Global Market Comments

November 27, 2020

Fiat Lux

FEATURED TRADE:

(NOVEMBER 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (CRM), (CRSP), (CVS), (SQ), (CRSP), (LUV), (GLD). (SLV), (SPY), (TMO), (UUP), (TAN), (FXA), (FXE), (FXY), (FXB), (CYB)

Global Market Comments

November 27, 2020

Fiat Lux

FEATURED TRADE:

(NOVEMBER 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (CRM), (CRSP), (CVS), (SQ), (CRSP), (LUV), (GLD). (SLV), (SPY), (TMO), (UUP), (TAN), (FXA), (FXE), (FXY), (FXB), (CYB)

Below please find subscribers’ Q&A for the November 25 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis.

Q: Is gold (GLD) still a hold?

A: Long term yes; short term no. Short term, cash is being drained out of gold in order to buy Bitcoin, just like silver. And once Bitcoin peaks, which could be today or tomorrow when it hits 20,000, then you could get a round of profit-taking and a nice little pop in gold. So, it's basically moving totally counter-cyclically to Bitcoin and the other cryptocurrencies right now.

(Note: since this webinar, Bitcoin has crashed by $3,000)

Q: A competitor of yours claims that asymptomatic transmission of COVID does not occur.

A: I would bet money that person does not have a medical degree. Asymptomatic transmission occurs in almost all diseases, so why COVID would be an exception is beyond me. I suggest that somebody is trying to sell newsletters at your expense with zero knowledge about the topic. Ask him to kiss a Covid victim. This is common in my industry where 99% of the people are crooks. This is also an example of the vast amounts of information that have been spread during an election year.

Q: Will you take a vaccine when it’s out or will you let others try it first?

A: Actually, by the time the public gets the vaccine, more than a million people will have already tried it, so I think it will be fairly safe. I am probably already the most vaccinated person on the planet; I've had flu shots every year for 40 years, so I will happily try it out. At my age, I have little to lose. And I would like to travel again, and that’s going to be a requirement for international travel. I am worried there could be long term side effects that we’ve seen with other drugs in the past, like all future children being born without arms and legs, which is what happened in the 1950s with Thalidomide.

Q: If the Senate flips to the Democrats, how do you see it affecting the market?

A: It doesn’t really affect the market overall; what it will do is affect sector reallocation. Solar, alternative energy and ESG companies do a lot better in A Democratic Senate, and energy oil companies do a lot worse. All you do is short the losers and buy the winners; it really makes no difference who wins. Most of the big conflicts over issues these days are social ones that don’t affect the market.

Q: Where do you see Tesla (TSLA) by the end of the year?

A: Well, this morning, it’s at an all-time high of $565. It looks like it wants to take a run at $600, and then we will be up 50% from where the news was announced that it was joining the S&P 500. That seems to me like a heck of a move on no real fundamental news. During this news, the market completely ignores a Model X recall and a Model Y pan from Consumer Reports. I would be inclined to take profits there or at least roll the strikes up on my options positions.

Q: What’s a good stock to play a commodity recovery?

A: You can’t do any better than Freeport-McMoRan (FCX), which I’ve been following for almost 50 years since I covered it for the Australian Financial Review newspapers.

Q: Will Salesforce (CRM) hold?

A: Yes, it’s just a matter of time before we break out to substantial new highs, and this is a stock that could double next year.

Q: What brokers do you suggest?

A: I would pick tastytrade. Click here for their site.

Q: Is CVS (CVS) a good buy?

A: I would say yes; a billion Covid-19 vaccine doses will need to be distributed next year. You can't do that without all the drug companies participating big time.

Q: Does Trump have a chance to win in his lawsuits?

A: It’s more likely that I will be elected the next Miss America; so, I wouldn’t place any bets on that. Some 30 consecutive Republican judges ruling against him does not augur well for his future.

Q: Would you buy any LEAPS here (Long Term Equity Participation Securities)?

A: Only in special one-off situations in the domestic stocks that haven’t moved in ten years. There are a lot of those out there now that I have been recommending. Those are all fertile territory for LEAPs, especially going out 2 years where you get the maximum bang for the buck and a 1,000% return. Don’t touch LEAPs in technology stocks here, and don’t touch Tesla in LEAPs.

Q: What’s your outlook on Southwest Air (LUV)?

A: I like it; it’s one of the healthiest domestic airlines most likely to come back.

Q: Are you going to update your long-term portfolio?

A: Yes, but I only update it twice a year and my next turn is on January 22. If you bought the last update on July 22, you made a fortune getting into Freeport McMoRan at $12 (it’s now $23), CRISPER Therapeutics at $80 (CRSP) (it’s now $110), and Square (SQ) at $110 (the current is $212). You can find it by logging into www.madhedgefundtrader.com, going to My Account, clicking on Global Trading Dispatch, on the drop-down menu, click on the Long-Term Portfolio tab and then clicking on the red tab for the Long-Term Portfolio. That lets you download an excel spreadsheet.

Q: Do you have any LEAPS to suggest now?

A: I only put out portfolios of LEAPS at giant market bottoms like we had in March. Then I put out lists and lists of LEAPS. At all-time highs, it’s not good LEAPS territory, except for specific names. So, if you want to get involved in that on a regular basis, I suggest you sign up for our Mad Hedge Concierge Service. There they are making millions of dollars a week right now.

Q: Where does the US dollar (UUP) go from here?

A: Straight down; the outlook for the buck couldn't be worse. I would be selling short the US dollar like crazy right now except that there are much better trades in US equities.

Q: Just to be clear, there’s no voter fraud?

A: There’s probably never been an election in US history without voter fraud on all sides; it’s just a question of who’s better at it. In the 1948 Texas Democratic Party runoff, back when the party owned Texas, Lyndon Johnson won by 87 votes out of 988,295 cast. It was later found that in five Hispanic-dominated counties that bordered Mexico, everyone had voted 100% for Johnson ….in alphabetical order. Johnson then took the seat with a 66% margin and went on to dominate the US Senate. I remember in the 1960 election, all the military absentee votes were sent flying around in circles over the Atlantic so Kennedy would win; that’s a story that’s been out there for a long time.

Q: You said stay away from other EVs except for Tesla?

A: A few have gone crazy this week, but that doesn’t mean they can actually make a car. So, you might get lucky on a quick trade on some of these, but long term, I don’t think any of the other non-Tesla EV companies are going to make it except for General Motors, which is plowing $27 billion into the sector. Even if (GM) may be able to put out a lot of cars, but they won’t be able to make very much money at it because they’re nowhere near the neighborhood of Tesla with the software where all the money is made.

Q: As the dollar gets weaker, will you expand your international stock picks?

A: Yes, we put out the first one in a long time, Ali Baba (BABA), on Monday, and we’ll be adding to that a bunch. I think the dollar could be weak for 5 or 10 years, a lot like it was in the 1970s.

Q: What’s your outlook for silver (SLV)?

A: Same as for gold (GLD). Quiet for the short term, double for the long term.

Q: Favorite names in biotech?

A: For that, you really need to subscribe to the biotech letter; we’re giving you two names a week there and all of them have done great. But another one might be Thermo Fisher (TMO), which seems to double every time I recommend it. It’s a great takeover target too.

Q: Is there any possibility of a 30% dip in the market (SPY) in 2021?

A: No, I don’t see more than a 10% dip in 2021. The tailwinds now are gale-force, generational, and will run for a decade.

Q: How do you sell the US dollar rally?

A: You buy all the ETFs that we cover in our foreign exchange sections. Those are the Australian dollar (FXA), the Euro (FXE), the Japanese Yen (FXY), the British pound (FXB), and the Chinese Yuan (CYB). Those are five ETFs that will do well on a weak dollar for the next several years.

Q: What about the Invesco Solar ETF TAN?

A: We have been recommending (TAN) for many years and it has done spectacularly well. I still love it long term, but it’s had one heck of a run; it’s up 300% from the March low. I think the entire country is about to have a solar explosion because the costs are now quite simply less than for oil. It’s an economic question. We are going to an all-Electric America.

Q: What do you think about LEAPS on gold?

A: It’s not really LEAPs territory yet, but on a two-year view, you’d have to do well on gold LEAPs.

Q: Is the Invesco DB US Dollar Index Bullish Fund (UUP) good to buy?

A: You should be looking to short the UUP. It’s a long dollar basket which we think will do terribly.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

October 27, 2020

Fiat Lux

FEATURED TRADE:

(HOW VERTEX IS CURING THE INCURABLE)

(VRTX), (PTI), (GLPG), (CRSP)

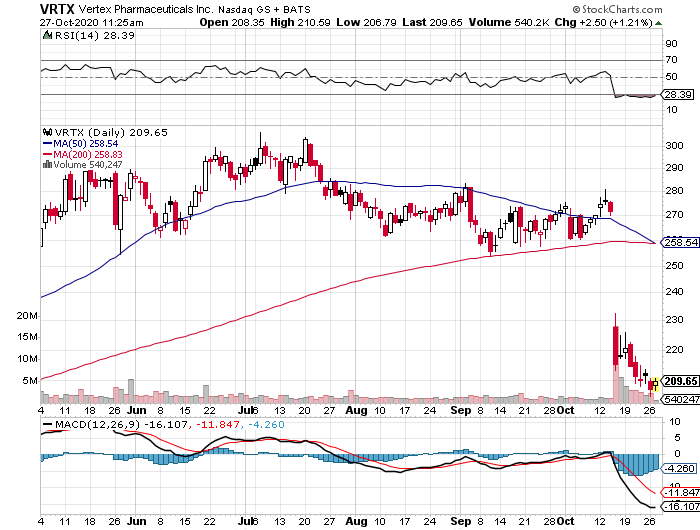

Erratic. Unpredictable. Volatile. Take your pick of the descriptions used when it comes to biotechnology stocks. Each of these adjectives can be a fitting descriptor to the industry most of the time.

However, not all biotechnology companies fall under that category. Some are reasonably stable, offering steady and increasing profits.

Vertex Pharmaceuticals (VRTX) is one of those biotechnology stocks that you can simply buy and hold for over a decade without losing any sleep.

One of the key factors in Vertex’s success is its monopoly on the cystic fibrosis (CF) market.

CF is a rare and life-threatening genetic disease that affects a patient’s digestive system and lungs. To date, there is no cure for this condition that overshadows the lives of 68,000 individuals in the US and the EU. However, there are treatment options for it.

Vertex developed the first-ever FDA-approved drug, Kalydeco, for the condition. As expected, it gained the much-coveted head start that led to its dominance today.

Its closest rivals, Proteostasis Therapeutics (PTI) and Galapagos NV (GLPG), are years away from ever catching up to the Massachusetts-based biotechnology stalwart. Neither has an approved drug as of today.

Since the approval of Kalydeco in 2012, Vertex stock has been enjoying an upward trajectory. With the recent addition of another CF blockbuster, Trikafta, the company is anticipated to keep its momentum.

From the moment Trikafta was released to the market, Vertex’s revenue and bottom line showed impressive growth. The drug, which is a triple combination therapy, is projected to capture almost 90% of the CF market worldwide.

Needless to say, Vertex has made it in the shade for at least the next 5 years, thanks to its CF market dominance.

In its second quarter earnings report, Vertex showed a 62% jump in its revenue year over year to hit $1.52 billion. Its net income of $837 million demonstrated a whopping 213% increase compared to the same period in 2019.

As anticipated, the star of the show was Trikafta.

The drug raked in $918 million in the second quarter alone – an amount higher than the combined sales of all the drugs in Vertex’s product line and an impressive growth from the $420 million it contributed last year.

As Vertex’s bottom line grew, its margins showed substantial improvement as well. Its operating margin for the second quarter of 2020 is at 57% compared to 44% during the same quarter last year.

With Vertex’s key metrics topping expectations, the company changed its 2020 revenue guidance from $5.7 billion to $5.9 billion, showing off a noteworthy increase from the $4 billion in sales it reported in 2019.

Although its CF pipeline has a number of promising candidates, Vertex is also looking outside the market for additional avenues of growth.

One of the most promising and exciting partnerships it forged in the past decade is with gene-editing company CRISPR Therapeutics (CRSP).

Just looking at this collaboration makes it clear that Vertex is once again playing the long game.

What we know so far is that the two companies are working on a treatment, called CTX001, for rare genetic blood disorders sickle cell disease and transfusion-dependent beta-thalassemia.

They are also developing two potential treatments for alpha-1 antitrypsin deficiency (AATD), which is a rare genetic liver and lung disorder that is similar to CF.

Detractors might point out that Vertex is a pricey stock. However, this biotechnology company currently has $71.2 billion in market capitalization.

More notably, it has no debt and holds $5.5 billion in cash. That puts the true value of Vertex at roughly $65.7 billion.

I believe that the biotechnology company’s overall outlook more than does justice for its valuation.

Granted that it is trading at 11 times its revenue and 26 times its adjusted EPS, its consistent performance and promising future ensure that its investors will be getting more bang for their buck.

In a word, Vertex remains a first-rate biotechnology stock to buy.

Mad Hedge Biotech & Healthcare Letter

September 24, 2020

Fiat Lux

(PLAY YOUR CARDS RIGHT WITH MODERNA)

(MRNA), (PFE), (AZN), (BNTX), (JNJ), (MRK), (VRTX), (CRSP)

The COVID-19 race is entering the home stretch, and it could only be a matter weeks before the world finds out which among the leading vaccine candidates will work.

For months, Moderna (MRNA) has been dubbed as the leader of the pack, with the company’s shares reaping the rewards thanks to this year’s wild growth and promising clinical results.

Now, it looks like Moderna is on the verge of officially claiming the crown as promising reports surfaced from its late-stage clinical trials.

If the Moderna’s COVID-19 vaccine candidate, called mRNA-1273, is proven to be at least 70% effective, the company will immediately ask for an emergency authorization to use it on high-risk patients.

Like Pfizer (PFE), Moderna is also expecting results to come as early as October. With potential delays in the trials, the company thinks the data would be released by November at the latest.

Moderna is also looking into building footprints outside the United States.

Part of its efforts to expand its potential market reach for mRNA-1273, Moderna opened a commercial hub – its first ever – in Switzerland, where it has already been collaborating with Swiss drug manufacturer Lonza (SWX: LONN).

This is a good move for Moderna.

After all, Europe presents a substantial market for the COVID-19 vaccine. For context, the European Union has over 446 million people while the US only has 328 million.

To date, Moderna has agreed to supply 100 million doses of its COVID-19 vaccine to the US government for up to $1.525 billion. The contract also provides for an optional additional 400 million doses, depending on mRNA-1273’s performance in the trials.

Meanwhile, Moderna already secured a deal with the Swiss federal government to deliver 4.5 million of mRNA-1273.

While it has yet to announce a similar deal with the rest of the EU, the company is reported to be in the advanced stages of its negotiations with other member countries, where it is estimated to provide an additional 160 million doses.

Overall, the global manufacturing projection for Moderna falls somewhere between 500 million and 1 billion doses starting in 2021.

Looking at the agreements, we can conservatively say that mRNA-1273 could rake in $12.4 billion in sales for Moderna by 2022.

Despite the current payment plans implying that each dose of Moderna’s vaccine would only cost $15.25, the company already received government funding of roughly $2.5 billion.

Taking those expenses into account, the actual value would be somewhere between $25 and $30 per dose.

In comparison, Pfizer’s vaccine candidate with BioNTech (BNTX) is estimated to cost less than $19.50 per dose while Johnson & Johnson (JNJ) announced that it will offer its vaccine at $10 per dose.

Meanwhile, AstraZeneca’s (AZN) candidate with Oxford University is expected to be even cheaper at $2.96 to $4 per dose.

With its COVID-19 vaccine rivals offering decidedly cheaper options, Moderna will need to leverage its first-mover advantage if it hopes to fight for a decent market share.

Outside COVID-19 vaccine efforts, Moderna has a rich pipeline, with 23 candidates distributed over 22 programs and 6 modalities.

Aside from the urgent need to offer a vaccine to the world, there is another reason why Moderna is focusing on the COVID-19 program right now.

If proven successful, the program can be used to validate another experimental vaccine, called mRNA-1647, which targets congenital cytomegalovirus infection.

Although CMV is identified as one of the leading causes of birth defects in the US, there remains no approved vaccine for it.

However, there is a catch.

Moderna will not be able to reap the full benefits of the CMV vaccine.

In fact, it will only be able to receive 50% of its profits if it becomes successful since mRNA-4157 is being developed alongside Merck (MRK).

The idea is for the drug to boost the oncology sector of Merck, with the goal of finding another blockbuster like the melanoma drug Keytruda.

As impressive as the CMV vaccine is as a product to launch in the market, there is a huge possibility that Moderna would not necessarily benefit from a large windfall because of it.

Aside from Merck, Moderna is also working with another biopharmaceutical giant and competitor in the COVID-19 vaccine race: Vertex (VRTX).

Moderna and the Massachusetts-based giant are collaborating to develop a treatment for cystic fibrosis, a niche that Vertex has dominated for years.

This is actually their second collaboration, but this project seems a tad more ambitious than the earlier one: Moderna and Vertex are working to develop a one-time treatment for cystic fibrosis using mRNA technology.

Basically, the two companies want to use gene-editing techniques to modify a patient’s DNA and correct the cells that cause cystic fibrosis.

The collaboration will span 3 years, with Vertex paying Moderna $75 million upfront. The smaller biotechnology company is also eligible for an additional $380 million in milestone payments plus royalties.

Notably, this is not the first cystic fibrosis treatment collaboration that Vertex formed with gene-editing companies.

Earlier this year, the company also secured a license option with CRISPR Therapeutics (CRSP) to work on practically the same thing.

Clearly, Vertex is hedging its bets on two potential options with this second partnership with Moderna.

Thanks to its trailblazing COVID-19 vaccine candidate, Moderna has become one of the most sought-after stocks of 2020, with its year-to-date growth reaching a stunning 360% last July.

Despite the temptation to bet big on Moderna stocks, bear in mind that early leaders like this biotechnology company will be facing incredible pressure from pharmaceutical titans like Pfizer, Johnson & Johnson, and AstraZeneca – all of which have the capacity to meet the manufacturing and distribution demands across the globe.

At best, a company with Moderna’s size would probably receive a slice of the market in the early days.

At worst, it might struggle to keep a foothold as stronger and larger competitors flood the market with cheaper but equally effective alternatives.

Nonetheless, this is not to say that you should completely avoid smaller biotechnology companies just because they are too small to compete with the larger fish.

Rather, I think it would simply be prudent to invest based on each player’s proven ability and outlined plans to meet the demand at a mass scale.

Doing so would guarantee that you not only limit your risks but also allow you to reap the rewards of successful vaccine deployment. If you play your cards right, then you might even get a handful of different COVID-19 vaccine winners in your back pocket.

Mad Hedge Biotech & Healthcare Letter

September 10, 2020

Fiat Lux

Featured Trade:

(CAN CRISPR STOP THE SILENT KILLER?)

(CRSP), (VRTX), (EDIT), (NTLA)

Obesity has virtually tripled worldwide since 1975.

In 2019 alone, the World Health Organization classified 38 million children under 5 years old as overweight or obese.

More alarmingly, obesity has been dubbed as the “silent killer” because it is one of the leading factors that cause premature deaths.

In 2017, 4.7 million or 8% of global deaths were linked to this condition.

For context, the number of deaths caused by obesity is 4 times the fatality rate from road accidents and almost 5 times the number of those who died from HIV/AIDS.

Right now, 39% of adults across the globe are considered overweight and 13% are obese.

By 2030, nearly half the adult population of the United States is expected to be suffering from obesity.

Now, we might have the answer to this “silent killer:” CRISPR gene editing.

A recent Harvard study showed that CRISPR gene editing can be used to engineer cells to avoid weight gain and even potentially stop the onset of obesity-related diseases like diabetes.

The solution is straightforward.

The scientists will convert the body’s white fat, which is the “bad fat,” into brown fat or the "good fat.”

Brown fat is known as the healthy fat because it produces heat for the body by burning calories. Meanwhile, white fat tends to build up and leads to obesity.

Through CRISPR gene editing, the white fat is transformed into brown fat. This will then be burned by the body and used as an energy source, which can also result in weight loss.

So far, the technology proved to be successful in mice which were put on a high-fat diet.

What CRISPR targets is a gene for a protein called UCP1, which is distinctly found in brown fat.

The function of UCP1 is to turn chemical energy into heat.

Using the UCP1, the researchers created cells that closely resembled brown fat cells. These are called human brown-like cells or HUMBLE cells.

The manufactured HUMBLE cells are then transplanted into the mice with weakened immune systems. These mice were also fed with a high-fat diet.

Upon observation, they found that the modified cells actively helped in preventing the progression of obesity in mice and even showed improvements in the metabolic function of the animals.

Over the course of 12 weeks, the mice given white fat cells continued to gain weight while those transplanted with the HUMBLE cells showed weight loss. The latter also showed higher sensitivity to insulin, indicating that they could be protected against diabetes.

This is where it gets interesting because the technique can ultimately lead to cell therapies not only for obesity but also other metabolic disorders.

In the future, the process could evolve into something as convenient as removing a small amount of a patient’s white fat and having that engineered into brown-like fat and re-implanted to the same person’s body.

Apart from that, the HUMBLE cells also appear to send a chemical trigger to the existing brown fat stored in the mice’s own bodies, stimulating them to burn more energy.

This means that a simpler treatment method could be explored in which the experts could mimic the signal to activate the patient’s own brown fat. This will no longer require re-engineering the white fat and re-implanting it, making the entire treatment extremely straightforward.

The release of this study has profound implications to the total available market for CRISPR gene editing technology.

In the US alone, over 34 million are suffering from diabetes. The medical spending and loss of work wages linked to this is valued at roughly $327 billion annually.

If this technology proves to be effective in boosting a patient’s insulin sensitivity, then it could open an exponentially huge market.

Aside from diabetes, obesity is also considered a major risk factor in certain types of cancer, fatty liver and kidney disease, osteoarthritis, and even pregnancy problems.

This study is another example of how gene editing can be utilized to find treatments for untreatable conditions in the past years.

With this groundbreaking potential, it is no wonder investors are lining up to get their hands in biotechnology stocks in the gene editing sector.

The most widely known gene editing stock is CRISPR Therapeutics (CRSP).

With a market capitalization of $5.72 billion, this company is the only one in its field with actual treatments set for launch in the market soon.

One is a rare genetic disease treatment called CTX-001. Every year, about 60,000 people are born with this condition, causing anemia, lifelong pain, and early death. The other treatment is CTX-100, which is geared towards cancer patients.

Compared to its competitors like Editas Medicine (EDIT), which has a market capitalization of $1.82 billion, and Intellia Therapeutics (NTLA) with $1.03 billion, CRSP has a financial runway that can be reassuring to its investors.

CRSP also has minimal debt and a beneficial partnership with healthcare giant Vertex Pharmaceuticals (VRTX). This makes it one of the most attractive gene editing stocks out today.

Nonetheless, buying early stage companies, especially in the biotechnology sector, can be like oil wildcatting back in the 1930s. The key is to spread your bets broad enough to boost your chances of finding a gusher.

If this CRISPR gene editing technology works to treat obesity and even diabetes, then it could revolutionize the medical field.

While it’s still wise to exercise caution when investing in gene editing stocks, this technology undoubtedly embodies how the future of medicine looks like.

Mad Hedge Biotech & Healthcare Letter

August 27, 2020

Fiat Lux

Featured Trade:

(THE FUTURE OF GENE-EDITING TECHNOLOGY)

(CRSP), (VRTX), (BAYRY), (NTLA), (NVS), (EDIT), (BMY)

There are wise investments, and there are excellent investments.

CRISPR Therapeutics (CRSP) has been proving to qualify in the latter category.

In fact, the company is considered one of the best biotechnology stocks to own during these turbulent times. It is estimated to dominate the gene-editing therapy market, which will reach roughly $11.2 billion in worth by 2025.

Four years ago, CRISPR Therapeutics stock was trading at $14.09. Today, each share is worth $90.35.

This means that CRISPR Therapeutics biotechnology company has been trading for 540% more than its value since it went public in 2016.

This is a remarkable pace for a biotechnology stock, with CRISPR Therapeutics raking in $289 million in trailing 12-month revenue thanks to strategic collaborations.

It even has a decent $890 million stored in cash, with the company reporting a 16% profit margin despite not having any treatment or drug available in the market yet.

More importantly, CRISPR Therapeutics holds a novel position of being under absolutely zero pressure to push a product out the door.

Nonetheless, the investor confidence in CRISPR Therapeutics relies heavily on the company’s leading position in the groundbreaking world of gene-altering treatments.

Basically, the company specializes in creating and developing therapies for genetic diseases with either no cure available or require frequent transfusions.

Looking at the results of the recent tests on the company’s pipeline candidates, CRISPR Therapeutics is projected to transform into a household name in the next five to 10 years.

CRISPR Therapeutics has five cell therapy candidates in the clinical stage. Three of these target immuno-oncology, while the two are designed for genetic blood disorders like beta-thalassemia sickle cell disease.

Among the five, the most advanced is CRISPR Therapeutics’ collaborative work with Vertex Pharmaceuticals (VRTX) on beta-thalassemia therapy CTX001.

This candidate received a fast-track designation from the FDA, with CRISPR Therapeutics releasing promising preliminary results recently.

However, it is another Vertex collaboration drug that actually yielded CRISPR Therapeutics $25 million at the beginning of 2020.

The drug, which is developed to treat muscular dystrophy disorder, is expected to account for approximately $800 million in future milestone payments in the next few years.

Although the genetic blood disorder programs are raking in millions these days, CRISPR Therapeutics’ cancer treatment pipeline offers an even greater potential in terms of stable revenue streams.

The company is utilizing a gene-editing platform, called CRISPR/Cas9, to create “off the shelf” novel chimeric receptor (CAR) T-cells.

If successful, then CRISPR Therapeutics can use a single batch to treat a broad group of cancer patients.

This is groundbreaking because the typical way involves harvesting T-cells from the patients, tailor-fitting the therapies, then re-introducing the cells to the body.

With this technology, CRISPR Therapeutics can easily cover more markets and offer regular treatments for patients within shorter intervals.

That’s why it comes as no surprise that a major biotechnology player like Bayer (BAYR) reached out to the smaller company for a collaboration.

The CAR T-cell market is projected to hit $8.4 billion by 2027, with an estimated compound annual growth rate of roughly 15%.

Specifically, CRISPR Therapeutics expects this product to become a leader in the solid tumor cancer therapy space, pegged to reach $425 billion by 2027.

However, it is not only CRISPR Therapeutics that is widely known in the gene-editing sector.

To date, the company has two close competitors: Intellia Therapeutics (NTLA), which has a strategic partnership with Novartis (NVS), and Editas Medicine (EDIT), which is working alongside Bristol Myers-Squibb (BMY).

Both are also using the CRISPR/Cas9 technology to come up with treatments.

Although Intellia Therapeutics and Editas went public the same year as CRISPR Therapeutics, neither has performed quite as well.

For perspective, CRISPR Therapeutics currently has a market capitalization of $6.3 billion. In comparison, Intellia Therapeutics has $1.13 billion while Editas Medicine has $2.13 billion.

Keep in mind though that clinical-stage companies, particularly in the biotechnology sector, are inherently risky plays.

Among the companies in the space, CRISPR Therapeutics is emerging to be a solid bet not only from a cash perspective but also based on its strong pipeline and profitable collaborations.

Overall, CRISPR Therapeutics is still considered a high-risk option.

Hence, the safest way to invest is to build a carefully hedged portfolio filled with well-researched gene-editing stocks. This will minimize your risks and guarantee your exposure to the upside in case any of your chosen biotechnology companies makes it to the market with a groundbreaking therapy.