Global Market Comments

January 8, 2026

Fiat Lux

Featured Trades:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

January 8, 2026

Fiat Lux

Featured Trades:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

July 1, 2025

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics are destiny, then America’s future looks bleak. You see, they’re just not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the number of middle-aged big spenders is falling, risk markets plunge.

Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

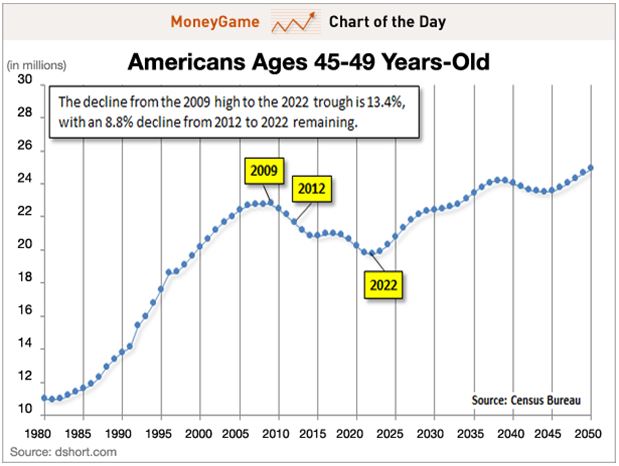

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, but they also backtest with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country, and you can develop a highly reliable timetable for when and where to invest.

Instead of poring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice back test.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2,000’s, and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate, peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle-aged not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan), while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

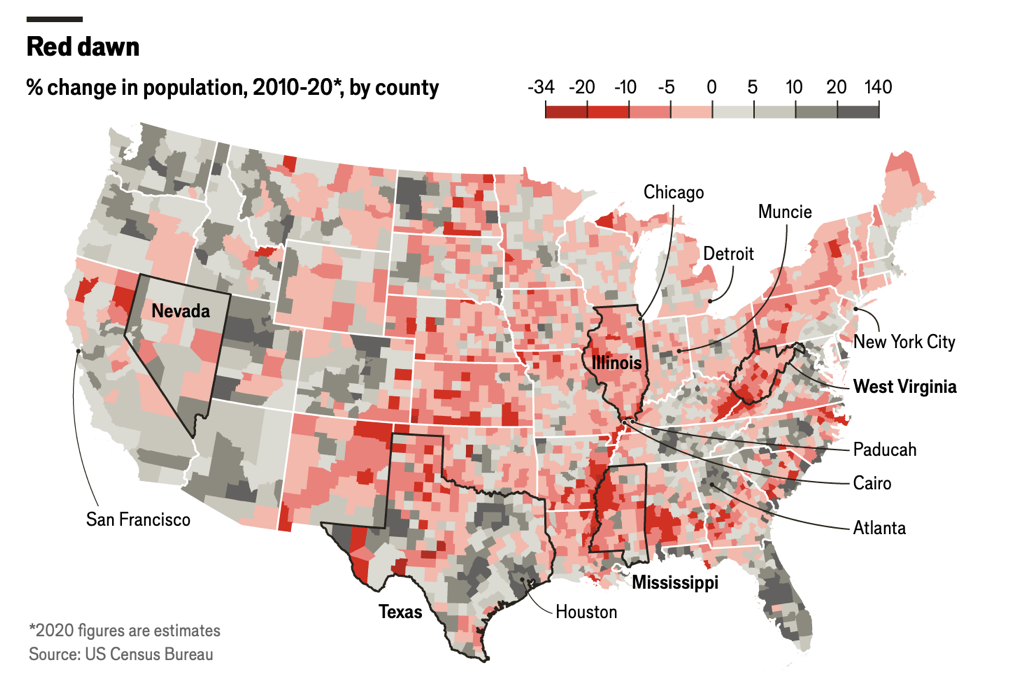

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills is picking up speed, and the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Global Market Comments

December 24, 2024

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

September 25, 2024

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS JUST BEGUN),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL), (CCJ),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

June 28, 2024

Fiat Lux

Featured Trade:

(THE NEXT COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

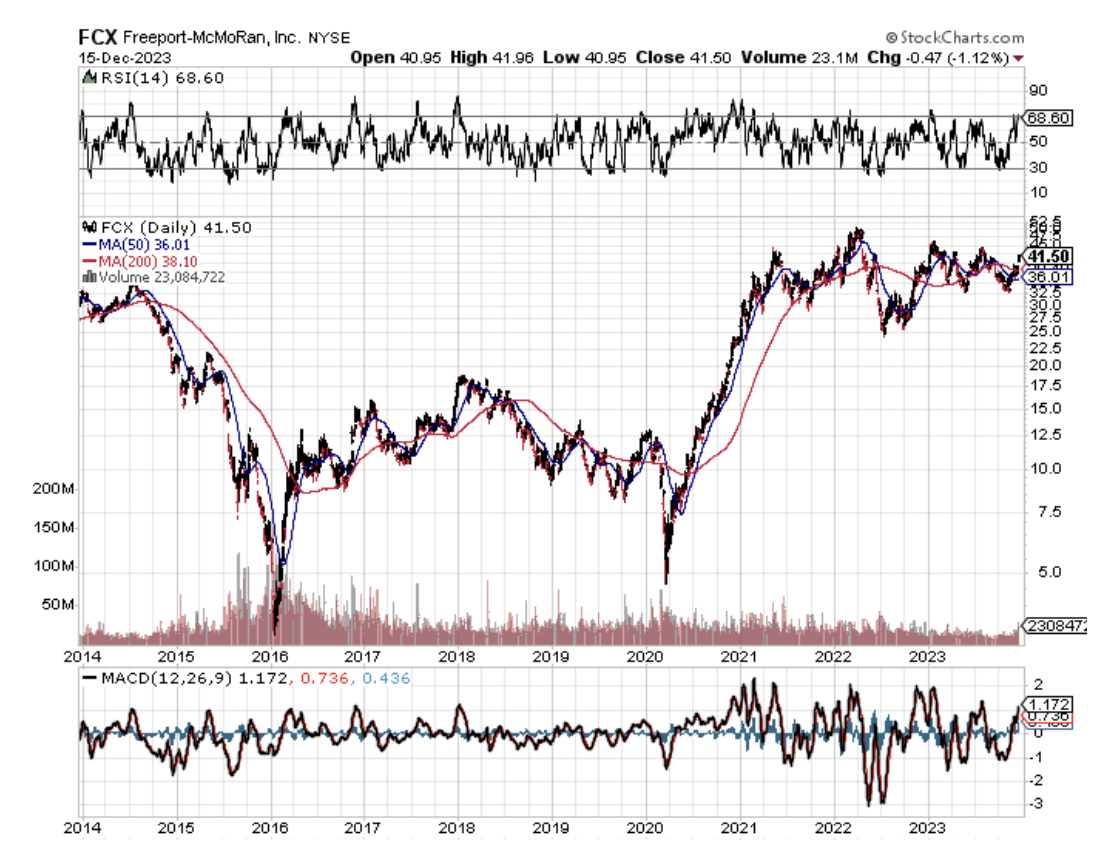

When I closed out my position in Freeport McMoRan (FCX) near its max profit earlier this year, I received a hurried email from a reader asking if he should still keep the stock. I replied very quickly:

“Hell, yes!”

When I toured Australia a couple of years ago, I couldn’t help but notice a surprising number of fresh-faced young people driving luxury Ferraris, Lamborghinis, and Porsches.

I remarked to my Aussie friend that there must be a lot of indulgent parents in The Lucky Country these days. “It’s not the parents who are buying these cars,” he remarked, “It’s the kids.”

He went on to explain that the mining boom had driven wages for skilled labor to spectacular levels. Workers in their early twenties could earn as much as $200,000 a year, with generous benefits.

The big resource companies flew them by private jet a thousand miles to remote locations where they toiled at four-week on, four-week off schedules.

This was creating social problems, as it is tough for parents to manage offspring who make far more than they do.

The Great Commodity Boom has started, and in fact, we are already years into a prolonged super cycle.

China, the world’s largest consumer of commodities, is currently stimulating its economy on multiple fronts, including generous corporate tax breaks and relaxed reserve requirements. Get a trigger like the impending settlement of its trade war with the US and it will be off to the races once more for the entire sector.

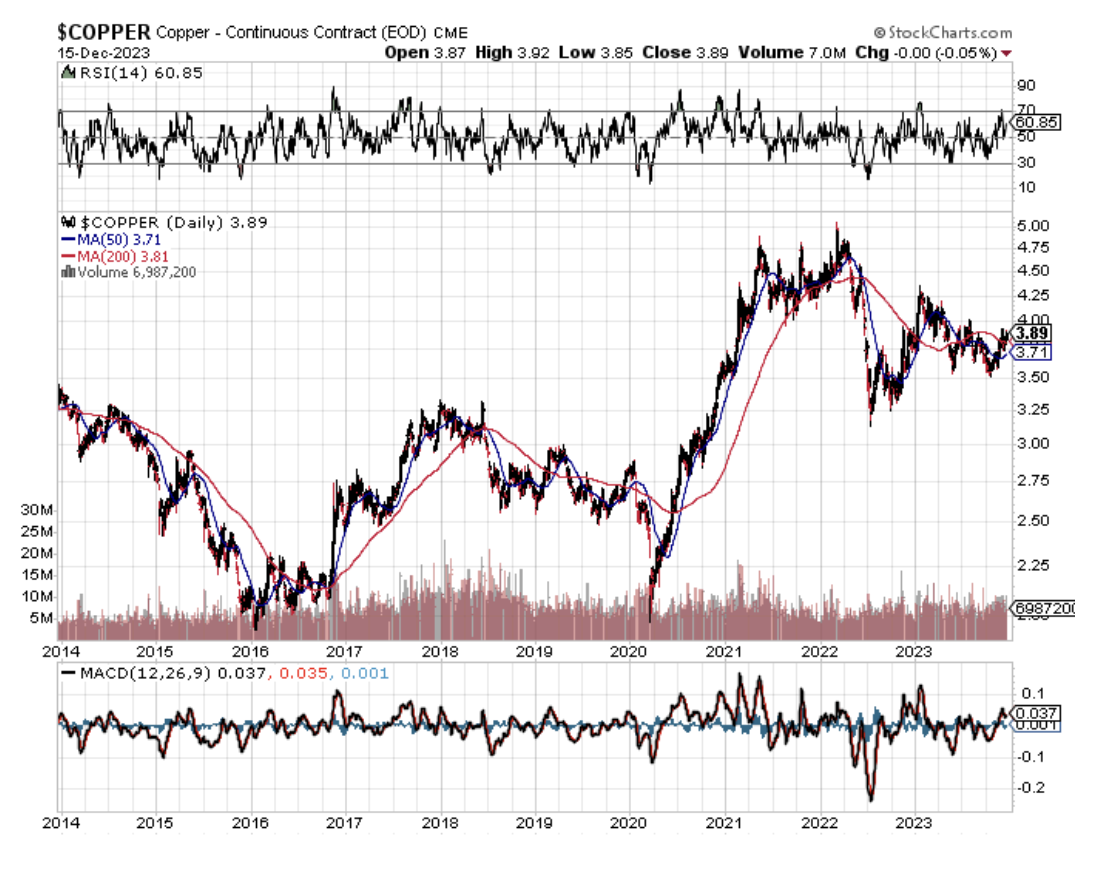

The last bear market in commodities was certainly punishing. From the 2011 peaks, copper (COPX) shed 65%, gold (GLD) gave back 47%, and iron ore was cut by 78%. One research house estimated that some $150 billion in resource projects in Australia were suspended or canceled.

Budgeted capital spending during 2012-2015 was slashed by a blood-curdling 30%. Contract negotiations for price breaks demanded by end consumers broke out like a bad case of chicken pox.

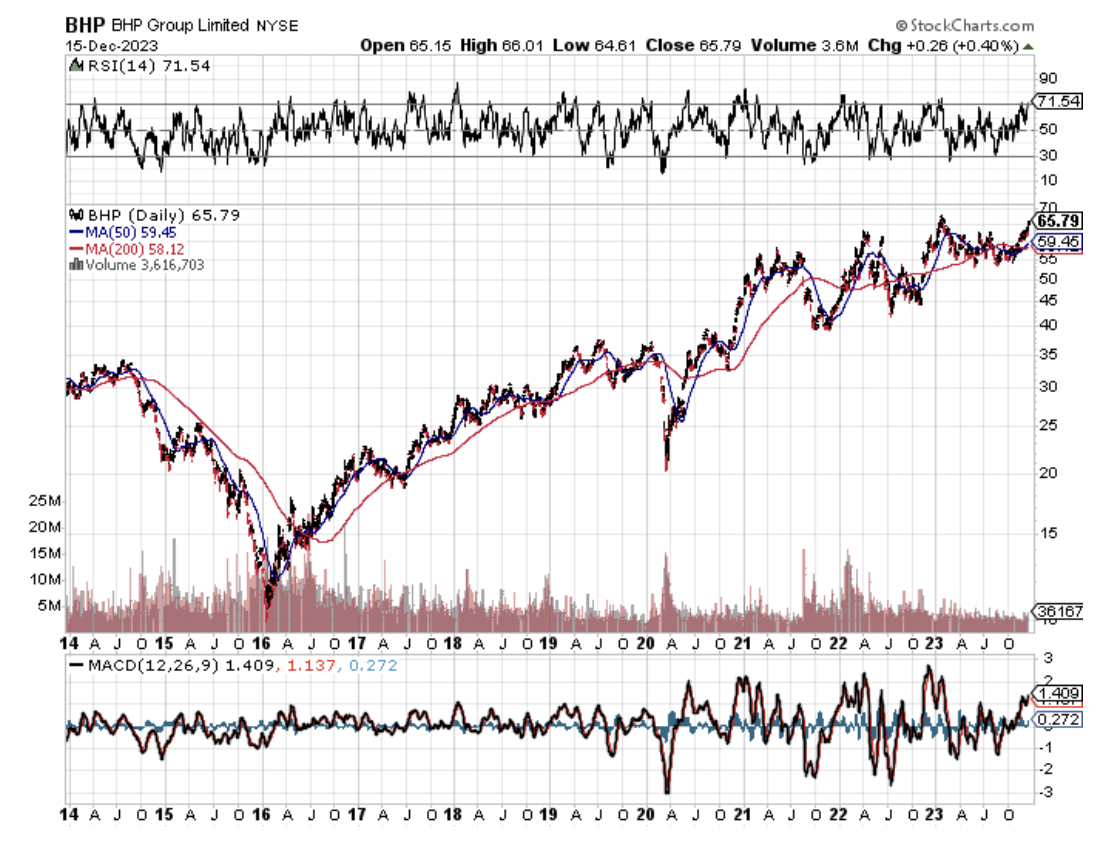

The shellacking was reflected in the major producer shares, like BHP Billiton (BHP), Freeport McMoRan (FCX), and Rio Tinto (RIO), with prices down by half or more. Write-downs of asset values became epidemic at many of these firms.

The selloff was especially punishing for the gold miners, with lead firm, Barrack Gold (GOLD), seeing its stock down by nearly 80% at one point, lower than the darkest days of the 2008-9 stock market crash.

You also saw the bloodshed in the currencies of commodity-producing countries. The Australian dollar led the retreat, falling 30%. The South African Rand has also taken it on the nose, off 30%. In Canada, the Loonie got cooked.

The impact of China cannot be underestimated. In 2012, it consumed 11.7% of the planet’s oil, 40% of its copper, 46% of its iron ore, 46% of its aluminum, and 50% of its coal. It is much smaller than that today, with its annual growth rate dropping by more than half, from 13.7% to 2.3% in 2020.

What happens to commodity prices if China recovers the heady growth rates of yore? It boggles the mind. If China doesn’t step up then India certainly will.

The rise of emerging market standards of living will also provide a boost to hard asset prices. As China goes, so do its satellite trading partners, who rely on the Middle Kingdom as their largest customer. Many are also major commodity exporters themselves, like Chile (ECH), Brazil (EWZ), and Indonesia (IDX), who are looking to come back big time.

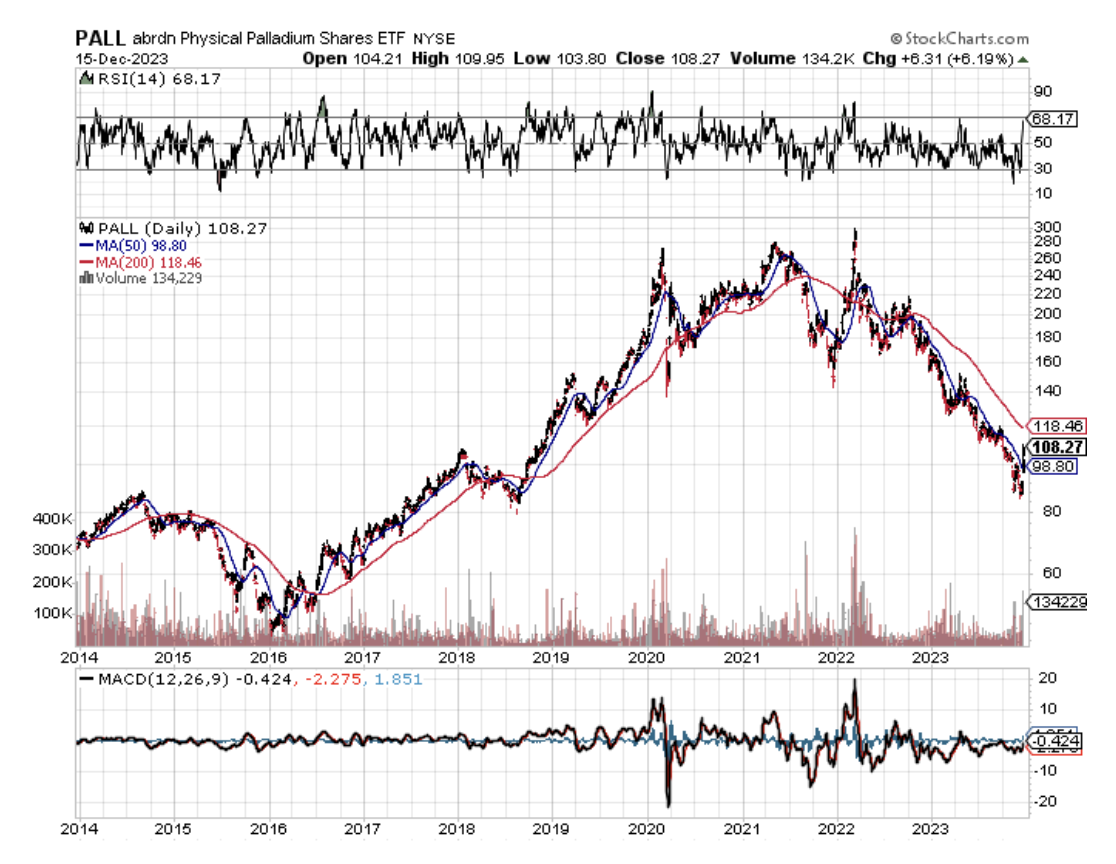

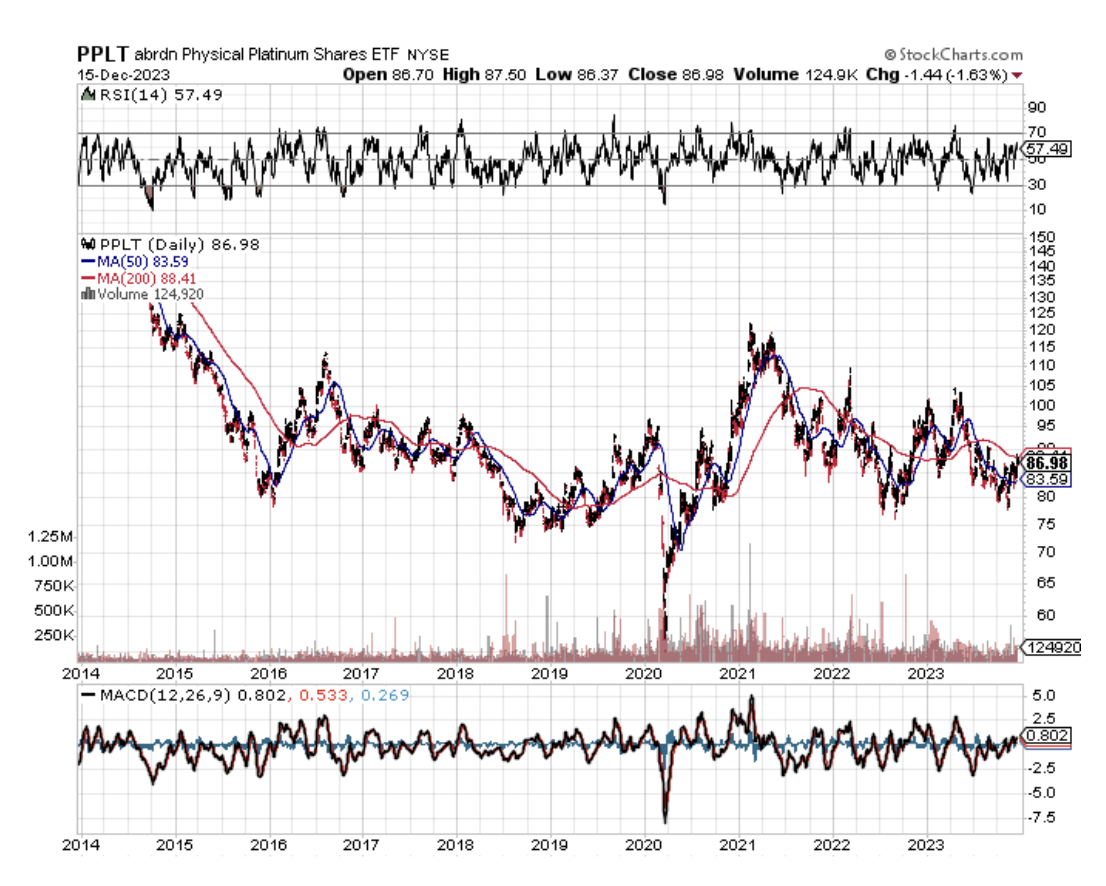

As a result, western hedge funds will soon be moving money out of paper assets, like stocks and bonds, into hard ones, such as gold, silver (SIL), palladium (PALL), platinum (PPLT), and copper.

A massive US stock market rally has sent managers in search of any investment that can’t be created with a printing press. Look at the best-performing sectors this year and they are dominated by the commodity space.

The bulls may be right for as long as a decade thanks to the cruel arithmetic of the commodities cycle. These are your classic textbook inelastic markets.

Mines often take 10-15 years to progress from conception to production. Deposits need to be mapped, plans drafted, permits obtained, infrastructure built, capital raised, and bribes paid in certain countries. By the time they come online, prices have peaked, drowning investors in red ink.

So a 1% rise in demand can trigger a price rise of 50% or more. There are not a lot of substitutes for iron ore. Hedge funds then throw gasoline on the fire with excess leverage and high-frequency trading. That gives us higher highs, to be followed by lower lows.

I am old enough to have lived through a couple of these cycles now, so it is all old news for me. The previous bull legs of supercycles ran from 1870-1913 and 1945-1973. The current one started for the whole range of commodities in 2016. Before that, it was down from seven years.

While the present one is short in terms of years, no one can deny how business cycles will be greatly accelerated by the end of the pandemic.

Some new factors are weighing on miners that didn’t plague them in the past. Reregulation of the US banking system has forced several large players, like JP Morgan (JPM) and Goldman Sachs (GS) to pull out of the industry completely. That impairs trading liquidity and widens spreads— developments that can only accelerate upside price moves.

The prospect of falling US interest rates is also attracting capital. That reduces the opportunity cost of staying in raw metals, which pay neither interest nor dividends.

The future is bright for the resource industry. While the gains in Chinese demand are smaller than they have been in the past, they are off of a much larger base. In 20 years, Chinese GDP has soared from $1 trillion to $14.5 trillion.

Some 20 million people a year are still moving from the countryside to the coastal cities in search of a better standard of living and improved prospects for their children.

That is the good news. The bad news is that it looks like the headaches of Australian parents of juvenile high earners may persist for a lot longer than they wish.

Buy all commodities on dips for the next several years.

Global Market Comments

May 16, 2024

Fiat Lux

Featured Trade:

(THE COMMODITY SUPER CYCLE HAS ALREADY STARTED),

(COPX), (GLD), (FCX), (BHP), (RIO), (SIL),

(PPLT), (PALL), (GOLD), (ECH), (EWZ), (IDX)

Global Market Comments

April 24, 2024

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)