(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE IS YOUR POST-ELECTION PORTFOLIO

plus THE LAST SILVER BUBBLE)

(NVDA), (META), (CRM), (TLT), (JNK), (CCI), (DHI), (LEN), (PHM),

(GLD), (SLV), (NEM), (FXE), (FXB), (FXA), (TSLA), (JPM),(BAC), (GS)

The world was supposed to end at midnight on December 31, 1999 because computers would be unable to cope with the turnover of the new millennium. I remember making presentations to big hedge funds, predicting that Y2K was a big nothing burger and, worst case, somebody’s toaster wouldn’t work.

I spent that New Year’s Eve with my kids at Disneyland in Orlando, watching one heck of a fireworks display. What happened the next morning? Even the toasters worked.

I think we are setting up for another Y2K outcome, except that this time, it’s the presidential election that has everyone in a tizzy.

The polls are tied at 48%-48% with a margin of error of 4%. In fact, for the last 50 years, the opinion polls have been wrong by an average of 3.4%. One side already has that 3.4% and probably more, plus all seven battleground states, but we won’t know for sure until November 6.

As an investment manager, it is not my job to pick a side or impose my view upon you but to deliver the best possible investment returns for my clients.

And let me tell you how.

Remember the Pandemic? Four years after the event, we now have the luxury of copious hard data. Out of 103,436,829 cases, some 1,203,648 Americans died, or 1.3%. But, the death rate in red states was much higher than in blue states.

For example, California suffered only 101,159 deaths out of a population of 39,128,162 for a death rate of 0.26%. Florida saw 86,850 deaths out of a population of 22,634,867 for a death rate of 0.38%. Deaths in Florida were 68% higher in the Sunshine State than in the Golden State.

Florida, in effect, traded lives for business profits. Florida also had a Typhoid Mary effect in that by staying open for spring breaks and vacations; it increased the death rates in surrounding red states.

Assume that half of those who died were voters and apply this math to the entire country, and Republicans lost 393,059 votes to the pandemic compared to only 268,935 for Democrats. Some 124,125 more Republican voters died than Democrats. Is 124,125 votes enough to decide this election?

Absolutely!

In the 2020 presidential election, Biden won the three battleground states of Georgia by the famous 11,779 votes, Arizona by 10,457 votes, and Nevada by 33,596 votes. That’s 33 electoral college votes right there out of 270 needed.

The opinion polls have missed these numbers by a mile because their algorithms don’t take the pandemic into consideration. They are counting dead voters, while the actual election polls only count live ones. I predict that the opinion polls will be spectacularly wrong….again.

Of course, these are back-of-the-matchbook ballpark calculations. I’ll leave it to some future aspiring PhD candidate to research his thesis with more precise figures. I have better things to do.

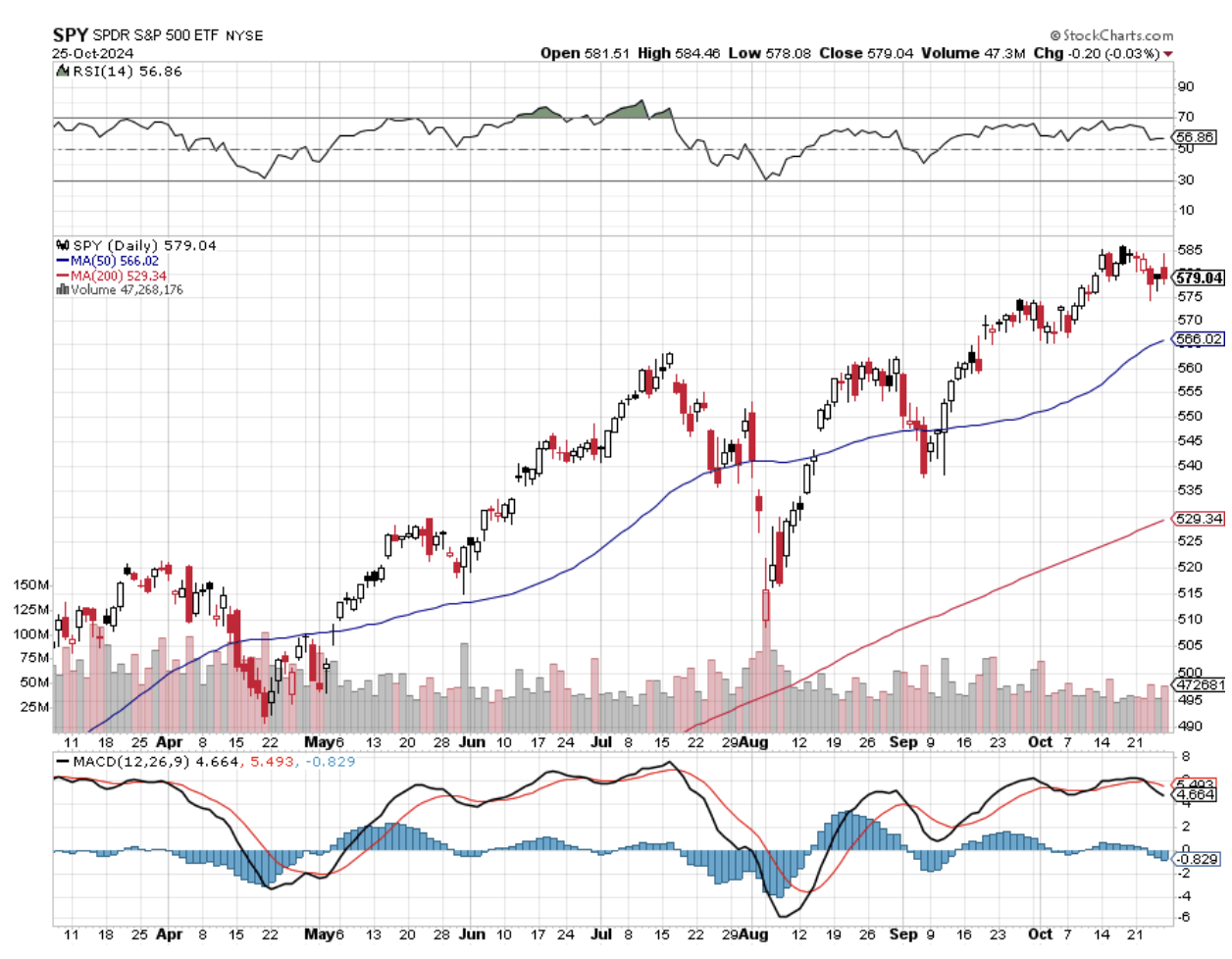

So, how do we make money off of all this? I have never seen investors so underweight and cautious going into a major risk event like this election. They have been scared out of the market by the media. Therefore, I expect the stock market to rise by 10% after the election, taking the S&P 500 as high as 6,400.

Let the great chase begin!

Here is your model portfolio for the rest of 2024.

(NVDA), (META), (CRM) – Underweight fund managers will chase this year’s best performers so they can look good at yearend. Similarly, they will dump their worst performers in the energy sector. So will individual investors for tax loss harvesting.

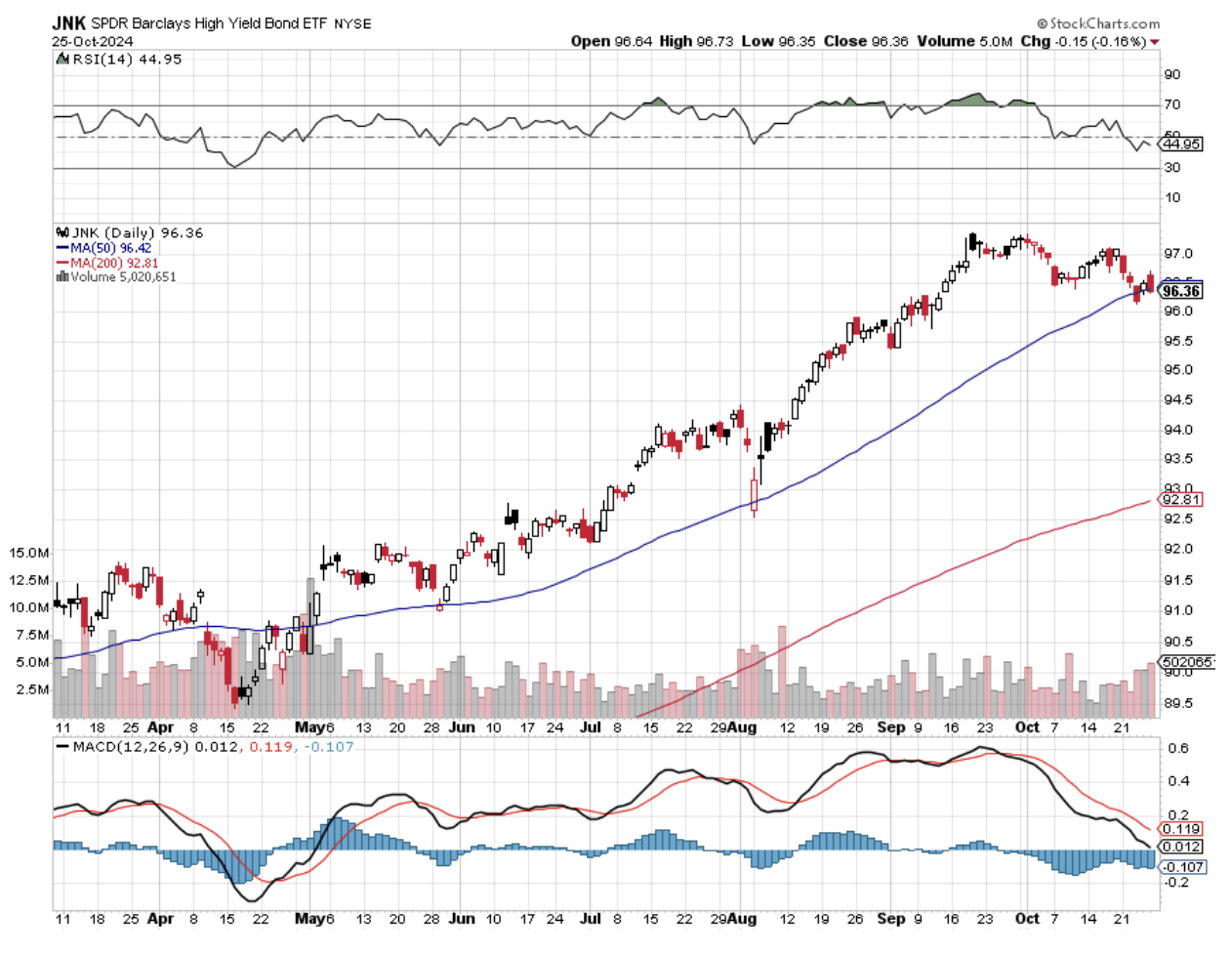

(TLT), (JNK), (CCI) – All interest rate plays make back recent losses as the threat of $10-$15 trillion in new borrowing by a future president, Trump, disappears.

(DHI), (LEN), (PHM) – There is no better interest rate play than new homebuilding. It’s tough to beat a structure shortage of 10 million homes.

(GLD), (SLV), (NEM) – Precious metals also do very well as they have less yield competition from other interest rate plays. These have become the principal savings vehicle for Chinese individuals.

(FXE), (FXB), (FXA) – A falling interest rate advantage for the US dollar means you want to buy all the currencies.

(JPM), (BAC), (GS) – Banks also do exceedingly well in a falling interest rate environment, and brokers and money managers will cash in on exploding stock market volume.

Also, on November 6, your toaster will probably still work. And I will never understand why the Center for Disease Control never accepted my application out of college. So, I went to Vietnam instead.

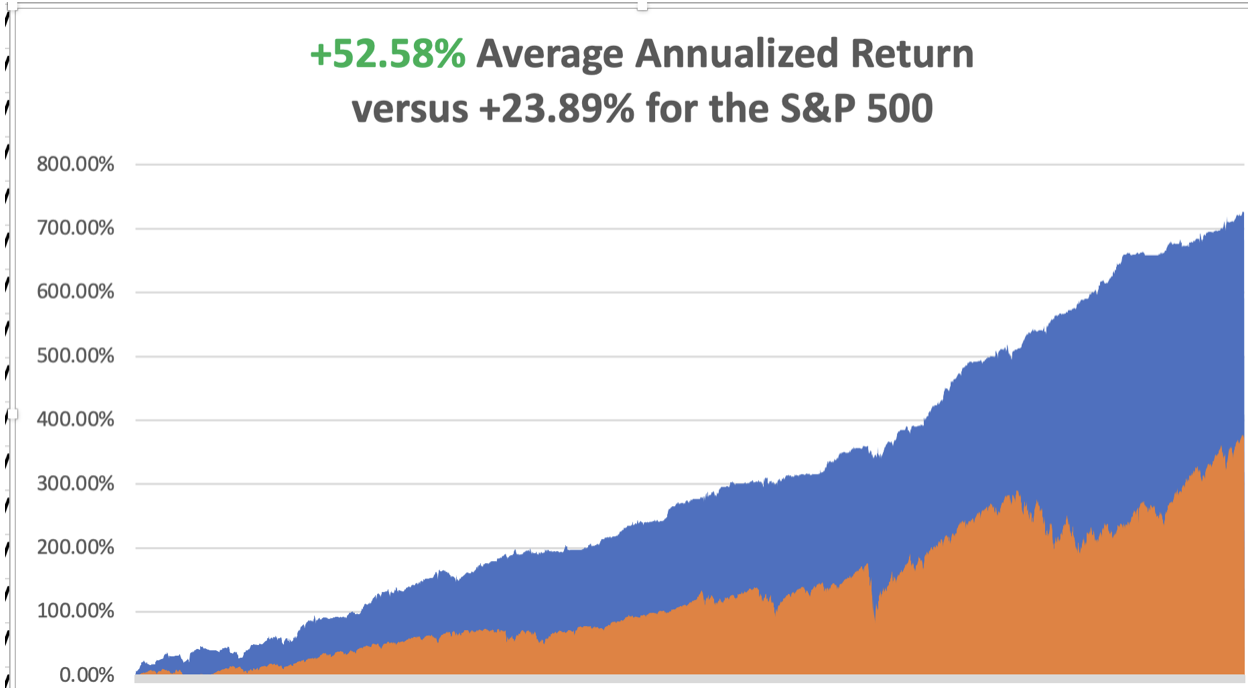

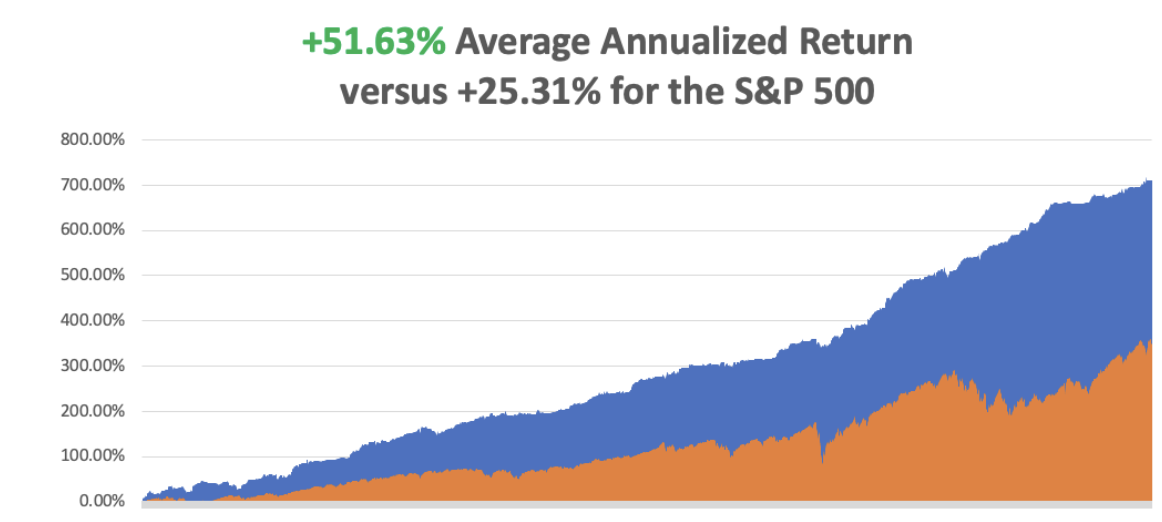

So far in October, we have gained a breathtaking +5.46%.My 2024 year-to-date performance is at an amazing+50.70%.The S&P 500 (SPY) is up +21.38%so far in 2024. My trailing one-year return reached a nosebleed +66.31. That brings my 16-year total return to +727.33%.My average annualized return has recovered to +52.58%.

I am remaining cautious with a 70% cash, a 20% long, and a 10% short. I maintained two longs in (GLD) and (JPM) that are well in the money. I sold short (TSLA) to take advantage of a massive 29% gain in two days off the back of blockbuster earnings.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 61 of 81 trades have been profitable so far in 2024, and several of those losses were really break evens. Some 16 out of the last 19 trade alerts were profitable. That is a success rate of +75.30%.

Try beating that anywhere.

New Home Sales Jumped 4.1% in September at 738,000 seasonally adjusted units on a signed contract basis. The median home price rose to 426,300. This despite a roller coaster month on interest rates, falling to 6.0% for the 30-year, then jumping back up to 7.0%.

Fusion is going Commercial in San Francisco, with a German company, Focused Energy, making a $65 million investment. The firm will draw heavily from staff from nearby Lawrence Livermore National Labs, which achieved a net energy gain for the first time in 2022. Focused Energy is one of eight companies given grants to accommodate a doubling of power demand by 2050. Commercial fusion will be the next big thing, where three soda cans of heavy hydrogen can power San Francisco for a day.

Money Market Funds See Massive Pre-Election Inflows, as investors see to avoid promised post-election violence. According to LSEG data, investors acquired a net $29.98 billion worth of money market funds during the week, posting their fourth weekly net purchase in five weeks. Personally, I think it is another Y2K moment.

Tesla Earnings Shock to the Upside, with both third-quarter profits and margins topping estimates. Elon Musk said that he expects 20% to 30% vehicle growth next year, sending the company's shares up 11% in post-market trading. The company still sees 2025 production of a cheaper model, maybe the Model 2. The Cybertruck has reached profitability for the first time and is reaching mass production. Tesla will see “slight growth” in deliveries this year. I am using the spike in the share price to take profits on my long to avoid election risk.

Apple iPhone Sales are Lagging, according to a leading analyst, with a drop in 10 million orders expected, down to 84 million units. The stock dropped 4% from an all-time high.

Boeing Reports $6 Billion Loss, a disastrous report from a dying company with awful management. This is going to be a very long-term workout. A strike resolution may market the bottom. Avoid (BAC) like a stalling airplane.

Newmont Mining Dives 7% after missing Wall Street expectations for third-quarter profit on Wednesday. Higher costs and lower production in Nevada took the shine away from a rise in total output. Newmont said that its costs rose due to planned maintenance at the Lihir project in Papua New Guinea — which it acquired following a $17 billion buyout of Newcrest — and higher expenditure for contract services across its portfolio. Buy (NEM) on dips.

McDonald's Kills Two in E.Coli Outbreak, linked to quarter pounders sold in Colorado and Nebraska. The stock dropped 10%. It’s clearly a supply chain problem. Given their vast size, with 45,000 stands in 100 countries, it’s amazing that this doesn’t happen more often. Avoid (MCD).

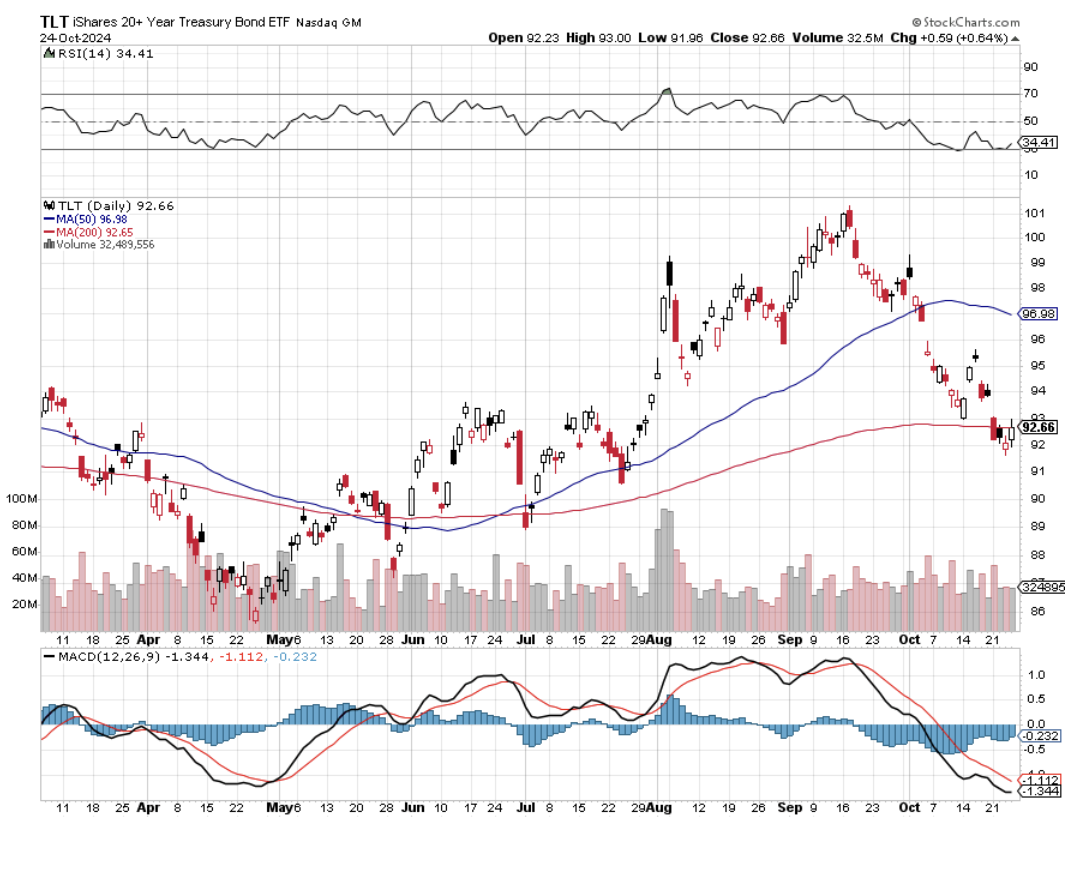

Bonds Plunge Anticipating a Trump Win, with the (TLT) down $10 from the recent high. If he does win, expect another $10 decline to $82. If Harris wins, expect a $10 rally. This is the best election trade out there.

Nvidia Tops $3.5 Trillion, as the shares hit a new all-time high at $144.45. It looks like it’s on a run to $150, then $160. Earnings are about to double when reported on November 20. Before then, investors will get some insight into demand for Nvidia’s newest Blackwell chips with earnings reports from big technology companies, including Microsoft (MSFT) coming at the end of this month. Buy (NVDA) on dips.

Hedge Funds Pour into Technology Stocks, such as semiconductors and hardware, at the fastest in five months amid the start of the third-quarter earnings season, according to Goldman Sachs on Friday. Outside the U.S., diverging reports from chipmaker Taiwan Semiconductor Manufacturing (TSM) and chipmaking equipment supplier ASML Holding (ASML) in opposite directions while investors await semiconductor companies such as Advanced Micro Devices (AMD) and Nvidia (NVDA) to unveil their earnings as they seek a trend. They are betting on a big post-election move-up.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000, here we come!

On Monday, October 28 at 8:30 AM EST, the Dallas Fed Manufacturing Index is published. On Tuesday, October 29 at 6:00 AM, the S&P Case Shiller National Home Price Index is out. We also get the US JOLTS Job Openings Report. Alphabet (GOOGL) and (AMD) report.

On Wednesday, October 30 at 11:00 AM, the ADP Employment Change Report is printed. (META) and (MSFT) report.

On Thursday, October 31 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the US Core PCE Price Index. (AMZN) reports.

On Friday, November 1 at 8:30 AM, the October Nonfarm Payroll Report is announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with silver on fire once again and at 12-year highs, I thought I’d recall the last time a bubble popped for the white metal. I picked up this story from my late friend Mike Robertson, who ran the Dallas-based Robertson Wealth Management, one of the largest and most successful registered investment advisors in the country.

Mike is the last surviving silver broker to the Hunt Brothers, who in 1979-80 were major players in the run-up in the “poor man’s gold” from $11 to a staggering $50 an ounce in a very short time. At the peak, their aggregate position was thought to exceed 100 million ounces.

Nelson Bunker Hunt and William Herbert Hunt were the sons of the legendary HL Hunt, one of the original East Texas wildcatters and heirs to one of the largest Texas fortunes of the day. Shortly after President Richard Nixon took the US off the gold standard in 1971, the two brothers became deeply concerned about financial viability of the United States government. To protect their assets, they began accumulating silver through coins, bars, the silver refiner, Asarco, and even tea sets, and when it opened, silver contracts on the futures markets.

The brother’s interest in silver was well-known for years, and prices gradually rose. But when inflation soared into double digits, a giant spotlight was thrown upon them, and the race was on. Mike was then a junior broker at the Houston office of Bache & Co., in which the Hunts held a minority stake and handled a large part of their business.The turnover in silver contracts exploded. Mike confesses to waking up some mornings, turning on the radio to hear silver limit up, and then not bothering to go to work because they knew there would be no trades.

The price of silver ran up so high that it became a political problem. Several officials at the CFTC were rumored to be getting killed in their personal silver shorts. Eastman Kodak (EK), whose black and white film made them one of the largest silver consumers in the country, was thought to be borrowing silver from the Treasury to stay in business.

The Carter administration took a dim view of the Hunt Brothers’ activities, especially considering their funding of the ultra-conservative John Birch Society. The Feds viewed it as an attempt to undermine the US government. The proverbial sushi hit the fan.

The CFTC raised margin rates to 100%. The Hunts were accused of market manipulation and ordered to unwind their position. They were subpoenaed by Congress to testify about their motives. After a decade of litigation, Bunker received a lifetime ban from the commodities markets, a $10 million fine, and was forced into a Chapter 11 bankruptcy.

Mike saw commissions worth $14 million in today’s money go unpaid. In the end, he was only left with a Rolex watch, his broker’s license, and a silver Mercedes. He still ardently believes today that the Hunts got a raw deal and that their only crime was to be right about the long-term attractiveness of silver as an inflation hedge. Nelson made one of the greatest asset allocation calls of all time and was punished severely for it. There never was any intention to manipulate markets. As far as he knew, the Hunts never paid more than the $20 handle for silver and that all of the buying that took it up to $50 was nothing more than retail froth.

Through the lens of 20/20 hindsight, Mike views the entire experience as a morality tale, a warning of what happens when you step on the toes of the wrong people.

The white metal’s inflation-fighting qualities are still as true as ever, and it is only a matter of time before prices once again take another run to the upside.

Unfortunately, Mike won’t be participating in the next silver bubble. Suffering from morbid obesity, he died from a heart attack a decade ago.

Silver is Still a Great Inflation Hedge

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/10/man-with-glasses.png606468april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-28 09:02:442024-10-28 11:23:59The Market Outlook for the Week Ahead, or Here is your Post Election Portfolio

Below, please find subscribers’ Q&A for the October 23 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: What the heck is happening with the iShares 20+ Year Treasury Bond ETF (TLT)? It keeps dropping even though interest rates are dropping. It seems to be an anomaly.

A: It is. What’s happening is that bonds are discounting a Trump win, and Trump has promised economic policies that will increase the national debt by anywhere from $10 to $15 trillion. Bonds don’t like that—you borrow more money through bonds, and the price goes up. Interest rates could go as high as 10% if we run deficits that high (at least the bond market may go that low.) On the other hand, stocks are discounting a Harris win. Stocks went up 60% over the last four years. I did roughly double that. And a Harris win would mean basically four more years of the same. So stocks have been trading at new all-time highs almost every day until this week when the election got so close that the cautious money is running to the sidelines. So what happens if there's a Harris win?Bonds make back the entire 10 points they lost since the Fed cut interest rates. And what happens if Trump wins? Bonds lose another 10 points on top of the 10 points they've already lost. Someone with a proven history of default doesn't exactly inspire confidence in the bond market. So that is what's going on in the bond market.

Q: Will the US dollar continue its run into year-end?

A: No, I have a feeling it’s going to completely reverse in two weeks and, give up all of its gains, and resume a decade-long trend to new lows. So, I think everything reverses after election day. Stocks, bonds, commodities, precious metals—the only thing that doesn't is energy, and that keeps going down because of global oversupply that even a Middle Eastern war can’t support.

Q: Are you expecting a major correction in 2025?

A: I am, actually. We basically postponed all corrections into 2025 and pulled forward all performance in 2024. So, I think we could get at least a 10% correction sometime next year, and that is normal. Usually, we get a couple of them. This year, we only got the one in July/August. So, back to normal next year, which means smaller returns from the stock market. In fact, smaller returns from everything except maybe gold and silver. This is why they're going up so much now.

Q: Are you discounting a huge increase in the deficit under Biden-Harris?

A: No, the huge increase in the deficit is behind us because we had all the pandemic programs to pay for, and if anything, technology inflation should go down because of accelerating technology. We're already seeing that in many industries now, so I don't think there'll be any policy changes under Harris, except for little tweaks here and there. All the big policies will remain the same.

Q: What is a dip?

A: A dip is different for every stock and every asset class. It depends on the recent volatility of the underlying instrument. You know, a dip in something like McDonald's (MCD) or Berkshire Hathaway (BRK/B) might be 5%, and a dip in Nvidia (NVDA) might be 15 or 20%. So, it really depends on the volatility of the underlying stock, and no two volatilities are alike.

Q: What are your top picks on nuclear?

A: Well, we've been in Cameco (CCJ), the Canadian uranium company, since the beginning of the year, and it has doubled. Vistra Corp (VST) is another one, and there are many more names after that.

Q: What are your thoughts on Toyota (TM)?

A: I love Toyota for the long term. The fact that they were late into EVs is now a positive since the EV business is losing money like crazy. They're the ones who really pioneered the hybrid business, and I’ve toured many of their factories in Japan over the years. Great company, but right now, they're being held back by the slow growth of the Japanese economy.

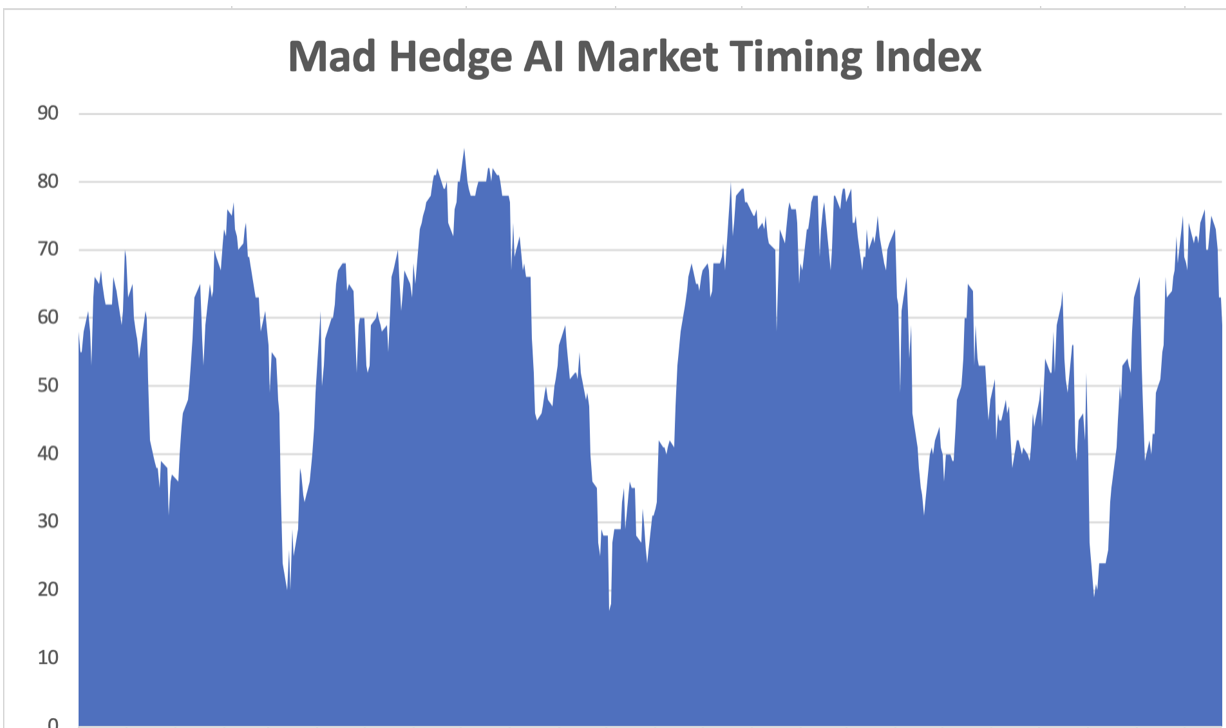

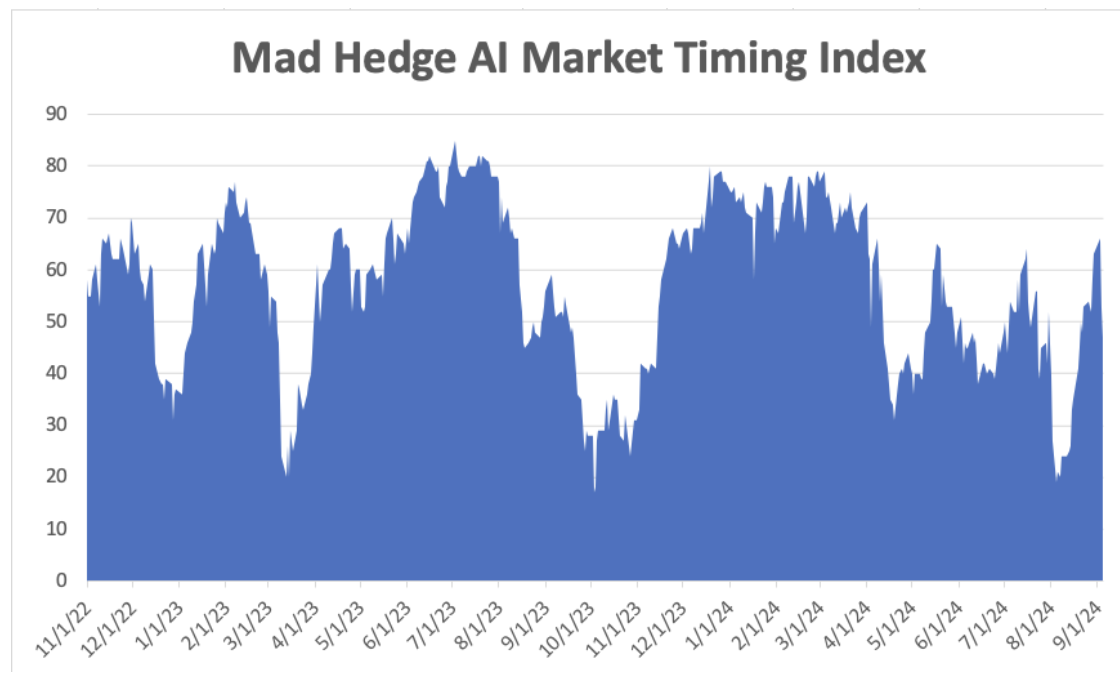

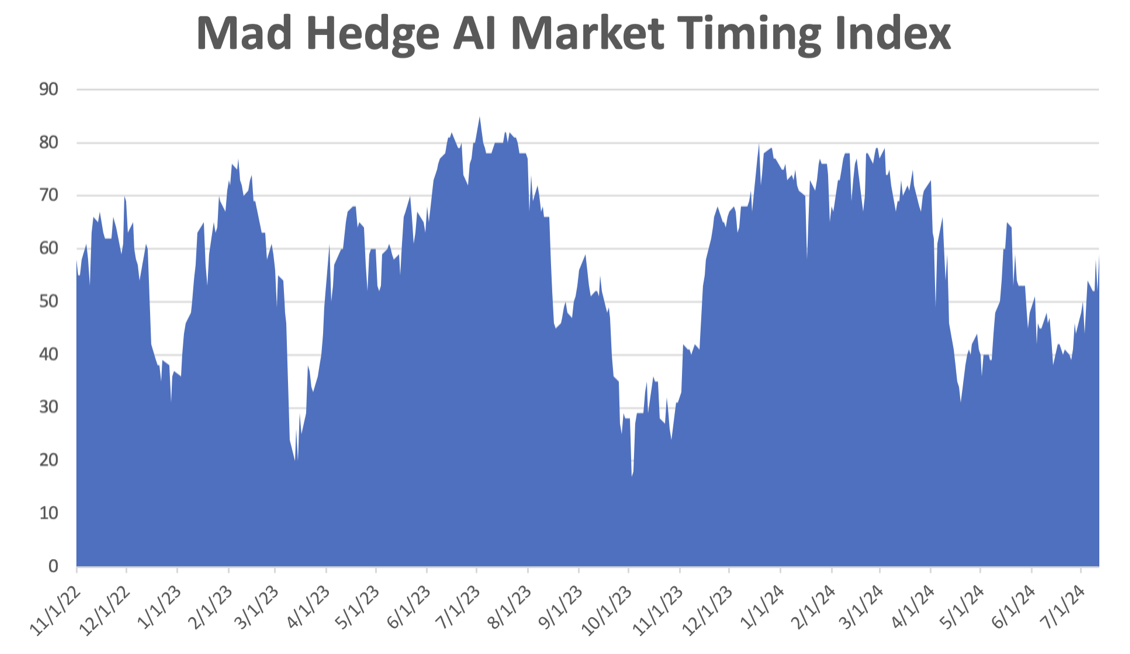

Q: Market timing index says get out. We're heading into the seasonally bullish time of the year. Should we be in or out over the next two months?

A: I would be in as long as you can handle some volatility around the stock market. When the market timing index is at 70, that means any new trades that you initiate have a 30% chance of making money. Now, they can sit at highs sometimes for months, and it actually did that earlier this year. Markets can get overbought and stay overbought for months, and that is a really difficult time to trade. If you're a long-term investor, you just ignore all of this and just stay in all the time.

Q: Silver has broken out; what's next?

A: Silver had had a massive run since the beginning of September—some 30%. We're up to about $31/oz. The obvious target for silver is the last all-time high, which I think we did 40 years ago, and that was at $50/oz. So there's another easy 60% of upside in silver. That's why I put out a LEAPS on the 2x long silver play (AGQ), and people are already making tons of money on that one. I think Silver will be your big performer going forward.

Q: Too late to invest in Chinese stocks?

A: No, it's selling off again. IT Could retest the lows, especially if the government sits on its hands for too long with more stimulus packages.

Q: Is big tech still a good bargain buy?

A: I would take “bargain” out of that. The rule on tech investing is you're always buying expensive stuff because the future always has a spectacular outlook. So, tech investing is all about buying something expensive that gets more expensive. This is exactly what tech stocks have been doing for the last 50 years, so it's not exactly a new concept. I know tons of people who never touched Nvidia (NVDA) or Tesla (TSLA) because it was too expensive. (NVDA) was too expensive when it was $2, and now it's even more expensive at $140 or, in Tesla's case, $260.

Q: Will Tesla (TSLA) go up or down tonight?

A: I have no idea. Anybody else who says they have an idea is lying. You go to timeframes that short, and you are subjecting yourself to random chance; even the weather could affect your position by tomorrow.

Q: How uncomfortable is the stem cell extraction?

A: Extremely uncomfortable. If they say it won't hurt a bit, don't believe them for a second. They take this giant needle hammer it into your backbone to get your spinal fluid (and I count the hammer blows.)Last time, I think I got up to 50 before I couldn't take the pain anymore, and they extracted the spinal fluid to get the stem cells. So, for those who don't tolerate pain very well, this is absolutely not for you.

Q: Why is Intel (INTC) stock doing so badly this year?

A: Low-end products, no new products, poor manager. Whenever a salesman takes over a technology company, you want to run a mile. That's what happened at Intel because they have no idea how the technology works.

Q: Should I sell my Philip Morris (PM) stock? It's just had a huge run-up.

A: No. For dividend holders, this is the dream come true. They pay a 4.1% dividend. This was a pure dividend play ever since the tobacco settlement was done 40 years ago. Then they bought a Swedish company that has these things called tobacco pouches, and that has been a runaway bestseller. So, all of a sudden, the earnings at Philip Morris are exploding. The dividend is safe. I think Philip could go a lot higher, so buy PM on dips. And I will dig into this story and try to get some more information out of it. I love high growth high dividend plays.

Q: What's the best play for silver?

A: I'm doing the ProShares Ultra Silver (AGQ), which is a 2x long silver and has gone from $30 to $50 since the beginning of September. If you want to sleep at night (of course, I don't need to), then you just buy the iShares Silver Trust (SLV), which is a 1x long silver play and that owns physical silver. I think it's held in a bank vault in London.

Q: Time to sell Copper (FCX)?

A: Short term, yes, as China weakens. Long-term, hang on because we are coming into a global copper shortage, and that'll take the price of copper up to $100 or (FCX) up to $100. So yes, love (FCX) for the long term. Short term, it has a China drag.

Q: Will inflation come back in 2025?

A: No, it won't. Technology is accelerating so fast, and AI is accelerating so fast it's going to cut costs at a tremendous rate. And that's why you're seeing these big tech companies laying off people hundreds at a time; it's because the low-end jobs have already been replaced by AI. There is a lot more of that to come. I'm not worried about inflation at all.

Q: Do you disagree with Tudor Jones on inflation?

A: Yes, I disagree with him heartily. Tudor Jones is talking his own book, which means he doesn't want to get a tax increase with a Harris administration. So he's doing everything he can to talk up Trump, and that isn't helping me with my investment strategy whatsoever. By the way, Tudor Jones is often wrong, you know; he made most of his money 30 years ago. And before that, it was when he was working for George Soros. So, yes, I agree with the man from Memphis. He’s in the asset protection business. You’re in the wealth creation business, a completely different kettle of fish.

Q: Do you hold the ProShares Ultra Silver (AGQ) overnight?

A: I've been holding my (AG for four months, and the cost of carry-on that is actually quite low because silver doesn't pay any dividend or interest. There really isn't much of a contango in the precious metals anyway—it's not like oil or natural gas. It’s a 3X plays that you really shouldn’t hold overnight.

Q: Where is biotech headed?

A: Up for the long term, sideways for the short term. That's because, after the election, risk on will go crazy. We could have a melt-up in stocks, and when that happens, people don't want to buy “flight to safety” sectors like Biotechs and healthcare; they want to buy more Nvidia. Basically, that's what happens. More Nvidia (NVDA), more Meta (META), and more Apple (APPL). They want to buy all the Mag7 winners. Well, let's call them the Mag7 survivors, which are still going up after a ballistic year.

Q: Any suggestions on where to park cash for five to six years?

A: 90-day T-Bills are yielding 4.75%. That would be a safe place to put it. And you might even peel off a little bit of that—maybe 10% — and put that into a junk fund, which is yielding 6%. You're still getting a lot of money for cash—but not for much longer. The golden age of the 90-day T-bill is about to end.

Q: BlackRock (BLK) keeps growing, trillions after trillions. Why is the stock so great at building value?

A: Because you get a hockey stick effect on the earnings. As the stock market goes up, which it always does over time, their fees go up. Plus, their own marketing brings in new money. So, you have multiple sources of income rising at a rapid pace. I'm kicking myself for not buying the stock earlier this year.

Q: How does any antitrust action by the government affect stock prices?

A: Short-term, it caps them. Long term, it doubles them because when you break up these big companies, the individual pieces are always worth a lot more than the whole. We saw that with AT&T (T), where you're able to sell the individual seven pieces for really high premiums. So, that's why I'm never worried about antitrust.

Q: Do dividend stocks provide little upward appreciation since they're paying investors already?

A: To some extent, that's true because low-growth companies like formerly Philip Morris (PM) and Altria (MO) had to pay high dividends to get people to buy their stock because the industries were not growing. AT&T is another classic example of that—high dividend, no growth. But that does set you up for when a no-growth company can become a high-growth company, and then the stocks double practically overnight. And that's what's happening with Philip Morris.

Q: Are you buying physical gold (GLD) and silver (SLV)?

A: I bought some in the 1970s when it was $34/oz for gold, and the US went off the gold standard, and I still have them. It's sitting in a safe deposit box in a bank I will not mention. The trouble with physical gold is high transaction costs—it costs you about 10% or more to buy and sell. It can be easily stolen—people who keep them hidden at home or have safes at home regularly get robbed. And what if the house burns down? You really can't insure gold holdings accept with very high premiums. So, I've always been happy buying the gold ETFs. The tracking error is very small unless you get into the two Xs and three Xs. Gold coins are good for giving kids as graduation presents—stuff like that. I still have my gold coins for my graduation a million years ago (and that was a really great investment! $34 up to, you know, $2,700.)

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

One of my Concierge clients holds a weekly staff meeting. Each employee is told his family is being held hostage and can only be rescued if they recommend the top-performing stock for the coming week. Then everyone throws in their two cents worth.

Last week, for the first time in the company’s history, no one could come up with a single name, even if it meant sacrificing their family (nobody was really sacrificed).

That speaks volumes.

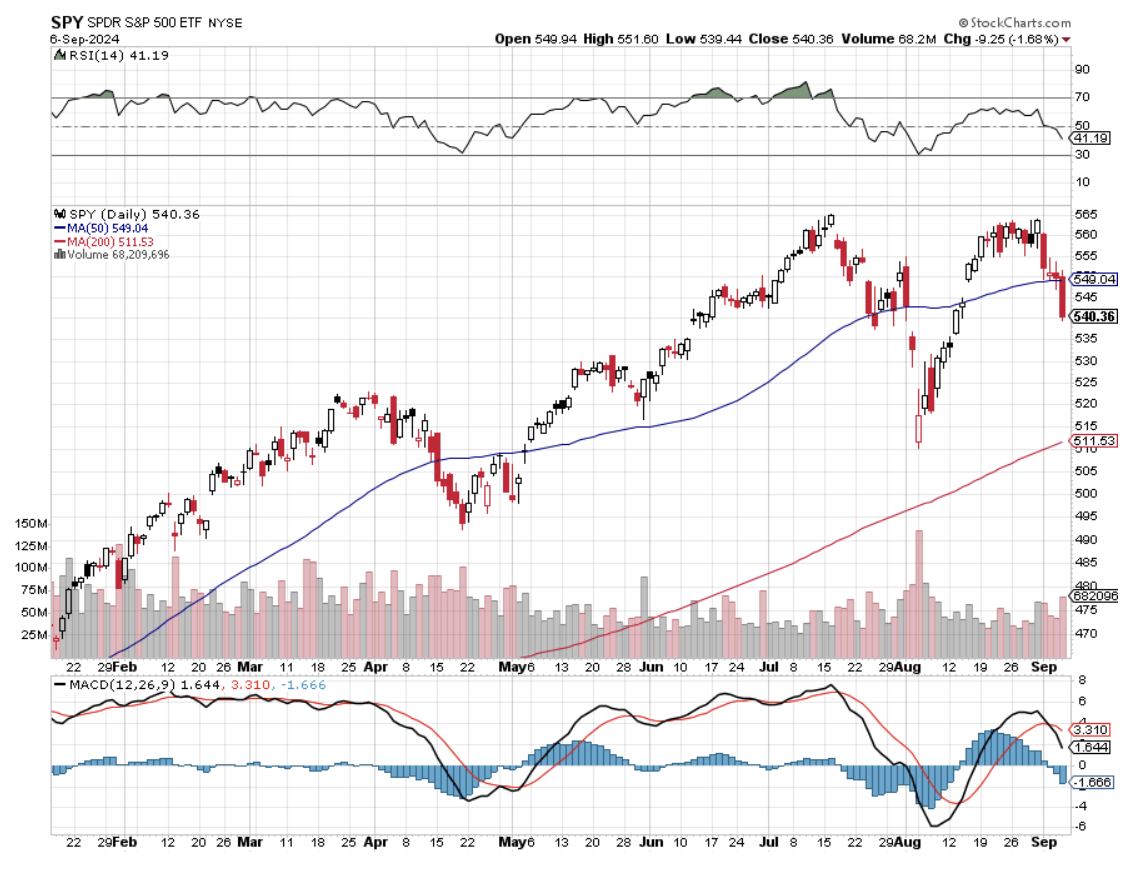

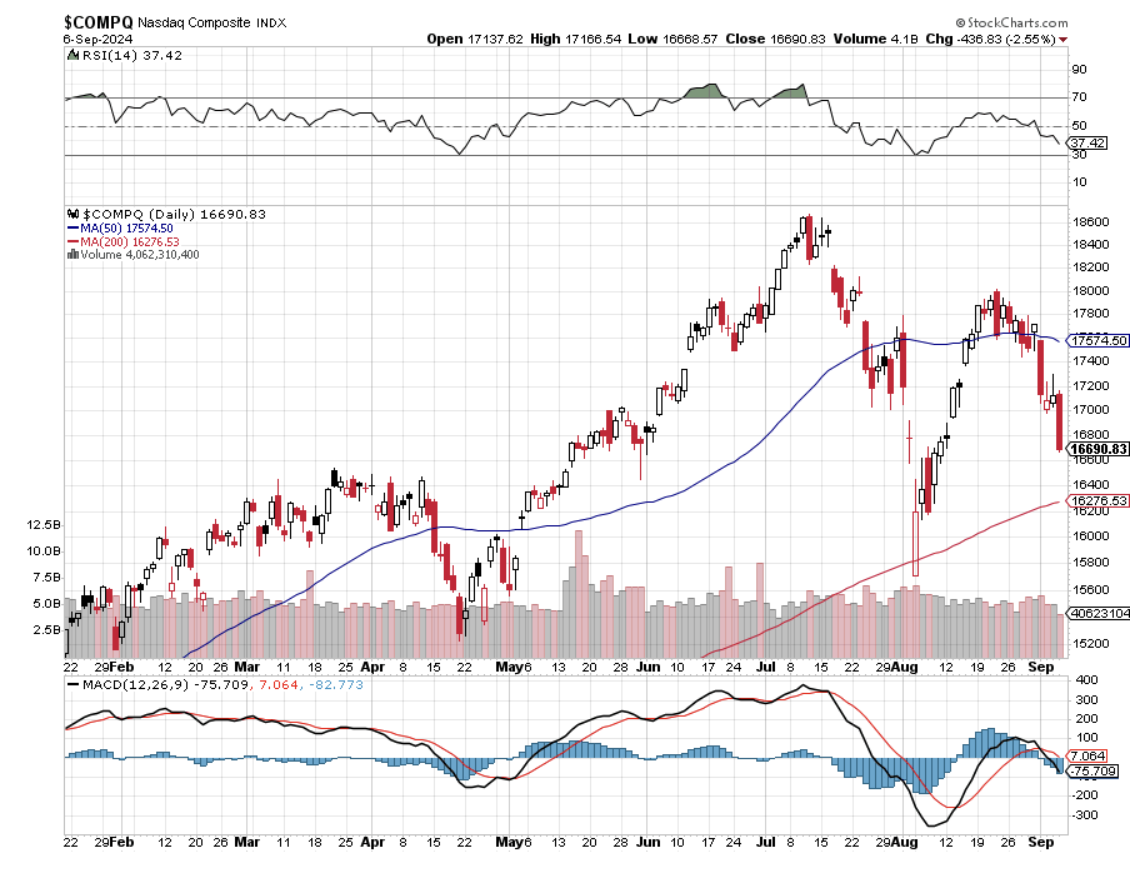

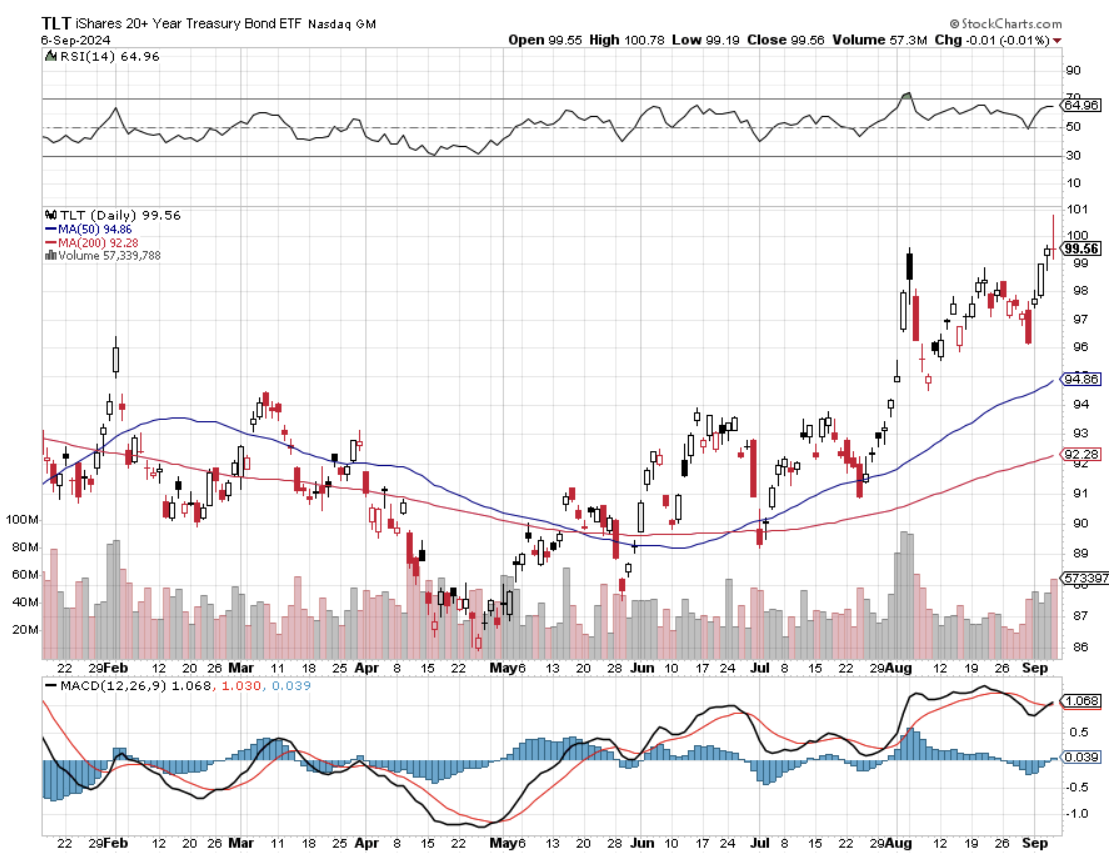

In fact, until last week, every asset class in the market was discounting an imminent recession: Commodities(COPX), energy (USO), real estate (ARE), and the US dollar (UUP). Reliable recession hideouts like bonds (TLT), fixed income (JNK), and gold (GLD) caught an endless bid. Only the stock market (SPY), (NASD) wasn’t reading from the same music sheet.

Well, stocks finally got the memo, delivering the worst week in 2 ½ years. Suddenly, the glass has gone from half full to half empty. Permabears have suddenly morphed from complete idiots to maybe having something to say. Here it is only September 9 and the Month from Hell is already living up to its awful reputation. Is the stock market the slow learner in the bunch?

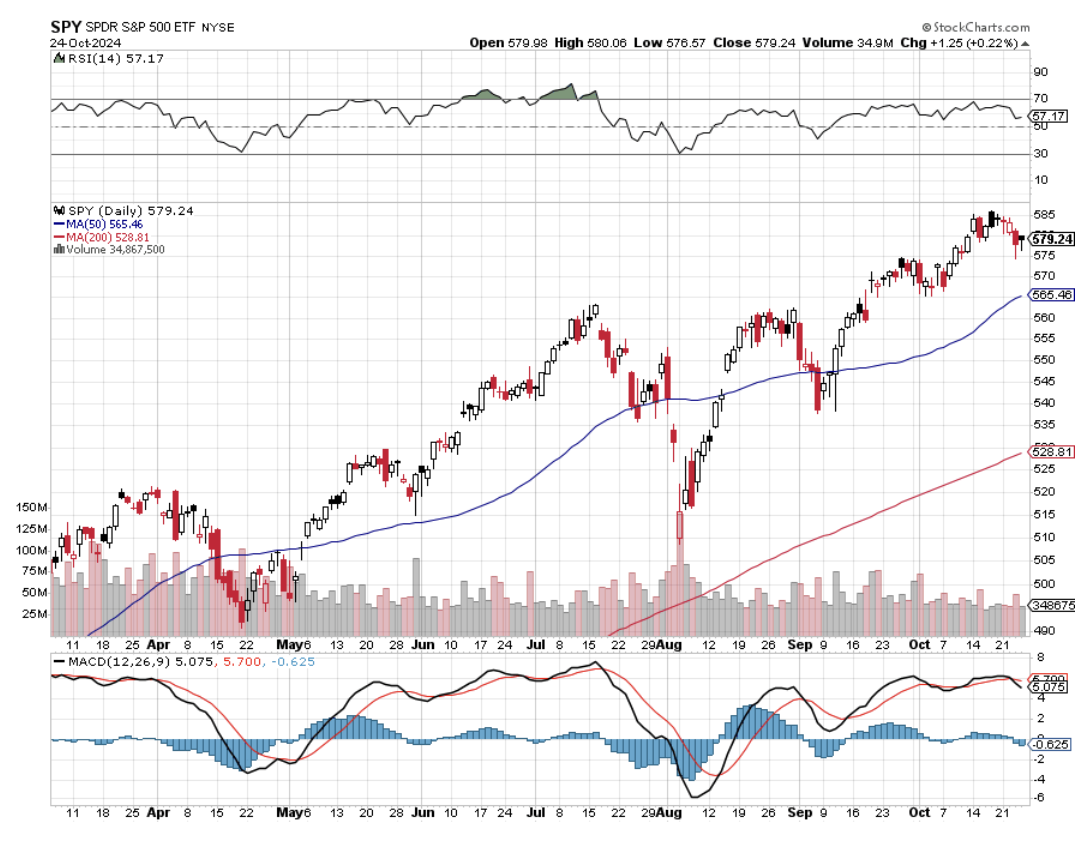

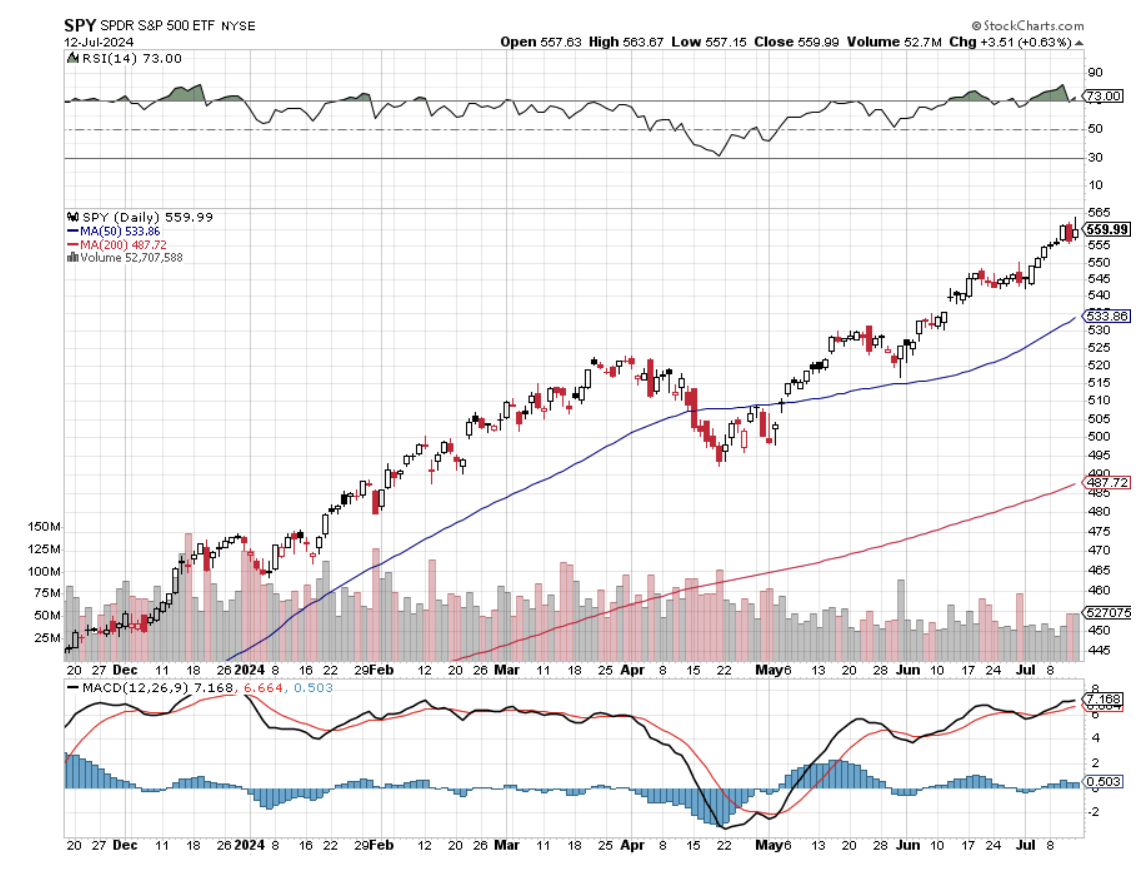

I came back from Europe in August rested, refreshed, invigorated, and in a near state of panic. The last 11% rally in the (SPY) made absolutely no sense to me whatsoever. Either the September jobs data would come in hot, canceling the Fed’s expected interest rate cut. Or, the data would come in cold, proving that the Fed waited too long to cut rates and inviting a recession, causing stocks to tank.

It would have been one of the worst self-inflicted wounds and own goals of all time.

What was especially dangerous was that we were going into the worth trading month of the year, September, with the (SPY) showing a crystal-clear double top on the charts.

It was a perfect lose/lose situation.

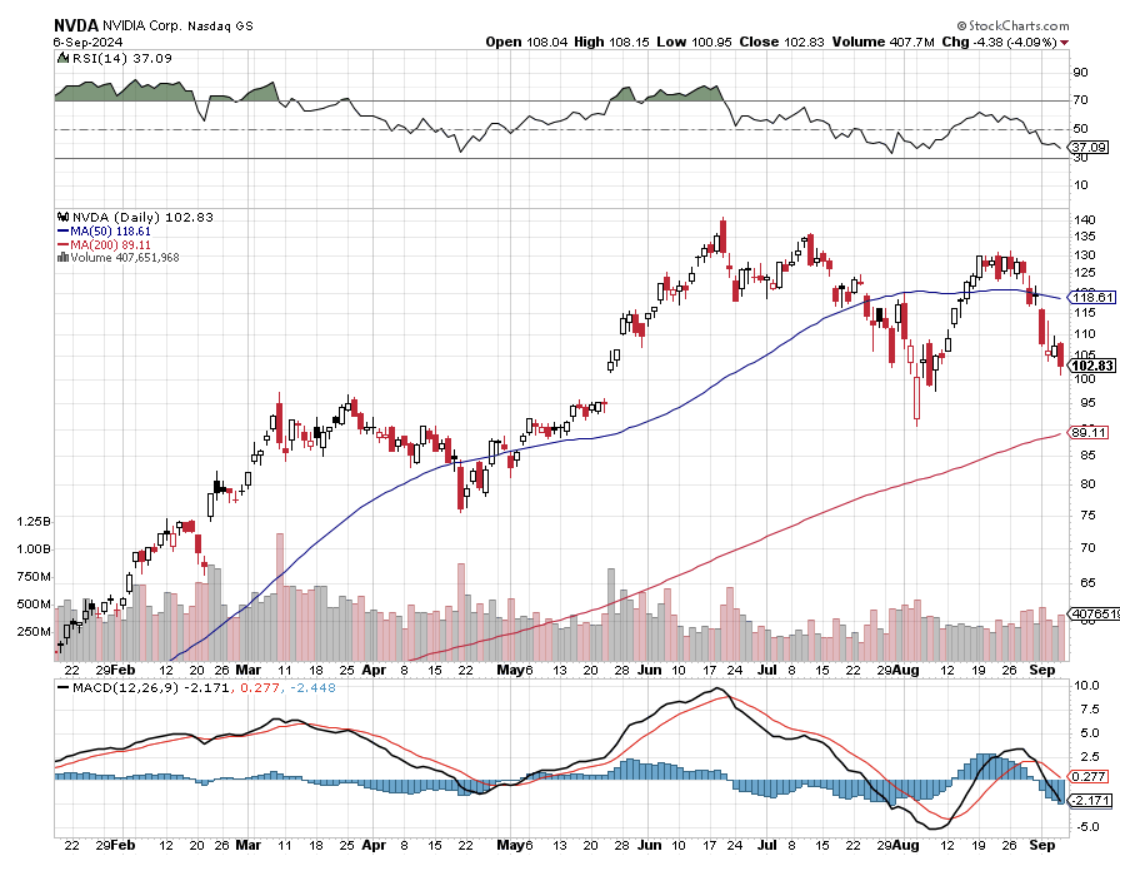

Seasonals are important, especially this month. This is because most mutual funds run an annual year that ends on September 30. To window dress their books and those glossy marketing brochures, they sell all their losers (think energy) in September and use the cash to buy more of their winners in October. (NVDA) yes, (XOM) not so much. This creates a swing in the indexes every year of 10%-20%.

To learn more about the seasonals, read tomorrow’s letter in detail, IF YOU SELL IN MAY AND GO AWAY, WHAT TO DO IN SEPTEMBER?

So I did what I usually do when the market refuses to give me marching orders. I let all my positions expire with the August 16 options expiration, took back the cash, and then sat on my hands. Suddenly, a 100% cash position was looking like a stroke of genius. It cleared the cobwebs, moved the fog away from my eyes, and took the monkey off my back all in one fell swoop.

And you know what? After surveying my big hedge fund clients, I learned they were doing exactly the same thing.

Let me pass on another piece of interesting intel. All of the many algorithms the hedge fund industry follows are bunching up around two specific bottoms for the stock market in coming months: September 18, the Fed rate cut day, and October 22, two weeks before the presidential election.

With any luck, other classic “BUY” signals will kick in at the same time with the Mad Hedge Market Timing Index below 20 by then and the Volatility Index ($VIX) over $30. It could be the best entry point of the year.

What has been fascinating is how much money has been pouring into the interest rate plays I have been banging the table about for the last six months. When was the last time the stock market has been led by AT&T (T), Altria (MO), and Crown Castle International (CCI)? You might have to look behind the radiator to find some old, dusty research on these names.

So far in September, we are down by -1.21%.My 2024 year-to-date performance is at +33.49%.The S&P 500 (SPY) is up +13%so far in 2024. My trailing one-year return reached +51.89. That brings my 16-year total return to +710.12.My average annualized return has recovered to +51.63%.

I executed only one trade last week, covering a short in Tesla at cost. I am now maintaining a 100% cash position. I’ll text you next time I see a bargain in any market. Now there is none. There is no law dictating that you have to have a position every day of the year. Only your broker wants you to trade every day.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 47 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of +72.24%.

Try beating that anywhere.

Nonfarm Payroll Report Fades at 142,000, but the Headline Unemployment Rate stays at 4.2%. More shocking is that the previous two months saw substantial downward revisions. The BLS cut July’s total by 25,000, while June fell to 118,000, a downward revision of 61,000. If the Fed doesn’t cut by 0.50% on September 18, the stock market will crash. Broadcom Beats and Stock Tanks driven by strong sales of its AI products and VMware software. But management’s guidance for the current quarter disappointed investors, sending shares of the chipmaker down nearly 7% in the after-market. This is too harsh of a reaction to an otherwise solid print. Buy (AVGO) on dips. ADP Employment Change Report Hits 3 ½-Year Low, up only 99,000 in August. Economists polled had forecast private employment would advance by 145,000 positions after a previously reported gain of 122,000.

Biden Blocks Nippon Steel Takeover of US Steel, no doubt to save the jobs these deals usually destroy. Good thing we got out of the (X) LEAPS a year ago at max profit. (X) dropped 20% on the news. Not a good time to concentrate on industry.

No Subpoenas Here Says NVIDIA, refuting rumors that it was the target of an antitrust action. Don’t believe everything you read on the internet. The Yield Curve has De-Inverted, meaning that short-term interest rates have fallen below long-term ones. Two-year interest rates at 3.72% are now 0.03% lower than ten-year ones at 3.75%. It’s a clear signal to the Fed that rates must be cut soon. Weekly Jobless Claims Drop 5,000 to 227,000. The weekly jobless claims report from the Labor Department on Thursday, the most timely data on the economy's health, also showed unemployment rolls shrinking to levels last seen in mid-June. It reduces the urgency for the Federal Reserve to deliver a 50-basis points interest rate cut this month.

US Oil Production Hits All-Time High. In August 2024, U.S. oil production hit a record 13.4 million barrels per day according to the U.S. Energy Information Administration. Big Oil has become more productive as horizontal drilling and hydraulic fracturing, which is also known as fracking, have seen technological breakthroughs. The fossil fuel industry benefits from tax incentives, such as the intangible drilling costs tax credit, that are built into the tax code. The intangible drilling costs tax break is expected to benefit oil and gas companies by $1.7 billion in 2025 and $9.7 billion through 2034

Crude Oil Now Down on the Year, after a precipitous weekend selloff. Blame a weak China, lost OPEC discipline, and overproduction by Iraq. The bearish Goldman Sachs commodities report was also a factor. Avoid the worst-performing asset class in the market. Eli Lilly is now a trillion-dollar stock, the first Biotech to do so. The drug giant is riding the wave of Mounjaro and Zepbound, its blockbuster injectable GLP-1 medications for weight loss. The drugs are also used to treat diabetes and cardiovascular disease. Eli Lilly’s shares have soared 65% this year.

Goldman Goes Big on Gold. Central banks in emerging market countries are continuing to buy gold — with purchases tripling since the middle of 2022 amid fears of U.S. financial sanctions and a mountain of sovereign debt. Goldman is taking a more selective approach to commodity investing as soft demand in China weighs on crude oil and copper prices. The investment bank has slashed its Brent oil outlook by $5 to a range of $70 to $85 per barrel and delayed its copper target of $12,000 per metric ton until after 2025.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 9 at 3:00 PM EST, Consumer Inflation Expectations are out On Tuesday, September 10 at 6:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, September 11 at 7:30 AM, the Core CPI is printed.

On Thursday, September 12 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, September 13 at 8:30 AM, the University of Michigan Consumer Sentiment. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I was having lunch at the Paris France casino in Las Vegas at Mon Ami Gabi, one of the top ten-grossing restaurants in the United States. My usual waiter, Pierre from Bordeaux, took care of me with his typical ebullient way, graciously letting me practice my rusty French.

As I finished an excellent, but calorie packed breakfast (eggs Benedict, caramelized bacon, hash browns, and a café au lait), I noticed an elderly couple sitting at the table next to me. Easily in their 80s, they were dressed to the nines and out on the town.

I told them I wanted to be like them when I grew up.

Then I asked when they first went to Paris, expecting a date sometime after WWII. The gentleman responded, “Seven years ago.”

And what brought them to France?

“My father is buried there. He’s at the American Military Cemetery at Colleville-sur-Mer along with 9,386 other Americans. He died on Omaha Beach on D-Day. I went for the D-Day 70th anniversary.” He also mentioned that he never met his dad, as he was killed in action weeks after he was born.

I reeled with the possibilities. First, I mentioned that I participated in the 40-year D-Day anniversary with my uncle, Medal of Honor winner Mitchell Paige, and met with President Ronald Reagan.

We joined the RAF fly-past in my own private plane and flew low over the invasion beaches at 200 feet, spotting the remaining bunkers and the rusted-out remains of the once floating pier. Pont du Hoc is a sight to behold from above, pockmarked with shell craters like the moon. When we landed at a nearby airport, I taxied over railroad tracks that were the launch site for the German V1 “buzzbomb” rockets.

D-Day was a close-run thing and was nearly lost. Only the determination of individual American soldiers saved the day. The US Navy helped too, bringing destroyers right to the shoreline to pummel the German defenses with their five-inch guns. Eventually, battleships working in concert with very lightweight Stinson L5 spotter planes made sure that anything the Germans brought to within 20 miles of the coast was destroyed.

Then the gentleman noticed the gold Marine Corps pin on my lapel and volunteered that he had been with the Third Marine Division in Vietnam. I replied that my father had been with the Third Marine Division during WWII at Bougainville and Guadalcanal and that I had been with the Third Marine Air Wing during Desert Storm.

I also informed him that I had led an expedition to Guadalcanal two years ago looking for some of the 400 Marines still missing in action. We found 30 dog tags and sent them to the Marine Historical Division at Quantico, Virginia for tracing. I proudly showed them my pictures.

When the stories came back it, turned out that many survivors were children now in their 80s who had never met their fathers because they were killed in action on Guadalcanal.

Small world.

I didn’t want to infringe any further on their fine morning out, so I excused myself. He said Semper Fi, the Marine Corps motto, thanked me for my service, and gave me a fist pump and a smile. I responded in kind and made my way home.

Oh and say “Hi” when you visit Mon Ami Gabi. Tell Pierre that John Thomas sent you and give him a big tip. It’s not easy for a Frenchman to cater to all these loud Americans.

Third Marine Air Wing

The D-Day Couple

The American Military Cemetery at Colleville-sur-Mer

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/09/d-day-couple.png8201096april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-09 09:02:592024-09-09 11:16:00The Market Outlook for the Week Ahead, or September Lives Up to its Reputation

(MARKET OUTLOOK FOR THE WEEK AHEAD or THE HIDDEN AI IN YOUR LIFE),

(SPX), (NVDA), (CSCO), (LEN), (DHI), (KBH), (SMCI), (BRK/B), (META), (AAPL), (GOOGL), (TSLA), (JNK), (HYG), (FXA), (FXE), (FXB), (FXC), (EEM), (IWM)

It's great to be back in California, even just temporarily.

Driving down to visit a Concierge client, the weather is hot and dry, the scenery is spectacular. What were once endless hills of dry grass are now countless miles of vineyards. Boy, has the Golden State changed a lot since 1952.

The vines are heavy with grapes. I stopped by and picked a purple bunch to test out the fruit. The grapes were rich and sweet. It looks like 2024 is going to be a good vintage. No wonder there is a wine glut.

It's going to be a vintage year for Mad Hedge performance as well. We picked up a welcome +3.74%in the testing month of August, +33.61%so far in 2024, and +711.32%since inception.

The harder I work, the luckier I get.

Which raises the most important question of the day: Did September just happen in August? The price action we saw last month is certainly reminiscent of many recent faith-testing Septembers and Octobers.

If that is the case, then it could be off to the races from now. Except this time, it won’t be just a Magnificent Seven rally. It will be an everything rally as the bull broadens out to include all interest rate sectors, which is almost everything.

(SPX) 6,000 by yearend looks like a piece of cake.

The bottom line for all of this is that investors and the markets are still wildly underestimating the impact artificial intelligence will have on our futures, and therefore stock prices. Publishing the Mad Hedge AI Letter three times a week (click here for the link), I can see AI sneaking into every aspect of our lives without our knowledge.

I visited my doctor the other day and they asked for my Medicare card. I didn’t have it because there is no use for this US government ID in Europe from where I just returned. The receptionist said, “Don’t worry, may I have your phone please?” She went into my photos app, searched for “Medicare” and there it appeared instantly. Apple had surreptitiously installed an AI search function on my phone without even telling me.

Try it!

What we are witnessing is the greatest capital spending binge since WWII 83 years ago, when in three short years, the US produced 297,000 aircraft, 193,000 artillery pieces, 86,000 tanks, and two million army trucks. It also double-tracked all east-west rail lines and created from scratch four atomic bombs.

And you want to short that???

The indexes certainly have plenty of room to run. Since the 2020 pandemic bottom, virtually all money has gone into big tech and out of the rest of the market, generating net outflows out of equities and into bonds. What happens when you get net inflows into big tech AND the rest of the market? Markets go up a….lot.

Dow 240,000 here we come.

Now for the challenging chore of sector picking.

Bonds (TLT) are usually the first pick at the beginning of any interest rate-cutting cycle. However, this has been the best telegraphed interest rate cut in history so most of the juice has already been squeezed out of this one. The (TLT) has moved a prolific $18 off the $82 bottom with no interest rate cuts at all. So there might be $5 or $10 of upside left this year, but no more.

Derivative high-yield plays have much more to offer. Those would include junk bonds (JNK), (HYG), BB-rated loans (SLRN), and REITS like the Vornado Realty Trust (VOR), my favorite Crown Castle International (CCI), and Health Properties (DOC).

Utilities usually do well in falling interest rate cycles as they are such big borrowers. In this basket, you can throw NextEra Energy (NEE), Southern Company (SO), and Duke Energy (DUK).

Falling rates also reliably deliver a weak US dollar, so buy every foreign currency play out there (FXA), (FXE), (FXB), (FXC). Also, buy foreign stock markets like the (EEM).

And then there are always big borrowing small caps (IWM), poor performers for the last decade which can always use the life jackets of falling interest rates. Keep in mind that 40% of small caps are regional banks and another 40% are money losers.

And then there are the old reliables. Any of the Magnificent Seven will probably work if you can get them on any selloff like we had on August 5.

So far in August, we are up by +2.67%.My 2024 year-to-date performance is at +33.61%.The S&P 500 (SPY) is up +18.23%so far in 2024. My trailing one-year return reached +52.25. That brings my 16-year total return to +710.24.My average annualized return has recovered to +51.91%.

I executed no trades last week and am maintaining a 100% cash position. I’ll text you next time I see a bargain in any market. Now there are none. I am running one short in Tesla (TSLA).

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 49 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of +74.24%.

Try beating that anywhere.

NVIDIA Dives on Fabulous Earnings, one of the greatest “Buy the rumor, sell the news” moves of all time. The stock dropped to $25, or 17.85% off its all-time high. Production snags with its much-awaited Blackwell chips are to blame. The company’s quarterly met or beat analysts’ estimates on nearly every measure. But Nvidia investors have grown accustomed to blowout quarters, and the latest numbers didn’t qualify. Buy (NVDA) on this dip.

PCE Rises a Modest 02% in July. That is the so-called core personal consumption expenditures price index, which strips out volatile food and energy items, according to Bureau of Economic Analysis data out Friday. On a three-month annualized basis — a metric economists say paints a more accurate picture of the trajectory of inflation — it advanced 1.7%, the slowest this year

Pending Home Sales Drop 5%, and 8.5% YOY, on a signed contracts basis. Many buyers are waiting until after the presidential election to make a move. Pending home sales fell in all four regions last month. The positive impact of job growth and higher inventory could not overcome affordability challenges and some degree of wait-and-see related to the upcoming U.S. presidential election.

Sales of new U.S. single-family homes rocketed by 10.6%, their highest level in more than a year in July. A drop in mortgage rates boosted demand, offering more evidence that the housing market is recovering. Sales reached a seasonally adjusted annual rate of 739,000 units last month, the highest level since May 2023. It was also the sharpest increase in sales since August 2022. New home sales are counted at the signing of a contract. Buy homebuilders on dips (LEN), (DHI), (KBH).

US GDP Reaccelerates to 3.0% Growth in Q2, up from the previous estimate of 2.8%, according to the Bureau of Economic Analysis. Stronger consumer spending more than offset other categories. Can’t beat the USA.

Weekly Jobless Claims Remain Unchanged at 231,000, down 2,000. After being inflated by weather and seasonal factors in July, initial jobless claims in August are stabilizing at a slightly lower level, another indication that layoffs remain low.

Is Costco (CSCO) the Next Stock Split? Costco, which has risen nearly 40% since the start of 2024, is a potential candidate. Given the company’s share price—over $900 as of Tuesday—and the trend among other retailers with similarly high prices to split.

Hindenburg Research Attacks Super Micro, alleging "accounting manipulation" at the AI server maker, the latest by the short seller whose reports have rocked several high-profile companies. Close ties with chip giant Nvidia have allowed Super Micro, known for its liquid cooling technology for high-power semiconductors, to capitalize on the surge in demand for AI servers.

Though revenue has surged, margins have taken a hit recently due to the rising costs of server production and pricing pressure from rivals including Dell. Avoid (SMCI).

Berkshire Hathaway Tops $1 Trillion Market Cap, a long-time Mad Hedge recommendation. It’s the first nontech company ever to do so, even though (BRK/B) has a major holding in Apple (AAPL). Keep buying the big dips. The stock has rallied this year on strong insurance results and economic optimism. The Omaha, Nebraska-based company joins the ranks of a small group to crack the milestone, dominated by technology giants like Alphabet Inc. (GOOGL), Meta Platforms Inc. (META) and Nvidia Corp. (NVDA).

S&P Case Shiller Hits New All-Time High in June. Prices nationally rose 5.4% in June from the year prior. An index measuring prices in 20 of the nation’s large metropolitan areas gained 6.5% from the year prior. On an unadjusted basis, it was the national index’s fourth consecutive all-time high. Prices in New York, San Diego, and Las Vegas grew the most, with year-over-year gains ranging from 8.5% and 9%, while those in Portland, Ore., Denver, Colo., and Minneapolis grew the least.

Canada Imposes 100% Tariff on Chinese EVs. The problem for Tesla is that they had been supplying the Canadian market from their China factory. The supply can be replaced with US-made cars but at a much higher cost. Tesla sold off $8 on the news. Sell rallies in (TSLA).

Is the US Tipping into Recession? A continued drop in job openings will translate into faster increases in unemployment, an argument in favor of the Fed beginning to cut interest rates to guard the labor market. The next jobs reports could be crucial. Policymakers face the dilemma of two risks: being too slow to ease policy, potentially causing a 'hard landing' with high unemployment ... or cutting rates prematurely, leaving the economy vulnerable to rising inflation

Yield Chasers Post Record Demand for Junk Bonds. That’s helped make 2024 the busiest year for the issuance of new corporate high-yield bonds, with $357 billion sold so far, since the easy money days during the pandemic. Issuance of US leveraged loans, meanwhile, is running at its fastest pace on record. Buy (JNK) and (HYG).

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 2 we have Labor Day. All US markets will be closed. On Tuesday, September 3 at 6:00 AM EST, the ISM Manufacturing PMI is released.

On Wednesday, September 4 at 7:30 PM, the JOLTS Job Openings Report is printed.

On Thursday, September 5 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the ADP Employment Report.

On Friday, September 6 at 8:30 AM, the August Nonfarm Payroll Report is released. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, having visited and lived in Lake Tahoe for most of my life, I thought I’d pass on a few stories from this historic and beautiful place.

The lake didn’t get its name until 1949 when the Washoe Indian name was bastardized to come up with “Tahoe”. Before that, it was called the much less romantic Lake Bigler after the first governor of California.

A young Mark Twain walked here in 1863 from nearby Virginia City where he was writing for the Territorial Enterprise about the silver boom. He described boats as “floating in the air” as the water clarity at 100 feet made them appear to be levitating. Today, clarity is at 50 feet, but it should go back to 100 feet when cars go all-electric.

One of the great engineering feats of the 19th century was the construction of the Transcontinental Railroad. Some 10,000 Chinese workers used black powder to blast a one-mile-long tunnel through solid granite. They tried nitroglycerine for a few months but so many died in accidents they went back to powder.

The Union Pacific moved the line a mile south in the 1950s to make a shorter route. The old tunnel is still there, and you can drive through it at any time if you know the secret entrance. The roof is still covered with soot from woodfired steam engines. At midpoint, you find a shaft to the surface where workers were hung from their ankles with ropes to place charges so they could work on four faces at once.

By the late 19th century, every tree around the lake had been cut down for shoring at the silver mines. Look at photos from the time and the mountains are completely barren. That is except for the southwest corner, which was privately owned by Lucky Baldwin who won the land in a card game. The 300-year-old growth pine trees are still there.

During the 20th century, the entire East Shore was owned by one man, George Whittell Jr., son of one of the original silver barons. A man of eclectic tastes, he owned a Boing 247 private aircraft, a custom mahogany boat powered by two Alison aircraft engines, and kept lions in heated cages.

Thanks to a few well-placed campaign donations, he obtained prison labor from the State of Nevada to build a palatial granite waterfront mansion called Thunderbird, which you can still visit today (click here ). During Prohibition, female “guests” from California crossed the lake and entered the home through a secret tunnel.

When Whittell died in 1969, a Mad HedgeConcierge Client bought the entire East Shore from the estate on behalf of the Fred Harvey Company and then traded it for a huge chunk of land in Arizona. Today the East Shore is a Nevada State Park, including the majestic Sand Harbor, the finest beach in the High Sierras.

When a Hollywood scriptwriter took a Tahoe vacation in the early 1960s, he so fell in love with the place that he wrote Bonanza, the top TV show of the decade (in front of Hogan’s Heroes). He created the fictional Ponderosa Ranch, which tourists from Europe come to look for in Incline Village today.

In 1943, a Pan Am pilot named Wayne Poulson who had a love of skiing bought Squaw Valley for $35,000. This was back when it took two days to drive from San Francisco. Wayne flew the China Clippers to Asia in the famed Sikorski flying boats, the first commercial planes to cross the Pacific Ocean. He spent time between flights at a ranch house he built right in the middle of the valley.

His wife Sandy bought baskets from the Washoe Indians who still lived on the land to keep them from starving during the Great Depression. The Poulson’s had eight children and today, each has a street named after them at Squaw.

Not much happened until the late forties when a New York Investor group led by Alex Cushing started building lifts. Through some miracle, and with backing from the Rockefeller family, Cushing won the competition to host the 1960 Winter Olympics, beating out the legendary Innsbruck, Austria, and St. Moritz, Switzerland.

He quickly got the State of California to build Interstate 80, which shortened the trip to Tahoe to only three hours. He also got the state to pass a liability limit for ski accidents to only $2,000, something I learned when my kids plowed into someone, and the money really poured in.

Attending the 1960 Olympic opening ceremony is still one of my fondest childhood memories, produced by Walt Disney, who owned the nearby Sugar Bowl ski resort.

While the Cushing group had bought the rights to the mountains, Poulson owned the valley floor, and he made a fortune as a vacation home developer. The inevitable disputes arose and the two quit talking in the 1980’s.

I used to run into a crusty old Cushing at High Camp now and then and I milked him for local history in exchange for stock tips and a few stiff drinks. Cushing died in 2003 at 92 (click here for the obituary)

I first came to Lake Tahoe in the 1950s with my grandfather who had two horses, a mule, and a Winchester. He was one-quarter Cherokee Indian and knew everything there was to know about the outdoors. Although I am only one-sixteenth Cherokee with some Delaware and Sioux mixed in, I got the full Indian dose. Thanks to him I can live off the land when I need to. Even today, we invite the family medicine man to important events, like births, weddings, and funerals.

We camped on the beach at Incline Beach before the town was built and the Weyerhaeuser lumber mill was still operating. We caught our limit of trout every day, ten back in those days, ate some, and put the rest on ice. It was paradise.

During the late 1990’s when I built a home in Squaw Valley I frequently flew with Glen Poulson, who owned a vintage 1947 Cessna 150 tailwheel, looking for untouched high-country lakes to fish. He said his mother had been lonely since her husband died in 1995 and asked me to have tea with her and tell her some stories.

Sandy told me that in the seventies she asked her kids to clean out the barn and they tossed hundreds of old Washoe baskets. Today Washoe baskets are very rare, highly sought after by wealthy collectors, and sell for $50,000 to $100,000 at auction. “If I had only known,” she sighed. Sandy passed away in 2006 and the remaining 30-acre ranch was sold for $15 million.

To stay in shape, I used to pack up my skis and boots and snowshoe up the 2,000 feet from the Squaw Valley parking lot to High Camp, then ski down. On the way up I provided first aid to injured skiers and made regular calls to the ski patrol.

After doing this for many winters, I finally got busted when they realized I didn’t have a ski pass. It turns out that when you buy a lift ticket you are agreeing to a liability release which they absolutely had to have. I was banned from the mountain.

Today Squaw Valley is owned by the Colorado-based Altera Mountain Company, which along with Vail Resorts owns most of the ski resorts in North America. The concentration has been relentless. Last year Squaw Valley’s name was changed to the Palisades Resort for the sake of political correctness. Last weekend, a gondola connected it with Alpine Meadows next door, creating the largest ski area in the US.

Today there are no Washoe Indians left on the lake. The nearest reservation is 25 miles away in the desert in Gardnerville, NV. They sold or traded away their land for pennies on the current value.

Living at Tahoe has been great, and I get up here whenever I can. I am now one of the few surviving original mountain men and volunteer for North Tahoe Search & Rescue.

On Donner Day, every October 1, I volunteer as a docent to guide visitors up the original trail over Donner Pass. Some 175 years later the oldest trees still bear the scars of being scrapped by passing covered wagon wheels, my own ancestors among them. There is also a wealth of ancient petroglyphs, as the pass was a major meeting place between Indian tribes in ancient times.

The good news is that residents aged 70 or more get free season ski passes at Diamond Peak, where I sponsored the ski team for several years. My will specifies that my ashes be placed in the Middle of Lake Tahoe. At least I’ll be recycled. I’ll be joining my younger brother who was an early Covid-19 victim and whose ashes we placed there in 2020.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Ponderosa Ranch

The Poulson Ranch

At the Reno Airport

Donner Pass Petroglyphs

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/JOHN-THOMAS-lake-e1673280781709.png414500april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-09-03 09:02:212024-09-03 11:49:46The Market Outlook for the Week Ahead, or The Hidden AI in your Life

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SEA CHANGE), (BB RATED BANKS LOANS), and (RESCUING THE USS POTOMAC),

(TLT), (JNK), (SLRN), (BRLN), (BKLN), (FFRHX), (WES), (CCI), (GLD), (DE), (BRK/B), (TSLA), (NVDA).

I believe there was a major sea change in the markets last week, which has taken the economy from inflation to deflation. All asset classes performed as they should, with some extreme moves. It is now time to focus on the 493 of the S&P 500 and let the Magnificent Seven take a long-needed rest.

Not only does this pave the way for a Fed interest rate cut in September, but several more to follow. This opens the floodgates for the (TLT) to rise above $100 by yearend, and maybe even to $110. Remember the old high for bonds is $166. Higher beta fixed-income plays will rise much more.

Stocks will keep rising but with different leadership from dozens of interest-sensitive sectors, including real estate, their suppliers, industrials, precious metals, financials, energy, and outright value plays long left in the doghouse. If you can’t grasp these new trends, your portfolio will be out to sea shortly. An S&P 500 of 6,000 looks like a pretty safe bet by yearend.

That brings to the fore investment in fixed-income securities. There are two ways to make money on a fixed income. Coupon interest rates are still at historically high levels. And as rates fall, fixed-income prices rise, opening the door to capital gains, which could reach 10%-20% in the coming year.

The fixed-income market at $100 trillion is double the size of the stock market. And there are many more bond listings than stock ones. So the number of possible investments is almost endless. I shall give you a brief overview of some of the more interesting subsectors.

US Government bonds – are the gold standard with a guaranteed return. But you pay for the extra security with lower rates; the current ten-year US Treasury bond yield is 4.20%, much lower than the present 90-day T-bill of 5.21%. The easiest way to buy these is through the (TLT). The 30-year government bond should be avoided as the extra 0.14% in yield doesn’t adequately compensate you for the extra 20 years of risk

Junk Bonds – Also known as “high yield” bonds have always been misnamed. The default rates never remotely approached the levels that justified their high yields, not even during the financial crisis, as my old friend former junk bond king Michael Milliken has amply proven. The (JNK) is currently yielding 6.59% and has the potential for larger capital gains than government bonds.

Master Limited Partnerships – These are partnerships granted generous tax benefits with the goal of producing oil. They issue annual Form K-1’s to include with your tax return. Dividends are deferred until the MLP’s investment reaches the end of its useful life, which can be decades. MLPs used to be a huge industry with dozens of listed companies.

When the price of oil went to negative numbers during the pandemic, most of them got wiped out. Because of this rocky past, there are a handful of large, well-capitalized MLPs with extremely high yields. One is Western Midstream Partners (WES) with a 9.20% yield. Energy Transfer Partners (ET) pay a 7.96% yield.

These yields will remain safe as long as oil prices are stable or rising, as I expect in a long-term global economic recovery. Take oil back to zero again in another pandemic and these returns will get turned on their head.

With the normalizing of interest rates, it's time to normalize investment strategies as well. That means bringing back the old 60/40 strategy where one half of the portfolio ensures the other, with a modern twist. You can put 60% of your assets in stocks, with half on technology and half on domestic cyclicals.

The other 40% should be allocated to some mix of the above fixed-income investments guaranteeing annual high returns. It is not a bad strategy for mature investors, especially if they would rather be on a golf course instead of spending all day in front of a screen picking bottoms and tops for stocks, like Millennials.

Here’s where to get a Safe 8.48% Yield, BB-rated bank loans, which will soar in value with even just one quarter-point rate cut. BB bank loans are very low risk, and they have a spread that’s about 290 basis points above the overnight Fed rate. How does one buy such an animal? The actual bank loans themselves are made by lending institutions to companies. These loans aren’t made accessible to individual investors who want to make a play for yield. Rather, large institutional investors snap them up and add them to their fixed-income portfolios. The top ticker symbols are (SLRN), (BRLN), (BKLN), and (FFRHX). Check them out.

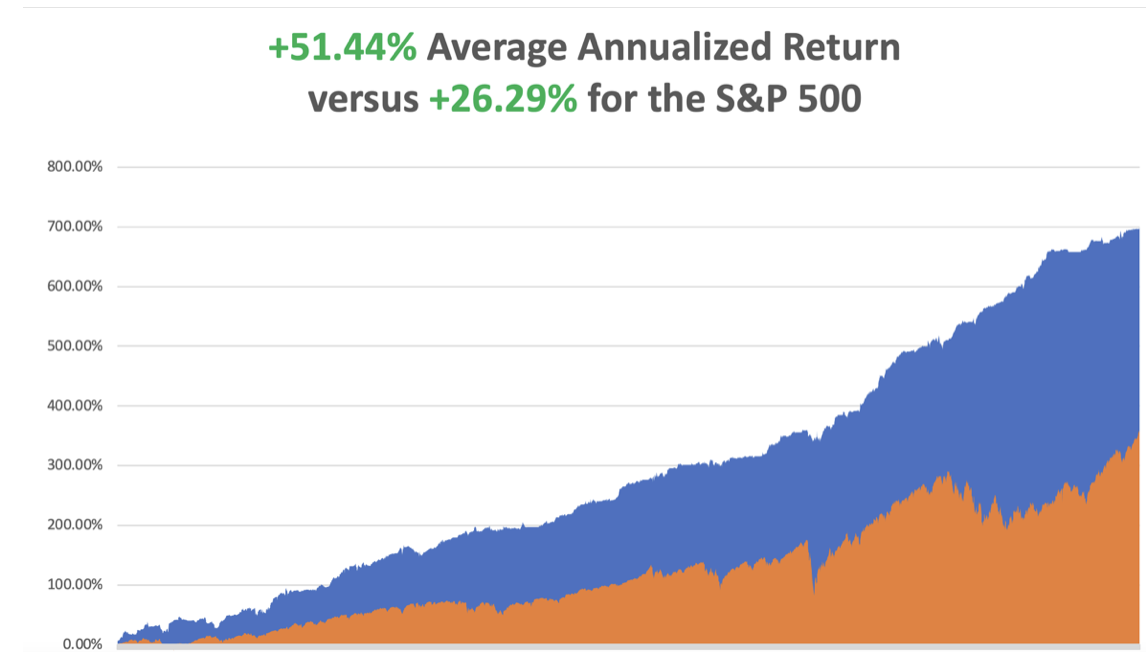

So far in July, we are up +2.17%. My 2024 year-to-date performance is at +22.19%.The S&P 500 (SPY) is up +17.40%so far in 2024. My trailing one-year return reached +37.07. That brings my 16-year total return to +698.82%.My average annualized return has recovered to +51.44%.

I used the blockbuster CPI Report last week to jump off my 100% cash position and piled on six new positions. Those included interest rate-sensitive longs in (CCI), (GLD), (DE), (BRK/B), and shorts in big tech leaders (TSLA) and (NVDA).

Some 63 of my 70 round trips were profitable in 2023. Some 35 of 44 trades have been profitable so far in 2024, and several of those losses were really break-even.

Nonfarm Payroll Report Comes in Weak for June at 206,000. The Headline Unemployment rate rose to a three-year high at 4.1%. All interest rate plays rocketed as a September interest rate comes back on the table. If the Fed doesn’t cut soon, we are going into recession. Buy (TLT) on dips.

Fed Governor Jay Powell Warns of Recession Risks if interest rate cuts don’t take place soon, spiking all markets. Powell is showing his cards for the next few Fed Meetings. Buy all interest rates plays like (TLT), (JNK), (NLY), and (CCI).

CPI comes in Negative. The writing is not only on the wall right now, it’s blasting us with great neon lights. That was the message this morning from the Consumer Price Index, which this morning delivered a gob-smacking 0.1% DECLINE in June. We are now in deflation and the YOY inflation rate is now down to only 3.0%. As a result, a Fed interest rate cut of 25 basis points is now a certainty in September and more will follow. All falling interest rate plays in the stock market are in play. Rising rate plays could be the trade for the rest of 2024.

PPI Rises 0.2%, with Wholesale Prices coming in as expected. The producer price index is now up 2.6% year over year. The inflation pictures goes back to mixed. Stocks rallied with big tech recovering about half of yesterday’s losses.

Consumer Sentiment at a Three-Year Low at 66.0%, down from 68.5 as the economic slide continues, according to the University of Michigan. It’s another pre-recession indicator.

Bank Earnings Beat and the stocks are rising in expectation of falling interest rates, with (JPM), (BAC), and (C) reporting. Wells Fargo (WFC) Bombed again. Buy banks on dips which have been on a tear all day.

Tesla Delays Robotaxi Day, past its original August 8 target to probably October, tanking the shares by 11%. The date propelled the massive 50% rally in the hares over the past month. Musk is always overly aggressive on his targets. Sell calls against existing (TSLA) stock positions.

Apple Expects 10% Rise in iPhone Shipments in 2024, after a bumpy 2023, counting on AI features to fuel demand for the iPhone 16. Apple is now the newly discovered AI stock. Buy (AAPL) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, July 15 at 9:30 AM EST, Feder Governor Jay Powell speaks. He has lately been leaning dovish. On Tuesday, July 16 at 9:30 AM, Retail Sales are published.

On Wednesday, July 17 at 9:30 AM, Building Permits are out.

On Thursday, July 18 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, July 19 at 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I usually get a request to fund some charity about once a day. I ignore them because they usually enrich the fundraisers more than the potential beneficiaries. But one request seemed to hit all my soft spots at once.

Would I be interested in financing the refit of the USS Potomac (AG-25), Franklin Delano Roosevelt’s presidential yacht?

I had just sold my oil and gas business for an outrageous profit and had some free time on my hands so I said, “Hell Yes,” but only if I get to drive. The trick was to raise the necessary $5 million without it costing me any money.

To say that the Potomac had fallen on hard times was an understatement.

When Roosevelt entered the White House in 1932, he inherited the presidential yacht of Herbert Hoover, the USS Sequoia. But the Sequoia was entirely made of wood, which Roosevelt had a lifelong fear of. When he was a young child, he nearly perished when a wooden ship caught fire and sank, he was passed to a lifeboat by a devoted nanny.

Roosevelt settled on the 165-foot USS Electra, launched from the Manitowoc Shipyard in Wisconsin, whose lines he greatly admired. The government had ordered 34 of these cutters to fight rum runners across the Great Lakes during Prohibition. Deliveries began just as the ban on alcohol ended.

Some $60,000 was poured into the ship to bring it up to presidential standards and it was made wheelchair accessible with an elevator, which FDR operated himself with ropes. The ship became the “floating White House,” and numerous political deals were hammered out on its decks. Some noted guests included King George VI of England, Queen Elizabeth, and Winston Churchill.

During WWII Roosevelt hosted his weekly “fireside chats” on the ship’s short-wave radio. The concern was that the Germans would attempt to block transmissions if the broadcast came from the White House.

After Roosevelt’s death, the Potomac was decommissioned and sold off by Harry Truman, who favored the much more substantial 243-foot USS Williamsburg. The Potomac became a Dept of Fisheries enforcement boat until 1960 and then was used as a ferry to Puerto Rico until 1962.

An attempt was made to sail it through the Panama Canal to the 1962 World’s Fair in Seattle, but it broke down on the way in Long Beach, CA. In 1964 Elvis Presley bought the Potomac so it could be auctioned off to raise money for St. Jude Children’s Research Hospital. It sold for $65,000. It then disappeared from maritime registration in 1970. At one point, there was an attempt to turn it into a floating disco.

In 1980, a US Coast Guard cutter spotted a suspicious radar return 20 miles off the coast of San Francisco. It turned out to be the Potomac loaded to the gunnels with bales of illicit marijuana from Mexico. The Coast Guard seized the ship and towed it to the Treasure Island naval base under the Bay Bridge. By now, the 50-year-old ship was leaking badly. The marijuana bales soaked up the seawater and the ship became so heavy it sank at its moorings.

Then a long rescue effort began. Not wanting to get blamed for the sinking of a presidential yacht on its watch, the Navy raised the Potomac at its own expense, about $10 million, putting its heavy lift crane to use. It was then sold to the City of Oakland, CA for a paltry $15,000.

The troubled ship was placed on a barge and floated upriver to Stockton, CA, which had a large but underutilized unionized maritime repair business. The government subsidies started raining down from the skies and a down to the rivets restoration began. Two rebuilt WWII tugboat engines replaced the old, exhausted ones. A nationwide search was launched to recover artifacts from FDR’s time on the ship. The Potomac returned to the seas in 1993.

I came on the scene in 2007 when the ship was due for a second refit. The foundation that now owned the ship needed $5 million. So, I did a deal with National Public Radio for free advertising in exchange for a few hundred dinner cruise tickets. NPR then held a contest to auction off tickets and kept the cash (what was the name of FDR’s dog? Fala!).

I also negotiated landing rights at the Pier One San Francisco Ferry Terminal, which involved negotiating with a half dozen unions, unheard of in San Francisco maritime circles. Every cruise sold out over two years, selling 2,500 tickets. To keep everyone well-lubricated, I became the largest Bay Area buyer of wine for those years. I still have a free T-shirt from every winery in Napa Valley.

It turned out to be the most successful fundraiser in the history of NPR and the Potomac. We easily got the $5 million and then some. The ship received a new coat of white paint, new rigging, modern navigation gear, and more period artifacts. I obtained my captain’s license and learned how to command a former Coast Guard cutter.

It was a win-win-win.

I was trained by a retired US Navy nuclear submarine commander, who was a real expert at navigating a now thin-hulled 73-year-old ship in San Francisco’s crowded bay waters. We were only licensed to cruise up to the Golden Gate Bridge and not beyond, as the ship was so old.

The inaugural cruise was the social event of the year in San Francisco with everyone wearing period Depression-era dress. It was attended by FDR’s grandson, James Roosevelt III, a Bay area attorney who was a dead ringer for his grandfather. I mercilessly grilled him for unpublished historical anecdotes. A handful of still-living Roosevelt cabinet members also came, as well as many WWII veterans.

As we approached the Golden Gate Bridge, some poor soul jumped off and the Coast Guard asked us to perform search and rescue until they could get a ship on station. Nobody was ever found. It certainly made for an eventful first cruise.

Of the original 34 cutters constructed, only four remain. The other three make up the Circle Line tour boats that sail around Manhattan several times a day.

Last summer, I boarded the Potomac for the first time in 14 years for a pleasant afternoon cruise with some guests from Australia. Some of the older crew recognized me and saluted. In the cabin, I noticed a brass urn oddly out of place. It contained the ashes of the sub-commander who had trained me all those years ago.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain Thomas at the Helm

https://www.madhedgefundtrader.com/wp-content/uploads/2024/07/John-Thomas-and-friends.png8401110april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-07-15 09:02:572024-07-15 12:26:34The Market Outlook for the Week Ahead, or Sea Change

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.