Mad Hedge Technology Letter

April 16, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

Mad Hedge Technology Letter

April 16, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

There is only so much juice you can squeeze from a lemon before nothing is left.

Silicon Valley has been focused mainly on squeezing the juice out of the Internet for the past 30 years with intense focus on the American consumer.

In an era of minimal regulation, companies grew at breakneck speeds right into families' living quarters and was a win-win proposition for both the user and the Internet.

The cream of the crop ideas were found briskly, and the low hanging fruit was pocketed by the venture capitalists (VCs).

That was then, and this is now.

No longer will VCs simply invest in various start-ups and 10 years later a Facebook (FB) or Alphabet (GOOGL) appears out of thin air.

That story is over. Facebook was the last one in the door.

VCs will become more selective because brilliant ideas must withstand the passage of time. Companies want to continue to be relevant in 20 or 30 years and not just disintegrate into obsolescence as did the Eastman Kodak Company, the doomed maker of silver-based film.

The San Francisco Bay Area is the mecca of technology, but recent indicators have presaged the upcoming trends that will reshape the industry.

In general, a healthy and booming local real estate sector is a net positive creating paper wealth for its people and attracting money slated for expansion.

However, it's crystal clear the net positive has flipped, and housing is now a buzzword for the maladies young people face to sustain themselves in the ultra-expensive coastal Northern California megacities. The loss of tax deductions in the recent tax bill make conditions even worse.

Monthly rental costs are deterring tech's future minions. Without the droves of talent flooding the area, it becomes harder for the industry to incrementally expand.

It also boosts the salaries of existing development/operations staffers who feed into the local housing market spiking prices because of the fear of missing out (FOMO).

After surveying HR tech heads, it's clear there aren't enough artificial intelligence (AI) programmers and coders to fill internal projects.

Compounding the housing crisis is the change of immigration policy that has frightened off many future Silicon Valley workers.

There is no surprise that millions of aspiring foreign students wish to take advantage of America's treasure of a higher education because there is nothing comparable at home.

The best and brightest foreign minds are trained in America, and a mass exodus would create an even fiercer deficit for global dev-ops talent.

These US-trained foreign tech workers are the main drivers of foreign tech start-ups. Dangling financial incentives for a chance to start an embryonic project at home is hard to pass up.

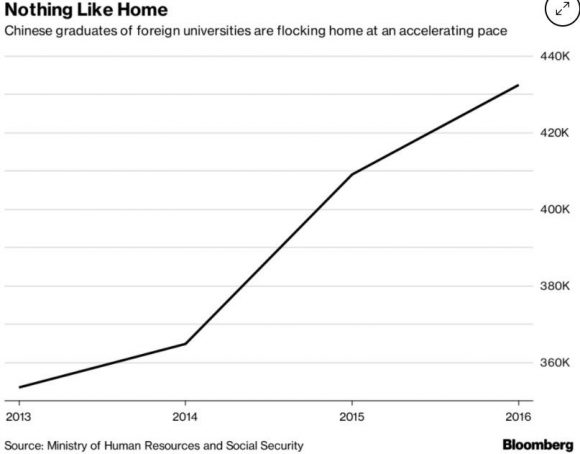

Ironically enough, there are more AI computer scientists of Chinese origin in America than there are in all of China.

There is a huge movement by the Chinese private sector to bring everyone back home as China vies to become the industry leader in AI.

Silicon Valley is on the verge of a brain drain of mythical proportions.

If America allows all these brilliant minds to fly home, not only to China but everywhere else, America is just training these workers to compete against American companies in the future.

A premier example is Baidu co-founder Robin Li who received his master's degree in computer science from the State University of New York at Buffalo in 1994.

After graduation, his first job was at Dow Jones & Company, a subsidiary of News Corps., writing code for the online version of the Wall Street Journal.

During this stint, he developed an algorithm for ranking search results that he patented, flew back to China, created the Google search engine equivalent, and named it Baidu (BIDU).

Robin Li is now one of the richest people in China with a fortune of close to $20 billion.

To show it's not just a one-hit wonder type scenario, three of the top five start-ups are currently headquartered in Beijing and not in California.

The most powerful industry in America's economy is just a transient training hub for foreign nationals before they go home to make the real cash.

More than 70% of tech employees in Silicon Valley, and more than 50% in the San Francisco Bay Area are foreign, according to the 2016 census data.

The point that really hits home is that the insane cost of housing is preventing burgeoning American talent from migrating from rural towns across America and moving to the Bay Area.

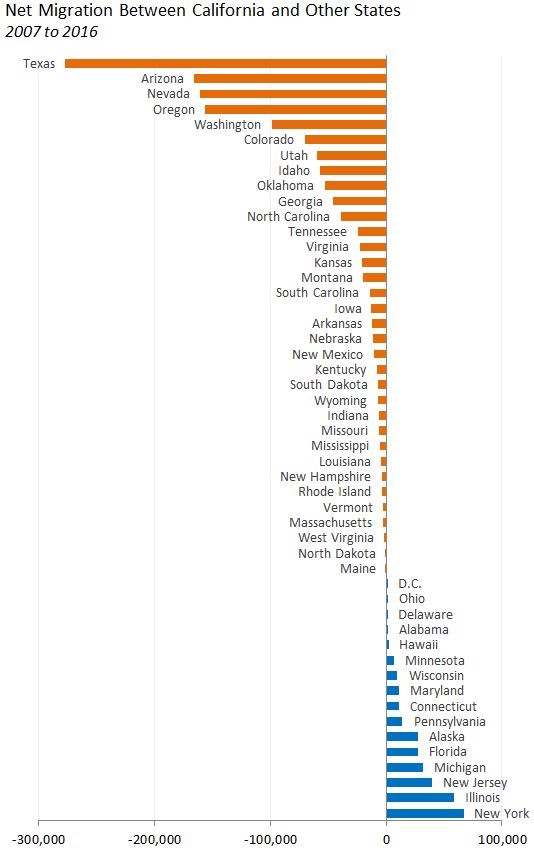

This trend was reinforced by domestic migration statistics.

Between 2007 and 2016, 5 million people moved to California, and 6 million people moved out of the state.

The biggest takeaways are that many of these new California migrants are from New York, possess graduate degrees, and command an annual salary of more than $110,000.

Conversely, Nevada, Arizona, and Texas have major inflows of migrants that mostly earn less than $50,000 per year and are less educated.

That will change in the near future.

Ultimately, if VCs think it is expensive now to operate a start-up in Silicon Valley, it will be costlier in the future.

Pouring gasoline on the flames, Northern Californian schools are starting to close down as there is a lack of students due to minimal household formation.

The biggest complaint is that there is no affordable housing.

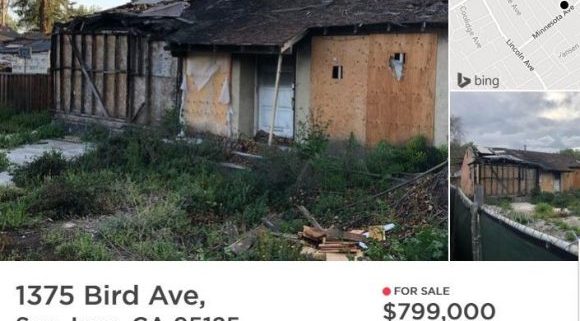

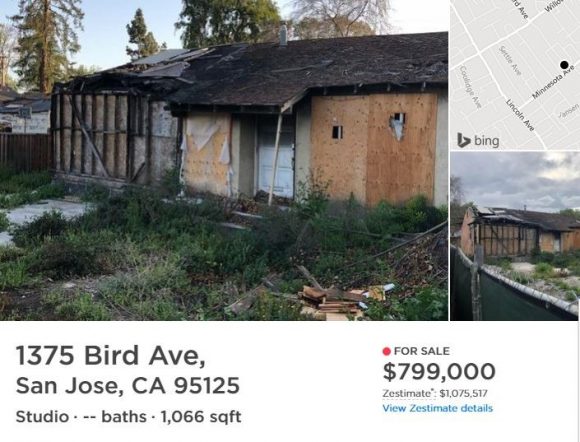

A 1,066-square-foot property in San Jose's Willow Glen neighborhood went on sale for $800,000.

This would be considered an absolute steal at this price, but the catch is the house was badly burned two years ago. This is the price for a teardown.

When you combine the housing crisis with the price readjustment for big data, it looks as if Silicon Valley has peaked.

Yes, the FANGs will continue their gravy train but the next big thing to hit tech will not originate from California.

VCs will overwhelmingly invest in data over rental bills, and the percolation of tech ingenuity will likely pop up in either Nevada, Arizona, Texas, Utah, or yes, even Michigan.

Even though these states attract poorer migrants, the lower cost of housing is beginning to attract tech professionals who can afford more than a burnt down shack.

Washington state has become a hotbed for Bitcoin activity. Small rural counties set in the Columbia Basin such as Chelan, Douglas, and Grant used to be farmland.

The bitcoin industry moved three hours east of Seattle for one reason and one reason only - cost.

Electricity is five times cheaper there because of fluid access to plentiful hydro-electric power.

Many business decisions come down to cost, and a fractional advantage of pennies.

Once millennials desire to form families, the only choices are regions where housing costs are affordable and areas that aren't bereft of tech talent.

Cities such as Las Vegas and Reno in Nevada; Austin, Texas; Phoenix, Arizona; and Salt Lake City, Utah, will turn into hotbeds of West Coast growth engines just as Hangzhou-based Alibaba (BABA) turned that city into more than a sleepy backwater town with a big lake at its center.

The overarching theme of decentralizing is taking the world by storm. The built-up power levers in Northern California are overheated, and the decentralization process will take many years to flow into the direction of these smaller but growing cities.

Salt Lake City, known as Silicon Slopes, has been a tech magnet of late with big players such as Adobe (ADBE), Twitter (TWTR), and EA Sports (EA) opening new branches there while Reno has become a massive hotspot for data server farms. Nearby Sparks hosts Tesla's Gigafactory 1 and most likely its next addition.

The half a billion-dollars required to build a proper tech company will stretch further in Austin or Las Vegas, and most of the funds will be reserved for tech talent - not slum landlords.

The nail in the coffin will be the millions saved in taxes.

The rise of the second-tier cities is the key to staying ahead of the race for tech supremacy.

__________________________________________________________________________________________________

Quote of the Day

"Twitter is about moving words. Square is about moving money." - said CEO of Twitter, Jack Dorsey, to The New Yorker, October 2013

Mad Hedge Technology Letter

April 11, 2018

Fiat Lux

Featured Trade:

(WHY YOU SHOULD BE BETTING THE RANCH ON TECHNOLOGY),

(AMZN), (NFLX), (FB), (Samsung), (Tencent)

Global IT spending is forecasted to surpass $3.7 trillion in 2018, a boost of 6.2% YOY, according to a report released by leading technology research firm Gartner, Inc. (IT).

This year is the best growth rate forecasted since 2007, and is a precursor to a period of flourishing IT growth.

IT budgetary resilience is oddly occurring in the face of a tech backlash engulfing Mark Zuckerberg as collateral damage during higher than normal volatility due to an unstable geo-political environment and nonstop chaos in the White House.

Zuckerberg's reputation has been torn to shreds by the media and politicians alike.

Tech has had better weeks and months, for instance as this past January when tech stocks went up every day. Facebook (FB) still had a great business model in January as well.

The biggest takeaway from the report was the outsized capital investments going into enterprise software, which spurs on exponential business formation.

Enterprise software will successfully record its highest spend rate increasing by 11.1% YOY to $391 billion. This is far and away an abnormally fast pace of increase, but is completely justified based on every brick and mortar migrating toward data harnessing.

The software industry will benefit immensely by the universal digitization of all facets of life as software acts as the tool that businessmen use to propel companies to stardom.

Application software spending will healthily rise into 2019, and infrastructure software also will continue to grow, boosted by the revamping of laggard architecture.

Data center systems are predicted to grow 3.7% in 2018, down from 6.3 percent growth in 2017. The longer-term outlook continues to have challenges, particularly for the storage segment.

The lower relative rate of spend is exacerbated by the chip shortage for memory components, and prices have shot up faster than previously expected.

The new Samsung Galaxy 9 cost an additional $45 in semiconductor chip costs because of the importunate costs that sabotage cost structures.

Exorbitant pricing was set to subside in the early part of 2018, but the dire shortage of chips is here to stay until the end of 2018.

Even though the supply side has ramped up 30%, demand is far outpacing supply, spoiling any chance for tech devices to be made on the cheap.

Global spend for digital devices will grow in 2018, reaching $706 billion, an increase of 6.6 percent from 2017. Not only will we see the standard characters such as phones and tablets, but new creative ways to produce devices in the micro-variety will soon populate our shores.

Amazon Alexa and Apple's HomePod are just the beginning and will spawn micro-devices that would fit nicely into a flashy James Bond film.

The demand for ultra-mobile premium smartphones will slow in 2018 as more consumers delay their upgrade and feel comfortable using older devices -- kind of like a smashed-up Volvo station wagon handed down from sibling to sibling.

In times of uncertainty, corporations hold back spending until the near-term variables can be flushed out, and unforeseen costs causing operational turbulence can be anticipated.

However, the industry has brushed aside the turmoil that has attempted to infiltrate the core growth story.

Investors cannot overlook that total tech spending growth for 2018 is the highest in the past 15 years.

Next quarter's earnings are now on tap, and investors will turn to fundamentals as a cheat sheet for what's in store.

It's undeniable that currently tech stocks aren't cheap anymore. They are also more expensive than they were at the beginning of the year barring Facebook and a few other stragglers.

The momentum has intensified with the five biggest tech firms accounting for more than 14% of the S&P 500 index's weighting.

Tech's relative performance has fended off the bears with PE multiples down a paltry 4.9% this year compared to the cratering of 11.4% in the general market.

And tech is still trading at a tiny fraction of the crisis of the dot-com era.

The outsized reinvestments back into business models don't tell the tale of an industry brought down to its knees begging for salvation.

Look no further than across the Pacific Ocean. Samsung Electronics Co. represents almost 25% in South Korea's Kospi index. At the same time, Asia's most valuable company, Tencent Holdings, makes up almost a 10% weighting in Hong Kong's Hang Seng Index.

Back stateside, about 90% of US tech firms beat revenue estimates in the last quarter of 2017, marking the best success rate for any industry.

The positive sentiment has continued into this year with wildly bullish expectations led by the FANG stocks.

The broader volatility is a gift to investors who hesitated and missed the monster rally that has graced tech the past few years.

Tech is vital to emerging markets. And this is the first year since 2004 that tech constitutes the biggest sector in the MSCI Emerging Markets Index blowing past financials.

Tech had a 28% weighting at the end of 2017, the weighting more than doubling from six years ago.

As it stands today, tech enjoys light regulation and by a long mile. Tech is actually the least regulated industry in America and has used this period of light regulation to stack up profits to the sky.

Banks are nine times more regulated than tech companies, and manufacturing companies are five times more regulated.

Legislation such as Dodd-Frank has done a lot to taper the excesses of the sub-prime frenzy that almost took down Wall Street.

The lean regulation has helped tech companies such as Facebook and Google build a gilt-edged competitive advantage that has been exploited to full effect.

After the Fed closed the curtains on its QE program, tech and its earnings are the sturdiest pillar of the nine-year bull market.

The Street is reliant on the big players to earn its crust of bread and show investors that tech isn't just a flash in the pan.

The two numbers acting as the de-facto indicators of the health of the overall economy are Netflix's subscriber growth numbers and Amazon's AWS Cloud revenue.

These two companies do not focus on profits and are the prototypical tech growth companies.

If they beat on these metrics, the rest of tech should follow suit.

The market is entirely dependent on big tech to drag investors through the time of transition. My bet is that tech will over-deliver booking stellar earnings.

__________________________________________________________________________________________________

Quote of the Day

"By giving the people the power to share, we're making the world more transparent." - said Facebook CEO Mark Zuckerberg

Mad Hedge Technology Letter

April 5, 2018

Fiat Lux

Featured Trade:

(GOOGLE IS FIRING ON ALL CYLINDERS ... BUY THE DIP),

(GOOGL), (FB), (AMZN), (AAPL), (MSFT)

Google (GOOGL) makes bucket loads of money and even makes Facebook's (FB) business model look dwarfish.

Total revenue in 2017 came in at more than $110 billion, up 23% YOY and almost three times larger than Facebook's annual revenue of $40.65 billion in 2017.

It's easy to comprehend why the big keep getting bigger if you understand the basic trajectory of technology companies.

A new report from the search consulting firm Adthena chronicled the flow of ad dollars into digital e-commerce and found that retailers are spending 76.4% of total ad budget on Google shopping ads.

Last year was a record-breaking year for total digital ad revenue, and this year the industry is slated to grow another 20%.

Young people aren't watching television as they used to and are more comfortable using computers, tablets, and smartphones to gorge on their entertainment and work.

By 2020, digital ads will comprise 44.6% of total ad revenue as cord-cutting by consumers accelerates and broadband streaming becomes the norm across all of America and the world.

Mobile is the triumphant victor here as the majority of dollars will migrate to smartphone platforms.

China and America will overwhelmingly make up the bulk of digital ad spend, and Europe will remain a distant third.

Last quarter, Alphabet missed Wall Street expectations on the bottom line failing to reach earnings per share (EPS) targets of $9.98. The $9.70 miss wasn't a total failure but disappointing enough for Alphabet shares to nosedive.

Alphabet has positioned itself perfectly for the future and has many irons in the fire.

Google's ad business remains its go-to segment totaling $27.27 billion in revenue in Q4, a main driver of outperformance.

Cost per click (CPC) decreased slightly less than what analysts expected, but that was the trigger for a quick dip in share prices even though Alphabet beat on the top line.

In total, it is immaterial if Alphabet misses slightly on this metric. And, coincidentally, Alphabet is changing the way it calculates ad fees by switching over to cost per impression (CPI), which charges advertisers for raw viewing of an ad.

This pricing mechanism will create higher margins that slightly suffered last quarter because advertisers now are charged for users not clicking an ad as well.

(CPC) has been eroding for years. Alphabet attributes the slight dip to the widespread migration to mobile and the importance of YouTube ads, which yield lower rates than desktop ads.

Alphabet's "other revenues" segment, including its burgeoning enterprise business, hardware sales, and app store Google Play, posted $4.69 billion in revenue, bringing total Google revenue to $31.91 billion in Q4 2017.

Google search, the premier legacy business in tech, still comprises 85% of total revenue. Crucially, the cash mountain procured aids in capital allocation. Alphabet heavily reinvests back into different parts of the business or M&A.

Certainly, it has laid some eggs such as the Google glasses and its attempt at social media through Google+, which flamed out, too.

Many of these new projects originate from the 20% of work time that is allocated to free-spirited entrepreneurship. This initiative has harvested benefits spawning from Google news and other supplementary projects.

Alphabet's innovative qualities feedback into their core product as well, but management understands it needs to evolve to meet the capricious needs of users.

Google founders Sergey Brin and Larry Page thirst for a fresh injection of vivacity into their business and added several outside valuable pieces that include YouTube, Motorola, and Nest Labs for around $17 billion.

These growth engines will fit nicely under the umbrella of firms that Google has collated.

The cloud segment has become a "billion dollar per quarter business." It is dwarfed by the ad revenue but is still the glue that holds the firm together because of the heavy reliance of big data storage to power its firm.

The cloud is still a small sliver of the business and trails Amazon (AMZN), and Microsoft's (MSFT) cloud businesses, but Google drive cloud platform was "the fastest growing major public cloud provider" in 2017.

Apple (AAPL) has even subcontracted Google to store iPhone data on its Google cloud. I bet you didn't know that.

The cloud will continue to gain momentum for Google. Developing the best search engine in the world makes the company specialists in harvesting data because refining a search engine takes an extraordinary amount of data to fine-tune the user searches to perfection.

There are a few headwinds Alphabet is coping with, predominantly traffic-acquisition costs (TAC) as a percentage of revenue will continue to rise, but the increase in velocity will taper off by mid-2018.

Google's total (TAC), which includes funds it pays to phone manufacturers such as Apple that integrates its services, such as search, hit $6.45 billion, or 24% of Google's advertising revenues.

The rising cost of finding eyeballs will squeeze margins.

Another bogey on the horizon is Amazon's foray into the digital ad sphere. It possesses the quality of data to claw away market share and could damage the comprehensive duopoly that Alphabet enjoys with Facebook.

Large cap tech is competing with each other in almost every critical industry guided by the invisible hand of a massive treasure trove of big data. This is unavoidable.

Alphabet's other gambles such as smart-home hardware maker Nest Labs and health-care company Verily are bets on the future as all big tech firms position themselves to compete in a myriad of emerging industries.

These products aren't expected to harvest profits for years and lost Alphabet a combined $500 million last year.

There are a few companies that are perfectly aligned with the direction of future business and technological development, and Alphabet is one of them.

Whether the autonomous vehicle subsidiary Waymo or its smart-home investment in Nest Labs, Alphabet is diversified into most of the cutting-edge trends moving forward.

If the sushi hits the fan with its up-and-coming segments, Alphabet can always fall back on what it knows best - selling ads.

__________________________________________________________________________________________________

Quote of the Day

"We want Google to be the third half of your brain." - said co-founder of Google and president of Alphabet, Sergey Brin.

Mad Hedge Technology Letter

April 4, 2018

Fiat Lux

Featured Trade:

(SPOTIFY KILLS IT ON LISTING DAY),

(SPOT), (DBX), (GOOGL), (AAPL), (AMZN), (CRM), (NFLX), (FB)

The banner year for the cloud continues as Dropbox's (DBX) blowout IPO passed with flying colors.

Investors' voracity for anything connecting to big data continues unabated.

Big data shares are now fetching a big premium, and recent negative news has highlighted how important big data is to every business.

Let's face it, Spotify (SPOT) needs capital to reinvest into its platform to achieve the type of scale that deems margins healthy enough to profit, even though it says it doesn't.

Big data architecture takes time to cultivate, but more importantly it costs a huge chunk of money to construct a platform worthy enough to satisfy consumers.

The daunting proposition of competing with the FANGs for users only makes sense if there is a reservoir of funds to accompany the fight.

Spotify CEO Daniel Ek has milked the private market for funding, making himself a multibillionaire in the process. And as another avenue of capital raising, he might as well go to the public to fund the venture in the future.

Cloud and big data companies have identified the insatiable investor appetite for their services. Crystalizing this sentiment is Salesforce's (CRM) recent purchase of MuleSoft - integration software that connects apps, data, and devices - for 18% more than its original offer for $6.5 billion.

The price was so exorbitant, analysts speculated that a price war broke out, but Salesforce paid such a high price because it is convinced that MuleSoft will triple in size by 2021. That is another great trading opportunity missed by you and me.

An 18% premium to the original price will seem like peanuts in five years. The year 2018 is unequivocally a sellers' market from the chips up to the end product and everything in between on the supply chain.

Spotify cannot make money if it's not scaled to 150 million users, compared to its current 76 million. And 200 million and 300 million would give CEO Daniel Ek peace of mind, but it's a hard slog.

Pouring gas on the fire, Spotify is going public at the worst possible time as tech stocks have been the recipient of a regulatory witch hunt pounding the NASDAQ, sending it firmly into correction territory.

Next up was Spotify's day to shine in the sun directly listing its stock.

Existing investors and Spotify employees are free to unload shares all they want, or load up on the first day. In addition, no new shares are being issued. This is unprecedented in the history of new NYSE listings.

Spotify is betting on its brand recognition and massive desire for big data accumulation. It worked big time, with a first day's closing price of $149, verses initial low ball estimates of $49.

Cloud companies are the cream of the big data crop, but Spotify's data hoard will contain every miniscule music preference and detail a human can possibly exhibit for potentially 100 million-plus people.

Spotify's data will become the most valuable music data in the world and for that it is worth paying.

But at what price?

Spotify has no investment bankers, and circumnavigating the hair-raising fees a bank would earn is a bold statement for the entire tech industry.

Sidestepping the traditional process has ruffled some feathers in the financial industry.

The mere fact that Spotify has the gall to execute a direct listing is just the precursor to big banks being phased out of the profitable investment banking sector.

Goldman Sachs (GS) was the lead advisor on Dropbox's (DBX) traditional IPO, and it was a resounding success rocketing 40% a few days after going public.

IPOs are not cheap.

The numbers are a tad misleading because Spotify paid about $40 million in advisory to the big investment banks leading up to the big day.

This is about a $28 million less than when Snapchat (SNAP) went public last year.

Uber and Lyft almost certainly would consider this option if Spotify nails its IPO day.

Banks are being squeezed from all sides as nimble, unregulated tech firms have proved better adaptable in this quickly changing environment.

Spotify's business model is based on spectacular future growth, which may occur.

It is a loss-making company that produces no proprietary solutions but is overlooked for its valuable data.

The company is the market leader in paid subscribers at 76 million, far outpacing Apple Music at 39 million and Pandora at 5.5 million.

Total MAUs (Monthly Active Users) expect to reach more than 200 million users, and paid subscribers could hit the 96 million mark by the end of 2018.

Spotify's business model bets on transforming the free subscribers who use Spotify with ad-supported interfaces into paid subscribers that are ad-free. Converting a small amount would be highly positive.

Gross margin is a number that sheds light on the real efficiencies of the company, and Spotify hopes to hit the 25% gross margin point by the end of 2018.

I am highly skeptical that gross margins can rise that high unless they solve the music royalty problem.

Royalty costs are killer, forcing Spotify to shell out a massive $9.75 billion in music royalties since its inception in 2006.

Spotify is paying too much for its content, but that is the cruel nature of the music industry.

The ideal solution would eventually amount to producing high quality original entertainment content on its proprietary platform akin to Netflix's (NFLX) business model with video content.

Spotify's capital is being drained by royalty fees amounting to 79% of its revenue.

This needs to be stopped. It's a losing strategy.

Considering Google (GOOGL) and Facebook (FB) do not pay for their own content, it frees up capital to pile into the pure technical side of the operations, enhancing their ad platforms luring in new users.

This is why the Mad Hedge Technology Letter sent you an urgent Trade Alert to buy Google yesterday when it was trading at $1,000.

All told, Spotify has managed to lose $2.9 billion since it was created 12 years ago - enough capital to create a new FANG in its own right.

Dropbox was an outstanding success and attaching itself to the parabolic cloud industry is ingenious.

However, potential insane volatility should temper investors' expectations for the first day of trading.

The lack of a road show, no lockup period, and no underwriting or book building will sacrifice stability in the short term.

There is incontestably a place for Spotify, and the expected 30% to 36% growth in 2018 looks attractive.

But then again, I would rather jump into sturdier names such as Lam Research (LRCX), Nvidia (NVDA), and Amazon (AMZN) once markets quiet down.

The private deals that took place before the IPO changed hands were in the range of $99 to $150. Considering the reference point will be set at $132, nabbing Spotify under $100 would be a great deal.

The market will determine the opening price by analyzing the buy and sell orders for the day with the help of Citadel Securities.

It's a risky proposition that 91% of shares are tradable upon the open. Theoretically, all these shares could be sold immediately after the open.

Legging into limit orders below $140 is the only prudent strategy for this gutsy IPO, but better to sit and observe.

__________________________________________________________________________________________________

Quote of the Day

"One of the only ways to get out of a tight box is to invent your way out." - Amazon CEO Jeff Bezos

Mad Hedge Technology Letter

April 3, 2018

Fiat Lux

Featured Trade:

(THE BIG WINNER FROM THE PHOENIX CAR CRASH),

(WAYMO), (TSLA), (GOOGL), (AAPL), (AMZN), (UBER), (GM), (FB)

In 2014, the juicy sound clips recorded by NFL legend Chris Carter at the annual NFL rookie symposium would be enough for those at league headquarters to have nervous breakdowns.

During a keynote speech, Chris Carter recommended that every rookie about to kick-start a sports career should find a "fall guy" just in case they found themselves on the wrong side of the law.

Carter later rescinded his comments and sincerely apologized for insinuating marginal tactics.

Lo and behold, it seems the most attentive listeners at the symposium weren't the players but the swashbuckling chauffeur-share service that has become the "fall guy" of Big Tech, none other than Uber.

The great thing (read: sarcastic here) for Uber about killing a pedestrian with autonomous vehicle technology is that it does not need to change its Silicon Valley mind-set of "move fast and break things."

Everything Uber touches seems to turn to mush. At least lately.

This revelation is extremely bullish for the other big players in the A.I. (Artificial Intelligence) driverless car space, mainly Waymo and General Motors (GM).

Granted, Uber came late to the party, but that cannot be an excuse for the myriad of shortcuts it promotes to build its business.

Waymo, the autonomous subsidiary of Google (GOOGL), has been honing its software, algorithms, and sensors for the past nine years like a sage samurai swordsmith from Kyoto. This type of detailed nurturing has led Waymo to rack up more than 5 million miles of testing on live roads.

The company recently commenced the first niche ride-hailing service in Phoenix, AZ, and just announced that it will purchase up to 20,000 electric cars from Jaguar Land Rover in a $1 billion deal to outfit with its cutting-edge technology.

Every day is a joyous day for Waymo because the first mover advantage is in full effect.

GM, another laggard, though considered in the top three, won't commence its robotic car fleet until late 2019. However, by that time, Waymo could be on the verge of mass rollouts if there are no setbacks.

The cherry on top for Waymo is Uber's knack of making a dog's breakfast of anything it pursues, magnifying an insurmountable lead for Waymo to possess.

Granted, the autonomous vehicle brain trust expected casualties, and the firm that made news for this mishap would be stuck with this label along with suspended operations.

Waymo missed a direct hit thanks to Uber and Tesla.

Tesla also took a direct hit when it announced that Walter Huang, an Apple engineer, sadly was killed in a Model X accident last weekend while his car was on autopilot.

It capped a horrible week by announcing a comprehensive recall of every Model S made before April 2016 for a faulty part. After fighting tooth and nail to maintain the $300 support level, Tesla swiftly sold off down to $250.

The disruption fetish permeating the ranks of the tech industry has its merits. Often the end result manifests through cheaper prices and better consumer services.

However, Uber's over-aggressiveness has placed it at the forefront of the regulation backlash along with Facebook (FB).

Google has certainly been playing its cards right, and having not run over a pedestrian consolidates its leading position

Luckily, the National Transportation Safety Board does not punish every participant using this technology.

No news is good news.

An extensive review of internal processes will hit team morale, and the burden of blame with fall upon the engineers.

The fallout from the tragic incidents will set back Tesla and Uber at least three to six months.

The suspension of their operations is akin to a white flag because Waymo is currently leaps ahead and plans to ramp up the mass rollout in the next two years with technology that is best of breed.

The running joke in the industry is that Uber's autonomous vehicle engineers are comprised of Waymo rejects.

Waymo already has more than 600 for-profit vehicles in operation in Arizona. And as every day without a fatality is considered a success, the Jaguars are next in line to be tricked-out with sensors and software.

Unceremoniously, Waymo has focused on safety as the pillar of its autonomous driving operation. Its conservative attitude toward danger will serve it well in the future. Waymo even spouted that its technology would have avoided the Uber accident.

Waymo has no desire to physically produce cars, but it aspires to sell licenses to the technology that could be installed in trucks and delivery vehicles, too.

The licenses could act as de-facto SaaS (software as a service) reoccurring revenue that has catapulted cloud companies to untold heights.

Google would also be able to integrate Google Maps, Google Docs, and all Google services into the robot-cab experience. The robo-taxi would merely serve as an incubation chamber to use the plethora of Google services while being transported from point A to point B.

And with Uber temporarily wiped off the map, Waymo seems like a great bet to monetize this segment at massive scale.

Google is truly on a roll as of late, even finding the perfect fall guy for the big data leak that has roiled the tech world, inducing a wicked tech sell-off - Facebook.

Instead of extracting data from user-posted content, Google's search builds a profile on users' search tendencies, and it is just as culpable in this ordeal.

Ironically, all the heat is coming down on Facebook's plate, and Mark Zuckerberg's lack of tactical PR noise is cause for investor concern.

The mountains of cash vaulted up over the years has made barriers of entry into new fields simple.

For example, Amazon's desire to lead health care came out of left field, and 10 years ago nobody ever thought the iPod company would make smart watches.

The interesting development in broader tech is the disintegration of unity that once supported the backbone of these firms.

Tim Cook, chief executive officer of Apple, railed on Facebook's business model and trashed Mark Zuckerberg's blatant disregard for privacy in order to profit from people's personal lives.

Large cap tech has never had as much overlap as it does now, and the new normal is throwing others under the bus.

If Google is dragged into the Facebook regulatory orbit, the silver lining is that the world's best autonomous driving technology will soon transform its narrative and put its incredibly profitable search business on the back burner.

Markets are forward looking and reward outstanding growth stories.

Tech is growth.

Morgan Stanley issued a report claiming the repercussions of mass-integrating this technology would be to the tune of about half a trillion dollars. That includes the $18 billion saved in annual health costs to automotive injuries. Also, 42% of police work ignites from a simple traffic stop. This would vanish overnight as well as concrete parking garages that blight cities. Car insurance is another industry that will be swept into the dustbin of ancient history.

Yes, tech has evolved that fast when Google can start claiming its revered search business as the daunted L word - legacy business.

The fog of war is starting to burn off and the visible winner is Waymo.

The shaping of its autonomous vehicle business is starting to take concrete form and although this won't affect earnings in the next few years, it will be a game changer of monumental proportions.

Uber is seriously in the throes of having an existential problem because of Waymo's outperformance. Venture capitalists heavily invested in Uber because of the promises of autonomous vehicle technology.

This is its entire growth story of the future.

Without it, it is a simple taxi company run on an app. There is no competitive advantage.

Waymo is on the verge of creating a scintillating growth business that is effectively Uber without a driver while simultaneously destroying Uber.

Ouch!

It speaks volumes to the ascendancy. And if Waymo miraculously capitulates, Google can always call Chris Carter and find another "fall guy."

__________________________________________________________________________________________________

Quote of the Day

Asked what he would do if he was Mark Zuckerberg, Apple CEO Tim Cook said, "I wouldn't be in this situation."