if you didn’t know that these stocks just split, Apple at 4:1 and Tesla for 5:1. In fact, both stocks posted robust gains in real terms, Apple up 5% and Tesla up 10%. Tesla just hit my five-year split-adjusted target of $2,500. Every other analyst had a much lower target or were bearish. Time to run a mile as splits often herald intermediate market tops.

Apple hit a $2.3 trillion in market cap at the peak, up a staggering $300 billion in days. We are truly in La La Land here. The price-earnings multiple has soared from 9X to 40X. That 5G iPhone better deliver. Didn’t you hear that 5G was causing Coronavirus, a popular internet conspiracy theory?

The Dow Average just lost its Apple turbocharger. Some 1,000 of the 2,000 points the Dow Average gained in August were due to Apple alone. With the Dow rebalancing today, with (XOM), (PFE), and (RTX) out and (CRM), (AMGN), and (HON) in, Apple’s influence has been greatly diluted. With the (VIX) back up above $26, the worst is yet to come. The stock market is screaming for a correction.

Copper (FCX) hit a new 3-year high, with demand soaring in China. They were the first to cap Covid-19 and restore their economy. The red metal is a great call on the recovery of the global economy. Those who bought the Freeport McMoRan (FCX) LEAPS I recommended in March are sitting pretty. The shares are up 228% since then.

Tesla to sell $5 billion in stock to finance the construction of new factories in Nevada, TX, and Germany. (TSLA) fell 5% on the news. I had been advising clients to sell all week. It won’t be a conventional secondary stock offering but an effort to sell into every stock spike. More proof that Elon hates Wall Street as if we needed more. With a market cap of $450 billion, investors are finally viewing Tesla as a data company rather than a car company.

US car sales recover to 15.2 million in August on an annualized basis. That brings us almost back to pre-pandemic levels. This is the best indicator yet that the US is returning to a semi-normal economy. Of course, zero interest rates and other unprecedented incentives are a big help.

Consumer Spending popped, up 1.9% in July, which accounts for two-thirds of the US economy. Those who have money are spending like there’s no tomorrow, and with a global pandemic, maybe there won’t be. New car purchases were a big winner as buyers take advantage of 0% financing everywhere.

Weekly Jobless Claims dropped to 880,000, still terrible, but less terrible than last week. California claims have topped 8 million since the pandemic began. Continuing claims drop to 13.3 million, down from the 25 million peak in May.

US Unemployment Rate plunged to 8.4% in August, from 10.2%. The August Nonfarm Payroll report jumps by 1.37 million. It’s a much faster improvement than expected. Retail gained 248,000, Education & Health Services were up 147,000, and Leisure & Hospitality were up 174,000, Government was up 344,000. It’s all thanks to the miracle of government spending. The Dow Average is down 500 points anyway.

China to dump US Treasury bonds in response to Trump's escalating trade war, putting $200 billion in paper up for sale. They hold $1.07 trillion in total and is our largest single creditor. The (TLT) is down two points on the news, where I am running a double short position. Who is going to fund America’s massive borrowing?

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch bounced back hard with some super aggressive buying of stocks right at the Thursday and Friday market bottoms and selling short of bonds at the top.

By going full speed ahead, damn the torpedoes, I brought in the best two-day return in the 13-year history of the Mad Hedge Fund Trader, up a heroic 8.27%.

It started out as a terrible week, getting flushed out of one of my short positions in the (SPY) for a big loss as the market hit a new all-time high.

Then I got long banks (JPM), Apple (AAPL), Amazon (AMZN), Visa (V), and went triple short bonds (TLT). I still retain one short in the (SPY), which is now profitable. I would have bought Bank of America (BAC) and Citigroup (C), but the market ran away before I could write the trade alerts.

The instant crash was yet another gift. Right after I shorted bonds, the Chinese hinted that they would unload $200 million worth of their US Treasury bond holdings. The harder I work, the luckier I get.

If these positions expire at max profit in eight trading days, I will be back at new all-time highs. Notice that I am shifting my longs away from tech and toward domestic recovery plays.

You only need 50 years of practice to know when to bet the ranch.

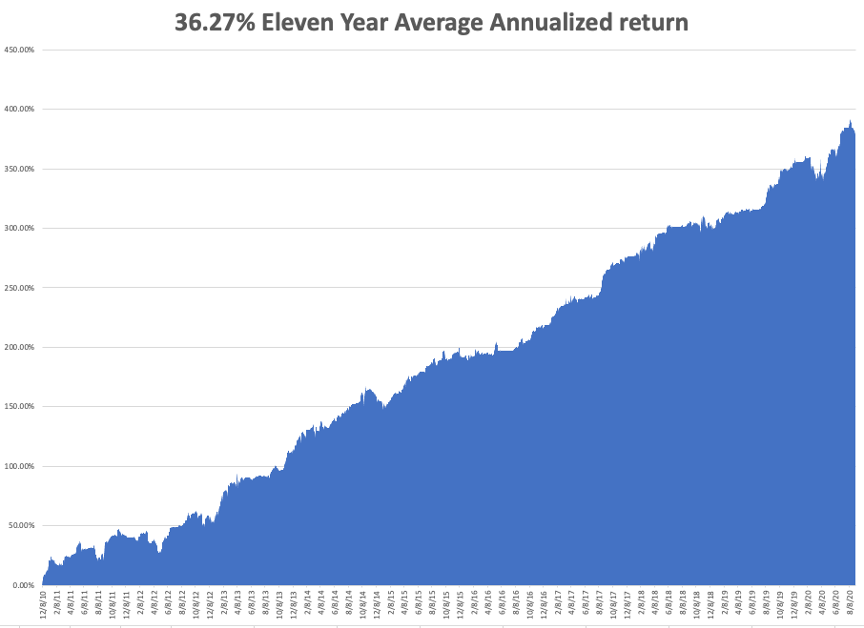

That takes our 2020 year to date back up to 30.99%, versus -0.70% for the Dow Average. September stands at 4.44%. That takes my eleven-year average annualized performance back to 36.27%. My 11-year total return returned to 386.90%. My trailing one-year return popped back up to 51.60%.

It is a quiet week as always following the fireworks of the jobs data.

The only numbers that really count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, September 7, it is Labor Day in the US, and markets are closed.

On Tuesday, September 8 at 10:00 AM EST, the Economic Optimism Index for September is released.

On Wednesday, September 9, at 8:13 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, September 10 at 8:30 AM EST, the Weekly Jobless Claims are announced. US Core Producer’s Price Index for August is also out.

On Friday, September 4, at 8:30 AM EST, the US Inflation Rate for August is printed. At 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I am headed back to Lake Tahoe to flee the horrific smoke in the San Francisco Bay Area drifting our way from the rampant California wildfires. If people don’t believe in global warming, they should come here where we have it in spades. We’ll even give you some.

At least we’ve been getting spectacular sunsets.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/09/CA-sunset.png640480Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-08 09:02:532020-09-08 11:10:54The Market Outlook for the Week Ahead, or Why Cash is Still Trash

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-09-04 09:04:412020-09-04 10:26:32September 4, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.