Mad Hedge Technology Letter

February 8, 2021

Fiat Lux

Featured Trade:

(VENTURE CAPITALISTS SHARE THE CLUES TO THE TECH MARKET)

(NVDA), (OTCMKTS: SFTBY), (GOOGL), (BABA), (AMZN), (UBER), (FB)

Mad Hedge Technology Letter

February 8, 2021

Fiat Lux

Featured Trade:

(VENTURE CAPITALISTS SHARE THE CLUES TO THE TECH MARKET)

(NVDA), (OTCMKTS: SFTBY), (GOOGL), (BABA), (AMZN), (UBER), (FB)

To gain a glimpse into the current psyche of tech investing, we need to take a raw snapshot of the state of Softbank’s Vision Fund.

The Vision Fund is the brainchild of the Japanese telecom company’s founder Softbank Masayoshi Son and is the world’s largest technology-centric venture capital fund with over $100 billion in capital.

The torrent of bullish price action of late has meant that SoftBank recorded a record quarterly profit in its Vision Fund as a gangbusters’ stock market lifted the value of its portfolio companies.

However, the significant gains accrued in equity were also substantially offset by painful derivatives losses as Son attempted to parlay his winnings into leverage directional bets in the short-term.

The Vision Fund’s $8 billion profit in the December quarter is a stark change from the prior March when the pandemic was in full gear and the Fund booked major losses amid embarrassing flops like office space sharing company WeWork.

As 2020 came to a close, tech growth firms like Uber (UBER) stock exploded higher and DoorDash (DASH) gave the Vision Fund a nice payday going public at the end of the year in stellar fashion.

On the options trading front, things didn’t go so rosy.

SoftBank posted a 285.3 billion yen or $2.7 billion derivatives loss in the period.

I understand “hedging your bets” but for Son to create this massive loss undeniably has to infuriate deep-pocketed investors from Arab nations that have stuck with him through tumultuous events.

The staggering option losses was why the asset management arm registered a loss of 113.5 billion yen or $1.08 billion, up from losses of 85.2 billion yen in the previous three-month period.

Experiencing wonderful gains only to have the narrative wiped out because of high stakes option bets is perhaps a sign of the times as phenomena like the Gamestop (GME) have moved to the forefront indicating that players have access to too much liquidity at this point in the market cycle.

Some 15 companies have gone public from the Vision Fund so far, and Son does have a long list of busts and winners.

However, one might assume that he won’t hit on every company as he revealed that his Vision Fund 1 and Vision Fund 2 have invested in a total of 131 companies. In the case of DoorDash, SoftBank invested about $680 million for a stake now worth about $9 billion while its $7.7 billion investment in Uber is worth $11.3 billion.

There are still shining stars on the balance sheet.

Another six more portfolio companies are planning IPOs this year and bringing this volume model to the public markets is logical considering even zombie companies are getting funded out the wazoo at this point.

Tech is also still holding its perch as the darling of the market and Son is simply delivering to market what investors want which is growth tech and more of it.

Other issues on Softbank’s list are to sell off its interests in Alibaba, T-Mobile US Inc., and SoftBank Corp., the Japan telecommunications unit. SoftBank also announced a deal to sell its chip designer Arm to Nvidia (NVDA) for $40 billion.

On top of the risky growth companies, Softbank has also parked its capital in a who’s who of tech firms such as a $7.39 billion investment in Amazon.com (AMZN), $3.28 billion in Facebook (FB). and $1.38 billion in Alphabet or Google (GOOGL). The operation is managed by its asset management subsidiary SB Northstar, where Son personally holds a 33% stake.

Son labeled his options debacle as a “test-drive stage” hoping to play down the fact that he should have made a lot more with the massive ramp-up in tech demand in 2020.

It’s not all smooth for Son with the chaos at Alibaba (BABA), Son’s most exotic investment success to date and SoftBank’s largest asset, tanked 20% last quarter amid a Chinese government clampdown on Alibaba Founder Jack Ma.

This has to worry Son’s future tech investing prospects in China (P.R.C.).

SoftBank’s own sale of Arm to Nvidia (NVDA) is still making the rounds through the EU approval process. The United Kingdom and European Union are both preparing to launch probes into the deal.

All in all, a mixed bag for the Vision Fund where profits should have been higher and most of the damage was self-inflicted.

At some point, throwing massive amounts of capital to juice up tech growth firms will backfire, but the generous access to liquidity that Son has makes this strategy work while even affording him some massive failures.

In short, the Vision Fund should be many times more profitable and it’s a reminder that these leveraged bets aren’t going away which should mean enough liquidity out there to take the markets higher.

We should also be aware that the eventual “market mistake” could give us 10% tech corrections, which are no brainer buying opportunities if the same liquidity volume persists.

Then consider that many tech companies have done well in the recent earnings season and combine that with the eventual reestablishment of buybacks and the neutral observer must think that tech has more room to run in 2021.

Global Market Comments

February 2, 2021

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO),

(PFE), (BMY), (AMGN), (CELG), (CRSP), (FB), (PYPL), (GOOGL), (AAPL), (AMZN), (SQ), (JPM), (BAC), (MS), (GS), (BABA), (EEM), (FXA), (FCX), (GLD), (SLV), (TLT)

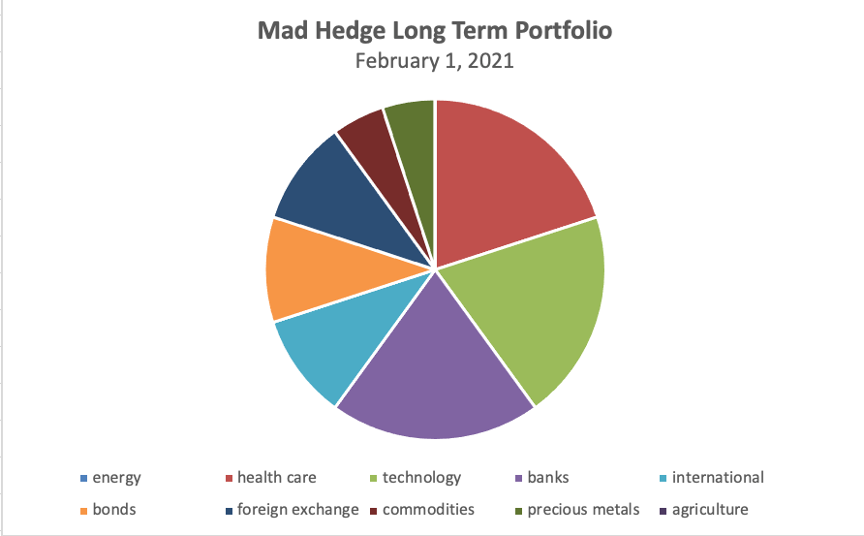

I am really happy with the performance of the Mad Hedge Long Term Portfolio since the last update on July 21, 2020. In fact, not only did we nail the best sectors to go heavily overweight, we also completely dodged the bullets in the worst-performing ones.

For new subscribers, the Mad Hedge Long Term Portfolio is a “buy and forget” portfolio of stocks and ETFs. If trading is not your thing, these are the investments you can make, and then not touch until you start drawing down your retirement funds at age 72.

For some of you, that is not for another 50 years. For others, it was yesterday.

There is only one thing you need to do now and that is to rebalance. Buy or sell what you need to reweight every position to its appropriate 5% or 10% weighting. Rebalancing is one of the only free lunches out there and always adds performance over time. You should follow the rules assiduously.

Despite the seismic changes that have taken place in the global economy over the past nine months, I only need to make minor changes to the portfolio, which I have highlighted below.

To download the entire new portfolio in an excel spreadsheet, please go to www.madhedgefundtrader.com, log in, go “My Account”, then “Global Trading Dispatch”, then click on the “Long Term Portfolio” button.

Changes

I am cutting back my weighting in biotech from 25% to 20% because Celgene (CELG) was taken over by Bristol Myers (BMY) at a 110% profit compared to our original cost. We also earned a spectacular 145% gain on Crisper Therapeutics (CRSP). I’m keeping it because I believe it has more to run.

My 30% weighting in technology also gets pared back to 20% because virtually all of my names have doubled or more. These have been in a sideways correction for the past six months but are still an important part of any barbell portfolio. So, take out Facebook (FB) and PayPal (PYPL) and keep the rest.

I am increasing my weighting in banks from 10% to 20%. Interest rates are finally starting to rise, setting up a perfect storm in favor of bank earnings. Loan default rates are falling. Banks are overcapitalized, thanks to Dodd-Frank. And because of the trillions in government stimulus loans they are disbursing, they are now the most subsidized sector of the economy. So, add in Morgan Stanley (MS) and Goldman Sachs (GS), which will profit enormously from a continuing bull market in stocks.

Along the same vein, I am committing 10% of my portfolio to a short position in the United States Treasury Bond Fund (TLT) as I think bonds are about to go to hell in a handbasket. I rant on this sector on an almost daily basis, so go read Global Trading Dispatch.

I am keeping my 10% international exposure in Chinese Internet giant Alibaba (BABA) and the iShares MSCI Emerging Market ETF (EEM). The Biden administration will most likely dial back the recent vociferous anti-Chinese stance, setting these names on fire.

I am also keeping my foreign currency exposure unchanged, maintaining a double long in the Australian dollar (FXA). The Aussie has been the best performing currency against the US dollar and that should continue.

Australia will be a leveraged beneficiary of the synchronized global economic recovery, both through strong commodity prices and gold which has already started to rise, and the post-pandemic return of Chinese tourism and investment. I argue that the Aussie will eventually make it to parity with the US dollar, or 1:1.

As for precious metals, I’m baling on my 10% holding in gold (GLD), which delivered a nice 20% gain in 2020. From here, it is having trouble keeping up with other alternative assets, like Bitcoin, and there are better fish to fry.

Yes, in this liquidity-driven global bull market, a 20% return is just not enough to keep my interest. Instead, I add a 5% weighting in the higher beta and more volatile iShares Silver Trust (SLV), which has far wider industrial uses in solar panels and electric vehicles.

As for energy, I will keep my weighting at zero. Never confuse “gone down a lot” with “cheap”. I think the bankruptcies have only just started and will stretch on for a decade. Thanks to hyper-accelerating technology, the adoption of electric cars, and less movement overall in the new economy, energy is about to become free. You are looking at the next buggy whip industry.

My ten-year assumption for the US and the global economy remains the same. I’m looking at 3%-5% a year growth for the next decade.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient, productive, and profitable than the old.

You won’t believe what’s coming your way!

I hope you find this useful and I’ll be sending out another update in six months so you can rebalance once again.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

January 20, 2021

Fiat Lux

Featured Trade:

(THE CONTRARIAN PLAY)

(ADT), (GOOGL)

How about a tech contrarian play focused on one of the more primitive areas of technology?

And did I say it’s cheap?

Among the discounted tech equities out there is security specialist, ADT (ADT), that is increasingly using technology as solutions for its customers.

This time, I am talking about normal folks just wanting to live their lives, the collective desires certainly trend towards investors buying security home solutions ADT stock that use technology to protect your home.

Yes, this isn’t a sexy tech stock, but not all are.

And contrary to initial thought, crime has gone down nationally during the pandemic because more people working from home meant less opportunity for trouble to come about the home.

The US set records for decreases in residential burglaries last year, but we all know that it will be different when the freedom of autonomy picks up and we are out of our houses on Friday and Saturday night.

Even in the Great Recession of 2008, crime increased presumably to financial desperation and need.

This sets the stage for ADT to experience more buying as we press into 2021.

What is the bull case as we dig into the weeds?

The ability to get on-premise security solutions today is markedly better than what it was a year ago or the ability three or four months ago.

The strength in execution resulted in ADT finishing Q3 with strong backlogs, the highest of the year.

They had solid sales in install in October as well.

So it's broadly diversified, much of it tied with getting access to the premises.

I’m optimistic about the commercial business with total revenue up sequentially in Q3.

The business includes a largely recurring revenue base of 35%.

It's buoyant and durable, highly diversified stuff. ADT is just shy of 250,000 customers in the commercial business.

There is upside in new and growing verticals, healthcare, education, government, critical infrastructure.

ADT also boasts the best service in the space, and that's the most critical source of differentiation.

Even though the total reported revenue in the quarter was essentially flat year-over-year, 2021 should translate into a “growth” year.

Installation and other revenue increased by $46 million, driven mainly by higher reported residential outright sales revenue resulting from the Defenders acquisition.

This increase was partially offset by lower installation revenue to commercial customers resulting from pandemic-induced economic challenges.

Monitoring and services revenue was up slightly year-over-year.

ADT generated $127 million of adjusted free cash flow during the third quarter. And through the first nine months of 2020, their adjusted free cash flow of $532 million is up more than 15% from the $459 million during the same period in 2019.

The strong year-to-date cash performance comes from a myriad of factors that more than offset the higher cash interest, including subscriber acquisition cost efficiency and the benefits from some favorable cost base trends in the current operating environment, along with some timing items.

First, the new direction with Alarm.com includes the launch of a first-generation ADT + Google offering developed through the commitment by Alarm.com that will result in several tailwinds.

First, it leverages the foundation and extends Command and Control until the end of 2022, and then beyond that, allows that platform to support end customers for the long haul.

I believe customers with integrated Google Nest product and services will perform well on an attrition basis because the product will be one of the superior ones.

The second benefit, integrated Google Nest services and Google Video services will be available and accelerate go-to-market with a co-branded offering in the second half of 2021 instead of mid-'22.

At a high level, ADT will capture efficiencies as a result while navigating a unique product road map to create differentiation.

Leveraging Google's prowess in machine learning and Artificial intelligence to fuel what Google calls ambient computing is the next-gen of home security solutions.

In computing, ambient intelligence (AmI) refers to electronic environments that are sensitive and responsive to the presence of people. Ambient intelligence was a projection on the future of consumer electronics, telecommunications, and computing that was originally developed in the late 1990s by Eli Zelkha and his team at Palo Alto Ventures for the time frame 2010–2020.

And if you can imagine for a moment, in today's world, to leverage this machine learning supported system in different ways with rules and automation, this will only increase the prestige and revenue drivers of ADT’s brand.

Another positive data point was the attrition rate, a record low 12.9% that was widespread across geographies, all categories, across all business areas. SMB was flat but residential and core commercial improved.

As 2021 plays out, I believe a combination of positive macroeconomic and macro-environmental factors will stick with ADT helping to continue to drive improvements in the business through the uncertainty of the end of the health crisis and beyond.

Although I wouldn’t put my life savings into ADT, it is worth a flier at $9 today.

Mad Hedge Technology Letter

January 8, 2021

Fiat Lux

Featured Trade:

(UNSTOPPABLE FACEBOOK)

(AMZN), (FB), (APPL), (MSFT), (GOOGL)

Salacious TikTok ads portraying perceived underaged girls shown to middle-aged men?

Yes, you guessed Facebook’s algorithm correctly.

But it doesn’t matter.

No matter what you throw at Facebook and Big Tech, they will get away with it.

The ability to hone narratives and control our communication channels means they can reroute anything remotely resembling a con and spin it into a pro.

As Facebook has encouraged misinformation to spread, including from US President Donald Trump, they come in when you least expect it to play both sides as they announced they will ban the President from Facebook.

An unruly mob of President Donald Trump's supporters stormed the Capitol to disrupt the election certification process and Facebook has finally banned the US President’s account.

Four people died — one was shot by police, and three died during medical emergencies.

Jake Angeli, a well-known QAnon influencer dubbed the "Q Shaman," seemed to be giving out orders in the Capitol sporting a Viking-like horned fur helmet and shirtless chest.

Google CEO Sundar Pichai called it the "antithesis of democracy" in an internal memo and Facebook removed a video of Trump spreading baseless claims of election fraud. The platform then blocked Trump from posting content for 24 hours.

Ironically enough, Facebook blocked employees from commenting on posts on its internal messaging boards discussing the ban showing how little employees can do in national crises.

Facebook employees also lashed out at Facebook’s lack of speed and aggressiveness in dealing with the situation.

I spoke to several employees at Facebook and they admit in unison that Facebook is an absolutely terrible place to work and executive intimidation is something workers must put up with because it is precisely the working culture in place when they walk in the door.

Even former Facebook security chief Alex Stamos chimed in saying Trump needed to be blackballed from Facebook and Twitter.

Zuckerberg did later send out a note that said, “peaceful transition of power is critical to the functioning of democracy, and we need our political leaders to lead by example and put the nation first.”

Zuckerberg doesn’t really need to say much but stay politically correct because he does most of his speaking with the action and non-action at the helm of the ship.

If you dig deeper, his flatform is utterly disgusting, and investors shouldn’t be surprised by the handling of this event.

Facebook’s handling of TikTok’s ads is one of many examples of its advertising system gone bonkers, and the company's ongoing prioritization of revenue over the safety of its 3 billion users, the public good, and the integrity of its own platform.

Middle-aged men using Facebook are fed a voracious stream of TikTok ads displaying skimpy teenage girls and even if they contact Facebook to stop it, Facebook won’t change a thing.

Besides the subliminal advertising in areas that could lead to predatory behavior, consumers are sold goods they never receive or are lured into financial scams; legitimate advertisers’ accounts or pages are hacked and used to peddle those nonexistent goods or scams; credit card numbers are stolen.

The one constant here is that Facebook doesn’t refund any of this malicious behavior and in fact, encourages it.

Facebook agreed to an implicit pact with scammers, hackers, and disinformation peddlers who use its platforms to rip off and manipulate people around the world.

Prioritizing revenue over the enforcement of policies is beginning to be the legacy of Big Tech.

The Facebook “moderators” are a small army of low-paid, unempowered contractors to manage a daily onslaught of ad moderation and policy enforcement decisions that often have far-reaching consequences for its users.

They are much more worried about losing their $15 per hour job than challenging the powerful overlords at Facebook.

And that’s not the beginning of it; Facebook's ad workers have at times been told to ignore suspicious behavior unless it “would result in financial losses for Facebook.”

Non-enforcement helped Facebook become the preferred platform of unscrupulous affiliate marketers and drop shippers that target people with financial scams, trick them into expensive subscriptions, or use false claims and trademark infringement.

Bought products often never arrive.

Facebook’s “best” practices constitute of looking the other way, even if an account is hacked, and only caring about business if credit chargebacks are threatened.

I have also been told by former Facebook employees that they are instructed to be “more lenient with accounts originating in Russia, Ukraine, and China.”

This episode truly shows why investors should still buy big tech.

They are unstoppable to such an extreme that most people can’t comprehend. Rules don’t apply to them.

And it’s not just Facebook, there are mounting headaches for all these CEOs that won’t affect the bottom line and in fact, offer these corporations a great chance to cut costs.

On January 4th, 2021, Google workers and contractors announced they were forming a union with the Communications Workers of America.

It’s the latest move in an ongoing fight between Google workers and management, and it could trigger a giant offshoring to cheap labor countries.

If most of America’s supply chain was offshored and never came back, then why can’t tech do it as well?

Why do they need to pay $150,000 to an employee in California when they can hire the same level of talent in Moldova for 20% of the cost?

That proves my point because whatever hurdles are set in front of big tech, they know how to maneuver around and avoid any deep carnage.

If investors know there will always be fix out there, even with the egregious behavior at Facebook, they won’t hesitate to pile into Big Tech.

Washington riots simply don’t matter, and markets took wind of it.

I am bullish the Big 5 of Apple, Facebook, Microsoft, Amazon, and Google.

Mad Hedge Technology Letter

January 6, 2021

Fiat Lux

Featured Trade:

(THE INSATIABLE GROWTH OF THE MOBILE BASE STATION MARKET)

(MRVL), (NOK), (KRX: 005930)

Mad Hedge Technology Letter

January 4, 2021

Fiat Lux

Featured Trade:

(SPLINTERNET GOES FROM BAD TO WORSE IN 2021)

(AMZN), (APPL), (TIKTOK), (TWTR), (MSFT), (GOOGL), (FB)