Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 4Global Strategy Webinar broadcast from Silicon Valley with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: If Trump figures out the trade war will lose him the election; will he stop it?

A: Yes, and that is a risk that hovers over all short positions in the market at all times these days because stocks will soar (INDU) when the trade war ends. We now have 18 months of share appreciation that has been frustrated or deferred by the dispute with China. The problem is that the US economy is already sliding into recession and it may already be too late to turn it around.

Q: Do you see the British pound (FXB) dropping more on the Brexit turmoil? Do you think the UK will stay in the EU?

A: If the UK ends Brexit through an election, then the pound should recover from $1.19 all the way back up to $1.65 where it was before Brexit happened four years ago. If that does happen, it will be one of the biggest trades of the year anywhere in the world, going long the British pound. This is how I always anticipated it would end. I was in England for the Brexit vote and I was convinced that if they held the election the next day, it would have lost. The only reason it won was because nobody thought it would— a lot like our own 2016 election. That brings Britain back into the EEC, saves Europe, and has a positive impact on markets globally. So, this is a big deal. Not to do so would be economic suicide for Britain, and I think wiser heads will prevail.

Q: Do you think it’s a good idea for Saudi ARAMCO to go public in Japan as reports suggest?

A: When the Arabs want to get out of the oil business (USO), (XLE), you want to also. That’s what the sale of ARAMCO is all about. They’re going to get a $1 trillion or more valuation, raising $100 billion in cash. And guess who the biggest investors in alternative energy in California are? It’s Saudi Arabia. They see no future in oil, nor should you. This is why we’ve been negative on the sector all year. By the way, bankruptcies by frackers in the U.S. are at an all-time high, another indicator that low oil prices can’t be tolerated by the US industry for long.

Q: Is it time to buy the ProShares Ultra Short 20 year Plus Treasury Bond Fund (TBT)?

A: No, not yet; I think we’re going to break 1.33% — the all-time low yield for the (TLT) will probably be somewhere just below 1.00%. We probably won’t go to absolute zero because we still have a growing economy. The countries that already have negative interest rates have shrinking economies or are already in recession, like Germany or Great Britain can justify zero rates.

Q: Are you going to run all your existing positions into expiration?

A: I’m going to try to—it’s only 12 days to expiration, and we get to keep the full profit if we do. As long as the market is dead in the middle here, there are no other positions to put on, no extreme low to buy into or extreme high to sell into. It’s a question of letting this sort of nowhere-trend play out, but also there's nothing else to buy, so there is no need to raise cash. So, we’re 60% invested now and we’re going to try running as many of those into expiration as we can. Looks like all the long technology positions are safe (FB), (AMZN), (MSFT), (DIS). The only thing we’re pressing here are the shorts in Walmart (WMT) and Russell 2000 (IWM).

Q: Do you think it’s a good idea for Tesla (TSLA) to build another Gigafactory in Shanghai, China during a trade war? Will this blow up in Elon’s face?

A: I don’t think so because the Chinese are desperate for the Tesla technology and they just gave Tesla an exemption on import duties on all parts that need to go there to build the cars. So, that’s a very positive development for Tesla and I believe the stock is up about $10 since that news came out.

Q: Will Roku (ROKU) ever pull back? Would you buy it up here?

A: No, we recommended this thing last year at $40; it’s now up to $165, and up here it’s just wildly overbought, in chase territory. Of course, the reason that’s happening is that the big concern last year was Amazon wiping out Roku, yet they ultimately ended up partnering with Roku, and that’s worth about a 400% gain in the stock. You know the second you get into this, it’s over. There are just too many better fish to fry in the technology area.

Q: What happens if our existing Russell 2000 (IWM) September 2019 $153-$156 in-the-money vertical BEAR PUT spread Russell 2000 position closes between $156 and $153?

A: You lose money. You will get the Russell 2000 shares put to you, or sold to you at $153.00, which means you now own them, and you’ll get a big margin call from your broker for owning the extra shares. If ever it looks like we’re getting close to the strike price going into expiration, I come out precisely because of that risk. You don’t want random chance dictating whether you’re going to make money in your position or not going into expiration. If you’re worried about that, I would get out now and you can still come out with a nice profit. Or, you can always wait for another down day tomorrow.

Q: Is it time to get super aggressive shorting Lyft (LYFT) or Uber (UBER) when they openly admit that they won’t make a profit anytime in the near future?

A: The time to short Uber (UBER) and Lyft was at the IPO when the shares became available to sell. Down here I don’t really want to do very much. It’s late in the game and Uber’s down about one third from its IPO price. We begged people to stay away from this. It’s another example where they waited for the company to go ex-growth before it went public, but it didn’t leave anything for the public. It was a very badly mishandled IPO—it’s now at $31 against a $45 IPO price and was at a new all-time low just 2 days ago. You knew when they offered the drivers shares, the thing was in trouble. Sometime this will be a buy, but not yet. Go take a long nap first.

Q: Is the fact that rich people are hoarding cash a good indicator that a recession is approaching?

A: Yes, absolutely. Bonds yielding 1.45% is also an indication that the wealthy are hoarding cash from other investment and parking it in US treasury bonds. I went to the Pebble Beach Concourse d’ Elegance vintage car show a few weeks ago and all of the $10 million plus cars didn’t sell, only those priced below $100,000. That is always a good indicator that the wealthy are bailing ahead of a recession. If you can’t get a premium price for your vintage Ferrari, trouble is coming.

Q: Argentina just implemented currency controls; is this the start of a rolling currency crisis among emerging nations?

A: No, I believe the problems are unique to Argentina. They’ve adopted what is known as Modern Momentary Theory—i.e. borrowing and printing money like crazy. Unfortunately, this is unsustainable and results in a devalued currency, general instability, and the eventual hanging of their leaders from the nearest lamppost. This is exactly the same monetary policy that the Trump administration has been pursuing since he came into office. Eventually, it will lead to tears, ours, not his.

Q: Is the new all-electric Porsche Taycan a threat to Tesla?

A: No, it’s not. Their cheapest car is $150,000 and it gets one third less range than Tesla does. It’s really aimed at Porsche fanatics, and I doubt they will get outside their core market. In the meantime, Tesla has taken over the middle part of the electric market with the Model 3 at $37,000 a car. That’s where the money is, and Porsche will never get there.

Q: How will the US pull out of recession if the interest rates are at or below zero?

A: It won’t—that’s what a lot of economists are concerned about these days. With interest rates below zero, the Fed has lost its primary means to stimulate the economy. The only thing left to do is use creative means like feeding the economy with currency, which Europe has been doing for 10 years, and Japan for 30, with no results. That’s another reason to not allow rates to get back to zero—so we have tools to use when we go into a recession 12-24 months from now.

Q: What’s the best way to buy silver?

A: The ETF iShares Silver Trust (SLV) and, if you want to be aggressive, the silver miners with the Global X Silver Miners ETF (SIL).

Q: Have global central banks ruined the western economic system as we know it for future generations?

A: They may have—mostly by printing too much money in the last 10 years in order to get us out of recession. This hasn’t really worked for Europe or Japan, mind you, though who knows how much worse off they would be if they hadn’t. What it did do here is head off a Great Depression. If we go back to money printing in a big way, however, and it doesn’t work, we will not have prevented a Great Depression so much as pushed it back 10 or 15 years. That’s the great debate ongoing among economists, and it will eventually be settled by the marketplace.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/JT-with-snorkel-story-1-image-6-e1535059927176.jpg267350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-06 04:02:202019-10-14 09:46:34September 4 Biweekly Strategy Webinar Q&A

(HOW THE MARKETS WILL PLAY OUT FOR THE REST OF 2019), (SPY), ($INDU), (USO), (TLT), (UUP), (COPX), (GLD),

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM WORKS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-29 04:06:502019-08-29 03:42:56August 29, 2019

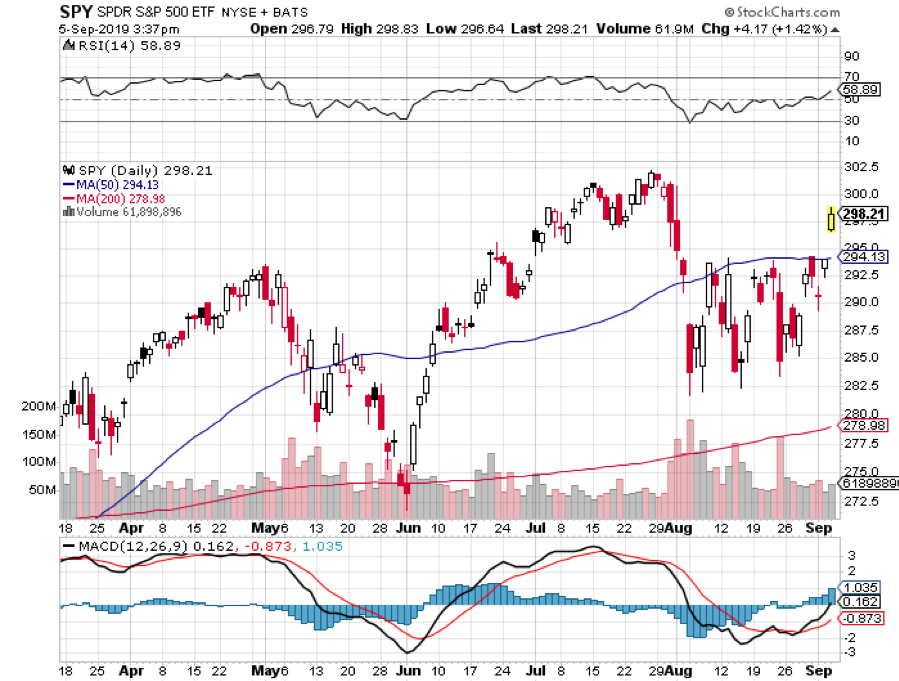

We are currently caught between a rock and a hard place.

The whims of one man will dictate whether after a brutal summer, markets recover to new all-time highs, or plunge into the depths of despair in a bear market and recession.

My bet is that the S&P 500 (SPY) will trade between the 50-day moving average at $294 and the 200-day moving average at $278. Right now, we are dead in the middle of that range.

Then on September 18, the Federal Open Market Committee convenes to deliver a decision on interest rates. I believe that no matter what the decision is, whether they cut rates or leave them unchanged, you will see another sharp selloff in stocks, possibly as much as another 2,000 Dow points. That will bring us a December 2018 repeat.

So why does falling interest rates bring cratering stock prices? For a start, you can take your traditional playbook on how markets are supposed to work and throw it in the trash. Low rates USED to bring high stock prices, but no more.

What is driving markets now is not the absolute level of interest rates today, no matter how low they may be historically. It is how many interest rate cuts are left until we get to zero. So an August 1 25-basis point rate cut meant there are fewer rate cuts in the future so a heart-stopping 2,000-point plunge in the Dow average ensued.

The same twisted logic will apply on September 18, only 16 trading days away. By the way, I plan to be 100% in cash by September 18.

Long term, the outlook gets more complicated.

If the trade war ends in September, then the stock market could rocket up to new all-time highs, surpassing 3,200 by the end of the year, up 14.2% from present levels.

If the trade war drags on, a recession is a sure thing in 12-24 months. That means a bear market in stocks is a sure thing in 6-15 months. And that assumes we are not already in a bear market. After all, the major indexes have been unable to top new highs made in January 2018.

The next bear market will likely take the indexes ($INDU) down 40%. They are, after all, the most overvalued assets in the world.

Oil (USO) will plunge to $25 a barrel. Ten-year US Treasury bond yield (TLT) will collapse to 0%, as I have long been advertising. The US dollar (UUP) leaps, deepening the recession. Commodity prices collapse (COPX) and gold (GLD) soars. We might even get into a shooting war in the South China Sea, as there will be nothing for the Beijing leadership to lose.

Again, it all depends on the whim of one man, one who has never done business in China, and who is constantly surprised by Chinese reactions to his own moves. There is no Trump Hotel in Beijing, nor one planned.

Good luck with that.

Just thought you’d like to know.

Getting Ready for Hard Times

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/John-Thomas-forest-medium.png334500Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-29 04:04:522019-10-14 09:42:48How the Markets Will Play Out for the Rest of 2019

It is often said the markets take the escalator up and the elevator down. A thousand Dow points in three days? That’s like taking the elevator down from the 101st floor of the Empire State Building down to the basement in one shot.

Welcome to your new $30 billion tax, or about $90 per American per year. That will be the effect of the new 10% tariff increase on $300 billion worth of goods imported from China. Unfortunately, this comes on top of an existing $210 per American, bring the total bill due from the China trade war to $300 per person.

Clearly, the Chinese think they can get a better deal from the next president and are inclined to wait it out. This has been my base case since the trade war started 18 months ago.

It was one of the most frenetic, emotion-charged, and violent weeks of the year, with almost daily wild swings on a daily basis. This is the environment where hedge funds and newsletters like this one earn their pay.

The July Nonfarm Payroll Report came in at 164,000, keeping the headline unemployment report to 3.7%. Average hourly earnings grew by a hot 3.2% YOY. The previous two months were revised down by 41,000. Overall, it was a disappointing report.

Manufacturing has been especially weak all year, adding only 16,000 jobs in July and averaging 8,000 jobs a month all year. The headline charge into the services economy continues. Retail lost 3,600, the sixth consecutive monthly decline. The strength was in Professional Services, up 31,000, Health Care at 30,000, and Social Assistance at 20,000.

The broader U-6 “discouraged worker” structural unemployment rate dropped from 7.2% to 7.0%, a new cycle low.

The British Pound (FXB) crashed by 1%, as the harsh reality of a hard Brexit looms. That’s because Boris Johnson, the pro Brexit activist, was named UK prime minister and filled his cabinet with anti-EC doormats. It virtually guarantees a recession there and will act as an additional drag on the US economy.

The end result may be a “Disunited Kingdom”, with Scotland declaring independence in order to stay in the EC, and Northern Ireland splitting off to create a united Emerald Island. The stock market there will crater and the pound will go to parity against the greenback.

Home Price Gains are Still Shrinking, from a 3.5% to a 3.4% annual gain in May, according to the S&P Corelogic Case Shiller National Home Price Index. The Median Home Price hit a new high of $285,700. That can’t buy you a parking space in San Francisco. This is removing a major leg from the economy.

Las Vegas saw the biggest increase at 6.4%, followed by Phoenix at 5.7% and Tampa at 5.1%. Shrinking price gains in the face of falling interest rates is a classic pre-recessionary indicator.

Apple hurdled a low bar, with an upward forward guidance delivering a 5% pop in the stock. Revenues rose 1% to $53.8 billion, while profits dropped 7%. The future looks bright on the eve of 5G iPhones. Hardware drops to less than half of sales for the first time. Services revenues jump to 21% of the total.

China is still a drag. Amazingly, Apple only bought $17 billion worth of its own stock last quarter against a commitment of $100 billion. So why are analyst “BUY” ratings at a decade low? Maybe it's because threats of retaliation in the China trade war are hanging over Apple like a sword of Damocles.

It took only three words to kill Wall Street. Confusion reigns. “Mid Cycle Adjustment” was how Fed governor Jay Powell described Wednesday’s 25 basis point interest rate cut, the first in 12 years, absolutely what the market didn’t want to hear. That implies that the Fed is “one and done,” and that there will be no more interest rate cuts in this economic cycle.

The president added insult to injury piling abuse on his own appointee, further eroding confidence in the independence of the Fed. A truly data dependent Fed wouldn’t have budged last week.

Bonds soared on “one and done.” Higher rates for longer give a new lease on life for the fixed income markets everywhere. Since 2008, major central bank balance sheets have exploded from $3 trillion to $16 trillion, and there is nowhere better for this mountain of money to go but the ten-year US Treasury bond.

Yields have smashed the four-year low at 1.82% and are headed to 1.40% by yearend. The market is wildly overbought for now on the back of an instant three-point rally, so keep buying those dips. Next up is the century low in rates.

Oil crashed 8% on increased global recession fears, in the worst plunge in four years and one of the biggest swan dives in history. The strong dollar doesn’t help either. I have recommended that investors avoid energy like the plague all year and it has worked like a charm. Long term, it’s going out of business anyway, so I don’t even want to trade it here.

Retailers got destroyed on the China news, with stocks down 6%-12% across the board. Best Buy (BBY) did a 12% swan dive. This will be the stick that broke the camel’s back for a lot of retailers already hanging on by their fingernails. Some 42% of US apparel, 69% of footwear, and 84% of accessories come from China.

Squeezed by Amazon on one side and administration China policies on the other, this will spell the death of retail. It looks like we’re going to have to go barefoot this winter. Thank goodness there’s global warming. The death spiral was further confirmed by the weak jobs figures in retail this morning.

I went into the week 100% in cash, giving me the dry powder to pursue the short side aggressively. I always tell followers that cash is a position, that it has option value, and this was a classic example of how well that can work.

The second I heard about the China tariff increase, I went pedal to the metal and increased my shorts from 0% to 40%, against 60% cash. My current shorts include the S&P 500 (SPY), US Treasury bonds (TLT), the Russel 2000 (IWM), and the giant retailer (WMT).

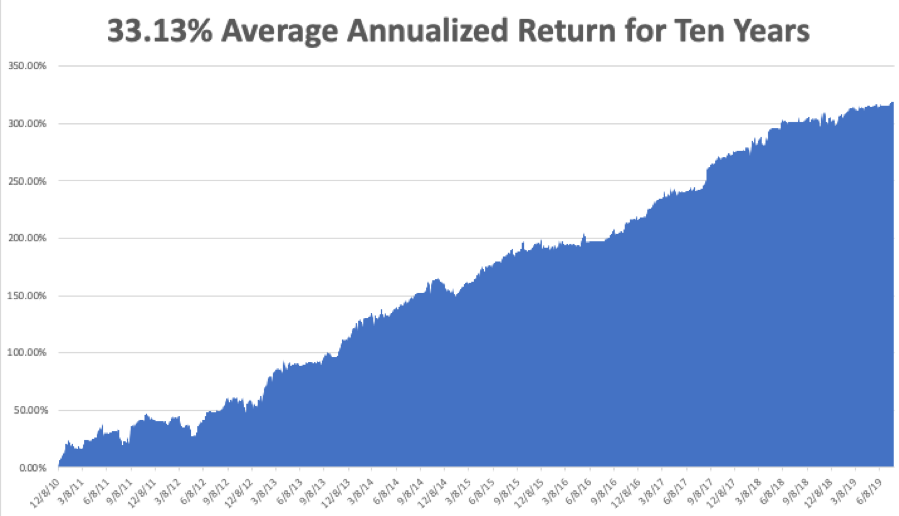

I see August as the best short selling opportunity of the year. I put out my first shorts the day after the Fed rate cut. My Global Trading Dispatch has hit a new all-time high of 320.30% and my year-to-date shot up at +20.16%. A robust earned a robust 1.83% so far in August, and 4.78% since I went back into the market from Zermatt, Switzerland three weeks ago.

My ten-year average annualized profit bobbed up to +33.13%. My Mad Hedge Market Timing Index saw one of the sharpest declines in its history, plunging from 65 to 23 on only two days. We could even be back to “BUY” territory by the end of next week.

The coming week will be a feeble one on the data front. Believe it or not, it could be a quiet week.

On Monday, August 5 at 2:00 PM, the July ISM Non-Manufacturing PMI is out.

On Tuesday, August 6 at 2:00 PM, the June JOLTS Jobs Openings report is published.

On Wednesday, August 7, at 8:30 AM, June Consumer Credit is released.

On Thursday, August 8 at 8:30 AM, the Weekly Jobless Claims are printed.

On Friday, August 9 at 8:30 AM, July Core Purchasing Price Index is printed, an inflation indicator.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, believe it or not, I have not been to the beach this year. As a native Californian, that is near high treason. So I am loading up the old Tesla with an ice chest, boogie boards, and kids and headed to nearby Stinson Beach in Marin County. I’m going early to beat the traffic and will take my usual short cuts I learned while living there eons ago.

Surf’s up!

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2016/08/John-in-Cap-e1473378948252.jpg400301Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-05 09:02:002019-09-04 13:21:52The Market Outlook for the Week Ahead, or Taking the Elevator Down

Featured Trade: (ITALY’S BIG WAKE UP CALL), (TLT), ($TNX), (TBT), (SPY), ($INDU), (FXE), (UUP), (USO), (WELCOME TO THE DEFLATIONARY CENTURY), (TLT), (TBT),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-31 10:06:422019-07-31 10:21:42July 31, 2019

Those planning a European vacation this summer just received a big gift from Mario Draghi, the outgoing president of the European Central Bank. His promise to re-accelerate quantitative easing in Europe has sent the Euro crashing and the US dollar soaring.

Over the last two weeks, the Euro (FXE) has fallen by 2.5%. That $1,000 Florence hotel suite now costs only $975. Mille Gracie!

You can blame the political instability in the Home of Caesar, which has not had a functioning government since WWII. The big fear is that the extreme left would form a collation government with the extreme right that could lead to its departure from the European Community and the Euro. Think of it as Bernie Sanders joining Donald Trump!

In fact, Italy has had 62 different governments since WWII. They change administrations like I change luxury cars, about once a year. Welcome to European debt crisis part 27.

I can’t remember the last time markets cared about what happened in Europe. It was probably the first Greek debt crisis in 2011. As a result, German ten-year bunds have cratered from 0.60% to -0.40%. But they care today, big time.

Given the reaction of the global financial markets, you could have been forgiven for thinking that the world had just ended.

US Treasury Bond yields (TLT) saw their biggest plunge in years, off 120 basis points to 2.05%.

Even oil prices collapsed for an entirely separate set of reasons, the price of Texas Tea pared 20% since April on spreading global recession fears.

Saudi Arabia looks like it's about to abandon the wildly successful OPEC production quotas that have been boosting oil prices for the past year. Iran has withdrawn from the nuclear non-proliferation treaty, responding with an undeclared tanker war in the Persian Gulf, which I flew over myself only a few weeks ago. The geopolitical premium is back with a vengeance.

So if the Italian developments are a canard, why are we REALLY going down?

You’re not going to like the answer.

It turns out that rising inflation, interest rates, oil and commodity prices, the US dollar, US national debt, budget deficits, and stagnant wage growth are a TERRIBLE backdrop for risk in general and stocks specifically. And this is all happening with the major indexes at the top end of recent ranges.

In other words, it was an accident waiting to happen.

Traders are extremely nervous, global uncertainty is high, the seasonals are awful, and Washington is a ticking time bomb. If you were wondering why I was issuing so few Trade Alerts in July, these are the reasons.

This all confirms my expectation that markets could remain stuck in increasingly narrow trading ranges for the next six months until the presidential election begins in earnest.

Which is creating opportunities.

The global race towards zero interest has the US as the principal laggard. So you should keep buying every serious dip in the bond market.

Stocks are still wildly overvalued for the short term, so I’ll keep my low profile there. As for gold (GLD) and the currencies, I keep buying dips there as well.

So watch for those coming Trade Alerts. I’m not dead yet, just resting. The contest here is to make as much money as you can, not to see how many trades you can clock. That is a brokers' game, not yours.

Waiting for My Shot

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-15.png389489Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-31 10:04:572019-08-27 14:39:43Italy’s Big Wake Up Call

(LAST CHANCE TO ATTEND THE FRIDAY, JULY 19 ZERMATT, SWITZERLAND STRATEGY SEMINAR)

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR HERE COMES YOUR NEXT HEART ATTACK),

(INDU), (SPY), (TLT), (GLD), (FXA), (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 01:06:032019-07-14 22:01:51July 15, 2019

Sitting on a remote Alpine mountaintop this morning, this being Switzerland one with ample WIFI, I turned on my screen for the first time in four weeks and almost had a heart attack.

Risk markets everywhere have gone up almost every day since I left San Francisco in June, taking the major indexes up to new all time highs. They are doing this in the face of slowing global economies, falling earnings growth, and rising energy prices and inflation. Even the respected Atlanta Fed has a Q2 GDP growth forecast of a dismal 1.4%.

Did I mention that the US government is about to run out of money again in September, inviting another shut down?

In the old days the Federal Reserve used to be the sober chaperone at the party, making sure things didn’t get out of hand. Today, they are the devilish frat boy surreptitiously pouring 200 proof ethanol into the punch bowel, much as I used to do at Chemistry Department parties at UCLA during the early 1970s. The problem was that everyone else was doing the same thing, leading to some prodigious hangovers.

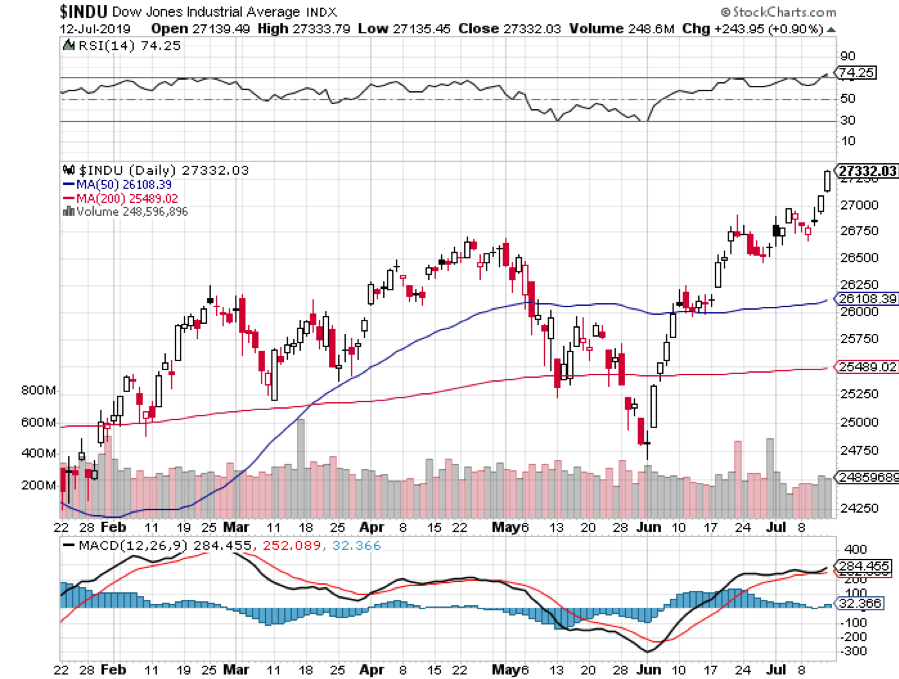

Another pint made it into the heady brew on Wednesday when Fed governor Jay Powell erred dovishly in his Humphrey Hawkins testimony in from of congress. It was enough to ignite the latest 500-point rally in the Dow (INDU).

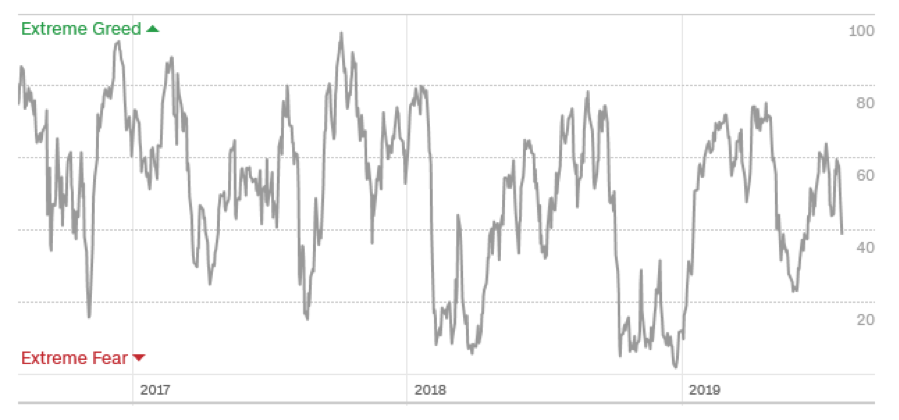

The bullishness was confirmed by my own algorithmically driven Mad Hedge Market Timing Index, which reached a three-month high at 65. We have rallied an awesome 45 points from the 20 level in only six weeks and are now a mere 10 points away from solid “SELL” territory.

The end result of all this has been to bring forward my yearend target for the S&P 500 (SPY) of the low 3,000s to, like well, now. And if H1 has been one giant love best, how does that bode for H2?

A frightening convergence of events is setting up. Just when the Fed announces its interest rate decision on July 31, companies will be announcing earnings disappointments AND my Market Timing Index will be hitting the high seventies.

It all sets up what we traders call “an asymmetric risk/reward.” Good news will bring small incremental gain while even a small disappointment will serve up a horrendous sell off. Fed funds futures are now indicating a 100% of a 25-basis point rate cut on the 31st, and see overnight rates plunging to only 1.75% by yearend end. Hence the heart problems mentioned above.

So as much as you may despise, loathe, and hurl epitaphs at me, I am not going to tell you to buy the stock market today. Your last chance to do that was the final week of May.

The quality trade these days is clearly in other asset classes, like bonds (TLT), foreign exchange (FXA), gold (GLD), and energy (USO). My only exceptions will be “BUYS” in any bombed out high-quality single names I can find.

As I have been out of the market, my Global Trading Dispatch has been flat ling at up 15.38% year-to-date and has earned precisely 0% so far in July. My trailing one-year declined to +14.2%.

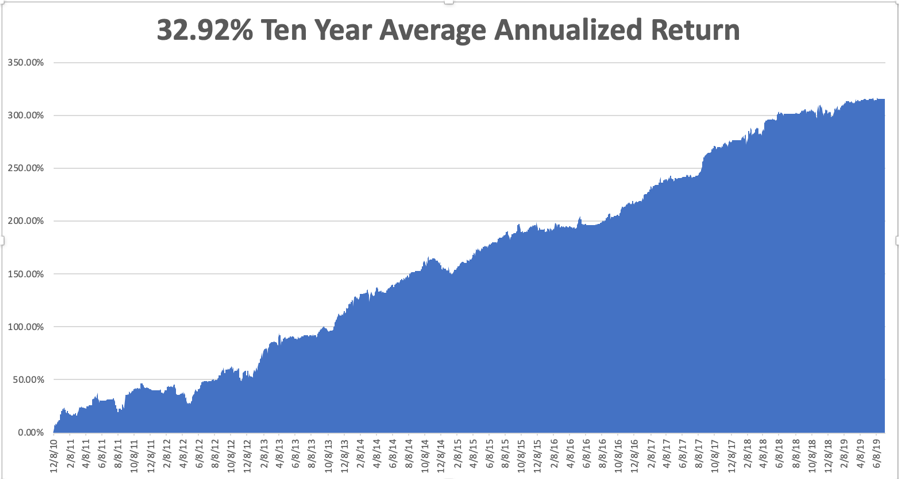

My ten-year profit fell back to +32.92%.With the markets now in the process of peaking out for the short term I am now 100% in cash with Global Trading Dispatch and 100% cash in the Mad Hedge Tech Letter.

The coming week will be a fairly sedentary one on the data front after last week’s fireworks.

On Monday, July 15 at 9:30 AM EST, New York’s Empire State Manufacturing Index is released.

On Tuesday, July 16 8:30 AM EST, the June US Retail Sales are out.

On Wednesday, July 17 at 8:30 AM EST, June Housing Starts are published.

On Thursday, July 18 at 8:30 AM EST, the Weekly Jobless Claims are printed. We also get the Philadelphia Fed Manufacturing Index.

On Friday, July 19 at 8:30 AM EST, we get the University of Michigan Consumer Sentiment Index. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am how on my usual summer schedule. I’ll be getting up early every morning to climb an Alpine peak. Then I’ll be riveted to my screen by 3:30 PM when the US markets open, scouring the world for good Trade Alerts.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Market Timing Index

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-8.png422564Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 01:02:042019-07-14 22:02:55The Market Outlook for the Week Ahead, or Here Comes Your Next Heart Attack

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.