Anyone would be forgiven for thinking that the stock market has become bipolar.

According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact.

Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the ultra low level of interest rates. Farm incomes are up, but are a tiny proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

A disproportionate share of corporate profits is being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace.

Caveat emptor. Buyer beware.

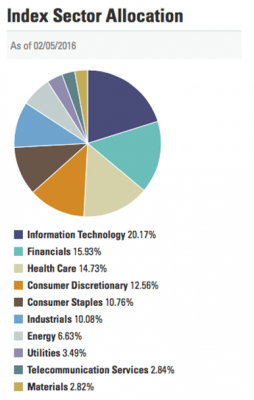

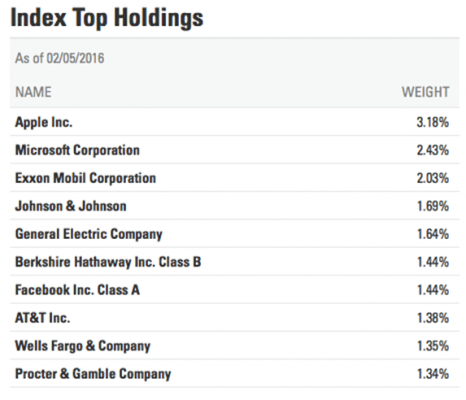

What?s In the S&P 500?

Has the Market Become Bipolar?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/09/bipolar-masks-e1455046648141.jpg287400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-10 01:07:452016-02-10 01:07:45The Bipolar Economy

For those of you who heeded my expert advice to buy the ProShares Ultra Short Euro ETF (EUO) last July, well done!

You are up a massive 48%! This is on a move in the underlying European currency of only 18.5%.

My browsing of the Galleria in Milan, the strolls through Spanish shopping malls, and my dickering with an assortment of dubious Greek merchants, all paid off big time. It turns out that everything I predicted for this beleaguered currency came true.

The European economy did collapse. Cantankerous governments made the problem worse by squabbling, delaying and obfuscating, as usual.

The European Central Bank finally threw in the towel and did everything they could to collapse the value of the Euro and reinvigorate their comatose economies. This they did by imitating America?s wildly successful quantitative easing, which they announced with local variations last Thursday.

And now for the good news: The best is yet to come!

Europe is now six days into a strategy of aggressive monetary easing which may take as long as five years until it delivers tangible, sustainable results. That?s how long it took for the Federal Reserve?s QE to restore satisfactory levels of confidence in the US economy.

The net net is that we have almost certainly only seen the first act of a weakening of the Euro which may last for years. A short Euro could be the trade that keeps on giving.

The ECB?s own target now is obviously parity against the greenback, which you will find predicted in my own 2015 Annual Asset Class Review released at the beginning of January (click here).

Once they hit that target, 87 cents to the Euro will become the new goal, and that could be achieved sooner than later.

However, you will not find me short the Euro up the wazoo this minute. I think we have just stumbled into a classic ?Buy the Rumor, Sell the News? situation with the Euro.

The next act will involve the ECB sitting on its hands for a year, realizing that their first pass at QE was inadequate, superficial, and flaccid, and that it is time to pull the bazooka out of their pockets once again.

This is a problem when the entire investment world is short the Euro. That paves the way for countless, rip your face off short covering rallies in the months ahead. Any smidgeon or blip of positive European economic data could spark one of these.

Trading the Euro for the past eight months has been like falling off a log. It is about to get dull, mean and brutish. So for the moment, my currency play has morphed into selling short the Japanese yen, which has its own unique set of problems.

As for the unintended consequences of the Euro crash, the Q4 earnings reports announced so far by corporate America tells the whole story.

Companies with a heavy dependence on foreign (read Euro and yen) denominated earnings are almost universally coming up short. On this list you can include Caterpillar (CAT), Procter and Gamble (PG), and Microsoft (MSFT).

Who are the winners in the strong dollar, weak Euro contest? US companies that see a high proportion of their costs denominated in flagging foreign currencies, but see their incomes arrive totally in the form of robust, virile dollars.

You may not realize it, but you are playing the global currency arbitrage game every time you go shopping. The standout names here are US retailers, which manufacture abroad virtually all of the junk they sell you here, especially in low waged China.

The stars here are Macy?s (M), Family Dollar Stores (FDO), Costco (COST), Target (TGT), and Wal-Mart (WMT).

You can see this divergence crystal clear in examining the behavior of the major stock indexes. The chart for the Guggenheim S&P 500 Equal Weight ETF (RSP), which has the greatest share of currency sensitive multinationals, looks positively dire, and may be about to put in a fatal ?Head and Shoulders? top (see the following story).

The chart for the NASDAQ (QQQ), where constituent companies have less, but still a substantial foreign currency exposure, appears to be putting in a sideways pennant formation before eventually breaking out to new highs once again.

The small cap Russell 2000, which is composed of almost entirely domestic, dollar based, ?Made in America? type companies, is by far the strongest index of the trio, and looks like it is just biding time before it blasts through to new highs.

If you are a follower of my Trade Alert Service, then you already know that I have a long position in the (IWM), which has already chipped in 2.12% to my 2015 performance.

You see, there is a method to my Madness.

Never Underestimate the Value of Research

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/John-Thomas1-e1422462857973.jpg302400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-28 11:35:022015-01-28 11:35:02The Unintended Consequences of the Euro Crash

I often see one stock index outperform another, as different segments of the economy speed up, slow down, or go nowhere. Sometimes the reasons for this are fundamental, technical, or completely arbitrary.

Many analysts have been scratching their heads this year over why the S&P 500 has been moving from strength to strength for the past year, while the Dow Average has gone virtually nowhere. Since January, the (SPX) has tacked on a reasonable 7.9%, while the Dow has managed only a paltry 3.4% increase.

What gives?

The problem is particularly vexing for hedge fund managers, who have to choose carefully which index they use to hedge other positions. Do you use the broad based measure of 500 large caps or a much more narrow and stodgy 30?

What?s a poor risk analyst to do?

The Dow Jones Industrial Average was first calculated by founder Charles Dow in 1896, later of Dow Jones & Company, which also publishes the Wall Street Journal. When Dow died in 1902, the firm was taken over by Clarence Barron and stayed within family control for 105 years.

In 2007, on the eve of the financial crisis, it was sold to News Corporation for $5 billion. News Corp. is owned by my former boss, Rupert Murdoch, once an Australian, and now a naturalized US citizen. News then spun off its index business to the CME Corp., formerly the Chicago Mercantile Exchange, in 2010.

Much of the recent divergence can be traced to a reconstitution of the Dow Average on September 20, 2013, when it underwent some major plastic surgery.

It took three near-do-wells out, Bank of America (BAC), Hewlett Packard, (HPQ), and Alcoa (AA). In their place were added three more robust and virile companies, Goldman Sachs (GS), Visa (V), and Nike (NKE).

Call it a nose job, a neck lift, and a tummy tuck all combined into one (Not that I?ve been looking for myself!).

And therein lies the problem. Like many attempts at cosmetic surgery, the procedure rendered the subject uglier than it was before.

Since these changes, the new names have been boring and listless, while the old ones have gone off to the races. Hence, the differing performance.

This is not a new problem. Dow Jones has been terrible at making market calls over its century and a half existence. As a result, these rebalancings have probably subtracted several thousand points over the life of the Dow.

They are, in effect, selling lows and buying highs, much like individual retail investors do. It is almost by definition the perfect anti-performance index. When in doubt, always measure your own performance against the Dow.

Dow Jones takes companies out of its index for many reasons. Some companies go bankrupt, whereas others suffer precipitous declines in prices and trading volumes. (BAC) was removed because, at one point, its shares took a 95% hit from its highs and no longer accurately reflected a relevant weighting of its industry. Citigroup (C) suffered the same fate a few years ago.

Look at the Dow Average of 1900 and you wouldn?t recognize it today. In fact, there is only one firm that has stayed in the index since then, Thomas Edison?s General Electric (GE). Buying a Dow stock is almost a guarantee that it will eventually do poorly.

This is why most hedge funds rely on the (SPX) as a hedging vehicle and how its futures contracts, options and ETF?s, like the (SPY), get the lion?s share of the volume.

Mind you, the (SPX) has its own problems. Apple (AAPL) has far and away the largest weighting there and is also subject to regular rebalancings, wreaking its own havoc.

Because of this, an entire sub industry of hedge fund managers has sprung up over the decades to play this game. Their goal is to buy likely new additions to the index and sell short the outgoing ones.

Get your picks right and you are certain to make money. Every rebalancing generates massive buying and selling in single names by the country?s largest institutional investors, which in reality are just closet indexers, despite the hefty fees they charge you.

Given their gargantuan size these days, there is little else they can do. Rebalancings also give brokerage salesmen talking points on otherwise slow days and generate new and much needed market turnover.

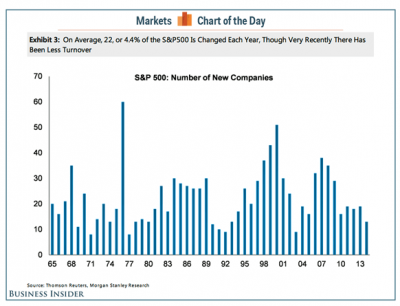

What has made 2014 challenging for so many managers is that so much of the action in the Dow has been concentrated in just a handful of stocks.

Caterpillar (CAT), the happy subject of one of my recent Trade Alerts, accounts for 35.3% of the Index gain this year. Walt Disney (DIS) speaks for 24.2% and Intel (INTC) 23.4%.

Miss these three and you are probably trolling for a new job on Craig?s? List by now, if you?re not already driving a taxi for Uber.

It truly is a stock picker?s market; a market of stocks and not a stock market.

Believe it or not, there are people that are far worse at this game than Dow Jones. The best example I can think of are the folks over at Nihon Keizai Shimbun in Tokyo (or Japan Economic Daily for most of you), who manage the calculation of the 225 stocks in the Nikkei Average (once known as the Nikkei Dow).

In May, 2000, out of the blue, they announced a rebalancing of 50% of the constituent names in their index. Their goal was to make the index more like the American NASDAQ, the flavor of the day. So they dumped a lot of old, traditional industrial names and replaced them with technology highfliers.

Unfortunately, they did this literally weeks after the US Dotcom bubble busted. The move turbocharged the collapse of the Nikkei, probably causing it to fall an extra 8,000 points or more than it should have.

Without such a brilliant move as this, the Nikkei bear market would have bottomed at 15,000 instead of the 7,000 we eventually got. The additional loss of stock collateral and capital probably cost Japan an extra lost decade of economic growth.

So for those of you who bemoan the Dow rebalancings, you should really be giving thanks for small graces.

Rebalancing? Yikes!

Miss This One, And You?re Toast

It Truly is a Stock Picker?s Market

The Key to Your 2014 Performance

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/Mickey-Mouse.jpg352339Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-07-10 01:05:012014-07-10 01:05:01Why is the S&P 500 Beating the Dow?

So, I?m sitting here in my Turkish redoubt, fighting off unusually aggressive flies and going over my charts. It?s further proof that no matter where in the world you travel, work follows you.

There is truly no rest for the wicked.

As a respite, I have the Best of the Guess Who playing on iTunes.

I noticed that the market priced our Caterpillar (CAT) July, 2014 $97.50-$100 in-the-money bull call spread at $2.50 at last night?s close. This is despite the options still having ten days left to the July 18 expiration. This means that the market is effectively pricing the inverse, the Caterpillar (CAT) July, 2014 $97.50-$100 in-the-money bear put spread at zero.

It?s not just Caterpillar that is doing this. I see this happening across the market, where downside protection is being thrown away for nothing. I see anomalies like this happening from time to time, but not very often. Think of it as complacency in the extreme, on adrenaline and with a turbocharger.

It always ends in tears, but who knows when? I priced the alert at $2.48 just to allow two cents for you to get an execution done. This should add 1.04% to your total return for 2014. If some high frequency dummy is willing to work for pennies, that?s fine with me. Nobody works for free.

If you don?t get done today, then re-enter the order on Monday. You will almost certainly get taken out after they remove the long weekend time decay.

Taking profits here does give you some black swan protection. We could have a flash crash at any time, if not in the main market, then certainly in single names. It also removes a 9/11 type risk. Sure, you say, this is all very improbable. But then, 9/11 was viewed as an impossibility on 9/10.

This has been a bang up trade for us in an otherwise detestable trading environment. We caught a nearly 10% rise in the shares in a market that was otherwise quiescent. I managed to do this with a half dozen other names as well.

It?s not that I have suddenly fallen out of love with the maker of heavy construction and mining equipment. I think (CAT) will continue to appreciate for the rest of 2014, possibly rising to $120-$130/share.

I have been following this company for 40 years and it is one of the most solid, best-managed companies out there. And I love their cool, yellow baseball caps.

(CAT) has finally crossed the wide desert and will continue from strength to strength (there goes those Middle East metaphors again!). And if China manages to engineer a recovery, then it will be really off to the races. So will the rest of the entire industrials sector for that matter.

The other problem with taking off a trade here is that there is nothing to replace it. Zero premiums mean there is not another risk-controlled position to replace the outgoing (CAT) position.

So don?t expect a lot of joy from me on the Trade Alert front until August.

I always take this as an invitation to say, ?Thank you very much, Mr. Market? and take a profit. It is also a sign of how far volatility has fallen, and by implication, option premiums.

Thank you, Mr. Caterpillar!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/Caterpillar-Tractor.jpg295494Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-07-07 09:21:402014-07-07 09:21:40Taking Profits on Caterpillar

Corporate earnings are up big! Great! Buy! No wait! The economy is going down the toilet! Sell! Buy! Sell! Buy! Sell! Help! Anyone would be forgiven for thinking that the stock market has become bipolar. There is, in fact, an explanation for this madness. According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy. Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact. Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the low level of interest rates and the collapse of the housing market. Farm incomes are up, but are a small proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive. It gets more complicated than that. A disproportionate share of corporate profits are being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes. They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, much more than they are here. Those with large domestic businesses, like retailers, earn far less, but pay more in tax, as they lack the offshore entities in which to park profits. The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace. Buyer beware.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/Caveat-Emptor.jpg331498Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-12-11 01:05:332013-12-11 01:05:33The Bipolar Economy

Corporate earnings are up big! Great! Buy! No wait! The economy is going down the toilet! Sell! Buy! Sell! Buy! Sell! Help! Anyone would be forgiven for thinking that the stock market has become bipolar. According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits account for only a small part of the economy. Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact. Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the low level of interest rates and the collapse of the housing market. Farm incomes are up, but are a small proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive. It gets more complicated than that. A disproportionate share of corporate profits are being earned overseas. So multinationals with a big foreign presence, like Intel, Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes. They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them. The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace. Caveat emptor. Buyer beware.

What?s In the S&P 500?

Has the Market Become Bipolar?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/08/Girl-Sad.jpg327437Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-21 09:05:252013-08-21 09:05:25The Bipolar Economy

Grain traders have suffered a terrible 2013, a perfect storm of great news for farmers and terrible news for prices. But while farmers can make up for low prices with higher production, no such convenience exists for grain traders.

In January, right out of the gate, the USDA predicted that the US would produce the largest corn crop in history, or some 96 million bushels. That would be the largest since 1936. It now appears that this could be a low-ball figure.

Some private estimated see the total reaching 100 million bushels before the crying is over. Some 63% of the corn crop is now rated good/excellent, well above the five-year average of 58%, and trending northward.

Geopolitics has also conspired to drive prices southward. Egypt, with its burgeoning 83 million population, with a single river (the Nile) and a bleak desert to support it, is far and away the world?s largest wheat importer. A recent coup d??tat on the heels on an economic collapse promises to remove it from the marketplace soon. Buyers without cash are not buyers at all, no matter how dire the need. Only food aid from the US government or the United Nations can step in at this stage to head off mass starvation.

As if the news were not bad enough, the Russian cartel that controls two thirds of the world?s $22 billion a year potash supply, a crucial fertilizer used globally, collapsed last week over a price dispute. Known to chemists like me as Potassium carbonate, potassium sulfate, or potassium chloride, this compound is a key factor in strengthening roots during the growing cycle. One analyst said that the breakup of the cartel is akin to ?Saudi Arabia dropping out of OPEC.?

The move promises to take potash prices down from the 2008 peak of $1,000/tonne to $300 by yearend. Potash stocks crashed worldwide, with lead firm Potash (OT) diving 30%. Agrium (AGU) was down by 15%.

This will enable farmers to buy more fertilizer at cheaper prices next year, driving down the prices on far month futures contracts today. Too bad the Canadian government didn?t allow the sale of Potash (POT) to China go through on national security grounds. The shareholders must be kicking themselves.

The move promises to demolish the entire grade trade for this year. Not only has the Potash industry been hurt, so have agricultural equipment manufacturers, like Deere (DE) and Caterpillar (CAT) and the Powershares Multisector Agricultural Commodity Fund ETF (DBA).

Long gone are the heady days of last year, when scorching temperatures induced by global warming caused grain prices to nearly double. Some nine out of the ten last years have been the hottest in recorded history. Global warming denier-in-chief, Texas governor Rick Perry, saw his state suffer 100 consecutive days of over 100 degree temperature.

For me, these developments put the grain trade off limits for the foreseeable future. The only kind thing to be said here is that this will eventually lead to a final bottom that we can eventually trade off of. That would set up a killer position for the nimble if hot weather returns in 2014.

Potash Crystals

I Don?t See Any Grain Buyers Here

https://www.madhedgefundtrader.com/wp-content/uploads/2013/08/Potash-Crystals.jpg333442Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-08 01:04:392013-08-08 01:04:39A Perfect Storm Hits the Grain Trade

Corporate earnings are up big! Great! Buy! No wait! The economy is going down the toilet! Sell! Buy! Sell! Buy! Sell! Help! Anyone would be forgiven for thinking that the stock market has become bipolar.

There is, in fact, an explanation for this madness. According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy. Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact.

Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the low level of interest rates and the collapse of the housing market. Farm incomes are up, but are a small proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that. A disproportionate share of corporate profits are being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes. They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, much more than they are here. Those with large domestic businesses, like retailers, earn far less, but pay more in tax, as they lack the offshore entities in which to park profits.

The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace.

Buyer beware.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/Caveat-Emptor.jpg331498Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-07-19 01:05:522013-07-19 01:05:52The Bipolar Economy

Panic is on deck, to use the baseball terminology that my foreign readers are often attempting to decipher. That is the only conclusion one can reach after getting gob smacked by the price action this morning. Copper got spanked for eight cents, oil burned $2, gold shed another $26, and silver puked 70 cents.

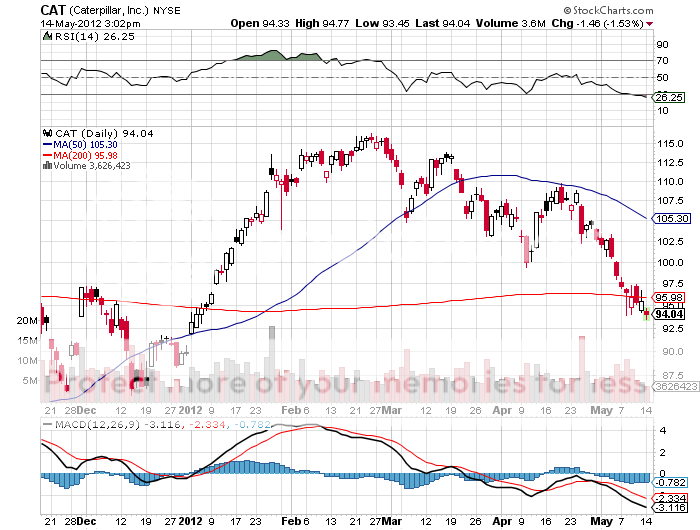

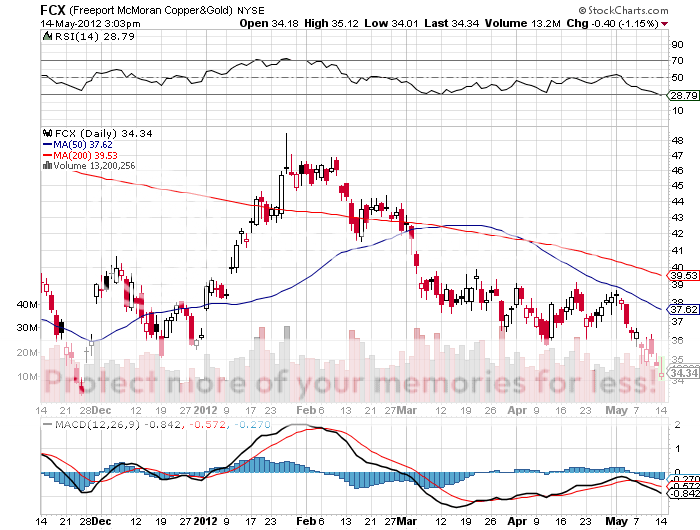

The tantrum like stock behavior in producing and equipment companies, like Freeport McMoRan (FCX) and Caterpillar (CAT) has been atrocious. How many of you out there know that JP Morgan (JPM) is the largest holder of futures contracts in the silver market and just got hit with a massive margin call? Why is all this happening on the 100 year anniversary of the sinking of the HMS Titanic?

Blame it all on Uncle Buck, whose recent steroid treatments has enabled him to unload the pounds, shed the fat, and adopt a new, more virile attitude towards life. Every other currency now looks like a 98 pound weakling. We now awake each morning to be greeted by the latest disastrous headline from Europe that accelerates the capital flight from the continental currency.

The Euro (FXE), (EUO), is deteriorating from bad to worse, with the foreign exchange community now clearly gunning for the next short term support at $1.26. Look at a ?10 note these days and it has recently printed upon it ?Abandon hope all ye who enter here.?

Traditional diversification currencies, like the Australian (FXA) and Canadian dollars (FXC) are now biting the hands that fed them, dragged down by their export commodities? pitiful performance. Hard as it is to imagine, the Ausie has been the world?s worst performing major currency this year, even underperforming the dreadful euro. Australian readers who followed my advice to pay for their summer vacations in advance at the $1.10 that prevailed at the beginning of the year are smiling. Those they didn?t are now looking for a discount caravan at a remote, dingo plagued campsite somewhere in the Outback.

The Japanese yen, the currency that everyone loves to hate, has perked up to a flight to safety bid while the rest of the world goes to hell in a hand basket. We are currently in between Bank of Japan quantitative easings there, so don?t expect this to last much longer. The tipping point into hyper debt driven, economic Armageddon there creeps ever forwards with each passing day on the calendar.

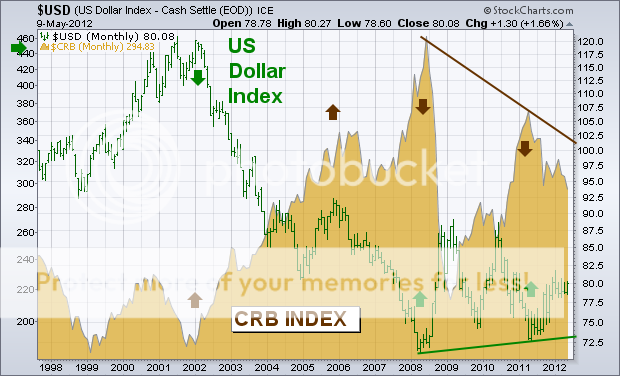

Take a look at the charts below for the US Dollar Index and it is obvious that things may soon get a whole lot worse. For starters, the dollar has only rallied back to the midpoint of a multiyear range. To get back up to the top of that range it needs to appreciate another 10%. To understand why this is a problem, look at the second chart that proves a tremendous inverse correlation between the dollar and commodities. A strong dollar always leads to falling demand for the hard stuff.

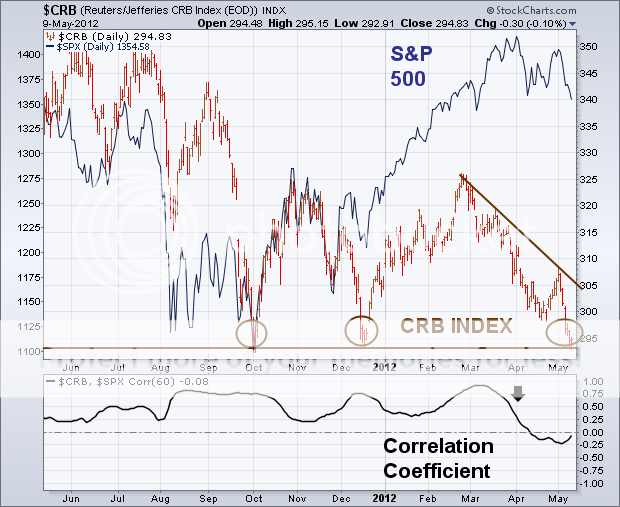

The third chart suggests that the other grotesquely overvalued asset class, US stocks, is also cruising for a bruising. Commodities led equities in this downturn by three months, as they usually do. If they break support here, then they will easily drag the (SPX) down to my medium term target of 1,275, off a heart thumping 10.3% from the recent top. If the economic data continues to worsen on a daily basis, as I have been chronicling on a daily basis for the last two months ad naseum and ad absurdum, then we have a clear shot at the fall, 2011 low at 1,060.

Oops, There Goes My Equity Portfolio

https://www.madhedgefundtrader.com/wp-content/uploads/2012/05/titanic_sinking1.jpg260400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-05-14 23:04:352012-05-14 23:04:35Strong Dollar Spells Death for Commodities

The market hung on tenterhooks all last week, waiting for the Chinese Q1 GDP figure. As recently as Thursday, rumors swept the market that the number could be as high as 9%, well above the consensus figure of 8.4%, taking the Dow up a red hot 181 points. When the flash hit in the afternoon Beijing time confirming 8.1% the equity futures flipped into sell mode. By the time the crying was over on Wall Street, virtually all of the day?s previous gains had been wiped out.

There are a few lessons to learn here for the aspiring trader. Never believe rumors, especially when they are supposed to originate from governments on the other side of the world. They are almost never true. They often originate from someone trying to unload an unfavorable position. Whoever dumped their portfolio of US stocks Thursday afternoon at the close did exceedingly well.

The second is that all is not well with the global economy. I heard China experts speculating that this quarter might be the bottom of the Middle Kingdom?s slowdown. But they are China experts to the extent that the probably ate in a Chinese restaurant once and watched one Bruce Lee movie. So much of what you hear about China in this country is nothing more than guesswork and I never pay attention to it.

I have a somewhat different take. There is no sign whatsoever that China?s growth recession is ending. Sure, domestic loan growth this month rose from ?700 billion to ?1 trillion, but much of that increase is due to carry over demand from the lunar New Year holiday of the previous month.

The biggest problem is that China?s main export customers are in distress. Its biggest, Europe, is in a serious recession and we have no idea how long that will last. The weakness of the Euro certainly says longer. Japan is falling off a cliff. Demand from a weak, 2% a year growing US is recovering, but is a shadow of what it once was. You can see that is the rapidly improving American trade surplus, which dropped from an eye popping $51 billion to $46 billion last month.

Think of the Chinese economy as a battleship. It is not going to turn on a dime. To complicate matters, China is only at the opening stages of a serious real estate bust. You can count on low end housing starts to plunge from 15 million to 5 million this year as the air comes out of the real estate bubble. That why copper has been so dead this year.

Two small easings of reserve requirements since November are not going to halt this slowdown. In fact, I think that Q2 could be even slower than the last. This is a big reason what I am looking for a prolonged ?RISK OFF? scenario over the summer.

Perhaps my old friend, Steven Roach, the former chairman of Morgan Stanley Asian and now in retirement as a Yale professor, put the best lipstick on this pig. The 8.1% report is down only 3.2% from the peak 11.3% growth rate. The 2008 crash saw the growth rate fall 8.2% from the top. We are a long way from that, thankfully.

There is a far more important message in the quarterly figure. This is not a temporary slowdown; it is a permanent one. There is never going to be a return to a continuous, white hot 11% GDP growth rate of the past. Recent years have seen the Middle Kingdom lose many of its competitive advantages.

Runaway wage inflation is rapidly eroding the country?s cost advantage. Oil over $100 a barrel is probably hurting China more than any other country. Remember, much of America?s infrastructure was built at $1 a barrel. This is why ?onshoring? will become the new economic trend of the decade (click here for ?Onshoring: The New Global Trend?).

But, as I never tire of pointing out in my meetings with the Chinese government, slowing the country down to a steady 8% rate is a good thing. This is a more sustainable and achievable rate that the country can live with. It reduces the volatility of the economy, not just for China, but for the world as a whole. Still, I often get back concerns about the country?s ?bicycle? economy that has to move forward quickly or risk falling over. These are leaders well aware that their country has a history of retirement in front of a firing squad instead of at at country club.

The whole affair also shows how important foreign developments have become for US financial markets. Look at the news flow driving markets these days and it all about China and Europe, with 5 minutes left over to wonder about whether Ben Bernanke is going to bring us QE3. That?s why you have to pay attention to someone like me who has been playing the game for 40 years and has pipelines straight into the key foreign ministries.

I think there is going to be a great buy in China sometime this year. Right when traders are jumping out of windows, managers are rending their hair, Merrill Lynch puts out a call to sell everything, and the Dow is down 2,000 pints? you want to back up the truck and load up on Chinese stocks.

This excursion should include international names like Caterpillar (CAT), Freeport McMoRan (FCX), BHP Billiton (BHP), and Rio Tinto (RIO), as well as domestic ones like China Mobile (CHL), China Telecom (CHA), and Baidu (BIDU). These are the companies that will far outperform everyone else in any sustainable Chinese recovery. You will also want to pick up some ETF?s like (FXI) and (CAF). But that time is definitely not now.

China?s Bicycle Economy

https://www.madhedgefundtrader.com/wp-content/uploads/2012/04/china-bicycle-3.jpg350247DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-04-15 23:04:142012-04-15 23:04:14China GDP Data Sends Bulls Fleeing

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.