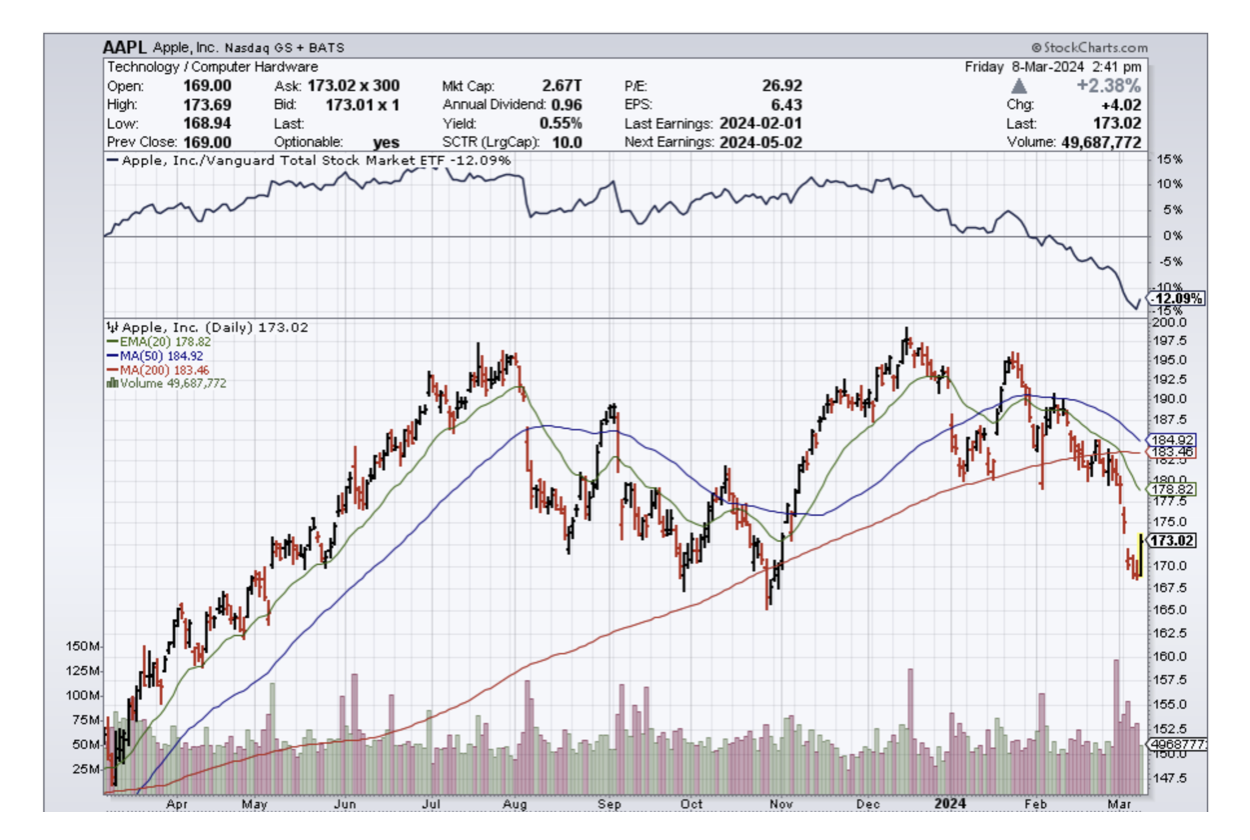

It’s no longer Apple’s world.

Times have changed.

Management at Apple including CEO Tim Cook need to get with the times or else they risk being left behind.

Large existential risks aren’t only felt by Apple, most of the tech sector risk being left behind by the AI bandwagon.

If there was any inkling that I might be wrong about this then explain the latest data point about Apple’s lackluster sales in Asia.

Sales of Apple’s iPhone plunged in China by 24% year over year as Apple faced stiff competition from local smartphone firms like Huawei, Oppo, Vivo and Xiaomi.

Apple came under particular pressure from Chinese tech giant Huawei, whose consumer business is experiencing a resurgence in China after the launch of its Mate 60 smartphone.

Several rival Chinese smartphone companies also logged drops in their unit sales in the six-week period, but the declines were less pronounced than that of Apple.

The best-performing smartphone brands for the first six weeks were Huawei and its spinoff Honor, which branched out of the tech giant in 2020 as a result of U.S. sanctions.

Huawei smartphone unit shipments rose 64% year over year in the first six weeks of 2024.

Apple is facing a backbreaking environment in its cash cow China.

Local Chinese smartphone makers have caught up and make a pretty nice version of a smartphone comparable to the iPhone including a reinvigorated Huawei.

Customers flocked to iPhones, once Huawei’s phones lost their competitiveness due to the lack of 5G and no cutting-edge semiconductors.

Losing the China market is a big blow to Apple’s management as deglobalization picks up speed.

Even more worrying is why isn’t Apple hopping on the AI bandwagon?

They risk being left behind as the “iPhone company.”

It’s not emerging as one of the largest risk to Apple’s strategic future.

They did well with last generation’s technology, but they look gradually misplaced for the next round of technological modernizations.

I haven’t heard much of what they are doing in AI, and they had to fire their team that worked on the Apple car.

No doubt that Apple shareholders are starting to question what management has up its sleeves and before it was ok to return to the well with iPhone sales growing.

However, we have clearly entered a paradigm shift where the iPhone well has run dry and shareholders are expecting more.

If Tim Cook can’t figure it out then large investors like Warren Buffett could start to unload shares in batches which could demoralize the stock in the short-term.

For now, I do believe Apple is worth a trade to the upside because it’s so beaten down.

It shocking that we have gotten to this point with Apple, but tech companies are all at risk of extinction unless they evolve with the times.

For the first time in a long time, it’s right to question whether to hold Apple shares for the long haul.