Mad Hedge Biotech & Healthcare Letter

July 2, 2020

Fiat Lux

Featured Trade:

(FIVE BIOTECH STOCKS TO BUY AT THE MARKET TOP)

(REGN), (GILD), (PFE), (ABBV)

Mad Hedge Biotech & Healthcare Letter

July 2, 2020

Fiat Lux

Featured Trade:

(FIVE BIOTECH STOCKS TO BUY AT THE MARKET TOP)

(REGN), (GILD), (PFE), (ABBV)

No, this is not a typo, a misprint, nor an alcohol-induced departure from reality. I only buy stocks at market tops when I believe that newer, higher market tops are imminent. That is certainly the case with the entire biotech sector.

That’s why I moved this morning into a very aggressive triple weighting to the sector.

As the world grapples with the COVID-19 pandemic, Regeneron (REGN) has been hailed as one of the “miracle stocks” in the biotechnology sector.

Although late to the party, Regeneron quickly became a frontrunner in the race to find a COVID-19 treatment in June when the company entered clinical trials with its COVID-19 treatment candidate. The New York biotechnology company has already started manufacturing, with the company expecting trial results to be released later this summer.

Regeneron followed the lead of other biotechnology companies repurposing seasoned medicines to treat this deadly disease, such as Gilead Sciences (GILD) and Pfizer (PFE).

Prior to developing it to target SARS-CoV-2, Regeneron’s antibody cocktail had been used to treat Ebola.

In response to Regeneron’s promising progress on the COVID-19 treatment, the market showed its appreciation by pushing the company’s shares up over 60% year-to-date.

Needless to say, Regeneron has been heavily outperforming the broad biotechnology indexes and even the broader market.

However, Regeneron’s success these days isn’t only attributed to its COVID-19 efforts. In fact, Regeneron’s annual revenue has been consistently increasing for more than a decade now.

Prior to starting its coronavirus program, the company has already lined up several candidates that can serve as catalysts for growth.

One of the catalysts for Regeneron’s growth is skin cancer injection Libtayo.

At present, Libtayo dominates the advanced cutaneous squamous cell carcinoma market as seen in the 179% jump in its sales to hit $75 million in the first quarter of 2020.

Riding on the momentum of Libtayo’s current sales, Regeneron is also looking to expand its coverage to include non-small cell lung cancer and basal cell carcinoma.

This means that Libtayo still has a long way to go before it reaches its peak.

To give this drug’s potential some context, keep in mind that roughly 9,500 individuals in the United States alone get a skin cancer diagnosis every day. Meanwhile, over 3 million Americans are diagnosed with either basal cell carcinoma or squamous cell carcinoma each year.

As for non-small cell lung cancer, this disease accounts for 84% of over 228,000 cases of lung cancer in the US annually.

Combined, the market size of Libtayo could reach roughly 3.2 million patients.

Libtayo is priced at $9,100 to cover a three-week treatment course. Patients are advised to regularly take the infusion every three weeks. This puts the annual cost of Libtayo treatment somewhere around $158,000.

With this annual treatment cost and the projected total market size in mind, it’s safe to say that Libtayo can yield profits of well over 12 figures. This is the best-case scenario, though.

If we go for the least likely scenario, where Regeneron only reaches 10,000 patients for all the diseases mentioned, then the company can still generate an annual revenue exceeding $1.5 billion.

As for the other products in Regeneron’s pipeline, the company’s recent earnings report showed that sales in the first quarter were only marginally impacted by the pandemic.

For instance, Eylea’s annual growth rate was only at 6%. Nonetheless, this wet macular degeneration and metastatic colorectal cancer medication’s first quarter sales still reached a decent $1.9 billion.

Moreover, there’s a growing market that can substantially boost Eylea’s performance in the coming years.

Studies show that the global market for wet age-related macular degeneration is projected to rise at an annual rate of 7.1%. By 2024, this market could reach $10.4 billion.

Aside from Eylea, Regeneron’s eczema biologic Dupixent sales have been soaring as well. This drug went up by an impressive 124% year-over year, generating $855 million in revenue.

Dubbed as Regeneron’s “pipeline in a product,” the company is looking to transform Dupixent into a mega-blockbuster drug like AbbVie’s (ABBV) Humira.

So far, Dupixent is being studied to determine if it can also be marketed to asthma patients and recently gained approval to be cover atopic dermatitis as well.

Overall, Regeneron merits a closer look, especially among biotechnology investors searching for a dependable stock with a lot more room to grow.

Not only does the company have over $7.2 billion in cash and have minimal debt, it also has a remarkable profit growth.

In the first quarter of 2020 alone, Regeneron’s bottom line jumped by a whopping 48% year over year to reach $771 million or $6.60 per share.

Looking at its annualized rate, Regeneron stock is actually trading for roughly 22 times earnings -- a reasonable price to pay for a well-rounded blue chip company that offers such impressive growth and a strong track record.

Mad Hedge Biotech & Healthcare Letter

June 25, 2020

Fiat Lux

Featured Trade:

(COVID-19’s STEROID ROADBLOCK)

GILD), (MRNA), (INO), (SVA), (AZN), (MRK), (SNY), (GSK), (NVAX), (JNJ), (PFE), (LLY), (REGN)

Science rarely gets communicated accurately.

Earlier this month, UK health experts said that an existing drug called dexamethasone can cut the risk of death among patients suffering from severe COVID-19.

According to the Oxford University researchers, dexamethasone lowered the COVID-19 deaths by roughly 35% among patients in ventilators and 20% among those who required oxygen.

The experts clarified that this means for every 8 patients on ventilators treated with dexamethasone, they were able to save 1 life.

In response to this study, here’s the gist of what most news outlets reported: “Miracle COVID-19 cure discovered!”

Now, health experts are scrambling to get their voices heard over the loud pronouncements of opportunistic businesses heralding the sale of this life-saving drug.

Days after the UK experts released this information, government authorities have issued warning after warning against stockpiling this drug for personal consumption.

Up until today, they’re still convincing people that dexamethasone is not a community drug and should only be used if prescribed by a medical professional.

That is, dexamethasone is a treatment for the sickest of the sick and should not be used as a preventive treatment.

Here’s how it works, and why it can only be used in severe cases.

The dexamethasone dampens the immune system for patients in ventilators or oxygen. This is effective because in severe cases, the immune system turns against the body, specifically the lungs, causing deaths. That’s what dexamethasone addresses.

This means that dexamethasone cannot be used on mild COVID-19 cases. Patients classified under this category still have relatively healthy immune systems, which would of course be more preferable tools to fight the disease.

Although there has been a misconception about this treatment, this drug is definitely a breakthrough that the world badly needs at the moment. The positive results of its efficacy make it a first-line therapy until a vaccine gets approved.

So far, the leaders in the vaccine race include Moderna (MRNA), Inovio (INO), Sinovac Biotech (SVA), AstraZeneca (AZN)/Oxford, Merck (MRK), Sanofi (SNY), GlaxoSmithKline (GSK), Novavax (NVAX), Johnson & Johnson (JNJ), and Pfizer (PFE).

Dexamethasone has been around for almost 60 years, making the drug available practically everywhere.

It’s also safe since dexamethasone is included in the WHO’s list of essential drugs.

What we know is that this drug has been approved by the UK government to be used on COVID-19 patients in ventilators and oxygen.

Before being identified as a potential COVID-19 cure, dexamethasone has been widely used as a steroid treatment for rheumatoid arthritis, asthma, bowel disorders, skin disease, and some cancers.

The average retail cost of this drug is around $50 per 10mg. Since the treatment only requires a low dosage, the price would fall somewhere between $6 to $8 per patient.

Needless to say, this cheap treatment could hurt the sales of competing drugmakers aiming to come up with their own COVID-19 cure.

To date, the leaders in this field include Eli Lilly (LLY), Regeneron (REGN), and of course, Gilead Sciences (GILD).

Among those, the only treatment to show a noticeable effect in treating severe COVID-19 patients is Gilead’s Remdesivir.

Although Remdesivir has not been hailed as a miracle cure, this Gilead product managed to offer sufficient benefits to fuel demand.

According to its Phase 3 trial data, 65% of patients dosed with Remdesivir for five days showed better clinical improvement compared to a standard-of-care group.

When the pandemic broke out, Gilead announced that it’s giving away its remaining supply of Remdesivir, which amounts to roughly 1.5 million doses.

Nonetheless, the company disclosed that it plans to invest up to $1 billion on the development of the drug for COVID-19 patients.

Since government funding also comprises a portion of Remdesivir’s development, the arrangement inevitably raises the question of how much revenue the drug can generate.

After all, pricing will definitely be crucial because the company will have to strike a balance between making an acceptable profit and offering an affordable cure to patients.

Financial analysts estimate that Remdesivir’s potential profit could reach $7.7 billion by 2022.

If these estimates turn out right, then Gilead investors are sitting on a veritable gold mine.

Regardless of Remdesivir’s sales, Gilead remains a giant biotechnology and pharmaceutical company with a market capitalization of $97.18 billion.

In fact, it’s considered as one of the recession-resistant companies today thanks to its diversified portfolio and strategic acquisitions.

One of the main reasons for its stature in the industry is the fact that Gilead continues to be the definitive leader in the HIV market today.

Its top-selling drug Biktarvy recorded an impressive $4.1 billion in sales for the first quarter of 2020 alone, a substantial increase from its $3.6 billion earnings during the same period in 2019.

On top of that, Gilead secured patent exclusivity for Biktarvy until the early 2030s. This all but guarantees that the company’s cash cow remains safe from competition for many years.

The expansion of gene therapy Yescarta to cover the European market also proved to be effective. Sales of this lymphoma treatment jumped from $96 million in the first quarter of 2019 to $140 million in the same period this year.

Meanwhile, Gilead’s $4.9 billion acquisition of Forty Seven in April this year indicated the company’s move to expand its oncology sector. Specifically, blood cancer therapy Magrolimab is projected as the next blockbuster.

All these demonstrate that Gilead is well-positioned to handle major financial and even health crises.

More importantly, Gilead’s position as a leader in the search for a COVID-19 cure indicates its capacity to withstand a possible second wave of this pandemic as well as the potential to boost its sales in the process.

Global Market Comments

June 22, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR THE FED RIDES AGAIN),

(TLT), (SPY), (TSLA), (IBB), (AMGN), (GILD), (ILMN)

The free Fed put was tested once again last week, and once again it held. It seems that the line in the sand is $300 for the (SPY), and if that doesn’t hold, $270 will do. At least, for a month.

How long this game will last is anyone’s guess. $14 trillion is a lot of money to throw at the problem. But then so are US Covid-19 deaths approaching 1,000 a day. Who knows what Jay Powell has up his sleeve? Probably quite a lot.

A large chunk of the US economy has gone missing and is never coming back, especially the portion represented by small companies. Whether stock investors will notice this will be the big bet for the remainder of 2020. My bet is they will if the spread of the epidemic can’t be stopped. I give it a 50/50 chance.

If the worst-case scenario happens, get ready to load the boat of LEAPS once again, for we have a Roaring Twenties and second American Golden Age ahead of us, if you can live to see it. We are one wonder drug discovery away from that starting tomorrow morning at 9:00 AM.

We got encouraging news last week with the commonplace steroid dexamethasone, which reduces deaths by 30%. Publishing the Mad Hedge Biotechnology & Health Care Letter, I can tell you there are hundreds more drugs like this under rapid development. Click here.

There is no doubt that biotech stocks (IBB) are breaking out to the upside. Take a look at the ten largest components of the iShares NASDAQ Biotechnology ETF and you’ll see they all have virtually the same chart (click here), stocks like Amgen (AMGN), Gilead Sciences (GILD), and Illumina (ILMN)

The trillions of dollars pouring into Covid-19 research is a big driver. In the meantime, past headaches have magically gone away, like the threat of a nationalization and drug price controls. No one feels like regulating drug companies in this environment. Almost all impediments to research have been tossed away. Relative to the rest of the superheated stock market, biotech shares are still cheap.

The Fed is to starting to buy individual bonds, in another unprecedented expansion of quantitative easing. They are clearly worried about exploding Corona cases, as I am. US Treasury bonds (TLT) dove two points on the news as this may represent a diversion of Fed buying from that market. Stocks soared 1,000 points.

The big message is more QE to come. Another election play? It is called “QE Infinity” for a reason. It’s a great level to trade against. I hope you loaded up on tech LEAPS at the bottom, as I begged you to do.

The Fed balance sheet soars, from $4 trillion to $7 trillion this year, says Fed governor Jay Powell. It is the fastest debt blow up in history. That’s $18,750 per taxpayer in four months. It could be $10 trillion by yearend. If you received less than this stimulus money, you got screwed. This always ends in stagflation….high inflation and slow growth, like we saw after the Vietnam War. Your grandkids are going to have to take side jobs driving for Uber to pay off this bill.

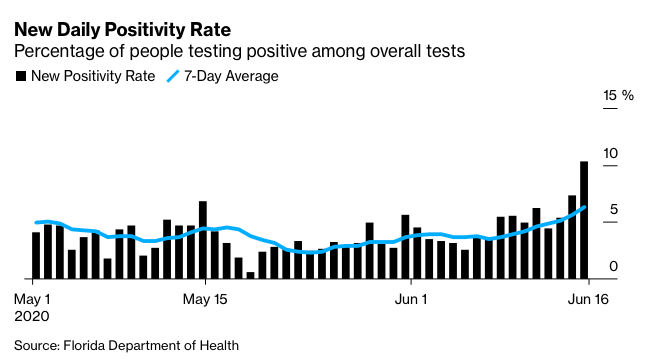

Reopening states see corona cases explode, tossing the “V” shaped economic recovery out the window. Some 25 states are seeing a rapid rise in new cases. Is this the second wave or an extension of the first? The green shoots have been squashed. Stocks won’t like it. The free pass is over.

Stocks pop on miracle steroid drug that reduces Covid-19 death rates. Dexamethasone is the drug in question, normally used for arthritis treatments. It’s just in time as Beijing is closing down schools again in the wake of a second wave.

A US dollar crash is a sure thing, says my old Morgan Stanley colleague, Steven Roach. I couldn’t agree more. Steve is expecting a 35% swan dive for Uncle Buck. A negative savings rate combined with a retreat from Globalization is a toxic combo. A 1970s type stagflation could ensue.

Weekly Jobless Claims are still sky-high, at 1.51 million, far above estimates. The Dow gave up 300 points at the opening, then quickly clawed it back. Walk down Main Street these days and they are still filled with empty storefronts. Many companies are simply running out of money, unable to wait for a recovery. In the meantime, Corona cases are hitting new records every day. Florida cases are off the charts. Things will get worse before they get better.

Retail Sales posted record pop, up 17.7% in May. You are going to see a lot of these record data points because we are coming off a near-zero base. It will actually take years to get to January business levels. I’m sorry, but the higher the free Fed put drives the stock market, the worse the long-term outlook for the economy is going to be.

Homebuilder Confidence is off the charts, with Sales Expectations jumping 22 points to 68. It’s a positive perfect storm, with record-low 2.90% 30-year fixed rate mortgage, Fed buying of mortgage securities and a massive Millennial tailwind that I have been calling for years. A sudden Corona-driven urban flight is sending customers into the arms of suburban builders. Get into Lennar Homes (LEN), KB Homes (KBH), and Pulte Homes (PHM) on dips if you can.

Tesla (TSLA) to open the second US factory this year, somewhere in the southwest as demand overwhelms supply for electric vehicles, exacerbated by the two-month Corona shutdown. The tax break bidding war has already begun, with Texas and Oklahoma slugging it out. The factory comes with 5,000 jobs. Tesla got its first factory for free, giving stock to Toyota for $10 a share. It was the best investment Toyota ever made.

The Mad Hedge June 4 Traders & Investors Summit recording is up. For those who missed it, I have posted all 9:15 hours of recordings of every speaker. This is a collection of some of the best traders and investors I have stumbled across over the past five decades. To find it, please click here.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

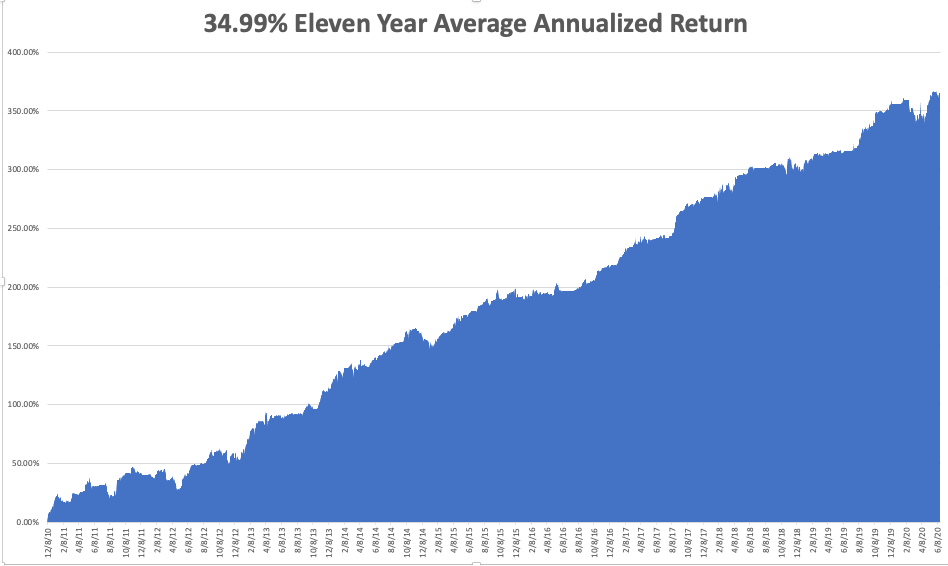

My Global Trading Dispatch performance nicely recouped the pasting we took last week, taking in a nice 7%, bringing June in at +1.21%. With the June options expiration, we managed to cash in on the accelerated time decay in seven positions for Global Trading Dispatch and another three for the Mad Hedge Technology Letter. My eleven-year performance stands at a new all-time high of 367.44%.

That takes my 2020 YTD return up to a more robust +11.53%. This compares to a loss for the Dow Average of -9.2%, up from -37% on March 23. My trailing one-year return popped back up to 51.92%. My eleven-year average annualized profit recovered to +34.99%.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here. On the economic front, some low-grade inflation numbers are published.

On Monday, June 22 at 11:00 AM EST, the May Existing Home Sales are out.

On Tuesday, June 23 at 11:00 AM EST, May New Home Sales are published.

On Wednesday, June 24, at 8:15 AM EST, the National Home Price Index is printed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are published.

On Thursday, June 25 at 8:30 AM EST, Weekly Jobless Claims are announced. Also out it the final figure for Q1 GDP.

On Friday, June 26, at 10:00 AM EST, the Baker Hughes Rig Count is out. At 11:00, we get the University of Michigan Inflation Expectations.

As for me, I’ll spend the weekend modernizing my camping equipment, some pieces of which are WWII surplus, or are at least 50 years old. Since all of the Boy Scout summer camps for the year have been cancelled, such a Philmont and Catalina Island, I’m creating my own.

We’re going on a 50-mile hike around California’s High Sierra Desolation Wilderness, a part of Northern California my family has been fishing at for a hundred years.

We’ll be trekking on the Pacific Crest Trail featured in the film Wild. I’ll try to regale you with pictures on my return and wild fish stories.

It’s easier said than done, for there is a national camping boom going on. It can be difficult to get simple things, like maps, without an August delivery date. Some of my WWII stuff may have to suffice after all.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

June 11, 2020

Fiat Lux

Featured Trade:

(THE BIOTECH MERGER BOOM ACCELERATES)

(AZN), (GILD), (BMY), (ABBV), (AGN), (TAK), (CI), (SNY), (JNJ), (UNH), (RHHBY), (LLY)

Nothing can ever be absolutely shocking in the biotechnology and healthcare world.

I’ll admit though that the reports on AstraZeneca’s (AZN) interest in acquiring Gilead Sciences (GILD) surprised me.

The two companies touched base last month on a potential acquisition deal.

If this rumor turns into a reality, then we’re looking at what could be the biggest healthcare deal to date.

That’s saying something considering the massive mergers we’ve seen in the past years.

So far, the biggest biotechnology and healthcare deal is the $87.6 billion acquisition of Celgene (CELG) by Bristol-Myers Squibb (BMY) in 2019.

In the same year, AbbVie (ABBV) acquired Allergan (AGN) for a whopping $83.8 billion, making it the third biggest deal in the healthcare sector to date.

The year 2018 paved the way for two more massive deals in the form of Takeda’s (TAK) $81 billion acquisition of Shire, which ranks fourth overall, and Cigna’s (CI) $68.4 billion deal with Express Scripts (ESRX) in seventh place.

Fifth on the list is by Sanofi’s (SNY) $73.5 billion deal with Aventis in 2004.

Although it has been two decades since it happened, the $72.5 billion merger of Glaxo and SmithKline Beecham in 2000 still counts as one of the biggest deals in the industry. This agreement gave birth to GlaxoSmithKline (GSK).

Prior to Bristol-Myers Squibb and Celgene deal, it was Pfizer’s (PFE) $87.3 billion acquisition of Warner-Lambert in 1999 that topped the list.

AstraZeneca’s current market capitalization is roughly $140 billion. Meanwhile, Gilead Science’s market cap stands at approximately $96 billion.

With all these in mind, the AstraZeneca-Gilead Sciences merger is estimated to reach roughly $250 billion on top of the significant synergies expected throughout the years.

If these two health industry heavyweights merge, then their newly formed company would become the third biggest healthcare company in the world behind Johnson & Johnson (JNJ), which has a market cap of $384.55 billion, and UnitedHealth Group (UNH) with $293.85 billion.

Looking at this potential merger in the context of the coronavirus race, it’s safe to say that the combined efforts of AstraZeneca and Gilead would create a COVID-19 titan.

AstraZeneca’s partnership with the University of Oxford resulted in a COVID-19 vaccine candidate that was recently selected as one of the top five candidates worthy of US government support through Trump’s Operation Warp Speed program.

Meanwhile, Gilead’s antiviral medication Remdesivir has been constantly hailed as the standard of care for COVID-19 treatment since the pandemic broke.

The drug which was previously marketed as an HIV medication is now expected to generate $2 billion in sales as a COVID-19 treatment in 2020 alone.

In 2022, Remdesivir is estimated to rake in roughly $7.7 billion in sales. After that, the antiviral drug is projected to generate annual sales somewhere between $6 billion and $7 billion.

Although everything is hypothetical, let’s take a quick look at where each company stands at the moment outside their COVID-19 efforts.

AstraZeneca has been a consistent strong stock market performer throughout the years.

In the first quarter of 2020, sales improved in practically all of AstraZeneca’s territories. Although it has a diversified portfolio of drugs and a robust pipeline, the company’s hottest segment is its oncology business.

A good example of this is non-small cell lung cancer treatment Tagrisso, which is starting to live up to expectations as the next mega-blockbuster for AstraZeneca.

The cancer drug’s first quarter sales reached an impressive $982 million, showing off a 56% jump year over year.

This is promising considering that its competitors include Roche’s (RHHBY) Tarceva and Eli Lilly’s (LLY) Cyramza.

As for its 2020 revenue forecast, AstraZeneca is reported to rake in $25 billion, from which it will generate approximately $7.5 billion in operating profit.

On the other hand, Gilead also has an impressive portfolio that it can bring to the table.

In the first quarter of 2020, the company earned $5.47 billion in revenue compared to the $5.20 billion it generated in the same period last year.

Despite the decline in its hepatitis products from $790 million in the first quarter of 2019 to $729 in the same period of 2020, Gilead’s HIV line made up for the loss by bringing in over $4 billion in sales compared to the $3.6 billion it earned last year.

Not only that, some of Gilead’s other candidates are exciting.

For example, rheumatoid arthritis drug Filgotinib is expected to become another blockbuster and generate $5 billion in revenue annually.

Meanwhile, the anti-tumor treatment Magrolimab is estimated to rake in $3 billion in peak sales.

With the company’s older drugs still capable of generating strong revenue and its new candidates showing their potential for revenue expansion, Gilead can be assured of a continued cash flow well into the 2030s.

Regardless of whether this rumored mega-merger pushes through, both Gilead and AstraZeneca are attractive stocks worthy of their premium valuations.

Mad Hedge Biotech & Healthcare Letter

April 30, 2020

Fiat Lux

Featured Trade:

(GILEAD SCIENCES GOES BALLISTIC ON REMDESIVIR TRIAL)

(GILD), (PFE), (JNJ)

Gilead Sciences (GILD) is aggressively pushing to bring the coronavirus disease (COVID-19) to its proverbial knees before this year ends.

The ongoing coronavirus disease (COVID-19) pandemic has brought about substantial disruptions to the world economy, not to mention the devastating losses it caused families watching their loved ones succumb to this deadly virus.

Apart from Gilead, other biotech giants like Pfizer (PFE) and Johnson & Johnson (JNJ) are also hard at work looking for a COVID-19 cure.

Luckily, reports indicate that they may finally see a light at the end of the tunnel as one experimental treatment showed promising efficacy for fighting the health crisis.

Based on the contextual analysis of the leaked information on the clinical trials conducted by Gilead, the biotech company’s decision to bet on Remdesivir as a probable COVID-19 treatment could pay off soon.

At this point, Remdesivir is still under investigation in several Phase 3 clinical trials. These involve more than 2,400 participants scattered in 152 clinical sites.

One of these locations is the University of Chicago Medical Center, where 125 patients who tested positive for COVID-19 are treated every day with infusions of Remdesivir. Out of these individuals, only two deaths were reported with the majority already discharged.

Based on this subgroup alone, the fatality rate among the tested subjects is 1.6%.

Although Remesivir’s results still need further validation particularly in terms of adding a placebo arm in the clinical tests, the initial findings are already quite impressive. For context, data from John Hopkins University revealed that the fatality rate in the entire United States is roughly 4.69%.

Apart from that, another key detail points to the high probability of Remdesivir’s efficacy against COVID-19.

Among the 125 patients who underwent the treatment, 113 of them experienced severe symptoms.

As explained by the World Health Organization, the vast majority of those classified as severe cases involve the elderly and the immunocompromised. In one study, the infection death rate of individuals in this category fall somewhere between 1.93% up to 7.8%

Reassessing Remdesivir’s results from this perspective, we finally understand the excitement surrounding the drug’s efficacy despite the lack of a placebo trial.

In terms of questions on Remdesivir’s economic potential, we can take a look at past respiratory outbreaks like the H1N1 in 2009 and the 1918 Spanish flu for guidance.

Despite “flattening the curve,” at the time, both diseases had resurgences that reached second and third waves after the initial outbreaks were contained.

Combined, the H1N1 and the Spanish flu infected roughly 24% to 33% of the entire global population prior to subsiding for good.

Hence, high demand for Remdesivir will be expected even after the world manages to contain the first COVID-19 outbreak.

What does this mean for Gilead investors?

Remdesivir results are expected to come back positive by the end of April. With the FDA’s Coronavirus Treatment Acceleration Program, the drug is estimated to gain approval in a few months' time.

If successful, Remdesivir is projected to rake in more than $1 billion in sales throughout the coronavirus outbreak period. This estimate is based on the sheer number of people infected and are potentially at risk.

The estimated sales figure is also based on the assumption that Gilead can produce enough Remdesivir supply to treat up to 500,000 patients and that the drug will cost roughly $2,000 for a single-course treatment.

Adding Remdesivir in its lineup, Gilead has adjusted its 2020 revenue guidance to surpass $22 billion with sales growing by more than 4%, thanks to this potential COVID-19 drug alone.

However, Gilead offers more than a promising COVID-19 treatment.

The biotech giant prides itself of a strong lineup, showing off a particular dominance as the market leader for HIV treatments.

Its top HIV drug Biktarvy saw a whopping 300% increase in its sales last year, reaching $4.7 billion in 2019 alone -- and it still hasn’t reached its peak.

Analysts noted that Biktarvy has more room to grow in the next years, with the HIV drug anticipated to continue serving as Gilead’s significant growth driver until 2033.

Another HIV market leader is Descovy, which is set to be the preferred choice among 40% to 45% of patients by the end of 2020.

Despite these promising developments, Gilead stock is still pretty cheap.

To date, this biotechnology company is trading at 13.2 times forward earnings with a measly PEG ratio of 0.3.

At this price -- and considering the company’s strong portfolio and pipeline candidates -- investors on the lookout for biotech exposure but are worried about the consequences of the COVID-19 pandemic should definitely add Gilead into their core holdings.

![]()