Biotechnology stocks have been rallying since mid-June, and it looks like the sector doesn’t have plans of stopping anytime soon.

The SPDR S&P Biotech ETF (XBI), which keeps track of the segment, has been up by 32.5% since the second half of 2022—a period that saw the S&P 500 rise by only 11.4%.

Nonetheless, doubts still linger in terms of how long this sector’s bull run will last. There are also questions on whether the recent shift in market sentiment indicates a substantive change or merely a momentary blip.

News about the biotech industry has been leaning towards the positive in the past months, and hopes for its recovery were bolstered by the much-discussed potential acquisition of Seagen (SEGN) by Merck (MRK).

The strong earnings reports of Regeneron (REGN) and Gilead Sciences (GILD) also added to the overall positivity of the sector.

Meanwhile, another big mover in the biotechnology world appears to be gearing up for a major move soon.

Amgen (AMGN) recently announced its plans to acquire ChemoCentryx (CCXI) for $3.7 billion.

This all-cash acquisition works out to roughly $52 per share and a whopping 115% premium to ChemoCentryx’s price.

ChemoCentryx is mostly known for its autoimmune disorder pipeline. In 2021, the company received FDA approval for Tavneos, which targets a relatively rare autoimmune condition called ANCA-associated vasculitis.

In the first quarter of 2022, Tavneos delivered $5.4 million in sales.

The announcement boosted ChemoCentryx’s shares to skyrocket by 108.4% while Amgen shares remained flat. However, this jump isn’t all too surprising.

The company getting acquired records a jump in stock price after the announcement because the acquirer typically pays a premium for the deal. It’s a strategic move since the higher the premium, the better the chances that the shareholders will approve the acquisition.

If all goes well, this acquisition is expected to be completed by the fourth quarter of 2022.

This move is a good indicator of Amgen’s response to its problem of stagnation. Over the years, this biotech giant has been seemingly left behind in churning out innovative treatments.

Pursuing a promising company like ChemoCentryx is an excellent way to diversify its pipeline and reignite growth.

The deal is especially promising in light of the company’s major setback in 2020 when the Phase 3 clinical trial for its heart failure drug fell short of delivering the promised results.

While issues with new products aren’t exactly new, particularly in the biotechnology sector, Amgen’s failure made investors skittish and led to selloffs.

However, Amgen was not deterred. After all, the setback came following decade-long progress leading up to 2020 when the company’s revenues steadily rose from $15 billion to $23 billion.

In the end, Amgen was still able to surpass its projected revenue to hit the $25 billion mark in 2020 thanks to its strategic move to acquire Otezla from Bristol Myers Squibb (BMY).

By 2021, Amgen shared that its 2020 results were up 9%. Last year, the company ignited some momentum and managed to raise its earnings from the year before to $26.2 billion.

Despite these efforts, the company still struggled with organic growth. This is perhaps why it has been aggressive in pursuing multiple revenue streams via M&A to find more ways for multiple expansions.

Part of this plan is the 2021 acquisition of Five Prime Therapeutics for $1.9 billion and Teneobio for $900 million.

Given the deals last year, investors didn’t truly expect Amgen to deliver more growth in 2022. This is possibly why the company’s shareholders were a bit surprised by the new acquisition.

However, this deal with ChemoCentryx will grant Amgen access to a slew of orally administered treatments not only for autoimmune diseases and inflammatory conditions but also for cancer.

Realistically, Amgen’s near-term outlook is not that groundbreaking. However, the overall valuation and potential of its M&A dealmaking are compelling enough to encourage investors patient enough to wait for the rewards in the long run.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-09 16:00:052022-08-09 18:23:59A Revived Biotech Gaining Momentum

The moment GlaxoSmithKline (GSK) completes the spinoff of its massive segments marketing drugstore staples, such as Tums and Advil, it will become the latest name to join the list of Big Pharmas shuffling their assets and rebranding itself into a pure-play biopharma stock.

The reorganization of this UK-based company is the culmination of years-long process that has transformed practically all the biggest pharmaceutical companies globally into biotechnology companies on steroids.

This type of transformation, which gets rid of sideline businesses, has been going on for years. Pfizer (PFE) dumped its chewing-gum segment back in 2002 and established another spinoff unit, Viatris (VTRS), with Mylan in 2020.

Bristol Myers Squibb (BMY) decided to spinoff its infant-formula division in 2009. In 2018, a new animal health company came to be from Eli Lilly (LLY).

By 2023, Johnson & Johnson (JNJ) expects to complete the creation of a spinoff company and unload its consumer health segment, which offers Tylenol and Band-Aids.

Essentially, they’re turning into Amgen (AMGN) and Gilead Sciences (GILD) but with more money and resources to churn out high-priced, complex treatments for rare diseases.

However, not all Big Pharma names plan to become pure-plays. For example, Merck (MRK) still intends to retain its animal health sector while Roche (RHHBY) wants to keep its diagnostics segment.

As for the rest, including AstraZeneca (AZN), Novo Nordisk (NVO), and AbbVie (ABBV), their plan is to focus on creating new drugs and marketing these treatments—nothing more, nothing less.

The idea of Big Pharma transforming into “Big Biotech” dates back to 1992, when Henri Termeer, the CEO of Genzyme—now owned by Sanofi (SNY)—was summoned to a Senate hearing in Washington to argue and justify one of the most expensive medicines ever put to market.

The medication in question was for a rare genetic condition called Gaucher disease. A year-long treatment for one person needed tens of thousands of human placentas, and the price tag? A jaw-dropping $380,000 annually.

Amid the demand to make the treatment cheaper, Genzyme stood by its decision and the price barely budged after two years.

The company’s tenacity and insistence on standing by its pricing altered the biopharma landscape. That is, drug developers realized that rather than marketing cheaper drugs to combat common diseases, they can focus on biotech-style treatments to target rare conditions.

At that time, Big Pharma companies were battling over pieces of massive markets. They allocated considerable funds to their commercial teams, hoping to outrank one another in crowded spaces.

Meanwhile, biotechs like Genzyme decided on a different strategy.

They concentrated on more innovative approaches. Actually, the biotech focused on biologics at that point. Then, the company simply ignored the pricing rules and set its own prices, which were considerably higher.

A more recent go-to proof of concept for this strategy is Abbott Laboratories (ABT), which was initially a diversified company that offered an extensive range of products like medical devices and even infant formula.

In 2013, the company spun off its branded pharmaceutical sector into AbbVie, which became a pure-play biopharma that focused on developing and marketing the arthritis drug Humira. Since then, Humira has transformed into one of the top-selling drugs in history.

More than that, AbbVie pays substantial dividends while its shares have delivered 500% returns since the spinoff. In comparison, the S&P 500 has returned roughly 220% within the same timeframe.

While this is a shift that investors have clamored to see in the healthcare sector, it also means that the transformations could turn companies with solid revenue streams that have become reliable despite the ups and downs of the drug discovery process into riskier bets.

Although treatments for rare diseases admittedly come with very high price tags, focusing on smaller markets brings with it the inherent risk that these buy-and-stuff-under-the-mattress blue chips could no longer deliver returns as consistently.

These days, though, the advancements have made faster and safer scientific breakthroughs much more plausible.

Companies have gained a better understanding of the human genome, oncology treatments, genetic diseases, and groundbreaking modalities like gene therapies.

The science has now caught up with the demand. More importantly, Big Pharma has finally woken up and started to leverage its resources to take advantage of the opportunities.

This gradual change can be seen in the surge of new treatments in the past years. From 2016 to 2020, the FDA approved an average of 46 new therapies annually.

This is more than half the number between 2006 and 2010 when the organization only approved an average of 22 new treatments every year.

Needless to say, these changes are also partly in response to the overall dissatisfaction of investors with the diversification strategies of Big Pharma.

Basically, the general message here is that Big Pharma should let the investors worry about diversifying their own portfolios and focus on developing safe and effective drugs.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-07-14 19:00:242022-08-02 16:27:49Goodbye Big Pharma, Hello Big Biotech

Gilead Sciences (GILD) has been primarily ignored by investors who have focused more on other biotechnology and healthcare companies, particularly those that made a significant impact in the fight against COVID-19.

Reviewing the recent performance of its share price, Gilead can be best described as the ugly duckling among the Big Pharma companies in the US.

The lack of significant catalysts in the past months makes Gilead incomparable to the big movers with diversified portfolios in the space, such as Bristol Myers Squib (BMY), Johnson & Johnson (JNJ), and even Merck (MRK).

Nonetheless, I consider Gilead one of the most undervalued biopharmaceutical names in the sector.

Founded in 1987, Gilead started as a biopharma geared toward researching and developing drugs for severe and rare diseases.

Fast forward to today, it now has roughly $80.57 billion in market capitalization.

It is also widely considered the undisputed market leader for HIV treatment, with much of its revenue coming from this segment.

In its 2021 annual report, $16.3 billion of Gilead’s $27.3 billion entire revenue came from its HIV program. That’s approximately 59.7% of the total.

Globally, the market for HIV treatments reached a total of $30.46 billion in 2021.

This translates Gilead’s market share to more than 53% worldwide, with the company producing 6 of the top 10 leading products targeting the disease.

The global HIV market is expected to reflect long-term growth and is projected to reach $45.5 billion by 2028.

If Gilead sustains its market share of over 50%, it can comfortably rake in $23 billion in annual revenue from this segment alone.

While being a leader in a sustainable and stable market is definitely a good thing, Gilead has been working on diversifying its portfolio to avoid becoming too dependent on a single program.

Indicative of this plan was its efforts in 2020 when Gilead went through with 11 acquisitions and partnerships focused on oncology.

This move dramatically boosted its pipeline by 50%, with 10 drugs already queued in Phase 3 clinical trials for cancer treatments.

More importantly, this expansion to the oncology segment has also generated revenue with promising growth figures.

In fact, Gilead’s decision to focus on T-Cell therapies appears to be paying off as the company developed groundbreaking treatments with impressive efficacy rates.

In April 2022, Yescarta received the FDA's green light as the first ever CAR-T cell therapy targeting large b-cell lymphoma (LBCL).

This is an exciting update, with Gilead disclosing that 40.5% of patients who received just a single infusion of Yescarta experienced no disease progression or need for any additional cancer treatment for two years.

This is a 2.5x improvement over the current standard of care rate at 16.3%.

Yescarta’s success also serves as a promising sign for another oncology treatment, Tecartus, which targets mantle cell lymphoma (MCL).

Yescarta and Tecartus are indubitably great lucrative revenue streams in sales growth and market sizes.

The MCL market is estimated to be roughly $7 billion this year, with an annual growth rate of 7% through 2027.

In 2021, Tecartus generated $276 million in sales, accounting for 2.5% of the market share.

While that may not be an eye-popping figure, the number is actually up by 68% year-over-year, which means Gilead is slowly absorbing more and more of the MCL market share.

Notably, MCL is also quite rare, affecting only 0.5 individuals out of 100,000.

Given the figures, though, Tecartus is still well on its way to contributing more than $1 billion in sales in the following years.

Meanwhile, Yescarta offers a more promising growth story since the LBCL segment is practically 14x the size of the MCL space, as it affects 7 out of 100,000 people annually.

In 2022, the LBCL market is projected to reach $4.3 billion, with a CAGR growth rate of 15% from this year to 2030. In 2021, Yescarta raked in $695 million in sales, showing off a 41% increase year-over-year and taking over roughly 16.2% of the market share.

Given the present growth rates of both Yescarta and the LBCL market, it’s feasible for Gilead to capture at least 50% of the market by 2027.

Another notable oncology asset is Trodelvy, a metastatic triple-negative breast cancer (MTNBC) and metastatic urothelial cancer (MUC) treatment.

Like Yescarta and Tecartus, this is another potential blockbuster.

For 2022, the MTNBC market is estimated to be approximately $606 million, while the MUC market is at $1.189 billion. The growth rates for these are 4.7% and 17.9%, respectively.

In 2021, Trodelvy captured 21% of the market share with $380 million in revenue.

However, what’s more promising is that this figure indicates an 84% increase year-over-year, which shows the massive potential of Trodelvy and its ability to become a billion-dollar revenue stream in under two years quickly.

Although Gilead still has a number of therapies and drugs in the works, Tecartus, Yescarta, and Trodelvy are the frontrunners in becoming blockbusters within the next five years.

This should give the company some time to develop more treatments to boost and diversify its portfolio.

The biopharma industry is highly competitive, but Gilead appears to be healthy and attractive.

While the company continues to focus on growing its HIV segment, what makes it promising these days is expanding its oncology program, particularly its revolutionary T-Cell therapies.

Admittedly, Gilead is not as exciting as the other names on the Big Pharma list. However, its slow and steady approach to dominating massive and lucrative markets looks like an excellent winning strategy.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-26 17:30:142022-04-26 19:09:45Slow and Steady Wins the Race

As we gradually reach the pinnacle of biotechnology formation, a war is brewing in the life sciences world.

This can be one of the most exciting times for medical innovations for patients. Meanwhile, investors can be picky when picking where to put their money.

Even up-and-coming scientists can seize the opportunities to lay the groundwork for their own dream organizations.

At the same time, those aspiring to climb the corporate ladder have better chances at becoming CEO without the need to slog through the biopharma sector and scramble for whatever opening is available.

However, as more and more companies launch practically every day, claiming to offer groundbreaking and revolutionary breakthroughs, it’s critical to keep in mind that not all biotechs will succeed.

Actually, the number of biotech companies has been steadily rising since 2015.

In that year, 177 firms were formed, with biotech birth rates breaching the 200-per-annum mark by 2017 and 2018.

Seeing as many more have emerged even during the pandemic, it looks like the biotech world won’t be slowing down anytime soon.

Even funding hasn’t been deterred by economic downturns.

From 2015 to 2018, the total funding for biotech companies averaged between $68.6 million to roughly $90.2 million.

After a bustling, record-breaking 2020, the bar leading to 2021 was expectedly high.

Surprisingly, 2021 blew those figures out of the water as private investors opted to raise the bar even higher.

It’s the type of climb that’s truly hard to believe.

Biotechs raised over $22 billion in private funds in 2020 following a sluggish 2019. In 2021, that figure rose to $28.5 billion.

The top earner in these funding rounds last year was China’s Abogen, which took $1 billion in private investors’ money across two rounds.

Abogen is an mRNA-centered firm that’s currently working on a COVID-19 vaccine.

What makes its product different and possibly better than Moderna (MRNA), Pfizer (PFE), BioNTech (BNTX), and AstraZeneca (AZN) is that it would be thermostable. That is, it could be used in areas without access to refrigeration.

Another big winner in 2021 is Massachusetts-based biotech ElevateBio, which aims to be a one-stop shop for cell and gene therapies.

The idea is to develop a technology that fuses its gene-editing platform, cell engineering structure, and manufacturing warehouse into one system to ease and accelerate the drug development process.

Although not entirely the same, this plan has similarities with the strategies of Big Pharma names like AbbVie (ABBV) and Merck (MRK).

Amid the growing number of biotechs, a key challenge is how to stand out among companies that target the same disease areas. This kind of competition could hamper innovation.

The clearest indicator of success would be receiving approval and being able to launch the products commercially.

Ultimately, the goals are to offer safe and effective treatments and provide value to their shareholders.

Unfortunately, the reality is only a handful of startups do make it all the way to the top.

The more feasible scenario is that bigger businesses would acquire these companies—and that seems to be the case these days.

Alongside the booming biotech formation rate are the increasingly aggressive biotech buyout deals.

We’ve seen this before.

It started in 2019, with Bristol Myers Squibb (BMY) buying Celgene, followed by AbbVie splurging on Allergan and Takeda (TAK) merging with Shire.

In 2020, AstraZeneca bought biotech superstar Alexion Pharmaceuticals while Gilead Sciences (GILD) snapped up Immunomedics.

Meanwhile, Sanofi (SNY) stacked its deck with the $3.2 billion acquisition of Translate Bio. As for Merck, this biopharma sneaked in a massive win with an $11.5 billion buyout of Acceleron.

For this year, several names have already been eyed by Big Pharmas.

There’s Alynlam Pharmaceuticals (ALNY), an RNA-centered company, which seems to be the target of both Novartis (NVS) and Regeneron (REGN).

Another RNA-focused company, Ionis Pharmaceuticals (IONS), appears to be a key target as well, with the likes of GlaxoSmithKline (GSK), Bayer, and even Biogen (BIIB) waiting for an opportunity to pounce.

After all, acquisitions form an integral lifeline of the biotech world. Huge businesses with the resources swoop up promising buyout candidates to bolster their own pipelines.

However, M&A isn’t the only option for biotechs. There’s also the path where they can seek companies with similar focus and consolidate to become larger and more competitive entities.

This has been the expected plan for CRISPR Therapeutics (CRSP) for a long time. Hence, it is no surprise if other biotechs with their own groundbreaking technologies decide to follow the same route.

Overall, the biotech industry is booming amid its recent struggles with the market.

The faster growth rate of companies can be attributed to more investors seeing the industry's potential and, of course, better access to technology and scientific advancement.

Moreover, the world has become more interested in the biotech world and what the industry can offer due to the pandemic.

COVID-19 has shone a light on this sector following the quick and effective results of the vaccines and treatments.

That is, people have finally caught on to the idea that there is an incredible opportunity in biotech.

While a correction is to be expected at some point, the critical thing to bear in mind is that great ideas will always generate funding no matter what.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-21 18:00:072022-04-21 19:12:10Let's Get Ready to Rumble

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WATCH OUT FOR THE RECESSION WARNINGS) (TLT), (TSLA), (FB), (CRSP), (TDOC), (GILD), (EDIT), (SQ), (INDU), (NVDA), (GS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-11 12:04:332022-04-11 12:15:42April 11, 2022

The drumbeat of a coming recession is getting louder and louder.

There is no doubt that the traditional signals of a slowing economy are already flashing yellow, if not bright red.

Rocketing interest rates are the most obvious one, with ten-year US Treasury bonds yield soaring from 1.33% to 2.71% in a mere four months. This is why investors pulled a gut-punching $87 billion out of bond funds in Q1.

If the Fed continues with a quarter point rise at every meeting for the rest of the year, we might escape this cycle without a recession. If the Fed ramps up to a half point rate at every meeting as was discussed last week a recession becomes a sure thing.

Imminent positive real yields for the first time in a decade also threaten to draw money out of stocks and into bonds.

I happen to be in the non-recessionary camp and the reason is very simple. Companies are making too much damn money. This is especially true for technology companies, which account for some 75% of the profits made in the US. If anything, their profits are accelerating, although at a lower rate than seen in 2021.

Certainly, the tech companies themselves aren’t buying the recession scenario. They are hiring and investing as if the economic boom will continue forever. Tesla alone has completed two new factories in the past month, in Berlin, Germany and Austin, Texas, each capable of producing a half million vehicles a year. Tesla’s existing factories are all expanding capacity.

Sitting here in Silicon Valley, I can tell you that the job market is as hot as ever. Those who have jobs, like my own kids, are besieged with multiple job offers. It seems the standard time to keep a job these days is a year, after which one takes the next upgrade, promotion, and batch of stock options.

But the stock market seems hell-bent on discounting a recession anyway. You see this in the most economically sensitive sectors of the market, banks, semiconductors, and transport, which have just clocked a miserable month. If I am right (I’m always right), and there is no recession, these will be the sectors that lead the recovery.

Until the market makes up its mind, the disciplined among us will have to while away our time constructing lists of companies to buy for the rebound. That’s when the next leg of the bull market resumes.

We find out when this happens on Wednesday when the next batch of inflation data is released, which is likely to be diabolical.

Quantitative Tightening to Start as Soon as May, according to Fed Governor Brainard. That means our central bank will start selling its vast $9 trillion in bond holding in two months, a huge market negative. Bonds tanked. The Fed only quit quantitative easing in March.

Tesla Blows Away Q1 Sales, shipping 310,000 vehicles, far above expectations. This is despite supply chain problems, soaring interest rates, and the Ukraine War. Sky-high gasoline prices helped a lot, which is driving buyers into Tesla showrooms in drives. All other competitors are falling farther behind, unable to obtain parts and commodities which Tesla locked up long ago. This puts Tesla well on its way to its 1.5 million production goal for this year. Keep buying (TSLA) on dips. My long-term target is $10,000 a share.

The Metaverse May be Worth $13 Trillion by 2030, says Citibank. The same is so for Web 3.0, which includes virtual worlds, like gaming and applications in virtual reality. Citi’s broad vision of the metaverse includes smart manufacturing technology, virtual advertising, online events like concerts, as well as digital forms of money such as cryptocurrencies like I’ll be looking for the best plays.

Biotech May Be Staging a Comeback, after spending a year in hell, taking some shares down 80%-90%. Investors are also nibbling at the sector as a recession and bear market plays, as these companies keep growing regardless of the economic cycle. Buy (CRSP), Teledoc (TDOC), Gilead Sciences (GILD), ad Editas Medicine (EDIT) on dips.

US Bonds Just Suffered their Worst Quarter in a Half Century, with yields rocketing from 1.33% to 2.71%, and Mad Hedge was triple short most of the way down. Bear LEAPS holders, which are many of you, made fortunes. We could stall around current levels until the Fed delivered both barrels of a shot gun, two back-to-back half point rate rises from the Fed.

30-Year Fixed Rate Mortgage Rates Top 5.00%, trashing the home builders. If you thought buying a home was tough, its worst now. So far, no impact on home prices.

US Dollar Hits New Two-Year High. It’s all about rising interest rates. Expect a stronger greenback to come before the turn. The coming QT will put a two-step turbocharger on the move.

German Battery Sales Soar By 67%, to residential buyers to cope with pending energy shortages. Germany already has 2.2 million solar installations out of a population of 83 million. It’s a very smart move as batteries powered by solar panels can remove you from the grid entirely, as I have amply proven with my own installation. It may be the permanent solution to over-dependence on Russian energy supplies.

Tesla Moving into Bitcoin Mining, in partnership with Blockstream and Block, formerly Square (SQ). Tesla will supply the electric power with its massive 3.8-megawatt solar array. That is the size of a large nuclear power plant. The mining facility is designed to be a proof of concept for 100% renewable energy bitcoin mining at scale. If Elon Musk likes Bitcoin maybe you should too.

The Bank of Japan Now Owns 7% of the Japanese Stocks Market. The central bank had to buy the shares after it had already bought all the bonds in the country to support the economy. So, what happens when the policy flips from QE to QT? How about unloading $371 billion worth of shares on the market. This would e a neat trick since so much of the country’s shares are locked up in corporate cross holdings. Methinks I’ll be steering clear of Japanese stocks for the foreseeable future.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

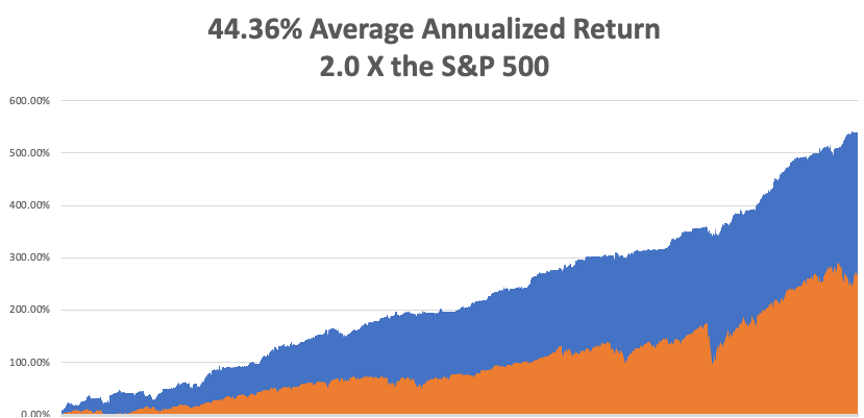

My March month-to-date performance retreated to a modest 0.38%. My 2022 year-to-date performance ended at a chest-beating 27.23%. The Dow Average is down -4.20% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 68.89%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 100% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 539.79%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.3 million, up only 100,000 in a week and deaths topping 985,000 and have only increased by 2,000 in the past week. You can find the data here.Growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 11 at 8:00 AM EST, Consumer InflationExpectations are released.

On Tuesday, April 12 at 8:30 AM, the Core Inflation Rate for March is announced.

On Wednesday, April 13 at 8:30 AM, the Producer Price Index for March is printed.

On Thursday, April 14 at 7:30 AM, the Weekly Jobless Claims are printed. We also get Retail Sales for March.

On Friday, April 8 at 8:30 AM, NY Empire State Manufacturing Index for March. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, back in 2002, I flew to Iceland to do some research on the country’s national DNA sequencing program called deCode, which analyzed the genetic material of everyone in that tiny nation of 250,000. It was the boldest project yet in the field and had already led to several breakthrough discoveries.

Let me start by telling you the downside of visiting Iceland. In the country that has produced three Miss Universes over the last 50 years, suddenly you are the ugliest guy in the country. Because guess what? The men are beautiful as well, the decedents of Vikings who became stranded here after they cut down all the forests on the island for firewood, leaving nothing with which to build long boats. I said they were beautiful, not smart.

Still, just looking is free and highly rewarding.

While I was there, I thought it would be fun to trek across Iceland from North to South in the spirit of Shackleton, Scott, and Amundsen. I went alone because after all, how many people do you know who want to trek across Iceland? Besides, it was only 150 miles or ten days to cross. A piece of cake really.

Near the trailhead, the scenery could have been a scene from Lord of the Rings, with undulating green hills, craggy rock formations, and miniature Icelandic ponies galloping in herds. It was nature in its most raw and pristine form. It was all breathtaking.

Most of the central part of Iceland is covered by a gigantic glacier over which a rough trail is marked by stakes planted in the snow every hundred meters. The problem arises when fog or blizzards set in, obscuring the next stake, making it too easy to get lost. Then you risk walking into a fumarole, a vent from the volcano under the ice always covered by boiling water. About ten people a year die this way.

My strategy in avoiding this cruel fate was very simple. Walk 50 meters. If I could see the next stake, I proceeded. If I couldn’t, I pitched my tent and waited until the storm passed.

It worked.

Every 10 kilometers stood a stone rescue hut with a propane stove for adventurers caught out in storms. I thought they were for wimps but always camped nearby for the company.

I was 100 miles into my trek, approached my hut for the night, and opened the door to say hello to my new friends.

What I saw horrified me.

Inside was an entire German Girl Scout Troop spread out in their sleeping bags all with a particularly virulent case of the flu. In the middle was a girl lying on the floor soaking wet and shivering, who had fallen into a glacier fed river. She was clearly dying of hypothermia.

I was pissed and instantly went into Marine Corp Captain mode, barking out orders left and right. Fortunately, my German was still pretty good then, so I instructed every girl to get out of their sleeping bags and pile them on top of the freezing scout. I then told them to strip the girl of her wet clothes and reclothe her with dry replacements. They could have their bags back when she got warm. The great thing about Germans is that they are really good at following orders.

Next, I turned the stove burners up high to generate some heat. Then I rifled through backpacks and cooked up what food I could find, force-fed it into the scouts and emptied my bottle of aspirin. For the adult leader, a woman in her thirties who was practically unconscious, I parted with my emergency supply of Jack Daniels.

By the next morning, the frozen girl was warm, the rest were recovering, and the leader was conscious. They thanked me profusely. I told them I was an American “Adler Scout” (Eagle Scout) and was just doing my job.

One of the girls cautiously moved forward and presented me with a small doll dressed in a traditional German Dirndl which she said was her good luck charm. Since I was her good luck, I should have it. It was the girl who was freezing the death the day before.

Some 20 years later I look back fondly on that trip and would love to do it again.

Anyone want to go to Iceland?

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Iceland 2002

https://www.madhedgefundtrader.com/wp-content/uploads/2022/04/john-thomas-in-iceland.png506776Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-11 12:02:132022-04-11 12:16:16The Market Outlook for the Week Ahead, or Watch Out for the Recession Warnings

Mad Hedge Biotech and Healthcare Letter April 7, 2022 Fiat Lux

Featured Trade:

(A BIOTECH DAVID AND GOLIATH STORY) (ALLO), (NVS), (GILD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-04-07 17:02:562022-04-07 20:35:35April 7, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.