Global Market Comments

January 17, 2025

Fiat Lux

Featured Trades:

(JANUARY 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(GS), (MS), (JPM), (C), (BAC), (TSLA), (HOOD), (COIN), (NVDA), (MUB), (TLT), (JPM), (HD), (LOW), FXI)

Global Market Comments

January 17, 2025

Fiat Lux

Featured Trades:

(JANUARY 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(GS), (MS), (JPM), (C), (BAC), (TSLA), (HOOD), (COIN), (NVDA), (MUB), (TLT), (JPM), (HD), (LOW), FXI)

Below please find subscribers’ Q&A for the January 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Sarasota, Florida.

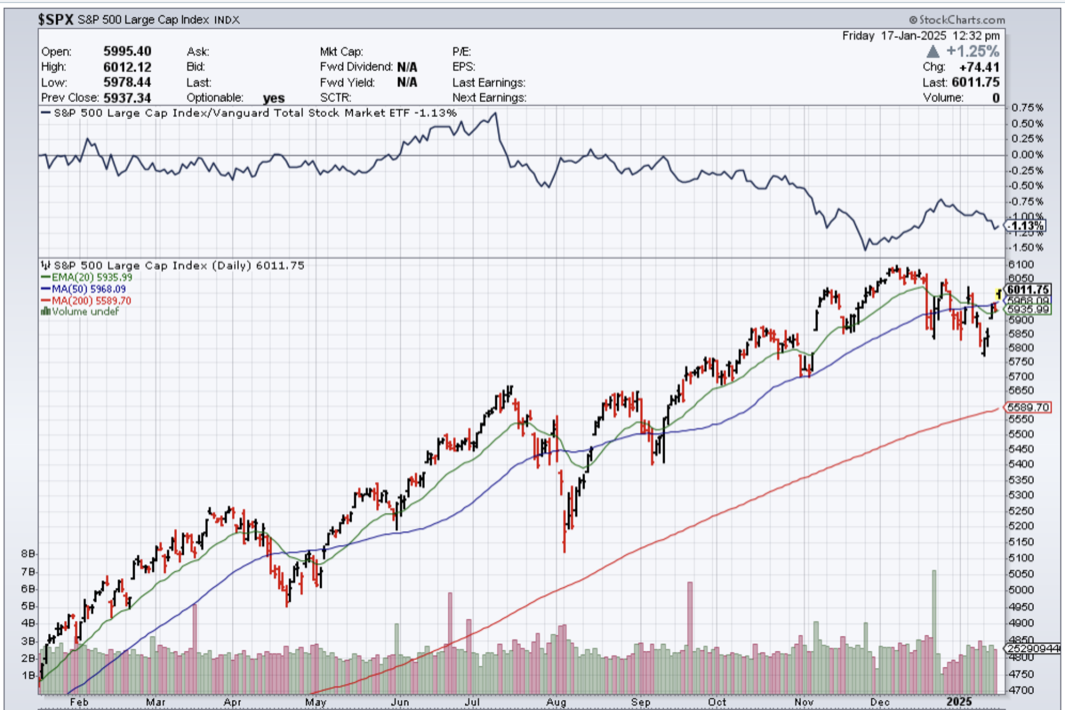

Q: What would I recommend right now for my top five stocks?

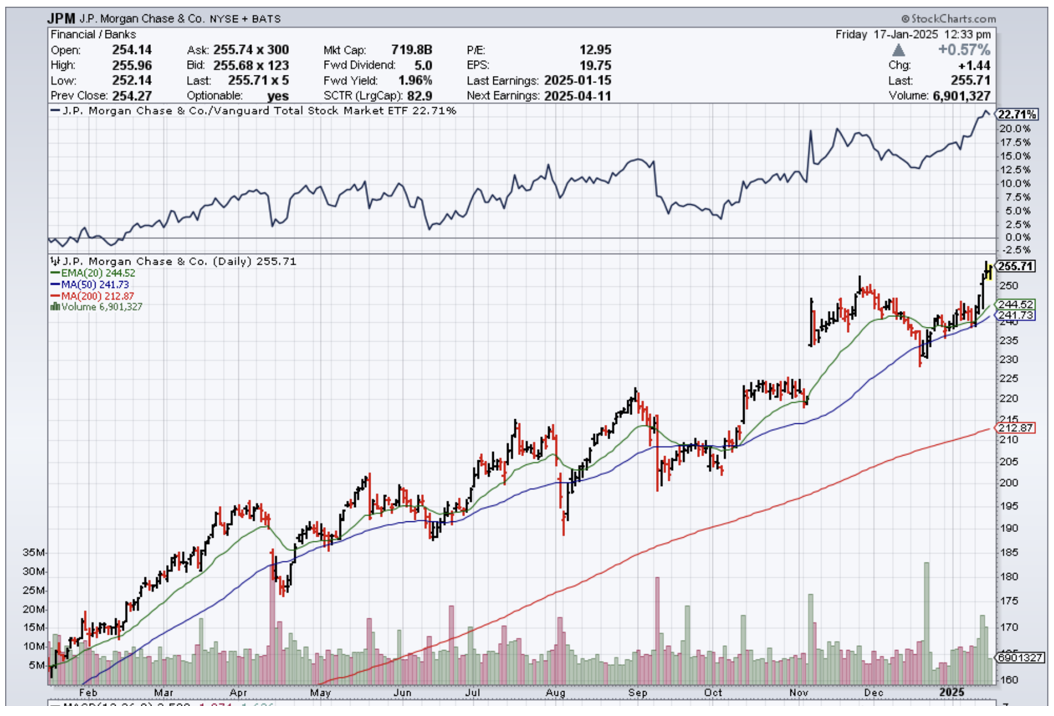

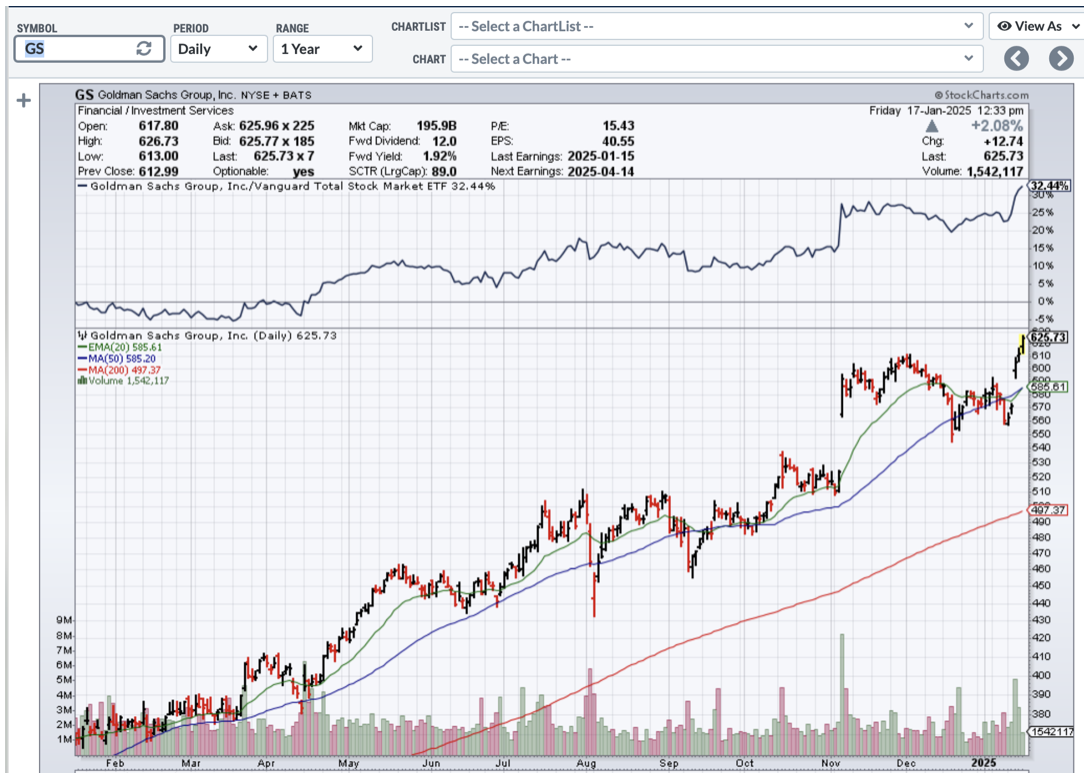

A: That’s easy. Goldman Sachs (GS), Morgan Stanley (MS), JP Morgan (JPM), Citibank (C), and Bank of America (BAC). There's five right there—the top five financials that are coming out of a decade-long undervaluation. A lot of the regional banks, which are also viable, are still trading to discount the book value, which all the financials used to trade out only a couple of years ago. Of course, JP Morgan's reaching a two-year return of around double, but the news just keeps getting better and better, so buy the dips. Buy every sell-off in financials and you will be a happy camper for the year.

Q: What do you think about Robin Hood (HOOD)?

A: Well, the trouble with Robinhood is it’s very highly dependent on crypto volumes. If you think crypto is going to go higher and volumes will increase, this is a great play. However, you get another 95%, out-of-the-blue selloff in crypto like we had three years ago and Coinbase (COIN) will follow it right back down again. On the last downturn, there were concerns that Coinbase would go under, so if you can hack the volatility, take a shot, but not with my money. I have the largest banks in the country that are about to double again; I would much rather be buying LEAPS in that area and getting anywhere from 100% to 1000% percent returns on a 2-year view—much more attractive risk-reward for me. And they pay a dividend.

Q: How do you define a 5% correction?

A: Well, if you have a $100 stock and it drops $5, that is a 5% correction.

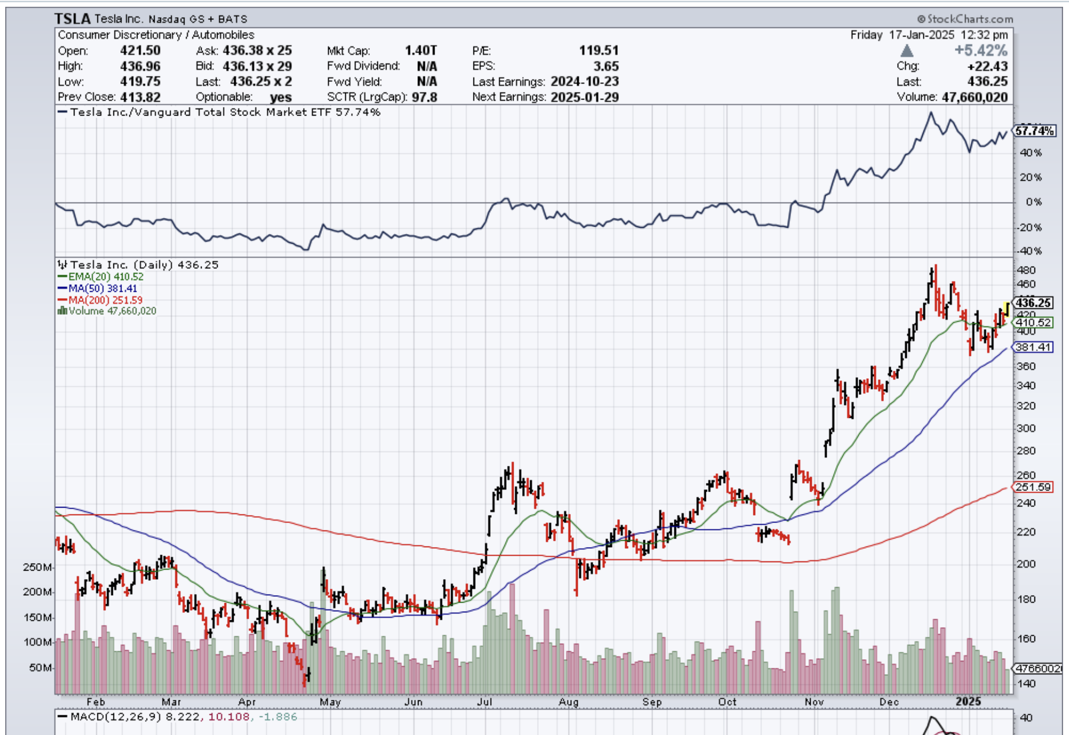

Q: Can you please explain what Tesla 2X leverage actually means and is it a way to trade Tesla as an alternative?

A: I steer people away from the 2Xs because the tracking error is really quite poor. You only get 1.5% of the upside, but 2.5 times the downside over time. These are more day trading vehicles. They take out huge fees, and huge dealing spreads—it's a very expensive way to trade. Far cheaper is just to buy Tesla (TSLA) stock on margin at 2 to 1, and there your tracking error is perfect, your fees are much lower, and you just have the margin interest rate to pay on the position, which is 6% a year or 50 basis points a month. No reason to make the ETF people richer than they already are. They keep coining these products—1x, 2x, 3x long shorts on every one of the high volume stocks, and it sucks a lot of people in, but it's higher risk, lower returns for the amount of money you're risking as far as I'm concerned. So that's the way to do it.

Q: What are your projections for Nvidia (NVDA)?

A: I think not just Nvidia, but all of the big tech is going to be kind of trading in a sideways range for a while, maybe 6 months, and then we get an upside breakout if you get the earnings breakout, which we are all expecting. AI is still in business, and still growing gangbusters. There are always a lot of Cassandra's out there saying that we're going to crash anytime, and I just don't see it. I know a lot of these people, I'm in touch with a lot of the companies, I see Beta releases of all products, the consumer products, and…the slowdown just ain't happening, I'm sorry. And I've been through a lot of these tech booms over the last 40 years, and this is only showing signs of just getting started.

Q: How come Tesla (TSLA) is up and down $30 every couple of days?

A: Number one, it is the most actively traded stock in the market right now. It has implied volatility on the options of 70%, which is really the highest in the market of any individual stock. That just creates immense amounts of trading by options traders, volatility traders, by call writing, and 2x and 3x ETF long and short players. All of the financial engineering and new products that we see all gravitate toward the high volume stocks like Nvidia, Tesla, and Apple because that's where the money is being made. Some days Tesla accounts for 25% of all the market trading. Financial engineers go where the action is, where the volume is, where the customer demand is.

Q: Why do you expect only 5% to 10% corrections if the Fed rate cuts get completely priced out?

A: I don't expect the Fed to keep cutting interest rates. We should get another rate cut this year, and that may be it for the year. If inflation comes back (and of course, all of the new administration’s policies are highly inflationary) it’s just a question of how long it takes for it to hit the system.

Q: Do you believe I should hold all of my municipal bonds (MUB) with 10-year call protection at 4.75%?

A: On a tax-adjusted basis, I would say yes. You know, stock markets may peak and deliver a zero return, and in that situation, muni bonds are very attractive. The nice thing about bonds is that you hold on to maturity—you get 100% of your money back. With stocks, that is not always the case. Stocks you have to trade because the volatility can be tremendous. And in fact, what I do is I keep all of my money in one year Treasury bills. Last time I did this, which was in September, I locked in a one-year return for 5%.

Q: Would you prefer to buy deep in the money and put spreads on top of any rally?

A: Absolutely yes. If this is a real trading year, you not only buy the dips, you sell the rallies. We did almost no real selling last year. We really only did it in June and July because the market essentially went straight up, except for two hickeys. This could be the year of not only call sprints but put spreads as well. You just have to remember to sit down when the music stops playing.

Q: You say buy the dips; what would your dip be in JP Morgan (JPM)?

A: Well lower volatility stocks by definition have smaller drawdowns. JP Morgan (JPM) is one of those, so I'd be very happy to buy a 5% dip in JP Morgan. If it drops more, you double the position on a 10% pullback. Higher volatility stocks like Tesla—I'm really waiting for 10% or 20% corrections. You saw I just bought a 22% correction twice in Tesla with it down 110 points. One of those trades is at max profit right now and the other one has probably made half its money since yesterday. That is the game. The amount of dip you buy is directly related to the volatility of the stock.

Q: Should you let your cash go uninvested?

A: Yes, never let your cash go uninvested just sitting as cash. Your broker will take that money and put it in 90-day T-bills and keep the money for himself. So buy 90-day T-bills as a cash management tool—they're paying about 4.21% right now— and you can always use those as collateral under my positions on margin.

Q: Is Home Depot (HD) a buy on the LA reconstruction story?

A: I would say no, Los Angeles is probably no more than 5% of Home Depot's business—the same with Lowe's (LOW). A single city disaster is not enough to move the stock for more than a few days, and the fact is: Home Depot is mostly dependent on home renovation, which tends not to happen during dead real estate markets because, you know, it takes the flippers out of the market. It really needs lower interest rates to get Home Depot back up to new highs.

Q: Do you expect a big market move at the end of the day when the Fed makes its announcement?

A: The market has basically fully discounted the move on January 28, and if anything happens, there'll probably be a “sell on the news.” So, I expect we could give up a piece of the recent performance on the announcement of the Fed news.

Q: Should we expect trade alerts for LEAPS coming from you?

A: Absolutely, yes. However, LEAPS are something you really only want to do on down moves. If we don't get any, we'll just do the front-month call spreads. You can still make 10%, 20% a month just concentrating on financial call spreads.

Q: What would have happened to our accounts if we kept the (TLT) $82-$85 iShares 20+ Year Treasury Bond ETF (TLT) call spread and it went all the way down to $82?

A: The value of your investment goes to zero. Of course, it was declining at a very slow rate, and the $80: you might have gotten a bounce off the $85 level. But if the inflation number had come in hot, as had all other economic data of the last month, then you could have easily gotten a gap down to $82 and lost your entire investment, because two days is not enough time to expiration to recover that 3-point loss. And that's why I stopped out yesterday.

Q: Didn't David Tepper buy China (FXI)?

A: With both hands last September, yes he did. And my bet is he got out before he got killed. I mean, that's what hedge funds do. He probably got out close to cost, and you likely won't see him promoting China again anytime in the near future.

Q: I have June 530 puts on the S&P 500, should I get rid of them?

A: Yes, I don't see a big crash coming. You probably paid a lot going all the way out to June, and it's probably not worth hanging on to. Put spreads are the better way to go—that cuts your cost by two-thirds and those you only want to put on at market tops.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 8, 2024

Fiat Lux

Featured Trade:

(TAKING A LOOK AT HOME DEPOT)

(HD)

I have been out shopping the neighborhood for good non-tech plays and I found another one.

You are going to think that I am completely MAD by thinking about this trade right now. But I’ve gotten used to that by now.

If you had to pick one sector of the 100 or so that Standard & Poor’s tracks, that is universally hated by all traders and investors, it would have to be the retailers.

Widely viewed as headed for the dustbin of history, many retailers are not going to make it to Christmas, let alone stay in business through 2025.

Do any value screen of all listed stocks, and about half of all the bargain stocks are found in the retail industry.

These are the buggy whip manufacturers of 1901 before they got run over by the auto industry.

Of course, you can blame Amazon, which is rapidly taking over all sales of everything in the US. They have about a 50% market share of all online sales. No wonder the government is going after them with an antitrust case.

This is thanks to their cutting-edge technology and massive economies of scale.

Amazon is probably the number one job destroyer in the US today, with some 5 million retail jobs on the chopping block over the next five years.

However, there is one safe haven that so far seems immune from Amazon’s appetite and that would be Home Depot (HD).

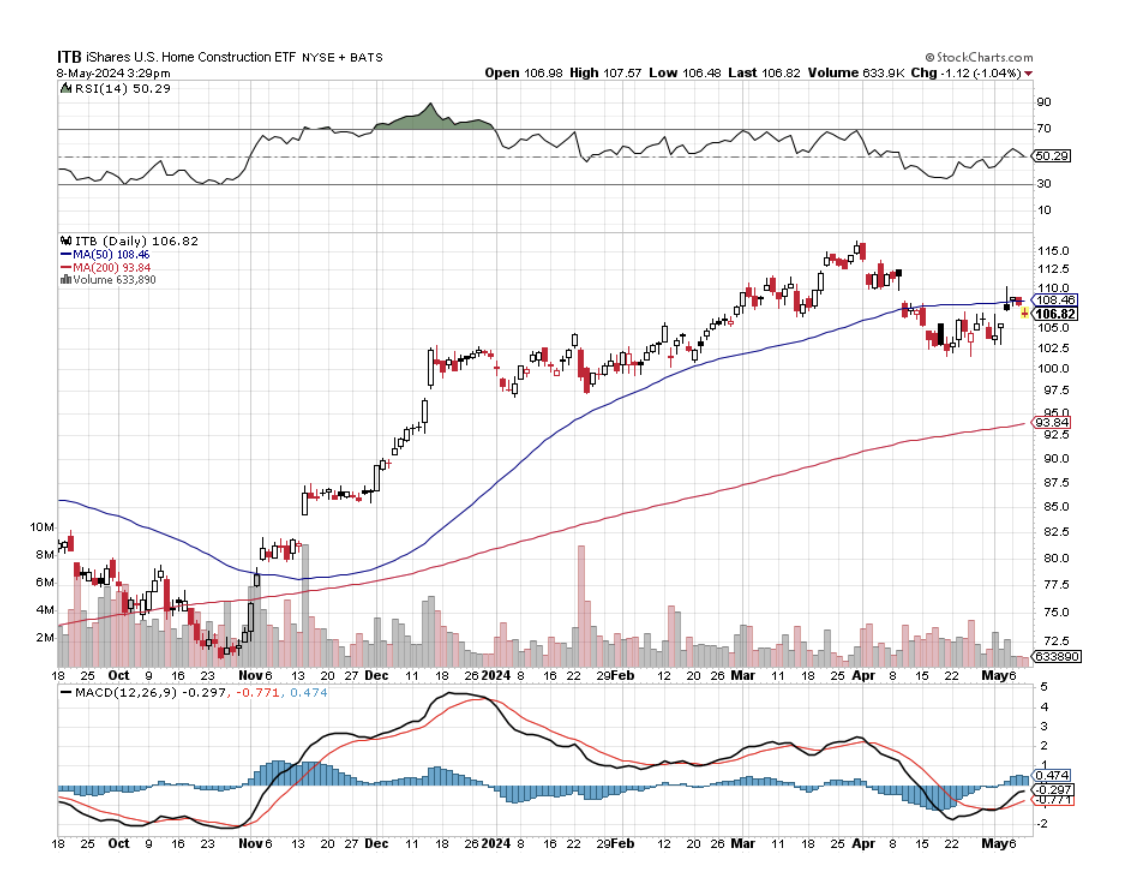

I am using the recent 18% sell-off in the shares to look at (HD), which is occurring, not because of anything Home Depot did, but because of higher interest rates for longer.

Longer term, I think Home Depot will continue to appreciate, as the housing and remodel boom will take off like a rocket once interest rates DO fall. That could be in four months….or sooner.

Then we will have a home remodeling boom that has years to run, and possibly decades. The more expensive homes get, the more inclined owners are to fix up their existing digs. They go to Home Depot to do that.

If you want to make a safer play, buy the iShares US Home Construction ETF (ITB) on this dip, which gives you broader exposure to the real estate recovery and has a much more solid bottom.

Baskets of shares always have lower volatility than single stocks, but lower returns as well.

We just have to give the market a chance to have a few more heart attacks before the current correction ends.

Home Depot is in a tiny retail niche that has so far avoided the Amazon onslaught. There are many reasons for this.

When you need a particular screw, lighting fixture, or unique plumbing part, calling Amazon will get you absolutely nowhere.

You need (HD)’s sympathetic, knowledgeable customer service people, usually retired contractors themselves, to point you in the right direction and assist with a few helpful suggestions.

They’ve done this for me a million times.

Home remodeling and repair is also an industry where a premium is paid for making parts available NOW! A burst pipe won’t wait for an Amazon priority delivery, nor will a leaky roof or broken sprinkler head.

A lot of independent contractors are now not even able to plan supplies weeks or months in advance. They buy what they see.

The home repair and remodel boom will continue, as it is the working man’s solution to high home prices, especially on the coasts, as the profusion of home repair YouTube videos testify. You can fix ANYTHING on YouTube.

While Home Depot recently reported annual revenues of $34.79 billion, up 2.92%. Operating income was reported at $4.8 billion, up 12.82%. Net income came in at an impressive $2.8 billion, up 16.69% YOY. Yet, you get a low 22.7 times price-earnings multiple typical of retailers.

They should do much better in the spring Q2 reporting season. We will know for sure when the company reports on Q2.

This gives us a great discount entry point for a super long-term company, which doesn’t care what the US dollar is doing, which will soon be falling.

Global Market Comments

February 23, 2024

Fiat Lux

Featured Trade:

(FEBRUARY 21 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXI), (SMCI), (PANW), (TSLA), (NVDA), (XLF),

(CCI), (XOM), (FANG), (AMD), (HD), (LOW)

Below please find subscribers’ Q&A for the February 21 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: What do you think of the comments of Ray Dalio and Jamie Dimon of an imminent war with Russia and China?

A: I think the chances of that are almost zero. You’re talking about Russia with a $1 trillion economy going to war against a combined GDP of the US and Europe of $50 trillion. Even Switzerland is sending tanks to Ukraine now. Our military is so dominant compared to any other country in the world, that it would be an instant wipeout. Russia and China know that, so they can threaten all they want but will take no action. That really has been the course since the end of WWII; talk is cheap. However, it is not a zero risk—a person like Ray Dalio, especially, always has to consider the 1% risk (Jamie Dimon less so.) I don’t worry about that at all; a lot of that is media hype. Newspapers have to fill their space every day of the year, even when nothing is happening.

Q: What about Russia putting nuclear weapons in space?

A: The US actually looked at doing this in the 60s and 70s when I was with the Atomic Energy Commission, and this is the problem: Uranium weighs four times that of lead, and it’s very hard to get any serious weight into space. And Russia has never been able to actually hit anything it aims at, so other than destroying a bunch of nearby Starlink satellites, it wouldn’t really accomplish much. Plus, we do have a treaty with Russia not to put nuclear weapons in space—not that agreements between the US and Russia are particularly trustworthy these days.

Q: Would you sell naked Nvidia (NVDA) puts right now?

A: Dan, somehow you got into my personal trading account and looked at all my positions! You know, I never advise people to sell naked puts unless they're happy to own the stock at that level. That means, first of all, you cannot leverage at all—the way people go bust on short put strategies is they sell far more puts than they have the money to support the cash buy if they have to do it. But I can tell you, I looked at the numbers this morning: if you sell short an Nvidia put now at 600 you can get about $10 for it. And, if Nvidia goes below 600 by option expiration day, you own Nvidia stock at a cost of $590. And I'm happy to own Nvidia at $590 because I think it could be worth $1,000 by yearend. There may be better ways to use your money with Nvidia at $600, like doing an at-the-money LEAPS which will get you a 100% return in a year even on no move. If you want to go, say, $40 out of the money or $50, like a 650-$650 Nvidia LEAPS, then you're looking at it with a 150% return in a year. So that is the better way to do it, it just depends on how aggressive you want to be and how eager you are to go back to work at Taco Bell if you lose all your money.

Q: What would you do with Super Micro Computer Inc. (SMCI) right now?

A: I would sell it, but then I would’ve sold it on the first 23x move. (SMCI) is a no-touch right now—I think they have a 3% float in their shares, and that’s what’s causing the spectacular market volatility.

Q: Will continued weakness in China (FXI) bring down the US markets?

A: No. We have very few investors from China in the US stock market. They really have no impact on our market. And the fundamentals couldn't be more different. You know, the US economy is in great shape right now (and getting better, I might add), while China continues to go down the toilet and is saber-rattling and warmongering. So, it's not good for stock prices for sure. You could put that at the bottom of the list of worries.

Q: Will Tesla (TSLA) ever turn around?

A: Well what you don’t know if you don't follow the company on a daily basis like I do, is that Tesla is continuously cutting costs, and increasing performance, and that will lead to greater sales and greater profits. But when that happens, I have no idea. I think the Tesla 2 coming out next year—the $25,000 EV could be a big turning point for the company. And of course, Tesla stock may front-run that by six months. So eventually, Tesla will come back.

Q: Thanks for your advice. I have a ton of Nvidia (NVDA) and some Tesla (TSLA). Should I sell my Tesla and put it in Nvidia?

A: No, you should do the opposite. Buy low, sell high—it’s my revolutionary new stock trading system which I’m thinking of copywriting. Nvidia has had one of the biggest stock gains in history, and Tesla is down year-on-year. So, that is the trade, and that is what a lot of long-term investors are doing, is doing that swap.

Q: Can we do a LEAPS on Palo Alto Networks (PANW)?

A: Absolutely. Wait for this selloff to finish, then go in at the money one year out and you should get a 100% or a double on your return. And by the way, when I’m convinced that tech stocks have finished this selloff, I’ll be issuing a whole bunch of LEAPS trade alerts. I’ll do the numbers and do the heavy lifting for you.

Q: Can Ukraine win the war against Russia without US aid?

A: No, in fact, it needs aid from both the US and Europe. Right now, Europe is carrying 100% of the burden, as the US has stopped providing aid to Ukraine, thanks to the Republican-led House of Representatives. And Ukraine is now ceding cities to Russia because they don’t have the ammunition or the missiles to defend them. So, give as much ammo as we can. Otherwise, it’s just a matter of time before US soldiers get involved in a European war once again. How the Republicans see cutting off as in America’s benefit, I can’t imagine, nor do many Republicans. They must be reading different news sources. But I’m also prejudiced on this, having been shot by Russians in Ukraine in October. (Those injuries are all healed by the way thanks to a stem cell injection and I’m back to hiking as usual.)

Q: When you say buy on dips, do you have a rule of thumb on what percentage a stock has to drop in order to consider it a dip?

A: It’s different for every stock because every stock has a different volatility. “Buy on the dip” might be a 5% for Cleveland Cliffs but it might be 20% for Nvidia. It’s all over the map—you just have to look at the charts and judge where the next support level is, before considering risking your own money.

Q: What’s your favorite dividend stock?

A: Well my Number One favorite, of course, is Crown Castle International (CCI)—the cellphone tower REIT—and REITS of any kind are going to be very high-yield and very attractive. Just stay away from the commercial office REITS, which are having their own well-publicized problems. Beyond that, the only attractive high dividend stocks are in energy: you have Exxon Mobil (XOM) yielding 3.7% and Diamondback Energy with the lovely ticker symbol of (FANG) yielding 4.48%. On the oils, you get a shot for not only the dividend but a nice capital gain on any recovery in the oil market. So that could be an attractive play once we finish bombing the Houthis and wiping out all their Iran-supplied missiles.

Q: What happened to the Japanese yen rally?

A: Well as with all other foreign currencies, it died and went to Heaven, because of the delay in US interest rate cuts. As long as the US doesn't cut interest rates, it will continue to have the strongest currency in the world. And when we get to the currency charts, you'll see exactly how strong the dollar has been. That does make the currencies very attractive right around here.

Q: Will commercial real estate blow up the banks, and therefore the stock market?

A: No, first of all, for big banks (XLF), commercial real estate is only 5% of their loan portfolio and if they lose 20% of that, that’s only a 1% loss of their total loans year for them and that is totally acceptable by in their business model. Second, if interest rates fall, the commercial real estate problem goes away because they can refinance at lower rates than you get now. Third, as the economy recovers, demand for office space will also recover, though it may take 5 years to soak up all the excess inventory that we have right now. San Francisco has an empty office space rate of about 30%, which is higher than it’s ever been. That is why a lot of smart, long-term real estate money is buying up buildings in San Francisco— they're buying them up for pennies on the dollar, so that sounds like a great investment. I remember back in the early eighties, Morgan Stanley did exactly the same thing in Houston after an oil collapse. You know, they were giving away office buildings—paying you to take them away, literally—and Morgan Stanley set up an in-house partner fund (it was only open for the partners from Morgan Stanley to invest in) and we went in and bought 600 million dollar’s worth of cheap Houston real estate. I think we ended up getting a 10x return on that, but that's what being a Morgan Stanley partner is all about. That was about 45 years ago, and it’s what’s happening now in San Francisco.

Q: Are you worried about Amazon (AMZN) with Jeff Bezos selling 8 billion dollars worth of stock?

A: Well, if you've made a couple of $100 billion you're allowed to spend $8 billion on yourself. And Amazon is one of the early leaders in AI technology, so I'm buying that on every dip. In fact, we had a long position in Amazon that just expired on Friday.

Q: Why is Home Depot Inc. (HD) stagnating?

A: Well that's easy: during the pandemic, everyone was stuck at home 24 hours a day, 7 days a week, so they wanted to fix stuff. With the end of the pandemic, that has ended and has slowed down business at both Home Depot and Lowes (LOW).

Q: Do you like Advanced Micro Devices (AMD) and would you buy it on a dip?

A: Absolutely, it’s all part of the same AI trade, as are all the other big chip stocks.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 18, 2023

Fiat Lux

Featured Trades:

(WEDNESDAY, SEPTEMBER 6, 2023 SAN DIEGO, CALIFORNIA GLOBAL STRATEGY LUNCHEON)

(TESTIMONIAL)

(AUGUST 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SNOW), (PANW), (AMZN), (FCX), (WPM), (CCI), (GOLD), (WEAT), (JNK), (TLT), (X), (XOM), (HD), (AA), (UNG), (TSLA)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the August 16 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Did you hear that Michael Burry was putting on a big short (the guy who made a fortune shorting housing in 2009)?

A: Yes, I heard that, but I never, ever trade-off of those kinds of comments. First of all, I think he’s wrong; and often, what happens in those situations is you hear about them going into the trade, but you never hear about them getting out, which might be tomorrow or next week. Also, there’s a nasty habit of big hedge fund managers telling you the opposite of what they’re actually doing. We hear big hedge fund traders like Bill Ackman getting super bearish at market bottoms, and then a few months later learn that they were buying with both hands, as was the case with the pandemic bottom. Be careful about other people’s opinions—they can be hazardous to your wealth. Just look at the data and the facts. That’s what I do.

Q: Would you buy Snowflake (SNOW) around current prices?

A: Yes—first of all Snowflake is a Warren Buffet favorite, which I always tend to follow. However, Warren can wait 5 years for a stock to work, and you can’t. So, I would wait for a bigger dip before getting into SNOW. So far, we are down 25% from the recent peak. One thing’s for sure, cybersecurity is a long-term winner, as seen by the ballistic move in Palo Alto Networks (PANW) since we started recommending it about 8 years ago.

Q: Why are US consumers so strong, and will that hold up for the rest of 2023?

A: US consumers are so strong because they banked so much money during 10 years of QE and all the pandemic stimulus, that they have a lot saved. They are now happy to spend to make up for the spending they couldn’t do during the pandemic. They’re basically in spending catch-up mode or revenge spending.

Q: How far do you see the iShares 20 Plus Year Treasury Bond ETF (TLT) go?

A: My worst-case scenario has it going to $90 down from $94—that’s a yield of about 4.50%. And that's where a lot of bond investors see fair value, and will start piling in. But as long as the momentum is against it, I’m not touching it. As soon as I am convinced there is a real bottom in the (TLT), I’m going to jump in with both hands and buy long-term LEAPS, where you can get a 100% or 200% return pretty quickly.

Q: Time to buy the Tesla (TSLA) dip?

A: We’re getting close. My guess is you might get a spike down to $200 from the recent $300 high. That’s also going to be LEAPS territory for us because the long-term outlook for this company is spectacular.

Q: What do you think of Freeport McMoRan (FCX), Silver (WPM), and United States Natural Gas Fund (UNG)?

A: I think they are all strong buys; I have LEAPS out on all of them. I think we start to get a big move in the 4th quarter of this year that’ll go well into next year—so big money just sitting on the table begging for you to take it.

Q: What are we to make of the crash of the Chinese Yuan?

A: The Chinese economy is weak and looks like it’s getting weaker. They still have a pandemic hangover. We don’t know what their real pandemic numbers are—they adopted our pandemic policy 2 years after we did, and they’re suffering as a result. They also insist on using their own vaccine, Sinovac, for nationalist reasons which is only 30% effective. But, when the Chinese economy does come back on stream, that’ll be the gasoline on the fire for the global economy, and that’s why we like commodities, industrials, energy, and so on.

Q: What does an 8% mortgage rate mean for the housing sector?

A: It is a disaster. I don’t think prices will drop very much—it’ll just cease all new buying because nobody qualifies for an 8% mortgage. They are going to either be only cash buyers out there or people waiting for the next drop in interest rates, and we’re already seeing that with the mortgage rate at 7.24%. If we do get a move up to 8%, it’ll just be a short-term spike that won’t last very long.

Q: Aren’t high-interest rates pushing rents higher?

A: Yes, absolutely. Since people can’t afford to buy houses, they are renting until they can, which pushes rental prices up and adds to the inflation numbers.

Q: When do you think the tech sector will rebound? It’s had a really bad three weeks.

A: End of August or sometime in September. I think. When people come back from the beach, they’re going to look at the long-term future of these companies and think “holy smokes,” why don’t I own more of these?” And we may even be doing LEAPS at high prices, which I almost never do, but the growth rate in tech next year is looking to be spectacular, and I think if we do a conservative at-the-money, we should at least double our money in a few months, similar to how US Steel (X) LEAPS did.

Q: Is Amazon (AMZN) a buy? They’re starting to develop their pharmacy rather well.

A: Yes, Amazon is on the buy list—it’s already up 50% this year. Jassy, the new CEO, is doing a great job. They also have a massive investment in AI which they can monetize anytime they want, and online pharmacies are a great place to start. They’ve been talking about doing that for at least 10 years.

Q: Are gold (GLD), wheat (WEAT), and precious metals a buy?

A: Yes, those are all strong buys on the dip.

Q: What about Tesla (TSLA) LEAPS?

A: Yes Tesla is definitely a LEAPS candidate $30 down from where it is now.

Q: What about Crown Castle International (CCI)?

A: CCI took a major hit from Verizon, canceling a contract with them (which is their biggest customer), so I want to wait for that to digest before I do anything yet. However, we are definitely approaching “BUY” territory; I think the yield is up to about 6.5% now.

Q: Should I take profits on the next jump up in United States Steel Corporation (X)?

A: Yes, it’s not worth hanging on 16 more months to maturity when there’s only 30% of the profit left. And, if all the takeover bids fail for some reason, the stock goes back to $20, and then your LEAPS becomes worthless. So, I would take profits; 100% profit in 2 months is nothing to turn up your nose at.

Q: How confident are you in (TLT) going to $110 by the end of the year?

A: Very confident; by then we will start seeing more hints of Fed interest rate cuts, inflation should be lower, and Goldman Sachs is in fact forecasting that the first rate cut will happen in March. So you’ll certainly start discounting that in the (TLT) by December. We could see the high in yields and the low in prices at the central bankers conference in Jackson Hole next week.

Q: What do you think about cruise lines and hotels right now?

A: The business is great, they’re all packed. However, during the pandemic, these sectors had to take on massive amounts of debt to keep from going under when their ships were tied up with zero revenue for two years; same with the hotels. So, the balance sheets are terrible in all of these areas including airlines. That’s why I’ve been avoiding them, too many better plays. Don’t go away from your core trades looking for trouble.

Q: When do we finally start seeing the Fed stop raising rates?

A: I think they already have; I think the most recent rate rise was the last one. If I’m wrong, they’ll do one more quarter—it’s totally dependent on the numbers.

Q: Won’t falling rates be bullish for bonds and gold?

A: Yes, that's why we’re buying them; but I’m waiting on the bond LEAPS—I want to see a firm bottom before getting back in there. 2024 will be all about falling interest rates plays.

Q: What’s causing the volatility in the United States Natural Gas Fund (UNG)?

A: A Strike in Australia, collapsing supplies in Europe (where prices are up 40%), and expectation of a global economic recovery in China. Ultimately, it’ll be China that takes this thing up to $10, $12, or $14 for the UNG, but you need them to recover first. That’ll probably happen next year, which is why we have the two-year LEAPS on there.

Q: With junk (JNK), have we seen the high rates?

A: Yes. If not, we’re very close, so it’s worth starting to scale in here.

Q: Should I short Home Depot (HD), as US consumers are holding back on home upgrades?

A: No, you should not short anything because you’re going against a long-term bull market trend that probably continues for another 10 years. So, any shorts should be measured in days and not weeks.

Q: Should I start chasing oil, because it’s been on quite a run, and should I buy Exxon (XOM)?

A: Yes, if we get an economic recovery next year, oil goes over 100 easily and will take all the oil companies up with it.

Q: Is (UNG) a domestic or foreign gas ETF?

A: It’s mostly domestic, and it’s a mix of the top natural gas producers in the US.

Q: Are the BRIC countries going to bring down the dollar?

A: You’ve got to be out of your mind. Would you rather store your money in China and Indonesia or the US? That’s your choice. I know there’s a lot of internet conspiracy theories out there—I get about a question a day on this. It’s Never going to happen; not in my lifetime. But it does attract internet traffic, which is the purpose of putting out these ridiculous stories like a BRIC-engineered digital currency replacing the dollar as a reserve currency. It’s just clickbait.

Q: Why is there a short squeeze in copper?

A: EV production is going from 2 million to 10 million a year in 2030, and every EV needs 200 pounds of copper. By the way, there are now 527 EV models on the market, but only one company makes money doing this, and that’s Tesla (TSLA).

Q: We’ve been waiting for a recession in the US for years, and US consumers are still going strong. What gives? I want rates to drop so I can invest in real estate again.

A: Well, yes. This recession has been predicted for 2 years. The problem is we have a certain political party telling us every day that the economy is the worst it’s ever been when, in actuality, the health of the economy is amazingly strong, and certainly the strongest economy in the world. So, I don't think we get a real recession until well into the 2030s because of massive technological development and a huge demographic tailwind—that’s an absolute winning combination, last seen in the 1990s. Plus, now we have AI accelerating everything. So, look at the numbers; don’t listen to opinions. Opinions can be fatal to your wealth.

Q: Does the use of an adjustable-rate loan make sense for the purchase of a second home?

A: Yes, it does. During the great interest rate spike of the 1980s, I bought my home in New York with an adjustable-rate loan. The initial interest rate was 18%, but when rates dropped to 11%, the value of the home tripled. Not a bad trade—and I bet the same kind of opportunity is out there now, provided you can get another adjustable-rate loan. By the way, in Europe, they only have adjustable-rate loans. The 30-year fixed anomaly only exists in the US and Canada because you have the US government as the unlimited buyer of last resort for 30-year fixed mortgages.

Q: Thoughts on other steel companies and aluminum?

A: I like them all. The country needs 200,000 miles of new long-distance transmission lines to accommodate the electrification of the economy, and those are all made out of aluminum except for the last mile—most people don’t know that. Buy Alcoa (AA).

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 27, 2023

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MAKING A SILK PURSE FROM A SOW’S EAR)

(META), (GOOGL), (MSFT), (AAPL), (AMZN), (NFLX), (TSLA), (SPY), (TLT), (ENPH), (UUP), (GLD), (SLV), (EEM)

CLICK HERE to download today's position sheet.

Global Market Comments

February 24, 2023

Fiat Lux

Featured Trade:

(FEBRUARY 22 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (BA), (CCI), (HD), (TLT), (TSLA), (PPLT), (PALL),

(JPM), (NVDA), (AAPL), (GOOGL), (META), (AMZN)

CLICK HERE to download today's position sheet.