Mad Hedge Technology Letter

January 19, 2022

Fiat Lux

Featured Trade:

(MICROSOFT TAKES A GIANT LEAP FORWARD)

(MSFT), (ATVI), (PINS), (GOOGL), (AAPL), (AMZN)

Mad Hedge Technology Letter

January 19, 2022

Fiat Lux

Featured Trade:

(MICROSOFT TAKES A GIANT LEAP FORWARD)

(MSFT), (ATVI), (PINS), (GOOGL), (AAPL), (AMZN)

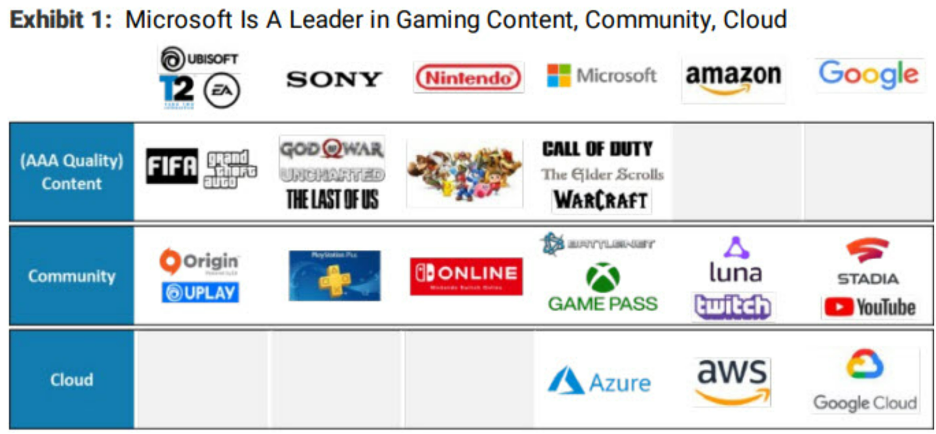

CEO of Microsoft (MSFT), Satya Nadella, and his management team have made an aggressive step towards making inroads to the metaverse.

Gaming will be the launching pad to the metaverse that will first start as digital communities and later evolve into interoperable and integrated digital worlds.

The rest of the metaverse will germinate via these gaming communities and Microsoft knows that which is why they purchased Activision (ATVI) in cash for $68 billion and change.

The price was 3X higher than what they paid for LinkedIn but equally as strategic as many tech behemoths look forward to the next “big thing.”

The deal will mean MSFT will be one of the biggest gaming companies in the world just nudging out China’s Tencent and Japan’s Sony.

In the U.S., they will be by far the biggest gaming company and Nadella has made it a point of emphasis to navigate the gaming world by tapping M&A.

Remember, it was Nadella who built the MSFT cloud from scratch and Microsoft possessing its own stand-alone cloud asset dovetails nicely with their deep dive into gaming.

There are intrinsic synergies resulting from owning both.

The lack of native cloud infrastructure was a critical reason why ATVI gave up, as Chief Executive Officer Bobby Kotick said in an interview, “You look at companies like Facebook and Google and Amazon and Apple, and especially companies like Tencent — they're enormous and we realized that we needed a partner in order to be able to realize the dreams and aspirations we have,” he said.

This was the best Kotick could have wished for and I’ve mentioned this overarching trend of the best Silicon Valley companies getting stronger and now it’s even more pronounced as we are on the verge of exiting this pandemic this year.

In a higher interest rate environment, cash hoarders like Microsoft, Apple (AAPL), and Amazon (AMZN) simply have more ammunition than these smaller outfits who get penalized because of a harder route to access cheap capital making future cash flows costlier.

Now many of these smaller companies are realizing that they need to stand on their own two feet and that’s a scary thought for many CEOs who have been accustomed to tapping the capital markets to paper over the cracks.

What’s good about ATVI?

Activision owns mobile-gaming studio King, maker of Candy Crush, one of the most popular mobile games of all time.

Microsoft has almost zero presence in mobile gaming.

Nadella wants his gaming empire to facilitate direct payment like Apple’s App Store.

That’s effectively the holy grail of today’s gaming.

Microsoft has been at war with Apple and Google, over the fees the app stores charge for games.

It’s no surprise that Microsoft wants complete control over its ability to distribute games and content.

The deal also allows Microsoft an access point to secure an influential pool of gamers creating their own gaming content and worlds.

After adding Minecraft, LinkedIn, and GitHub, Nadella has been on the hunt for a game-changing asset that will drive the bottom line of MSFT via a large community of creators.

He failed to land social video service TikTok, while negotiations with Pinterest (PINS) and Discord were rebuffed.

ATVI is really a feather in the cap for Nadella, who won’t stop there and knows it’s just one battle of a greater war for tech supremacy.

These high-quality assets don’t get cheaper over time either.

Simply put, Microsoft loves subscription businesses, and gaming is among the best of them, and they are the stickiest around with recurring revenue that makes predicting future cash flows that much easier.

The ATVI pickup will raise the price of buying gaming assets across the board as I foresee a rush into these types of assets where not only can a company purchase the content, licenses, and gaming platform, but they can also add top-notch gaming developers which are equally as important as Microsoft tries to outmuscle Apple and Google.

This move is highly bullish for MSFT, so much so, that anti-trust regulators might cast a suspicious eye on this deal.

Mad Hedge Technology Letter

January 14, 2022

Fiat Lux

Featured Trade:

(AVOID ARKK INNOVATION FUND LIKE THE PLAGUE)

(ARKK), (GOOGL), (TDOC), (ZM)

I was a little taken aback by the content and attitude of boutique investment fund CEO and CIO of Ark Invest Cathie Woods as I watched her podcast -- set in a palatial estate with vaulted ceilings.

The line that stuck out to me was when she began to explain that the ARK Innovation ETF (ARKK) is made up of “real companies with real revenue.”

Well, so is the liquor store down the street and that doesn’t mean we should all bandy together with each other, sing kumbaya and bet the ranch on this ETF fund that dabbles in ultra-high growth tech stocks.

She continued to praise her strategy by comparing ARKKs relative success with the dot com crash where companies were based on thin air and accrued massive valuations for nothing.

That’s a bad comparison because it was a different era and time, and just because that market then was frothy, it has nothing to do with a higher ARKK stock price in the short term.

She then explains to us viewers that she has never been so convinced by companies like Teledoc (TDOC) and this is a company that has experienced about a 400% drop in share price in the past 365 days.

The reason she gives support for TDOC is because they do $2 billion in annual revenue and then she followed that up by saying how great Zoom Video (ZM) is because their revenue has gone up “4-fold during the coronavirus” but fails to mention that their stock is down about 400% since October 2020.

She laments that these stocks have recently been treated as “stay at home” stocks and I believe that giving such an excuse to why these stocks have been performing poorly lately makes her look like she doesn’t know what she is doing.

If she champions TDOC for doing $2 billion in annual revenue, then why not invest in Alphabet (GOOGL) which does $180 billion of revenue per year. According to her math, GOOGL is a 90X better investment than TDOC.

In her video interview, she starts to explain the inflationary monster which of course, she has an incentive to downplay. Low rates mean a better environment for growth stocks to operate in.

She continues to explain that used car prices are up 60% but that “bubble has burst” because sales are down 4 recently.

Again, she is grasping for straws here because she has an incentive to.

Another data point she tries to spin off as anti-inflationary is the increase in average wages and explains that a 0.6% increase is the “lower end of the guidance” so that certainly will trend down.

Again, nominal wages have exploded in all industries, and this is again proof she likes to reverse engineer stats to fit her own interests.

During this interview or fireside chat, Woods appears to be an expert at cherry-picking data points that are in her best interest.

She fails to acknowledge that her timing of equity purchases is just as important as the type of stocks bought, and her recent timing has been terrible.

Her response to the underperformance was to blame the market and pontificate that the “dismissal (of her ARKK fund ETF) is misplaced” and “analysts and investors aren’t doing their homework.”

Her attempt to shift blame on the market is comical and the real traders in the room know that the market decides the prices of assets and not anyone or any organization can dictate the market to the market.

Showing a little humility might do her a little good as Ark Innovation ETF suffered an outflow of $352 million Wednesday, the biggest one-day drop since March.

She explains the Fed policy towards higher rates as just “jawboning” and begins to explain how she is seeing some anti-inflationary data coming down the pipeline imminently.

I will tell Woods that this “jawboning” isn’t just that, it’s real. The Fed is poised to react to combat inflation and not raising interest rates as fast as she thought doesn’t mean the narrative immediately evolves into something even close to anti-inflationary.

We are so far from that sentiment and her reaction is to dismiss anything that is a threat to her fund.

Sadly enough, she wants things how it was in 2020, massive amounts of quantitative easing for that capital to flow into her ARKK fund.

I am not saying that won’t ever happen again, but the zeitgeist must overcome the higher rates narrative that has completely consumed the broader market which is why tech growth has been hammered lately.

Her failure to act has meant her investors are down 50% in the last 13 months. Buying at tops are dangerous and even more important, she doesn’t describe the current market and describes only what she wants to happen in the future as it relates to higher ARKK prices.

I wouldn’t call that breaching her fiduciary responsibilities, but she is playing a snake oil saleswoman at her finest.

This could be a case of her thinking that she is playing with houses’ money, a longer time frame shows that ARKK is still up more than 300% since 2017.

If you ever feel like getting into high tech growth, avoid this fund, just buy the stocks you like outright.

This is an example of how ETFs will not work in today’s climate, as ETFs only function properly if they go up every year.

The markets could spend the first third of the year grappling with higher rates, and there will be another time to buy tech growth. For Woods to completely ignore her failure of timing the tech growth market, it shows she isn’t looking out for your best interest as an investor.

Avoid tech growth today until we get through the short-term challenges.

Mad Hedge Technology Letter

January 12, 2022

Fiat Lux

Featured Trade:

(JUMP OFF THE ROKU BANDWAGON)

(ROKU), (GOOGL), (AMZN)

Many “experts” have been advising investors to buy the dip in Roku (ROKU) since it dropped to $370 from the peak of $480 it reached in July 2020.

These experts kept banging the drum to buy the dip on Roku as it slid to $350 then $320.

The calls for dip-buying continue as Roku nosedived to $280 then most recently on a downgrade, Roku fell all the way to $177.

Painful as it feels to be an investor in Roku, this is not the time to double down on high-tech growth stocks.

Growth tends to usually overshoot to the upside as investors give a pass to growth for losing money and selectively put a premium on high growth rates.

But that deal is only valid in a low-interest rate environment and what we are witnessing is the reverse happen as investors are bolting from Roku like stallions out the back of a stable.

At a micro level, there is somewhat distaste at the ever-increasing competition Roku is facing and the lack of growth prospects overseas.

Overseas is usually the growth engine for many of these streaming cohorts, but the dilemma here is that margins are lower because of a poor purchasing power profiles for the median consumer overseas.

That’s not to say it’s easy to succeed in the U.S. — hardly so.

However, Roku’s business in the United States has been highly successful, but the issue here is that the market is getting somewhat saturated and since the stock market is priced based on future cash flow, where does the incremental buying come from to save Roku’s stock?

Roku faces a perilous uphill challenge to convince the incremental platform user to install its Roku stick at a time when Amazon (AMZN) and Google (GOOGL) are using their greater clout and sharper elbows to get rid of the tech peons.

Amazon reported sales of over 150 million Fire TV devices recently. Roku has over 56 million active accounts, although it’s not a direct comparison because Amazon’s figure counts sold devices and includes Fire TV devices that are not being used.

There is no possible way that Roku can secure 50% of the market here and 40% would be a stretch capping its ceiling.

Another leery signal came when smart television maker TCL who have partnered to make the Roku smart TV decided to jump ship to Google.

This could represent a red flag as these bigger companies have the capacity to poach talent, know-how, and convince suppliers to jump ship with a more lucrative contract for a larger install base.

This could be the first point of contact that could eventually lead to Google buying out TCL and cutting off Roku from a source of a hardware supplier.

TCL has now claimed to be one of the biggest sellers of sets featuring Google’s connected TV operating system and the partnership will take precedence over anything Roku is involved with.

In the short term, readers need to stay away from Roku as we need more commentary on how it plans to shake off Google and Amazon and how it plans to navigate a perceived saturation in its domestic business while underperforming overseas.

Granted, it’s intimidating to go up against Google and Amazon because there are less tools available in the tool kit in terms of stacking resources and convincing consumers that they are indeed a higher quality product.

Long term, I don’t see it for Roku.

Short term, it’s dicey at best.

This stock promises to be volatile in the next three months and actively trading this stock will probably mean selling sharp rallies and avoiding dips.

The first-mover advantage was stellar for a while and Roku rode that donkey up the mountain of success, but now as reality sets in and the first-mover advantage dissipates, they need a miracle or should just negotiate to sell itself while the stock price is still near $200.

It’s sink-or-swim at this point.

Mad Hedge Technology Letter

December 20, 2021

Fiat Lux

Featured Trade:

(GETTING AHEAD WITH THE CLOUD)

(AMZN), (ZS), (CRM), (GOOGL)

Dealing with the Cloud works and for every relevant tech company, this division serves as the pipeline to the CEO position.

If this isn’t the case for a tech company, then there’s something egregiously wrong with them!

Take Andy Jassy, the mastermind behind Amazon’s (AMZN) lucrative cloud computing division and is the man who succeeded company founder Jeff Bezos.

He’s been rewarded this important position based on his performance in the cloud and faces a daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon almost 30 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Cloud 101

If you've been living under a rock the past few years, the cloud phenomenon hasn't yet passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them work remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the recent ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there, your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

The cloud is where you want to be.

Mad Hedge Technology Letter

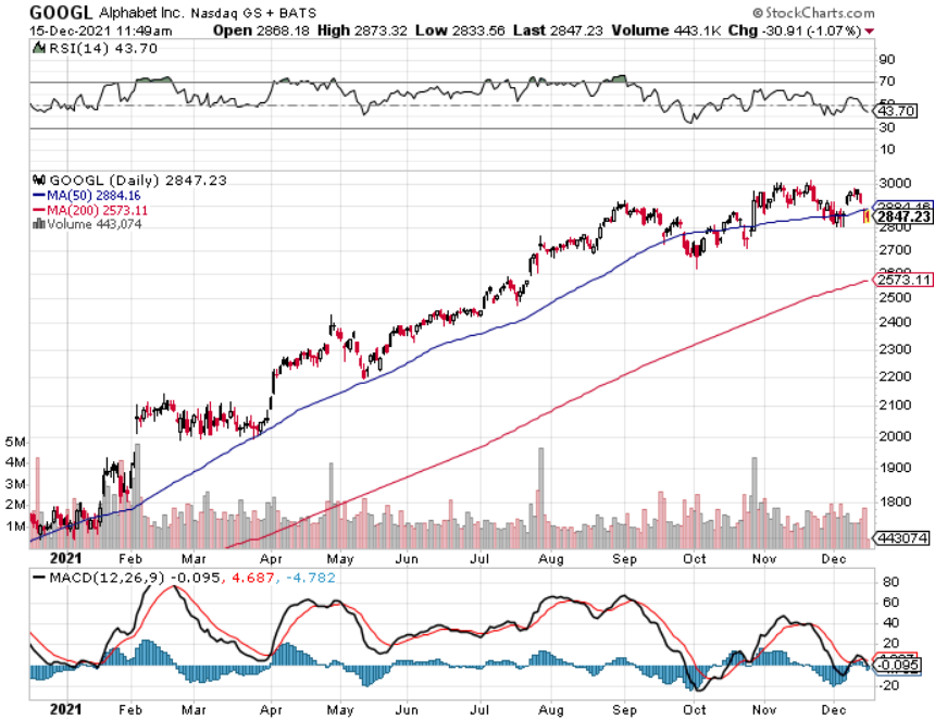

December 15, 2021

Fiat Lux

Featured Trade:

(BUY THE DIP IS BEING CHALLENGED)

(PTON), (ROKU), (TSLA), (GOOGL), (FB), (DOCU), (TDOC)

Ominous signals have started to emerge in the short-term patterns of tech stocks over the past few weeks.

We have essentially traded a Santa Claus rally to sell the spiked peaks as inflation numbers have come in way too hot for anyone to handle.

The poor inflation numbers have triggered a cascade of algorithmic selling.

Why is this important?

These stock patterns will offer us clues to how tech stocks will react in a quickly changing backdrop where the Fed is backing away from the cheap money cauldron as fast as it can.

For over ten years now, as tech stocks have bulldozed their way to higher highs and as Apple inches closer to $2.9 trillion in market cap and on its way to $3 trillion, investors have been systematically conditioned to buy the dip.

The Fed is doing its best to recreate a new type of conditioning where the dip is not bought and that is awful for tech stock prognosticators.

This effectively means a large layer of buyers on down days will be stripped away from the tech markets.

Any idiot would understand this means that tech stocks will not go as high as they could if dip buying is conditioned.

The tech market is trying to figure out the new rules of the game and that is resulting in choppy patterns almost in whipsawing fashion.

March 2022 is the new consensus for an interest rate rise which is bad news for tech stocks because pulling forward interest rate rises coincides with higher volatility in the short term.

The Fed could make another interest rate move in the second half of 2022.

This means that anyone dallying in the speculative area of the tech market needs to pull the reigns in immediately.

Stocks like Peloton (PTON), essentially a stationary bike with a tablet pasted on the dashboard, will historically underperform in the new environment.

Another tech stock I love to bully is Pinterest (PINS), by far the worst social media platform I have ever seen, will need to face reality without the Fed punchbowl that was most likely their biggest tailwind.

Tech stocks must now stand on their two feet and that’s scary news for all tech stocks not named Tesla, Facebook, Apple, Amazon, Microsoft, and Google.

After these top 5, the quality dwindles fast and expect a slew of rapid downgrades that will throttle the non-elite software stocks.

Adobe’s stock had its second-worst day of the year on Tuesday, as analysts jumped on the higher rates bandwagon and cited high valuations.

Valuations are now “high” even if these business models are the same as they were a few days ago.

Expect poor guidance from management with earnings growth, free cash flow, and annual revenue downgrades in the pipeline.

Other notable sell-offs this week include shares of cybersecurity companies Zscaler and Cloudflare, which crumbled 7.8% and 9%, respectively.

Zscaler had been up 55% for the year, prior to Tuesday, and has an enterprise value to revenue multiple for 2022 of 39. Cloudflare was up 91% and trades at a multiple of 61.

Tech growth works both ways in which they get the benefit of the doubt in a low-rate environment and vice versa in a tightening environment.

Case in point is a company I really like Roku (ROKU) whose shares are down a hideous 230% since mid-July.

The weakness in the secondary names has been biggest secret untold in tech for quite a while and the confirmation of a tough 2022 was what happened in the first two weeks of December.

And it gets worse when looking at the shelter-at-home darlings of 2020 Teledoc (TDOC) and DocuSign (DOCU) who have been totally neglected this year.

This goes to show that every year is different and as the stock market is levered to the skies, the slightest nudge by the Fed does a lot to wobble the trajectory of tech.

Luckily, tech still has the 6 big tech stocks to rally around and even if the best of the rest must go into hibernation in 2022, we still got guys like Mark Zuckerberg, Tim Cook, Elon Musk powering us through the sludge.