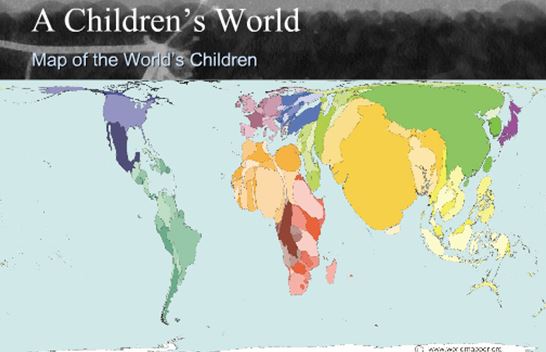

You can never underestimate the importance of demographics in shaping long-term investment trends, so I thought I’d pass on these two highly instructive maps.

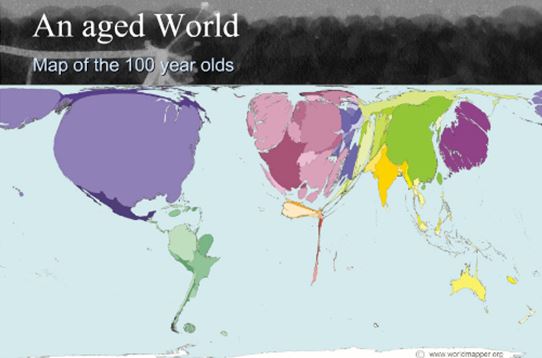

The first shows a map of the world drawn in terms of the population of children, while the second illustrates the globe in terms of its 100-year-olds.

Notice that China and India dominate the children’s map. Kids turn into consumers in 20 years, stay healthy for a long time, and power economic growth.

The US, Japan, and Europe shrink to a fraction of their actual size on the children’s map, so economic growth is in a long-term secular downtrend there.

There is more bad news for the developed world on the centenarian’s map, which shows these countries ballooning in size to grotesque, unnatural proportions.

This means higher social security and medical costs, plunging productivity, and falling GDP growth.

The bottom line is that you want to own equities and local currencies of emerging market countries and avoid developed countries like the plague.

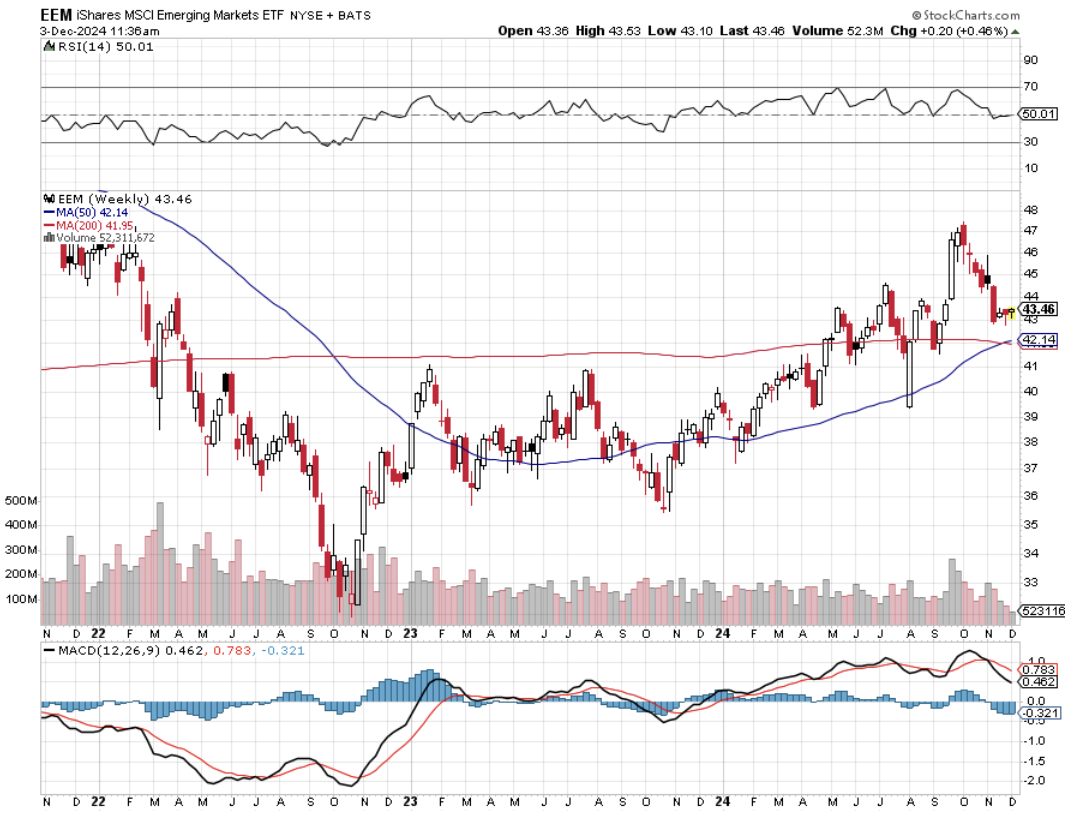

This is why we saw tenfold returns from SOME emerging markets (EEM) over the past ten and why there is an irresistible force pushing their currencies upward (CYB) over the long term.

Use any major meltdowns this year to increase your exposure to emerging markets, as I will.

Would You Rather Own Them?

Or Them?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/Children.jpg297369Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-12-04 09:02:342024-12-04 10:39:18America's Demographic Time Bomb

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE HIDDEN AI IN YOUR LIFE),

(SPX), (NVDA), (CSCO), (LEN), (DHI), (KBH), (SMCI), (BRK/B), (META), (AAPL), (GOOGL), (TSLA), (JNK), (HYG), (FXA), (FXE), (FXB), (FXC), (EEM), (IWM)

It's great to be back in California, even just temporarily.

Driving down to visit a Concierge client, the weather is hot and dry, the scenery is spectacular. What were once endless hills of dry grass are now countless miles of vineyards. Boy, has the Golden State changed a lot since 1952.

The vines are heavy with grapes. I stopped by and picked a purple bunch to test out the fruit. The grapes were rich and sweet. It looks like 2024 is going to be a good vintage. No wonder there is a wine glut.

It's going to be a vintage year for Mad Hedge performance as well. We picked up a welcome +3.74%in the testing month of August, +33.61%so far in 2024, and +711.32%since inception.

The harder I work, the luckier I get.

Which raises the most important question of the day: Did September just happen in August? The price action we saw last month is certainly reminiscent of many recent faith-testing Septembers and Octobers.

If that is the case, then it could be off to the races from now. Except this time, it won’t be just a Magnificent Seven rally. It will be an everything rally as the bull broadens out to include all interest rate sectors, which is almost everything.

(SPX) 6,000 by yearend looks like a piece of cake.

The bottom line for all of this is that investors and the markets are still wildly underestimating the impact artificial intelligence will have on our futures, and therefore stock prices. Publishing the Mad Hedge AI Letter three times a week (click here for the link), I can see AI sneaking into every aspect of our lives without our knowledge.

I visited my doctor the other day and they asked for my Medicare card. I didn’t have it because there is no use for this US government ID in Europe from where I just returned. The receptionist said, “Don’t worry, may I have your phone please?” She went into my photos app, searched for “Medicare” and there it appeared instantly. Apple had surreptitiously installed an AI search function on my phone without even telling me.

Try it!

What we are witnessing is the greatest capital spending binge since WWII 83 years ago, when in three short years, the US produced 297,000 aircraft, 193,000 artillery pieces, 86,000 tanks, and two million army trucks. It also double-tracked all east-west rail lines and created from scratch four atomic bombs.

And you want to short that???

The indexes certainly have plenty of room to run. Since the 2020 pandemic bottom, virtually all money has gone into big tech and out of the rest of the market, generating net outflows out of equities and into bonds. What happens when you get net inflows into big tech AND the rest of the market? Markets go up a….lot.

Dow 240,000 here we come.

Now for the challenging chore of sector picking.

Bonds (TLT) are usually the first pick at the beginning of any interest rate-cutting cycle. However, this has been the best telegraphed interest rate cut in history so most of the juice has already been squeezed out of this one. The (TLT) has moved a prolific $18 off the $82 bottom with no interest rate cuts at all. So there might be $5 or $10 of upside left this year, but no more.

Derivative high-yield plays have much more to offer. Those would include junk bonds (JNK), (HYG), BB-rated loans (SLRN), and REITS like the Vornado Realty Trust (VOR), my favorite Crown Castle International (CCI), and Health Properties (DOC).

Utilities usually do well in falling interest rate cycles as they are such big borrowers. In this basket, you can throw NextEra Energy (NEE), Southern Company (SO), and Duke Energy (DUK).

Falling rates also reliably deliver a weak US dollar, so buy every foreign currency play out there (FXA), (FXE), (FXB), (FXC). Also, buy foreign stock markets like the (EEM).

And then there are always big borrowing small caps (IWM), poor performers for the last decade which can always use the life jackets of falling interest rates. Keep in mind that 40% of small caps are regional banks and another 40% are money losers.

And then there are the old reliables. Any of the Magnificent Seven will probably work if you can get them on any selloff like we had on August 5.

So far in August, we are up by +2.67%.My 2024 year-to-date performance is at +33.61%.The S&P 500 (SPY) is up +18.23%so far in 2024. My trailing one-year return reached +52.25. That brings my 16-year total return to +710.24.My average annualized return has recovered to +51.91%.

I executed no trades last week and am maintaining a 100% cash position. I’ll text you next time I see a bargain in any market. Now there are none. I am running one short in Tesla (TSLA).

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 49 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of +74.24%.

Try beating that anywhere.

NVIDIA Dives on Fabulous Earnings, one of the greatest “Buy the rumor, sell the news” moves of all time. The stock dropped to $25, or 17.85% off its all-time high. Production snags with its much-awaited Blackwell chips are to blame. The company’s quarterly met or beat analysts’ estimates on nearly every measure. But Nvidia investors have grown accustomed to blowout quarters, and the latest numbers didn’t qualify. Buy (NVDA) on this dip.

PCE Rises a Modest 02% in July. That is the so-called core personal consumption expenditures price index, which strips out volatile food and energy items, according to Bureau of Economic Analysis data out Friday. On a three-month annualized basis — a metric economists say paints a more accurate picture of the trajectory of inflation — it advanced 1.7%, the slowest this year

Pending Home Sales Drop 5%, and 8.5% YOY, on a signed contracts basis. Many buyers are waiting until after the presidential election to make a move. Pending home sales fell in all four regions last month. The positive impact of job growth and higher inventory could not overcome affordability challenges and some degree of wait-and-see related to the upcoming U.S. presidential election.

Sales of new U.S. single-family homes rocketed by 10.6%, their highest level in more than a year in July. A drop in mortgage rates boosted demand, offering more evidence that the housing market is recovering. Sales reached a seasonally adjusted annual rate of 739,000 units last month, the highest level since May 2023. It was also the sharpest increase in sales since August 2022. New home sales are counted at the signing of a contract. Buy homebuilders on dips (LEN), (DHI), (KBH).

US GDP Reaccelerates to 3.0% Growth in Q2, up from the previous estimate of 2.8%, according to the Bureau of Economic Analysis. Stronger consumer spending more than offset other categories. Can’t beat the USA.

Weekly Jobless Claims Remain Unchanged at 231,000, down 2,000. After being inflated by weather and seasonal factors in July, initial jobless claims in August are stabilizing at a slightly lower level, another indication that layoffs remain low.

Is Costco (CSCO) the Next Stock Split? Costco, which has risen nearly 40% since the start of 2024, is a potential candidate. Given the company’s share price—over $900 as of Tuesday—and the trend among other retailers with similarly high prices to split.

Hindenburg Research Attacks Super Micro, alleging "accounting manipulation" at the AI server maker, the latest by the short seller whose reports have rocked several high-profile companies. Close ties with chip giant Nvidia have allowed Super Micro, known for its liquid cooling technology for high-power semiconductors, to capitalize on the surge in demand for AI servers.

Though revenue has surged, margins have taken a hit recently due to the rising costs of server production and pricing pressure from rivals including Dell. Avoid (SMCI).

Berkshire Hathaway Tops $1 Trillion Market Cap, a long-time Mad Hedge recommendation. It’s the first nontech company ever to do so, even though (BRK/B) has a major holding in Apple (AAPL). Keep buying the big dips. The stock has rallied this year on strong insurance results and economic optimism. The Omaha, Nebraska-based company joins the ranks of a small group to crack the milestone, dominated by technology giants like Alphabet Inc. (GOOGL), Meta Platforms Inc. (META) and Nvidia Corp. (NVDA).

S&P Case Shiller Hits New All-Time High in June. Prices nationally rose 5.4% in June from the year prior. An index measuring prices in 20 of the nation’s large metropolitan areas gained 6.5% from the year prior. On an unadjusted basis, it was the national index’s fourth consecutive all-time high. Prices in New York, San Diego, and Las Vegas grew the most, with year-over-year gains ranging from 8.5% and 9%, while those in Portland, Ore., Denver, Colo., and Minneapolis grew the least.

Canada Imposes 100% Tariff on Chinese EVs. The problem for Tesla is that they had been supplying the Canadian market from their China factory. The supply can be replaced with US-made cars but at a much higher cost. Tesla sold off $8 on the news. Sell rallies in (TSLA).

Is the US Tipping into Recession? A continued drop in job openings will translate into faster increases in unemployment, an argument in favor of the Fed beginning to cut interest rates to guard the labor market. The next jobs reports could be crucial. Policymakers face the dilemma of two risks: being too slow to ease policy, potentially causing a 'hard landing' with high unemployment ... or cutting rates prematurely, leaving the economy vulnerable to rising inflation

Yield Chasers Post Record Demand for Junk Bonds. That’s helped make 2024 the busiest year for the issuance of new corporate high-yield bonds, with $357 billion sold so far, since the easy money days during the pandemic. Issuance of US leveraged loans, meanwhile, is running at its fastest pace on record. Buy (JNK) and (HYG).

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 2 we have Labor Day. All US markets will be closed. On Tuesday, September 3 at 6:00 AM EST, the ISM Manufacturing PMI is released.

On Wednesday, September 4 at 7:30 PM, the JOLTS Job Openings Report is printed.

On Thursday, September 5 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the ADP Employment Report.

On Friday, September 6 at 8:30 AM, the August Nonfarm Payroll Report is released. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, having visited and lived in Lake Tahoe for most of my life, I thought I’d pass on a few stories from this historic and beautiful place.

The lake didn’t get its name until 1949 when the Washoe Indian name was bastardized to come up with “Tahoe”. Before that, it was called the much less romantic Lake Bigler after the first governor of California.

A young Mark Twain walked here in 1863 from nearby Virginia City where he was writing for the Territorial Enterprise about the silver boom. He described boats as “floating in the air” as the water clarity at 100 feet made them appear to be levitating. Today, clarity is at 50 feet, but it should go back to 100 feet when cars go all-electric.

One of the great engineering feats of the 19th century was the construction of the Transcontinental Railroad. Some 10,000 Chinese workers used black powder to blast a one-mile-long tunnel through solid granite. They tried nitroglycerine for a few months but so many died in accidents they went back to powder.

The Union Pacific moved the line a mile south in the 1950s to make a shorter route. The old tunnel is still there, and you can drive through it at any time if you know the secret entrance. The roof is still covered with soot from woodfired steam engines. At midpoint, you find a shaft to the surface where workers were hung from their ankles with ropes to place charges so they could work on four faces at once.

By the late 19th century, every tree around the lake had been cut down for shoring at the silver mines. Look at photos from the time and the mountains are completely barren. That is except for the southwest corner, which was privately owned by Lucky Baldwin who won the land in a card game. The 300-year-old growth pine trees are still there.

During the 20th century, the entire East Shore was owned by one man, George Whittell Jr., son of one of the original silver barons. A man of eclectic tastes, he owned a Boing 247 private aircraft, a custom mahogany boat powered by two Alison aircraft engines, and kept lions in heated cages.

Thanks to a few well-placed campaign donations, he obtained prison labor from the State of Nevada to build a palatial granite waterfront mansion called Thunderbird, which you can still visit today (click here ). During Prohibition, female “guests” from California crossed the lake and entered the home through a secret tunnel.

When Whittell died in 1969, a Mad HedgeConcierge Client bought the entire East Shore from the estate on behalf of the Fred Harvey Company and then traded it for a huge chunk of land in Arizona. Today the East Shore is a Nevada State Park, including the majestic Sand Harbor, the finest beach in the High Sierras.

When a Hollywood scriptwriter took a Tahoe vacation in the early 1960s, he so fell in love with the place that he wrote Bonanza, the top TV show of the decade (in front of Hogan’s Heroes). He created the fictional Ponderosa Ranch, which tourists from Europe come to look for in Incline Village today.

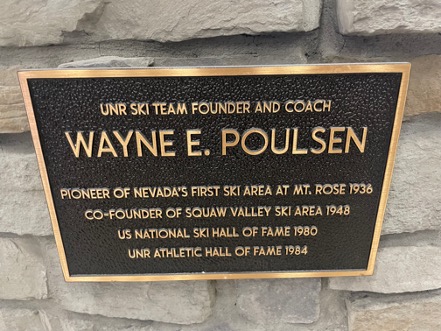

In 1943, a Pan Am pilot named Wayne Poulson who had a love of skiing bought Squaw Valley for $35,000. This was back when it took two days to drive from San Francisco. Wayne flew the China Clippers to Asia in the famed Sikorski flying boats, the first commercial planes to cross the Pacific Ocean. He spent time between flights at a ranch house he built right in the middle of the valley.

His wife Sandy bought baskets from the Washoe Indians who still lived on the land to keep them from starving during the Great Depression. The Poulson’s had eight children and today, each has a street named after them at Squaw.

Not much happened until the late forties when a New York Investor group led by Alex Cushing started building lifts. Through some miracle, and with backing from the Rockefeller family, Cushing won the competition to host the 1960 Winter Olympics, beating out the legendary Innsbruck, Austria, and St. Moritz, Switzerland.

He quickly got the State of California to build Interstate 80, which shortened the trip to Tahoe to only three hours. He also got the state to pass a liability limit for ski accidents to only $2,000, something I learned when my kids plowed into someone, and the money really poured in.

Attending the 1960 Olympic opening ceremony is still one of my fondest childhood memories, produced by Walt Disney, who owned the nearby Sugar Bowl ski resort.

While the Cushing group had bought the rights to the mountains, Poulson owned the valley floor, and he made a fortune as a vacation home developer. The inevitable disputes arose and the two quit talking in the 1980’s.

I used to run into a crusty old Cushing at High Camp now and then and I milked him for local history in exchange for stock tips and a few stiff drinks. Cushing died in 2003 at 92 (click here for the obituary)

I first came to Lake Tahoe in the 1950s with my grandfather who had two horses, a mule, and a Winchester. He was one-quarter Cherokee Indian and knew everything there was to know about the outdoors. Although I am only one-sixteenth Cherokee with some Delaware and Sioux mixed in, I got the full Indian dose. Thanks to him I can live off the land when I need to. Even today, we invite the family medicine man to important events, like births, weddings, and funerals.

We camped on the beach at Incline Beach before the town was built and the Weyerhaeuser lumber mill was still operating. We caught our limit of trout every day, ten back in those days, ate some, and put the rest on ice. It was paradise.

During the late 1990’s when I built a home in Squaw Valley I frequently flew with Glen Poulson, who owned a vintage 1947 Cessna 150 tailwheel, looking for untouched high-country lakes to fish. He said his mother had been lonely since her husband died in 1995 and asked me to have tea with her and tell her some stories.

Sandy told me that in the seventies she asked her kids to clean out the barn and they tossed hundreds of old Washoe baskets. Today Washoe baskets are very rare, highly sought after by wealthy collectors, and sell for $50,000 to $100,000 at auction. “If I had only known,” she sighed. Sandy passed away in 2006 and the remaining 30-acre ranch was sold for $15 million.

To stay in shape, I used to pack up my skis and boots and snowshoe up the 2,000 feet from the Squaw Valley parking lot to High Camp, then ski down. On the way up I provided first aid to injured skiers and made regular calls to the ski patrol.

After doing this for many winters, I finally got busted when they realized I didn’t have a ski pass. It turns out that when you buy a lift ticket you are agreeing to a liability release which they absolutely had to have. I was banned from the mountain.

Today Squaw Valley is owned by the Colorado-based Altera Mountain Company, which along with Vail Resorts owns most of the ski resorts in North America. The concentration has been relentless. Last year Squaw Valley’s name was changed to the Palisades Resort for the sake of political correctness. Last weekend, a gondola connected it with Alpine Meadows next door, creating the largest ski area in the US.

Today there are no Washoe Indians left on the lake. The nearest reservation is 25 miles away in the desert in Gardnerville, NV. They sold or traded away their land for pennies on the current value.

Living at Tahoe has been great, and I get up here whenever I can. I am now one of the few surviving original mountain men and volunteer for North Tahoe Search & Rescue.

On Donner Day, every October 1, I volunteer as a docent to guide visitors up the original trail over Donner Pass. Some 175 years later the oldest trees still bear the scars of being scrapped by passing covered wagon wheels, my own ancestors among them. There is also a wealth of ancient petroglyphs, as the pass was a major meeting place between Indian tribes in ancient times.

The good news is that residents aged 70 or more get free season ski passes at Diamond Peak, where I sponsored the ski team for several years. My will specifies that my ashes be placed in the Middle of Lake Tahoe. At least I’ll be recycled. I’ll be joining my younger brother who was an early Covid-19 victim and whose ashes we placed there in 2020.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Ponderosa Ranch

The Poulson Ranch

At the Reno Airport

Donner Pass Petroglyphs

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/JOHN-THOMAS-lake-e1673280781709.png414500april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-03 09:02:212024-09-03 11:49:46The Market Outlook for the Week Ahead, or The Hidden AI in your Life

Below please find subscribers’ Q&A for the November 1 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Boca Raton.

Q:Earlier you said that the bull market should start from here—are you sticking to that argument?

A: Yes, there are all kinds of momentum and cash flow indicators that are flashing “buy right now.” The market timing index got down to 24—couldn’t break below 20. Hedge fund shorts: all-time highs. Quant shorts: all the time highs, creating a huge amount of buying power for the market. And, of course, the seasonals have turned positive. So yes, all of that is positive and if bonds can hold in here, then it’s off to the races.

Q: Do you have a year-end target for Berkshire Hathaway (BRK/B)?

A: Up. They have a lot of exposure to the falling interest rate trade such as its very heavy weighting in banks; and if interest rates go down, Berkshire goes up—it’s really very simple. You can’t come up with specific targets for individual stocks for year-end because of the news, and things can happen anytime. I love Berkshire; it's a very strong buy here.

Q: Tesla (TSLA) is not doing well; what's the update here?

A: It always moves more than you think, both on the upside and the downside. Last year, we thought it would drop 50%, it dropped 80%. Suffice it to say that, with the price war continuing and Tesla determined to wipe out the 200 other new entrants to the EV space, they’ll keep price cutting until they basically own that market. While that’s great for market share, it’s not great for short-term profits. Yes, Tesla could be going down more, but from here on, if you’re a long-term investor in Tesla, as you should be, you should be looking to add positions, not sell what you have and average down. Also, we’re getting close to Tesla LEAPS territory. Those have been huge winners over the years for us and I’ll be watching those closely.

Q: Any trade on the Japanese yen?

A: We broke 150 on the yen—that was like the make-or-break level. I’m looking at a final capitulation selloff on the yen, and then a decade-long BUY. The Bank of Japan is finally ending its “easy money” zero-interest-rate policy, which it’s had for 30 years, and that will give us a stronger yen when it happens, but not until then. So watch the yen carefully, it could double from here over the long term, especially if it’s the same time the US starts cutting its interest rates.

Q: What do you think about Eli Lilly (LLY)?

A: We love Eli Lilly; they’re making an absolute fortune on their weight loss drug, and they have other drugs in the pipeline being created by AI. This is really the golden age for biotech because you have AI finding cures for diseases, and then AI designing molecules to cure the diseases. It’s shortened the pipeline for new drugs from 5-10 years to 5-10 weeks. If you’re old and sick like me, this is all a godsend.

Q: Do you like Snowflake (SNOW)?

A: Absolutely, yes—killer company. Warren Buffet loves it too and has a big position; I’d be looking to buy SNOW on any dip.

Q: Would you do LEAPS on Netflix (NFLX)?

A: I would, but I would go out two years, and I would go at the money, not out of the money, Even then you’ll get a 100-200% return. You’ll get a lot even on just a 6-month call spread. These tech stocks with high volatility have enormous payoff 3-6 months out.

Q: Projection for iShares 20 Plus Year Treasury Bond ETF (TLT) in the next 6 months?

A: It’s up. We could hit $110, that would be my high, or up $25 points or so from here.

Q: Would you buy biotech here through the ProShares Ultra Nasdaq Biotechnology (BIB)?

A: Probably, yes. The long-term story is overwhelming, but it’s not a sector you want to own when the sentiment is terrible like it is now. I guess “buy the bad news” is the answer there.

Q: What did you learn from your dinner with General Mattis?

A: Quite a lot, but much of it is classified. When you get to my age, you can’t remember which parts are classified and which aren't. However, his grasp of the global scene is just incredible. There are very few people in the world I can go one on one with in geopolitics. Of course, I could fill in stuff he didn’t know, and he could fill in stuff for me, like: what is the current condition of our space weaponry? If I told you, you would be amazed, but then I would get arrested the next day, so I’ll say nothing. He really was one of the most aggressive generals in American history, was tremendously underrated by every administration, was fired by both Obama and Trump, and recently is doing the speaker circuit which is a lot of fun because there’s no question he doesn’t know the answer to! We actually agreed to do some joint speaking events sometime in the future.

Q: I have some two-year LEAPS now but I’m worried about adding too much. Could we get a final selloff in 2024?

A: The only way we could get another leg down in the market is number one if the Fed raises interest rates (right now, we’re positioned for a flat line and then a cut) or number two, another pandemic. You could also get some election-related chaos next year, but that usually doesn’t affect the market. But for those who are prone to being nervous, there are certainly a lot of reasons to be nervous next year.

Q: What iShares 20 Plus Year Treasury Bond ETF (TLT) level would we see with a 5.2% yield?

A: How about $79? That’s exactly why I picked that strike price. The $76-$79 vertical bill call spread in the (TLT) is a bet that we don’t go above 5.20% yield, and we only have 10 days to do it, so things are looking better and then we’ll see what’s available in the market once our current positions all expire at max profit.

Q: The first new nuclear power plant of 30 years went online in Georgia. Do you see more being built in the future?

A: It’s actually been 40 years since they’ve built a new plant, and it wasn’t a new plant, it was just an addition to an existing plant with another reactor added with an old design. I think there will be a lot more nuclear power plants built in the future, but they will be the new modular design, which is much safer, and doesn’t use uranium, by the way, but other radioactive elements. If you want to know more about this, look up NuScale (SMR). They have a bunch of videos on how their new designs work. That could be an interesting company going forward. The nuclear renaissance continues, and of course, China’s continuing to build 100 of the old-fashioned type nuclear power reactors, and that is driving global uranium demand.

Q: Would you hold Cameco Corp (CCJ) or sell?

A: I would keep it, I think it’s going up.

Q: How to trade the collapse of the dollar?

A: (FXA), (FXB), (FXE), and (EEM). Those are the quick and easy ways to do it. Also, you buy precious metals—gold (GLD) and silver (SLV) do really well on a weak dollar.

Q: Conclusion on the Ukraine war?

A: It will go on for years—it’s a war of attrition. About half of the entire Russian army has been destroyed as they’re working with inferior weapons. However, it’s going to be a matter of gaining yards or miles at best, over a long period of time. So, they will keep fighting as long as we keep supplying them with weapons, and that is overwhelmingly in our national interest. Plus, we’re getting a twofer; if we stop Russia from taking over Ukraine, we also stop China from invading Taiwan because they don’t want to be in for the same medicine.

Q: If more oil is released from the strategic petroleum reserve, what is our effect on security?

A: Zero because the US is a net energy producer. If our supplies were at risk, all we’d have to do is cut off our exports to China and tell them to find their oil elsewhere—and they’re obviously already trying to do that with the invasion of the South China Sea and all the little rocks out there. So, I am not worried. And also remember, every year as the US moves to more EVs and more alternatives, it is less and less reliant on oil. I would advise the administration to get rid of all of it next time we go above $100 a barrel. If you’re going to sell your oil, you might as well get a good price for it. If you look at the US economy over the last 30 years, the reliance of GDP on oil has been steadily falling.

Q: Are US exports of Cheniere Energy (LNG) helping to drive up prices here?

A: I would say yes, it’s got to have an impact on prices. We’re basically supplying Germany with all of its natural gas right now. We did that starting from scratch at the outset of the Ukraine war, and it’s been wildly successful. That avoided a Great Depression in Europe. Europe, by the way, is the largest customer for our exports. That was one of the arguments for us going into the United States Natural Gas (UNG) LEAPS in the first place.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We’ve just seen our last interest rate rise in the economic cycle. Yes, I know that our central bank took no action at their last meeting in September. The market has just done its work for it.

And the markets are no shrinking violet when it comes to taking bold action. The 50 basis points it took bond yields up over the last two weeks is far more than even the most aggressive, economy-wrecking, stock market-destroying Fed was even considering.

And that doesn’t even include the rate hikes no one can see, the deflationary effects of quantitative tightening, or QT. That is the $1 trillion a year the Fed is sucking out of the economy with its massive bond sales.

It really is a miracle that the US economy is growing as fast as it is. After a warm 2.4% growth rate in Q2, Q3 looks to come in at a blistering 4%-5%. That is definitely NOT what recessions are made of.

Where is all this growth coming from?

Some of the credit goes to the pandemic spending, the free handouts we call got to avoid starvation while Covid ravaged the country. You probably don’t know this, but nothing happens fast in Washington. Government spending is an extremely slow and tedious affair.

By the time that contracts are announced, bids awarded, permits obtained, men hired, and the money spent, years have passed. That means money approved by Congress way back in 2020 is just hitting the economy now.

But that is not the only reason. There is also the long-term structural push that is a constant tailwind for investors:

Hyper-accelerating technology.

Yes, I know, there goes John Thomas spouting off about technology again. But it is a really big deal.

I have noticed that the farther away you get from Silicon Valley, the more clueless money managers are about technology. You can pick up more stock tips waiting in line at a Starbucks in Palo Alto than you can read a year’s worth of research on Wall Street.

What this means is that most large money managers, who are based on the east coast are constantly chasing the train that is leaving the station when it comes to tech.

On the west coast, managers not only know about the new tech, but the tech that comes after that and another tech that comes after that, if they are not already insiders in the current hot deal. This is how artificial intelligence stole a march on almost everyone, until a year ago, unless you were on the west coast already working in the industry. Mad Hedge has been using AI for 11 years.

You may be asking, “What does all of this mean for my pocketbook?” a perfectly valid question. It means that there isn’t going to be a recession, just a recession scare. That technology will bail us out again, even though our old BFF, the Fed, has abandoned us completely.

Which brings me to the current level of interest rates. I have also noticed that the farther away you get from New York and Washington, the less people know about bonds. On the west coast mention the word “bond” and they stare at you cluelessly. Indeed, I spent much of this year explaining the magic of the discount 90-day T-bill, which no one had ever heard of before (What! They pay interest daily?).

In fact, most big technology companies have positive cash balances. Look no further than Apple’s $140 billion cash hoard, which is invested in, you guessed it, 90-day T-bills when it isn’t buying its own stock, and is earning a staggering $7.7 billion a year in interest.

The great commonality in the recent stock market correction is easy to see. Any company that borrows a lot of money saw its stock get slaughtered. Technology stocks held up surprisingly well. That sets up your 2024 portfolio.

Put half your money in the Magnificent Seven stocks of Apple (AAPL), Amazon (AMZN), Meta (META), Microsoft (MSFT), Tesla (TSLA), (NVIDIA), and Salesforce (CRM).

Put your other half into heavy borrowers that benefit from FALLING interest rates, including bonds (TLT), junk bonds (JNK), (HYG), Utilities (XLU), precious metals (GOLD), (WPM), copper (FCX), foreign currencies (FXA), (FXE), (FXY), emerging markets (EEM).

As for me, I never do anything by halves. I’m putting all my money into Tesla. If I want to diversify, I’ll buy NVIDIA. Diversification is only for people who don’t know what is going to happen.

I just thought you’d like to know.

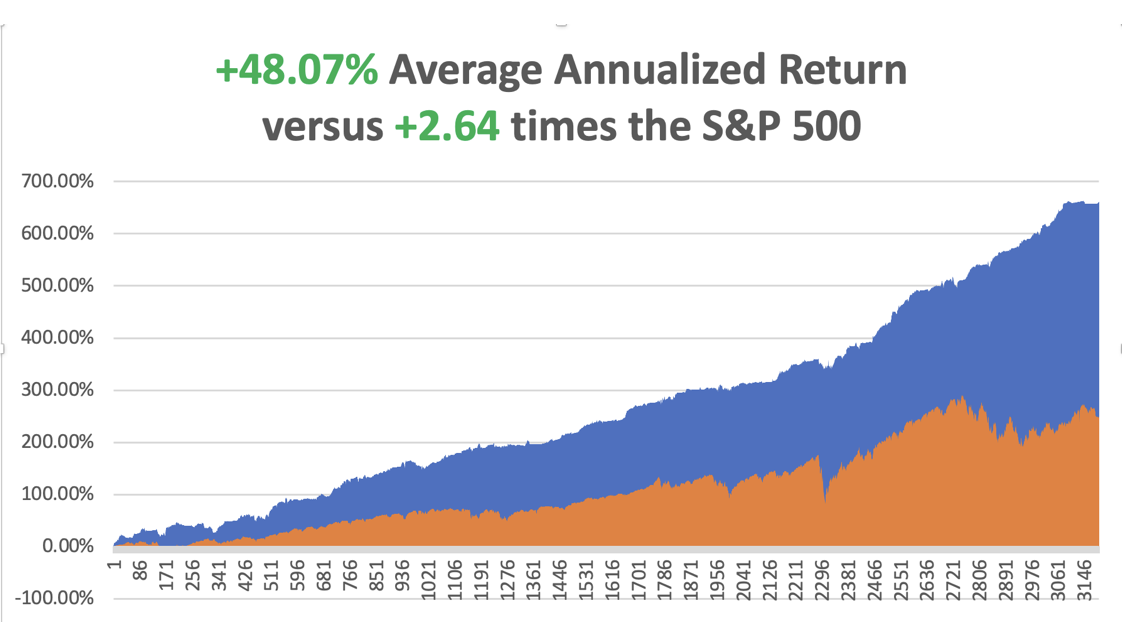

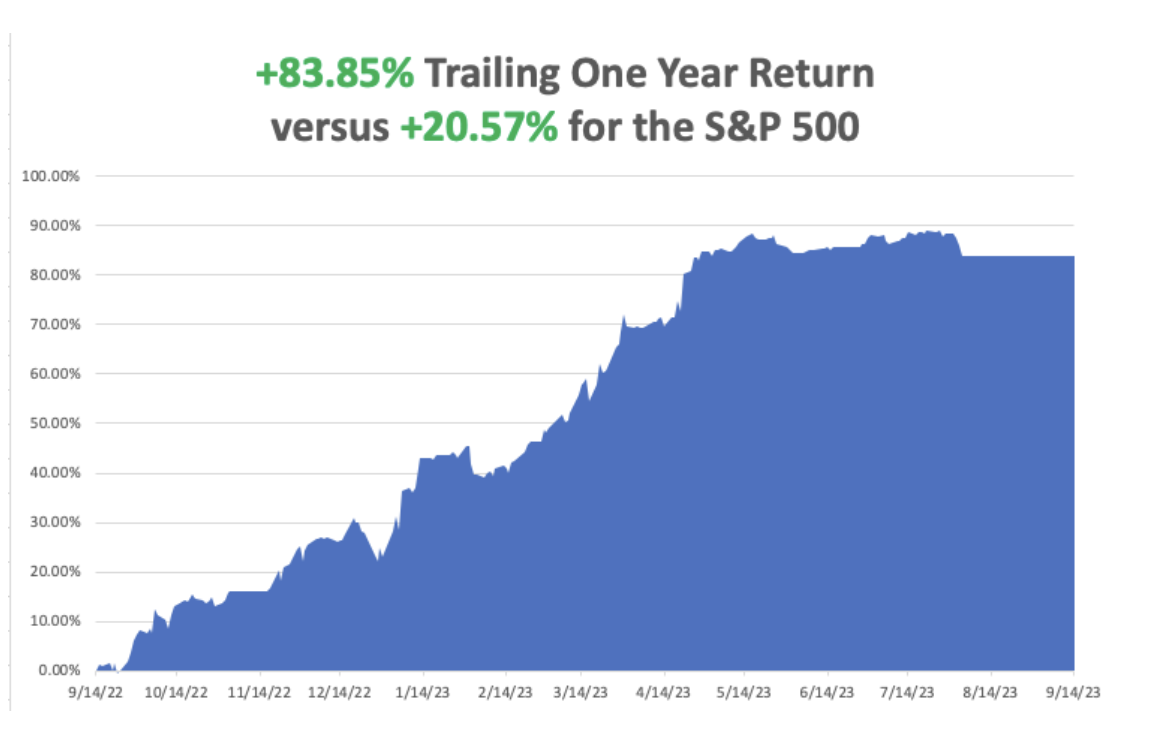

So far in October, we are up +2.96%. My 2023 year-to-date performance is still at an eye-popping +63.76%.The S&P 500 (SPY) is up +12.89%so far in 2023. My trailing one-year return reached +76.46% versus +22.57% for the S&P 500.

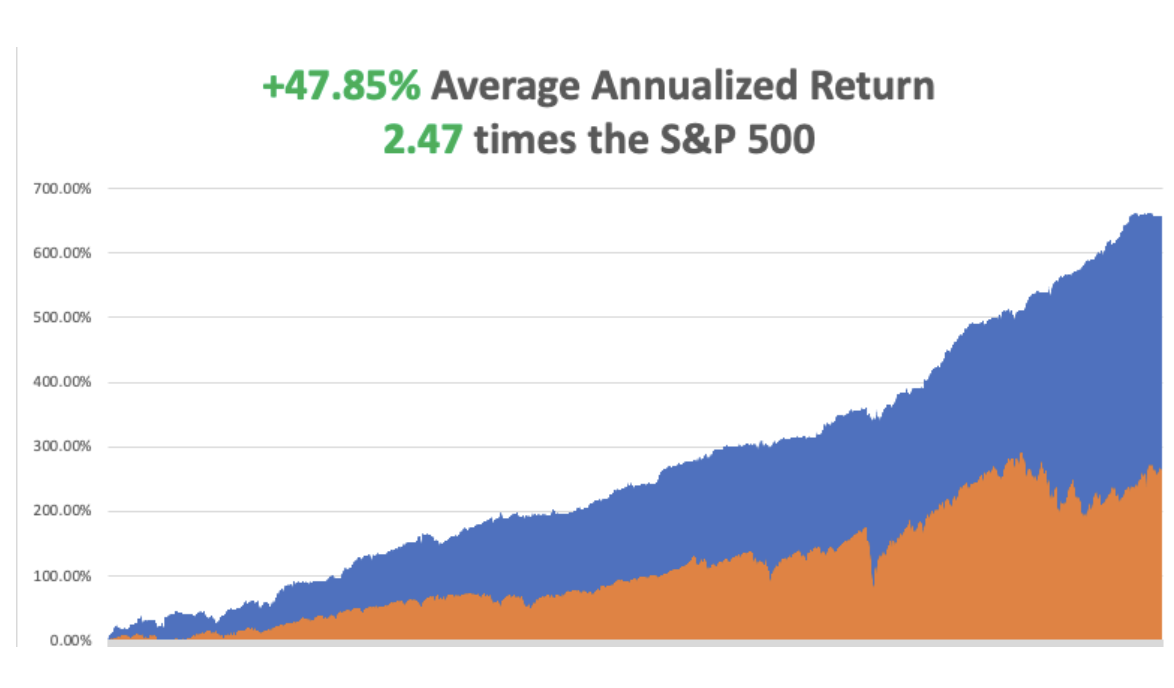

That brings my 15-year total return to +660.95%. My average annualized return has fallen back to +48.07%,another new high, some 2.64 times the S&P 500over the same period.

Some 44 of my 49 trades this year have been profitable.

Chaos Reigns Supreme in Washington, with the firing of the first House speaker in history. Will the next budget agreement take place on November 17, or not until we get a new Congress in January 2025? Markets are discounting the worst-case scenario, with government debt in free fall. Definitely NOT good for stocks, which are reaching for a full 10% correction, half of 2023’s gains.

September Nonfarm Payroll Report Rockets, to 336,000, and August was bumped up another 50,000. The economy remains on fire. The headline Unemployment Rate remains steady at an unbelievable 3.8%. And that’s with the UAW strike sucking workers out of the system. This is supposed to by impossible with 5.5% interest rates. Throw out you economics books for this one!

JOLTS Comes in Hot at 9.61 million job openings in August, 700,000 more than the July report. The record labor shortage continues. Will the Friday Nonfarm Payroll Report deliver the same?

ADP Rises 89,000 in September, down sharply from previous months, showing that private job growth is growing slower than expected. August was revised down. It’s part of the trifecta of jobs data for the new month. The mild recession scenario is back on the table, at least stocks think so.

Weekly Jobless Claims Rise to 207,000, still unspeakably strong for this point in the economic cycle. Continuing claims were unchanged at 1.664%.

Traders Pile on to Strong Dollar, headed for new highs, propelled by rising interest rates. There is a heck of a short setting up for next year.

Yen Soars on suspected Bank of Japan intervention in the foreign exchange markets to defend the 150 line against the US dollar. The currency is down 35% in three years and could be the BUY of the century.

Kaiser Goes on Strike with 75,000 health care workers walking out on the west coast. The issue is money. The company has a long history of labor problems. This seems to be the year of the strike.

Oil (USO)Gets Slammed on Recession Fears, down 5% on the day to $85, in a clear demand destruction move and worsening macroeconomic picture. Europe and China are already in recession. It’s the biggest one-day drop in a year. Is the top in?

Tesla Delivers 435,059 Vehicles in September, down 5% from forecast, but the stock rose anyway. The Cybertruck launch is imminent, where the company has 2 million new orders. Keep buying (TSLA) on Dips. Technology is accelerating.

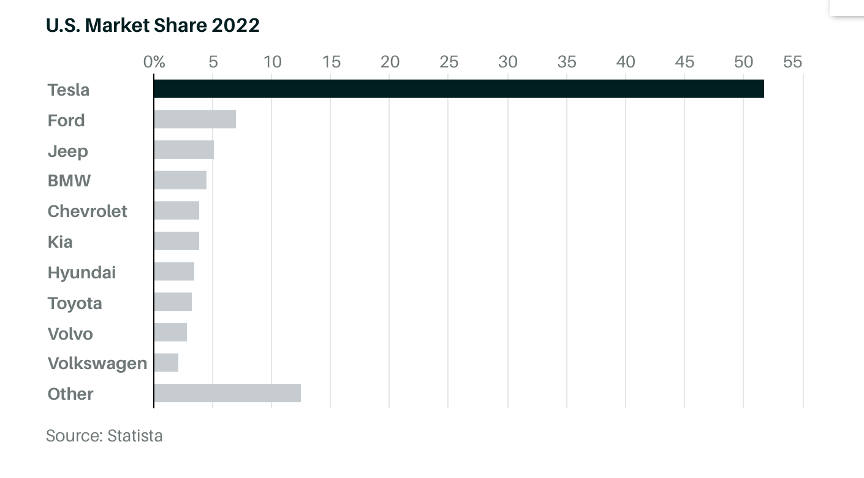

EVs have Captured an Amazing 8% of the New Car Market. They have been helped by a never-ending price war and generous government subsidies. EV sales are now up a miraculous 48% YOY and are projected to account for a stunning 23% of all California sales in Q3. Tesla is the overwhelming leader with a 52% share in a rapidly growing market, distantly followed by Ford (F) at 7% and Jeep at 5%. However, a slowdown may be at hand, with EV inventories running at 97 days, double that of conventional ICE cars. This could create a rare entry point for what will be the leading industry of this decade, if not the century. Buy more Tesla (TSLA) on bigger dips, if we get them.

Apple Upgrades New iPhone 15 to deal with overheating from third-party gaming. It will shut down some of its background activity, including some of the new AI functions, which were stressing the central processor. Third-party apps were adding to the problem, such as Uber and games from (META). This is really cutting-edge technology.

Moderna (MRNA) Bags a Nobel Prize in Chemistry. Katalin Kariko and Drew Weissman’s work helped pioneer the technology that enabled Moderna and the Pfizer Inc.-BioNTech SE partnership to swiftly develop shots. I got four and they saved my life when I caught Covid. I survived but lost 20 pounds in two weeks. It was worth it.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 9, there is no data of note released.

On Tuesday, October 10 at 8:30 AM EST, the Consumer Inflation Expectations is released.

On Wednesday, October 11 at 2:30 PM, the Producer Price Index is published.

On Thursday, October 12 at 8:30 AM, the Weekly Jobless Claims are announced. The Consumer Price Index is also released.

On Friday, October 13 at 1:00 PM the September University of Michigan Consumer Expectations is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, one of the many benefits of being married to a British Airways senior stewardess is that you get to visit some pretty obscure parts of the world. In the 1970s, that meant going first class for free with an open bar, and occasionally time in the cockpit jump seat.

To extend our 1977 honeymoon, Kyoko agreed to an extra round trip for BA from Hong Kong to Colombo in Sri Lanka. That left me on my own for a week in the former British crown colony of Ceylon.

I rented an antiquated left-hand drive stick shift Vauxhall and drove around the island nation counterclockwise. I only drove during the day in army convoys to avoid terrorist attacks from the Tamil Tigers. The scenery included endless verdant tea fields, pristine beaches, and wild elephants and monkeys.

My eventual destination was the 1,500-year-old Sigiriya Rock Fort in the middle of the island which stood 600 feet above the surrounding jungle. I was nearly at the top when I thought I found a shortcut. I jumped over a wall and suddenly found myself up to my armpits in fresh bat shit.

That cut my visit short, and I headed for a nearby river to wash off. But the smell stayed with me for weeks.

Before Kyoko took off for Hong Kong in her Vickers Viscount, she asked me if she should bring anything back. I heard that McDonald’s had just opened a stand there, so I asked her to bring back two Big Macs.

She dutifully showed up in the hotel restaurant the following week with the telltale paper bag in hand. I gave them to the waiter and asked him to heat them up for lunch. He returned shortly with the burgers on plates surrounded by some elaborate garnish and colorful vegetables. It was a real work of art.

Suddenly, every hand in the restaurant shot up. They all wanted to order the same thing, even though the nearest stand was 2,494 miles away.

We continued our round-the-world honeymoon to a beach vacation in the Seychelles where we just missed a coup d’état, a safari in Kenya, apartheid South Africa, London, San Francisco, and finally back to Tokyo. It was the honeymoon of a lifetime.

Kyoko passed away in 2002 from breast cancer at the age of 50, well before her time.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Sigiriya Rock Fort

Kyoko

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-10-09 09:02:402023-10-09 19:19:06The Market Outlook for the Week Ahead, or The Fed is Done!

(MARKET OUTLOOK FOR THE WEEK AHEAD, or BACK IN BUSINESS)

(TLT), (GLD), (SLV), (XLU), (IWM), (EEM), (FXA), (FXE), (FXB), (USO), (UUP), (AMZN), (TSLA), (F)

It’s a good thing I don’t rely on my Social Security Check to cover my extravagant cost of living, which is the maximum $4,555 a month. For it came within hours of coming to a halt when an agreement was passed by Congress to renew funding for another 45 days. It was almost an entirely Democratic bill, passing 335 to 91 in the House and the Senate by 88 to 9.

Unfortunately, that does put me in the uncomfortable position of delivering humanitarian aid to Ukraine right when $6.2 billion in US assistance is cut off. That was the price the Dems had to pay to get the Republicans on board needed to pass the bill. Better a half a loaf than no loaf at all. Still, I am going to have some explaining to do next week in Kiev, Mykolaiv, and Kherson. It’s a big win for Vladimir Putin.

Funding now ends on November 17, when the next crisis begins. The big question is when the markets will deliver a sigh of relief rally on Congress hitting the “snooze” button, or whether it will focus on the next disaster in November.

We’ll have to wait and see.

In the meantime, all eyes are on the market’s leading falling interest rate plays, which continue to go from bad to worse. Those include bonds (TLT), precious metals (GLD), (SLV), utilities (XLU), small-cap stocks (IWM), emerging markets (EEM), and foreign currencies (FXA), (FXE), (FXB).

Consider this your 2024 shopping list.

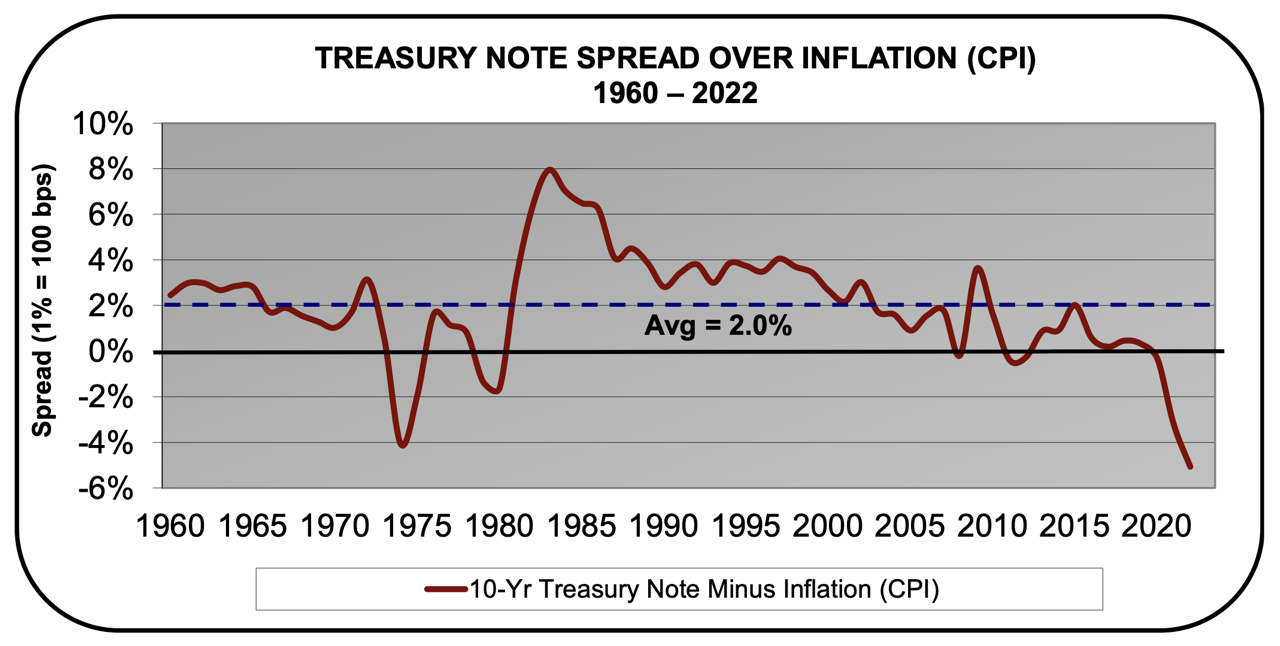

Ten-year US Treasury bond yields reached a stratospheric 4.70% last week a 17-year high and up a monster 0.90% since the end of June. Summer proved a fantastic time to take a vacation from the bond market.

They could easily reach 5% before the crying is all over. Perhaps this is why my old friend, hedge fund legend David Tepper, said his best investment right now is a subprime six-month certificate of deposit yielding 7.0%.

What we might be witnessing here is a return to the “old normal” when bonds spent most of their time ranging between 2%-6%. The 60-year historic average bond yield is 2% over the inflation rate (see chart below). That alone takes us to a 5.0% bond yield.

Interest rates have been kept artificially low for 15 years because no one wanted a recession in 2008 and no one wanted a recession during the pandemic in 2000. It all melded into one big decade-and-a-half period of easy money. Pain avoidance wasn’t just the universal American monetary policy, it was the global policy.

Now it’s time to pay the piper and unwind the thousands of business models that depended on free money. There will be widespread pain, as we are now witnessing in commercial real estate and private equity. Perhaps it is best to take the 5.5% bribe 90-day Treasury bond yield is offering you and stay out of the market.

While Detroit remains mired by the UAW strike, EVs have catapulted to an amazing 8% of the new car market. They have been helped by a never-ending price war and generous government subsidies. EV sales are now up a miraculous 48% YOY and are projected to account for a stunning 23% of all California sales in Q3.

Tesla is the overwhelming leader with a 52% share in a rapidly growing market, distantly followed by Ford (F) at 7% and Jeep at 5%.

However, a slowdown may be at hand, with EV inventories running at 97 days, double that of conventional ICE cars. This could create a rare entry point for what will be the leading industry of this decade, if not the century. Buy more Tesla (TSLA) on bigger dips, if we get them.

Hedge Funds are Cutting Risk at Fastest Pace Since 2020, when the pandemic began. From retail investors to rules-based systematic traders, appetite for equities is subsiding after a 20% rally this year that’s fueled by euphoria over artificial intelligence. Fast money investors increased their bearish wagers to drive down their net leverage — a gauge of risk appetite that measures long versus short positions — by 4.2 percentage points to 50.1%, according to Goldman Sachs Group Inc.’s prime brokerage. That’s the biggest week-on-week decline in portfolio leverage since the depths of the pandemic bear market.

The Treasury Bond Freefall Continues, as long-term yields probe new highs. New issue of $134 billion this week didn’t help. Nothing can move on the risk until rates top out, even if we have to wait until 2024.

Oil (USO) Hits $95, a one-year high, as the Saudi/Russian short squeeze continues. $100 a barrel is a chipshot and much higher if we get a cold winter. Inventories at the Cushing hub are at a minimum.

The US Dollar (UUP) Hits New Highs, as “high for longer” interest rates keep powering the greenback. The buck is also catching a flight to safety bid from a potential government shutdown. It should be topping soon.

Moody’s Warns of Further US Government Downgrades, in the run up to the Saturday government shutdown. The shutdown lasts, the more negative its impact would be on the broader economy. Unemployment could soar. It would also render all US government data releases useless for the next three months.

ChatGPT Can Now Browse the Internet, according to its creator, OpenAI. Until now, the chatbot could only access data posted before September 2021. The move will exponentially improve the quality and effectiveness of AI apps, including my own Mad Hedge AI

Amazon (AMZN) Pouring $4 Billion into AI, with an investment in Anthropic, a ChatGPT competitor. (AMZN) is racing to catch up with (MSFT) and (GOOGL). Its chatbot is caused Claude 2. Amazon’s card to play here is its massive web services business AWS. The AI wars are heating up.

Hollywood Screenwriters Guild Strike Ends, after 150 days, which is thought to have cost the US economy $5 billion in output. The hit was mostly taken by Los Angeles, where 200,000 are employed. The Actor’s union is still on strike. Talk shows should be offering new content in a few days.

S&P Case Shiller Rises to New All-Time High, for the sixth consecutive month as inventory shortages drove up competition. In July, the index in increased 0.6% month over month and 1% over the last 12 months, on a seasonally adjusted basis. July’s movement reached a new high for the nationwide home index, surpassing the record set in June 2022. Chicago (+4.4%), Cleveland (+4.0%), and New York (+3.8%) delivered the biggest gains. The median home price for existing homes rose to 1.9 to $406,700 according to the National Association of Realtors (NAR). The robust housing market suggests that while some buyers pulled back due to high borrowing costs, demand continues to outweigh supply.

This is the Unit I Will be Joining at the Front in Ukraine, as made clear by their YouTube recruiting video. They asked me to assist with mine removal on territory formerly occupied by Russia. I really don’t know what I’m getting into. Improvision is key. It’s better than playing golf in retirement. Polish up your Ukrainian first.

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%.The S&P 500 (SPY) is up +17.10%so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%,another new high, some 2.50 times the S&P 500over the same period.

Some 41 of my 46 trades this year have been profitable.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, October 2, at 8:30 PM EST, the ISM Manufacturing PMI is out.

On Tuesday, October 3 at 8:30 AM,the JOLTS Job Openings Report is released.

On Wednesday, October 4 at 2:30 PM, the ISM Services Report is published.

On Thursday, October 5 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, October 6 at 2:30 PM the September Nonfarm Payroll Report is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I will try to knock out a few memories early this morning while waiting for the Matterhorn to warm up so I can launch on another ten-mile hike. So I will reach back into the distant year of 1968 in Sweden.

My trip to Europe was supposed to limit me to staying with a family friend, Pat, in Brighton, England for the summer. His family lived in impoverished council housing.

I remember that you had to put a ten pence coin into the hot water heater for a shower, which inevitably ran out when you were fully soaped up. The trick was to insert another ten pence without getting soap in your eyes.

After a week there, we decided the gravel beach and the games arcade on Brighton Pier were pretty boring, so we decided to hitchhike to Paris.

Once there, Pat met a beautiful English girl named Sandy, and they both took off to some obscure Greek island, the ultimate destination if you lived in a cold, foggy country.

That left me stranded in Paris with little money.

So, I hitchhiked to Sweden to meet up with a girl I had run into while she was studying English in Brighton. It was a long trip north of Stockholm, but I eventually made it.

When I finally arrived, I was met at the front door by her boyfriend, a 6’6” Swedish weightlifter. That night found me bedding down in a birch forest in my sleeping bag to ward off the mosquitoes that hovered in clouds.

I started hitchhiking to Berlin, Germany the next day, which offered paying jobs. I was picked up by Ronny Carlson in a beat-up white Volkswagen bug to make the all-night drive to Goteborg where I could catch the ferry to Denmark.

1968 was the year that Sweden switched from driving English style on the left side of the road to the right. There were signs every few miles with a big letter “H”, which stood for “hurger”, or right. The problem was that after 11:00 PM, everyone in the country was drunk and forgot what side of the road to drive on.

Two guys on a motorcycle driving at least 80 mph pulled out to pass a semi-truck on a curve and slammed head-on to us, then were thrown under the wheels of the semi. The motorcycle driver was killed instantly, and his passenger had both legs cut off at the knees.

As for me, our front left wheel was sheared off and we shot off the mountain road, rolled a few times, and was stopped by this enormous pine tree.

The motorcycle riders got the two spots in the only ambulance. A police car took me to a hospital in Goteborg and whenever we hit a bump in the road bolts of pain shot across my chest and neck.

I woke up in the hospital the next day, with a compound fracture of my neck, a dislocated collar bone, and paralyzed from the waist down. The hospital called my mom after booking the call 16 hours in advance and told me I might never walk again. She later told me it was the worst day of her life.

Tall blonde Swedish nurses gave me sponge baths and delighted in teaching me to say Swedish swear words and then laughed uproariously when I made the attempt.

Sweden had a National Health care system then called Scandia, so it was all free.

Decades later a Marine Corps post-traumatic stress psychiatrist told me that this is where I obtained my obsession with tall, blond women with foreign accents.

I thought everyone had that problem.

I ended up spending a month there. The TV was only in Swedish, and after an extensive search, they turned up only one book in English, Madame Bovary. I read it four times but still don’t get the ending. And she killed herself because….?

The only problem was sleeping because I had to share my room with the guy who lost his legs in the same accident. He screamed all night because they wouldn’t give him any morphine.

When I was released, Ronny picked me up and I ended up spending another week at his home, sailing off the Swedish west coast. Then I took off for Berlin to get a job since I was broke. Few Germans wanted to live in West Berlin because of the ever-present risk of a Russian invasion so there we always good-paying jobs.

I ended up recovering completely. But to this day whenever I buy a new Brioni suit in Milan they have to measure me twice because the numbers come out so odd. My bones never returned to their pre-accident position and my right arm is an inch longer than my left. The compound fracture still shows up on X-rays.

And I still have this obsession with tall, blond women with foreign accents.

Go figure.

Brighton 1968

Ronny Carlson in Sweden

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-10-02 09:02:222023-10-02 14:52:17The Market Outlook for the Week Ahead, or Back in Business

All traders and portfolio managers with experience approaching a half-century, like myself and a handful of close friends, agree on one thing.

Someday, you will be wrong.

I don’t mean just a little bit wrong, I mean disastrously wrong. A real humdinger, even a life-threatening experience. Even wrong up the wazoo.

In fact, most old salts, even the best performing ones, suffer at least a couple of 50% losses of their total assets, and at least one 75% hit, at least once in their lives.

We’ve all been there.

The 1973 oil crisis. The 1987 stock market crash, when the Dow Average gave up a withering 22% in a single day (I tried to place an order to buy stock at the close and the clerk burst into tears and dissolved into a puddle on the floor).

The Dotcom crash. And of course, the granddaddy of them all, the Great Crash of 2008, which you all remember with the greatest discomfort.

Even my mentor, Warren Buffet, has admitted to taking three 50% hits in his lifetime and lived to tell about it.

The trick is to keep these misfortunes from wiping you out so completely that you can never make a comeback.

Better yet, don’t get into trouble in the first place. And I’ll tell you exactly how to do that right now.

One of the great pleasures of running the Mad Hedge Fund Trader is that I get to speak to thousands of interesting people every year. Believe me, there are all kinds.

I have found kids straight out of school who take to trading like a fish to water. Their instincts are incredible. They figure out the harsh realities of the market decades before I ever did.

When they ask me questions, I think, “Damn! Why didn’t I think of that?”

I have seen several of these gifted, natural born traders use the Mad Hedge Fund Trader turn pennies into millions over unbelievably short times.

You see, they have the trader gene.

Sadly, I also run into the opposite extreme. With some people you could have George Soros sitting on their left, Paul Tudor Jones on their right, both guiding their hands on the mouse to execute trades, and they are still going to still lose money.

These are not stupid people.

I have met many with Harvard MBAs, advanced degrees from MIT, and even Phi Beta Kappa’s, and it doesn’t do them a whit of good on the trading front. They just don’t have trading in them.

In other words, they lack the trading gene.

When I stumble across these people, I tell them to quit trading, end the self-abuse, and preserve whatever wealth they have left. I then order them to buy what I call my “Buy and Forget Portfolio.”

This is a collection of only six investments, which I have assembled over the decades that will be profitable in almost all circumstances. In good years it will grow generously. In bad years it will be down marginally. Over the long term, it will do extremely well.

Here it is:

The Mad Hedge Buy and Forget Portfolio

20% domestic US stocks (SPY)

20% international stocks (IXUS)

10% emerging stock markets (EEM)

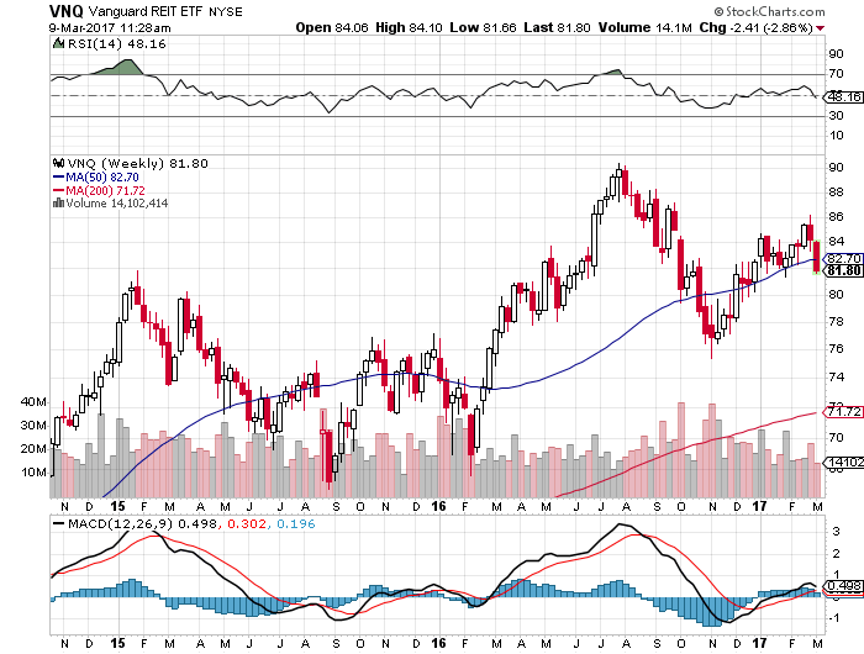

20% Real Estate Investment Trusts (VNQ)

15% long term US Treasury Bonds (TLT)

15% Treasury Inflation Protected Securities (TIP)

Notice that half the money is in equities and the remainder in fixed income securities.

If you initiated this portfolio in 1997, the year that TIPS first became available to the public, you would have earned an average annualized compounded return of 7.86% through the end of 2014, assuming reinvestment of dividends and interest.

During the bear market of 2000-2002, when the S&P 500 dropped 50%, this portfolio never suffered a loss of more than -4.7%. During the Great Crash of 2008, it fell -31%, versus -37% for the (SPY), and then very quickly bounced back.

Most long-only investors would have killed for returns like these.

So the bottom line is this. Expect a 4% drawdown every decade, a 31% hickey twice a century, and one of those twice-a-century events is only eight years behind us. That is not a bad proposition.

The heavy stock weighting can be easily explained by the fact that historically, stocks have outperformed bonds by a large margin.

For long periods of time, such as much of the 19th century, the Great Depression, and now, chronic structural deflation meant that bonds paid very little in interest.

Stocks also have the advantage in that during periods of inflation they can pass rising costs on to consumers via price hikes.

Guess what? We are just going into an inflationary period.

For the past 200 years, stocks have therefore delivered a compounded average annualized return of 8.3%.

Just to give you an example of how valuable the stock advantage can be, $1 invested in 1802 would be worth $8.8 million today.

This is why Oracle of Omaha Warren Buffet constantly sings the praises of compounding and dividend reinvestment and is why he rarely sells anything. In fact, his authorized biography is entitled Snowball (a great read, by the way).

The beauty of the Buy and Forget Portfolio is that the six elements counterbalance each other in all market circumstances. When stocks go up, bonds usually go down, and vice versa.

They both go the wrong way only for very short periods, such as in 2008 and always snap back.

And remember inflation, that long-forgotten thing where prices actually go up? It will make a return someday. And there is no better time to buy TIPS than during the deflationary surge that we are enduring now. TIPS prices are cheap.

Such is the beauty of diversification.

The great thing about the Buy and Forget Portfolio is that you can literally buy and forget about it. You won’t lose sleep at night, you could care less about what they say on CNBC, and don’t have to hide those embarrassing brokerage statements from your spouse.

The only thing you have to do is to rebalance it once a year to restore each component to its original weighting. More often than that and you run up big commission and tax bills.

Remember, you are trying to buy your own yacht, not your broker’s.

This will free you up to focus on the more important things in life.

Will Daenerys Targaryen gain her rightful place on the throne of the Seven Kingdoms in The Game of Thrones? Will Don Draper get his well-deserved comeuppance in the final season of Mad Men? Can the widow, Lady Mary, ever find true love again in the next season of Downton Abbey?

Of course, knowing all of this, some bad traders will continue to trade. For some, it is like an addition. They just have to win, whatever the cost. For others, it's like buying lottery tickets. Some just love the adrenaline and the thrill of the chase, even if it costs them money.

Whatever the reason, they continue trading until they run out of money. Then they will try to borrow your money to trade.

Could this be you?

All I can do is wish them the best.

Leave the trading to the masochists, like me.

Leave the Trading to the Masochists

https://www.madhedgefundtrader.com/wp-content/uploads/2017/12/john-snow-e1514508880916.jpg333250Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-21 09:02:342023-06-21 12:36:10The Buy and Forget Portfolio

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.