Down 8% on a faulty chatbot conversation – that’s what happened to Google’s (GOOGL) stock today.

That’s why we need to pare back the euphoria and nonstop celebration of ChatGPT.

Hold your horses.

It’s an emerging technology and could end up with chatbots chatting with other chatbots for little or no value.

My point is that it can still go very wrong from here.

Google’s stock swan dived on Wednesday after its own iteration of A.I. chatbot erroneously answered a question about the first usage of space telescopes via its promotional material.

It all lends itself to surmise that Google is way behind in this game and Microsoft has the situation by the scruff of the neck.

Only just a few days ago, Microsoft integrated the AI technology into the front page of its Bing search engine, and is available for user downloads on the Bing app.

The drop in share price meant that Google lost more than $100 billion off its market cap.

The service called Bard is to compete with the popular ChatGPT.

Despite the chatbot’s claim in the ad, NASA reports that the first photo of a planet outside the Milky Way was taken by the Very Large Telescope in 2004 — nearly 19 years before NASA’s Webb telescope.

Unpreparedness by Google could translate into a significant loss of ad revenue for Google’s cash cow Google search.

The desperation of throwing Bard out there not on their timeline could mean they are exposing a product that isn’t up to Google’s standards.

An AI chatbot that consistently delivers false answers will turn off an advertiser quicker than no AI chatbot.

Investing in Google is still worth it even if it takes time to correct the quality of their AI. because it is logical to give a good company the benefit of the doubt.

Another problem is that Google could be stuck with bad AI for a few years before it turns the corner.

For better or worse, they were forced to go public with whatever they had just for the optics of competition even if they are badly lagging behind.

The worst-case scenario is receiving a direct blow to the cranium in terms of total ad revenue.

Google is still relying on search to drive the rest of its business.

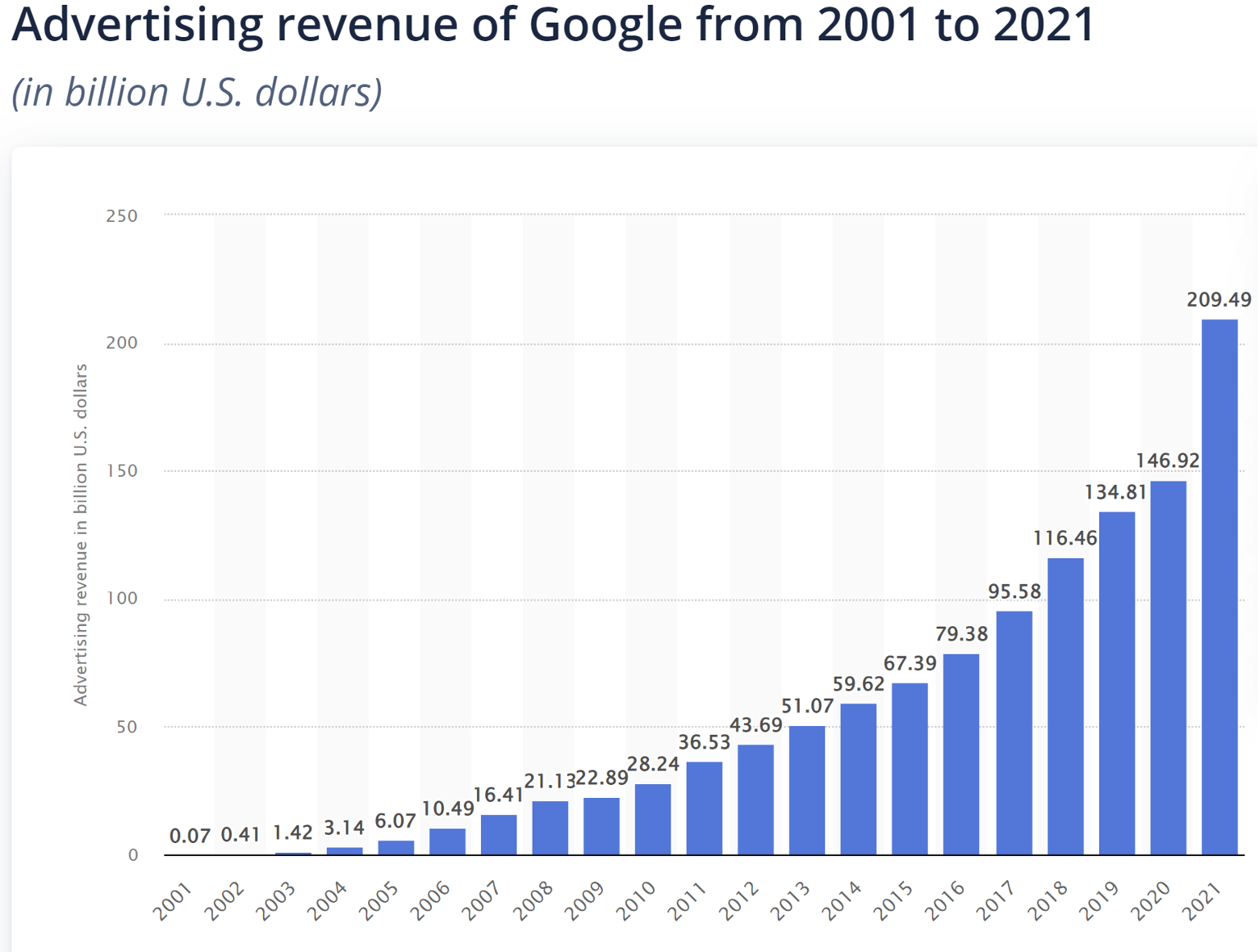

They earned over $200 billion in ad revenue in 2021.

This is the first threat to Google’s search model in a generation and the threat has them on their toes.

I do believe they possess the resources to solve this issue.

No doubt that Google CEO Sundar Pichai is throwing the kitchen sink to find and poach the best AI engineers to beef up the chatbot team.

Ultimately, the real new world of higher interest rates and high inflation environment means that your father’s tech playbook must be thrown out the window.

It’s quite evident that we are in the midst of a paradigm shift and new leaders during this shift will emerge.

History shows us that tech leaders of old have a habit of falling behind because they are too set in their ways to adapt to a world with new rules.

It might be so that at some point in the not-so-near future, we might need to set the search default to Bing.

How ironic?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-08 15:02:442023-03-01 21:46:30Chatbots Sink Stock 8%

Below please find subscribers’ Q&A for the January 25 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What do you think about LEAPS on Rivian (RIVN)?

A: Yes, I would do those, but a smaller position with closer strike prices. Go to the maximum maturity 2 years out and be conservative—bet on only a 50% rise in the stock. I’m sure it’ll double, but with the LEAPS you’ll have tremendous upside leverage, like 10 to 1, so don’t get greedy. Go for the 500% profit in 2 years rather than the 1,000%, because it is still a startup, and we need economic recovery for startups to get traction. If anything, Tesla (TSLA) will drag this stock back up as it dragged it down. They all move together.

Q: What’s the number of contracts on your $100,000 model portfolio?

A: Our model portfolio basically assumes we have 10 positions of $10,000 each totaling $100,000 in value. You can then change the number of contracts to suit your own private portfolio—take on as much or as little risk as you want. If you’re new. I recommend trading on paper first to make sure you can make money before you use the real thing.

Q: I’m new to this service. What’s the difference between the long-term portfolio and the short-term portfolio?

A: A long term portfolio is a buy-and-forget portfolio, with maybe a 5- or 10-year view. We only change it and make adjustments twice a year so we can average back into the new positions and take profits on the old ones. The main part of this service is usually front-month, and that’s where we take advantage of anomalies in the options market and market timing to make profits 95% of the time. And a big part of the short-term portfolio is cash; we often go 100% cash when there are no trades to be had. It’s actually more valuable knowing when not to trade than when to trade. If you have any more questions, just email customer support at support@madhedgefundtrader.com and we’ll address them individually.

Q: Is it time for a CBOE Volatility Index ($VIX) trade?

A: I hate trading ($VIX). I only do it from the short side; when you get down to these low levels it can flatline for several months, and the time decay eats you to death. I only do it from the short side, and then only the 5% of the time that we’re peaking in ($VIX). The big money is made on the short side, that’s how virtually the entire options trading industry trades this.

Q: Would you be loading up with LEAPS in February?

A: No, it’s the worst time to do LEAPS. You do LEAPS at long-term market bottoms like we had in October, and then we issued 12 different LEAPS. If you get a smaller pullback, there may be LEAPS opportunities, but only in sectors that are near all-time lows, like gold or silver. It depends on the industry and where we are in the market, but basically, you’re looking to do LEAPS at lows for the year because the leverage is so enormous, and so are the potential profits.

Q: Is the increasing good performance a result of your artificial intelligence? Learning from past mistakes?

A: Partly yes, and partly my own intelligence is improving. Believe it or not, when you go from year 54 to 55 in experience in the markets, you understand a lot more about the markets. Sometimes you just get lucky being on the right side of black swan events. Of course, knowing when the market is especially sensitive and prone to black swans is also a handy skill to have.

Q: Is it too late to get into Freeport McMoRan (FCX)?

A: Yes, I wouldn’t touch (FCX) until we get at least a $10 selloff, which we may get in February, so I think the long term target for (FCX) is $100. The stock has nearly doubled since the LEAPS went out in October from $25 a share to almost $50, so that train has left the station. Better off to wait for the next train or find another stock, there are a lot of them.

Q: Where do you park cash in the holding pattern?

A: Very professional hedge fund managers buy 90-day T-bills, because if you keep your cash in your brokerage account—their cash account—and they go bankrupt, it’ll take you 3 years to get your money back in a bankruptcy proceeding. If you own 90-day T-bills and your broker goes bankrupt, they’re required by law to just hand over the T-bills to you immediately. You take delivery of the T-bills, you park them at another brokerage house, and you keep them there. There is no loss of the use of funds.

Q: What about Long term US dollar (UUP)?

A: We go down for 10 years. Falling interest rates are poison for a currency; our rates are probably going to be falling for the next several years.

Q: Thoughts on Tesla (TSLA)?

A: Short term way overbought, we almost got up 60% from the low in weeks, but that’s Tesla, that’s just how it trades. It is the best performing major stock in the market this year. I wouldn’t be looking to go back into it until we drop back, give up half of that gain, get back down to about $135—then it would be a good options trade and a good LEAPS.

Q: Would you be taking profits in Nvidia (NVDA)?

A: I would take like half here and look to buy it back on the next dip because I think Nvidia’s got higher highs ahead of it.

Q: I can’t get a password for the website.

A: Please contact customer support on the homepage and they will set you up immediately. If not, you can call them at (347) 480-1034.

Q: Would you be selling long term positions?

A: No I would not, because if you sell a long term position they’re very hard to get back into; and I’m expecting $4,800 in the (SPX) by the end of the year. Everything goes up by the end of the year, even things you hate. So no, selling is what you did a year ago, now you’re basically looking for chances to get back in.

Q: Would you hold Tesla (TSLA) over this earnings report?

A: No, I sold my position yesterday, at 70% of its maximum potential profit. I don't need substantial selloff; I’m just going to go right back in again.

Q: Have you heard anything about Tesla silicon roof tiles tending to catch fire?

A: No I have not, but if your house got struck by lightning or if someone fired a bullet at it, that might do the trick. Otherwise, you need a huge input of energy to get silicon to catch on fire as it’s a pretty stable element. And if it was already happening on a large scale, you know the media would be absolutely all over it—the media loves to hate Tesla and loves to hate Elon Musk. That certainly would draw attention if it were happening; what's more likely is that fake news is spreading rumors that are not true. That's been a constant problem with Tesla from the very beginning.

Q: Would you open the occidental spread here today?

A: I would, but I would use strike prices $5 lower. I'd be doing the February $50-$55 vertical bull call spread to give yourself some extra protection, given that the general market itself is so high.

Q: Should I be shorting Apple (APPL) here?

A: No, but the smart thing to do is to sell the $160 calls because I don’t think we’ll get up to $160. You could take any extra premium income, and if you don’t get hit this month, keep doing it every month until you are hit, and then you can take in quite a lot of premium income by the time we get to new highs in Apple, possibly as much as $10 or $15. So, that would be a smart thing to do with Apple.

Q: What's your favorite in biotech and big pharma?

A: Eli Lilly (LLY), which just doesn't seem to let anybody in.

Q: If China were to shut down again, would it hurt the stock market?

A: Yes, but not much. The much bigger falls would be in Chinese stocks (which have already doubled since October) not ours.

Q: Thoughts on biotech?

A: Biotech is the new safety trade that will continue. Also, they’re having their secular ramp-up in technology and new drugs so that is also a good long-term bull call on biotech.

Q: What’s the dip in iShares 20+ Year Treasury Bond ETF (TLT)?

A: $4 points at a minimum, $5 is a nice one, $6 would be fantastic if you can get it.

Q: Could we get a trade-up in oil (USO)?

A: Yes, maybe $5 or $10 a barrel. But it’s just that, a trade. Long term, oil still goes to zero. Short term, China recovery gives a move up in oil and that's why we went long (OXY).

Q: You talk about California NatGas being dead, but California gets 51% of its electricity from natural gas, up from 48% in 2018.

A: Yes, but that counts all of the natural gas that gets brought in from other states. In fact, if you look at the longer-term trend over the last 20 years, coal has gone to zero, nuclear is going to zero, hydro has remained the same at about 10%. NatGas has been falling and green sources like wind and solar, have been rising quite substantially. And now, approximately 25% of all the homes in California get solar energy, or 8.4 million homes, and it is now illegal to put gas piping into any new construction. New York is doing the same. That means it will be illegal to do new natural gas installations in a third of the country. So, I think that points to lower natural gas consumption, and in fact, the 22-year target is to take it to zero, which might be optimistic but you never know. All they need is a smallish improvement in solar technology, and that 100% from green sources is doable by 2045, not only for California but for everybody. All energy plays are a trade only, not an investment.

Q: Any thoughts on the implications for the US and Germany providing tanks to Ukraine?

A: You can throw Poland in there, which is also contributing a tank division—so a total of 58 M1 Abrams tanks are going to Ukraine. By the way, I did command a Marine Corps tank battalion for two weeks on my reserve duty, so I know them really well inside and out. They are powered by a turbine engine, have a suspension as soft as a Cadillac, a laser targeting system accurate to three miles even for beginners, and fire recycled uranium shells that can cut through anything like a knife through butter. The answer is the war gets prolonged, and eventually forces Russia into a retreat or a negotiation. Even though the M1 is an ancient 47-year-old design, its track record against the Russian T72 is pretty lopsided. In the first Gulf War, the US destroyed 5,000 T72s and the US lost one M1 tank because he parked on a horizon, which you should never do with a tank. And every driver of a T72 knows that track record. So that explains why Russian tanks have been running out of gas, sugaring their gas tanks, sabotaging their diesel engines, and doing everything they can to avoid combat because of massive fatal design flaws in the T72. We only need to provide about 50 or 60 of the M1 tanks as a symbolic gesture to basically scare the entire Russian tank force away.

Q: Why do you think Elon kept selling Tesla? Did he think it would go lower?

A: Elon thinks the stock’s going to $10,000, but he needed up-front cash to build out six remaining Tesla factories, and for that, he needed about $40 billion, which is why he sold $40 billion worth of stocks last year when it was peaking. He also is sensitive to selling at tops; it’s better to sell stock in with Tesla at an all-time high than at an all-time low, so he clearly times the market to meet his own cash flows.

Q: What about military contractors?

A: I know Raytheon (RTX) and Lockheed Martin (LMT) have a two-year backlog in orders for javelin missiles and stingers, which are now 47-year-old technology that has to be redesigned from scratch. The US just placed an order for a 600% increase in artillery shells for the 155 mm howitzer. I thought we’d never use these again, which is why US stocks for ammunition got so low. But it looks like we have more or less a long term or even permanent customer in Ukraine for everything we can produce, in old Vietnam-era style technologies. How about that? I’m telling the military to give them everything we’ve got because everything we’ve got is obsolete.

Q: When should we buy Microsoft (MSFT)?

A: On the next 10% dip. It’s the quality stock in the US.

Q: Do you place an order to close the spread at profit as soon as you have filled in the trade?

A: You can do that, but it’s kind of a waste of time. Wait until we get close to the strikes; most of the big companies we deal in, you don't get overnight 10% or 20% moves, although it does happen occasionally.

Q: Natural Gas (UNG) prices are collapsing.

A: Correct, because the winter energy crisis in Europe never showed and spring is just around the corner.

Q: On the Tesla (TSLA) LEAPS, what about the January 2025 $600-$610 vertical bull call spread

A: That is way too far out of the money now. I would write that off and go back into it but do something like a January 2025 $180-$190. It has a much higher probability of going in the money, and still an extremely high return. It would be something like 500% if you get in down at these levels.

Q: How do you see Bitcoin short term/long term?

A: I think the loss of confidence in the asset has been so damaging that it may not come back in my lifetime. It could be another Tokyo situation where it takes 30 years to recover, or only recovers when the entire sector gets taken over by the big banks. So, I don’t see any merit in the crypto trade, probably forever. Once you lose confidence in the financial markets, it’s impossible to get it back. And it turns out that every one of these mainline trading platforms was stealing from the customers. No one ever comes back from that in the financial markets.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

At 29 Palms in my M1 Abrams Tank in 2000

https://www.madhedgefundtrader.com/wp-content/uploads/2022/12/john-thomas-tank-commander.jpg318516Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-27 09:02:302023-01-27 12:37:29January 25 Biweekly Strategy Webinar Q&A

The most talked about topic at the forum of the elites in Davos, Switzerland was the souring economic environment globally.

That’s starting to look more real by the day as companies realize aggressive revenue estimates need to be flushed down the toilet.

As funny as it sounds, the January gangbuster rally could have been just a delayed Santa Claus Rally that got pushed back one month.

Now we are entering earnings season, and that means some companies won’t be able to spin numbers in the right way.

That bodes ill for many tech companies as, beneath the surface, the engine humming along that is the tech sector is starting to flash a few red lights.

Tech shares sold off sharply this morning which is quite unusual when the U.S. 10-year treasury barely moves.

Why did it open up poorly?

Microsoft offered us unimpressive guidance that was $2 billion less than the consensus.

Clearly, Microsoft is trying to lower the bar earlier than the other tech companies, boding ill for sector-wide guidance.

That’s highly unusual for the tech bellwether who has the habit of beating and raising forecasts almost systemically.

I can’t imagine tech firms in the ecommerce space like Amazon or Etsy offering better than expected guidance either for the annual year or the quarter’s ahead.

Microsoft was also one of those tech firms that took a machete to staff and sliced off a big chunk of them.

I would have liked to see Microsoft fire more than 10,000 workers and felt they could have easily handled a 50,000 reduction.

The $1.2 billion charge resulting from these layoffs is just a drop in the bucket for MSFT.

CEO Satya Nadella used the words "caution" at least six times on the one-hour call on Tuesday.

Nadella also let investors know that Microsoft Azure, the cloud product, is slowing down to 31% and although still healthy, growth products aren’t growth products anymore when they dip into the 20% range.

The tech business model and the sector as a whole is getting a little stale.

They aren’t the shining stars of the equity market anymore as costs skyrockets and revenue decelerate. That designation is now reserved for energy and precious metals.

Don’t wait for tech to pull a rabbit out of the hat in the short run.

The bad news is that it doesn’t seem that revenue weakness will only be confined to Microsoft.

A large swath of the tech sector could be painted red when it’s all said and done, which is why equity holders are betting on US Central Bank head Jerome Powell saving the day.

The silver liner on offer from Nadella was telling us how MSFT is betting the ranch on artificial intelligence particularly ChatGPT.

Artificial Intelligence inching closer to material revenue contribution is highly positive, but in the here and now, it’s hard to see where the incremental great idea comes from.

Nadella also told us that enterprise software isn’t doing as great because companies are being thriftier in what software they use.

Firms are cutting software and reducing their software footprint where they can get away with it.

Sales of Windows Licenses dropped 39% year over year highlighting the issue of companies attempting to universally cut costs.

When the overall economic mindset originates from a thrifty-based beginning, it doesn’t favor technology stocks.

Tech usually basks in the glory of the excesses, which is why they overshoot to the upside.

Hence, Chairman Powell is now priced in to singlehandedly rescue tech shares as many investors wait for his pivot back to zero interest rates yet again just like the 2008 Great Financial Crisis on repeat.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-25 15:02:192023-02-01 22:34:37Unimpressive From The Behemoth

Below please find the subscribers’ Q&A for the January 11 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: In your trade alert you expected that the (TLT) might go up as much as 30% this year. But in your latest newsletter, you mentioned that the chaos in the US House of Representatives would greatly raise the risk of a default on US government debt by the summer and certainly cast a shadow over your 50% long bond position. Is it still a good idea to hold on to the (TLT) ETF over the next 2-6 months?

A: It is. The extremists who now control the House are not interested in governing or passing laws but gaining clicks, raising money, and increasing speaker’s fees. It may have converted (TLT) from a straight-up trade to a flat-line trade. We will still make the maximum profit on call spreads and LEAPS but with greater risk. But even chaos in the House can’t head off a recession, which the bond market seems intent on pricing in by going up. However, if you depend on government payments for any reason, be it Social Security, a government salary, a tax refund, or a payment for a contract, expect delays. The housing market also ceases because closings can’t take place during government shutdowns. Also, 30% of my bond longs expire in four trading days, and the remainder on February 17.

Q: Is it wise to sell the 2X ProShares Ultra Technology ETF (ROM) now or keep holding?

A: I think the (ROM), NASDAQ, and technology stocks in general may make several runs at the lows over the next six months but won’t fall much from here. A recession is priced in. Once we get through this, you’re looking at doubles and triples for the best names. So, the risk/reward overwhelmingly favors holding on to a one-year view.

Q: would you buy Tesla (TSLA) here?

A: I would start scaling in. The bad news is about to dry up, like Twitter, the recession, the pandemic in China, and Elon Musk selling shares. Then we face an onslaught of good news, like the new Mexico factory announcement, the Cybertruck launch, solid state batteries, and annual production hitting 2 million. At this level, the shares are priced in multiple worst-case scenarios. It is selling at 10X 2025 earnings, half the market multiple. At the end of the day, Tesla has an unassailable 14-year start over the rest of the industry and is the only company in the world that makes money on EVs. There’s an easy 10X here on two-year LEAPS.

Q: I’m in the Freeport McMoRan (FCX) January 25 2-year LEAP approaching the upper end of the 42/45 range. If it crosses 45, do we close the position?

A: Sell half, take your profit. If you’re in the LEAP, my guess is you probably have a 500% profit here in only 3 months, which is not bad. And then you keep the remaining half because you’re then playing with the house's money, and Freeport has a shot of going all the way to $100 a share by the 2025 expiration, and that will get you your full 1,000% return on the position. It’s always nice to be in a position where it’s impossible to lose money on a trade, and that certainly is where you are now with your (FCX) LEAP and everybody else in the FCX LEAP in October also.

Q: As a member of the Florida Retirement System, I’m curious how Blackrock (BLK) and other firms are dealing with the Santos’ plan for their portfolios.

A: Having a state governor manage your portfolio and make your sector and stock picks is an absolutely terrible idea. I can’t imagine a worse possible outcome for your retirement funds. Florida is not the only state doing this—Louisiana and Texas are doing it too. The goal is to drive money out of alternative energy and back into the oil industry, and obviously, this is being financed by the oil industry, which is pissed off over their low multiples. Suffice it to say it’s not a good idea to move out of one of the fastest-growing industries in the market and move into an industry that’s going to zero in 10 years. If that’s their investment strategy, I wish they’d stick to politics and leave investing for true professionals to do.

Q: What do you think about cannabis stocks?

A: I’m a better user of the product than the stock. How about that? How hard is it to grow weed? At the end of the day, these are just pure marketing companies, and that value added is low. Plus, they have huge competition from the black market still selling ½ to ⅓ below market prices because they’re tax-free; the local taxes on these cannabis sales are enormous.

Q: Would you recommend selling a bear market rally when the S&P goes to 405?

A: The (QQQ) would be the better short, something like the $310-320 vertical bear put spread for February to bring in some free money. That’s what I'm planning to do if we get up that high, which we may not.

Q: How do you take advantage of a low CBOE Volatility Index (VIX)?

A: You don’t; there’s nothing to do here with the (VIX) at $22. My trades this year were not volatility trades—because we did them with low volatility, they were pure directional trades betting that the longs would go up and the shorts would go down and they all worked.

Q: Will Rivian (RIVN) survive?

A: Yes, they have two years of cash flow in the bank, and they’re boosting production. However, a high-growth, non-earning stock like Rivian is just out of favor right now. Will they come back into favor? Yes, probably in a year or so, but in the meantime, people are much happier buying Microsoft (MSFT) at a discount than Rivian.

Q: Do you ever buy butterfly spreads?

A: No, four-legged trades run up a lot of commissions, are hard to execute because you have 4 spreads, and have lower returns. They are also lower risk and for people who have no idea what the market is going to do. I don’t need the lower risk trades because I know what markets are going to do.

Q: Do you suggest any Microsoft (MSFT) LEAPS?

A: Yes, go out two years with LEAPS and go out about 50% on your strike prices. A 50% move here in Microsoft in two years is a complete no-brainer.

Q: With weakness in retail, rising inventories, and high consumer debt, will consumers dip into savings?

A: Yes they will, but that will predominantly happen at the bottom half of the economy—the part of the economy that has minimal to no savings. The upper half seems to be doing well—the middle class and of course, the wealthy— and are not cutting back their spending at all, which is why this seems to be a recession that may not actually show up. So, what can I say? The rich are doing great and everyone else is doing less than great, and stocks are reflecting that. Nothing new here.

Q: Would you hold off on tech LEAPS for a bigger selloff, or closer to April?

A: If we do get another big selloff and challenge the October lows, I’ll be pumping out those LEAPS as fast as I can write them; except then, a two-year LEAPS will have an April of 2025 expiration.

Q: I just signed up. What are the advantages of LEAPS?

A: A possible 10x return in 2 years with very low risk. I would suggest going to my website, logging in, and doing a search for LEAPS. There will be a piece there on how to execute a LEAPS, and the Concierge members can also find that piece by logging into their website.

Q: Best and worst sectors?

A: First half, already mentioned them. We like commodities, healthcare, financials, and Berkshire Hathaway (BRK/B) in the first half and tech in the second half.

Q: Have we reached a low in cryptocurrencies?

A: Probably not, and I’ll tell you why I’ve given up on cryptos: I may not live long enough to see the bottom in crypto. It has Tokyo written all over it, and it took Tokyo 30 years to resume a bull market after it crashed in 1990. We’re still at the scandal stage where it turns out that the majority of these trading platforms were stealing money from customers. This is not a great inspiration for investing in that sector. When you have the best quality growth stocks down 80-90%; why bother with something that may not exist or may never recover in your lifetime? I’m out of the crypto business, but there are a wealth of crypto research sources still online and I’m sure they’d be more than happy to give you an opinion.

Q: Why have defense stocks like Raytheon (RTX) and Lockheed Martin (LMT) been weak recently?

A: A couple of reasons. #1 Just outright profit taking into the end of the year in one of the best-performing sectors. #2 The end of the war in Ukraine may not be that far off, and if that happens that could trigger a major round of selling in defense. We did get the three-day ceasefire over the Russian Orthodox New Year, that’s a possible hint, so that may be another reason.

Q: Political outlook on 2024?

A: It’s too early to make any calls, anything could happen; but if we get a repeat of the November election outcome, you could have Democrats retake control of both houses of congress—that’s where the betting money is going right now.

Q: Would you bottom fish in the United States Natural Gas Fund (UNG)?

A: No, I would not—I am avoiding energy like the plague. Remember the all-time low for natural gas is $0.95 per MM BTU, so we still could have a long way to go.

Q: Would you buy iShares China Large-Cap ETF (FXI) on a post-COVID breakout?

A: It looks like it’s already moved, so maybe kind of late on that. The problem is that in China, you don’t know what you are buying and the locals have a huge advantage in reading Beijing.

Q: What do you think about the Biden administration wanting to ban gas stoves?

A: That’s actually not a federal issue, it’s a state issue. California has already banned gas pipes for all new construction. It looks like New York will follow and that’s one-third of the US population. The goal is to replace them with electrical appliances which emit no carbon. I have a non-carbon house myself, I went down that path about 10 years ago, and it seems to be the only way to reduce carbon emissions—is to either price gasoline or oil out of the market, or to make it illegal, and they’re already making gasoline cars illegal, so gas and oil won’t be far behind. From 1900, we went from a hay powered economy to a gasoline-powered one in only 20 years so it should be doable.

Q: How can the push for all electric work well when we have so many shutdowns, much higher electricity cost, and cannot keep up with the demand already here?

A: Buy lots of copper for new local electric powerlines at the house level and buy lots of aluminum for the long-distance transmission lines. Global demand for both aluminum and copper has to triple to accommodate the grid buildout that is already planned. As far as hurricanes in Florida, there’s nothing you can do to stop those on a hundred-year view; I would move to higher ground, which is hard to do in Florida as the highest point in the state is only 345 feet and that’s a garbage dump.

Q: Can I get a copy of all these slides?

A: Yes, we post the PowerPoint on the website at www.madhedgefundtrader.com usually two hours after the production.

Q: Are you recommending buying precious metals right now (GLD), (GDX), (SLV), (and WPM) even after the upside breakout?

A: On upside breakouts, you buy the dips. A perfect dip would be a retest of the 200-day moving average. But we may not get that, since it seems to be everyone’s number-one choice right now. By the way, I haven’t been telling people to buy gold and LEAPS on all the gold plays since October—that’s where the big move has already been made.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It was so easy during the 10-year technology bull market after the Great Finance Crisis (GFC).

Investors just needed to buy and go take a nap.

Not anymore.

Around November 2021 was when the tech momentum came to a screeching halt with most tech shares reversing on a dime.

Many tech stocks sit today far from their peak.

Now more than ever, active stock management will be critical to overperforming in a world where index funds are effectively dead.

Yet there is still a large risk that we need to calculate in the tech world and that is regulation.

Just in the last week or two, two of techs biggest stalwarts have been hit with turbulence from the powerful regulators.

In a world where more government from every Western country has means higher costs and more bureaucracy, even more government rules appear to be coming our way.

Microsoft, once synonymous with large antitrust cases, is being scrutinized for its execution of monopoly powers.

The US Federal Trade Commission (FTC) announced it will sue to block Microsoft’s $69 billion takeover of Activision, the video game publisher responsible for titles such as Call of Duty, World of Warcraft, Overwatch, and the mobile game Candy Crush.

If approved, the deal would enable Microsoft to corner the video game market and force all game titles on its in-house console called Xbox.

It’s likely that this is just the beginning of anti-trust issue for many strong American tech companies.

The Democrats retook the Senate, meaning that American consumers are satisfied with the status quo, actively voted for high inflationary policies and want more government in American lives.

The populace’s stamp of approval with accelerated price rises for many of our cherished tech software and services means more profits for tech companies.

Luckily for these tech companies, software such as Microsoft Office or Google’s Gmail is monopoly, and any cost explosion will be passed along to the end consumer.

Can you imagine a world where an annual Microsoft Office subscription is $400 per year?

Of course this won’t happen in one day, but I can ensure everyone that Silicon Valley giants with monopolistic products won’t reduce profit just because they feel like it.

Microsoft’s focus on enterprise software has largely kept it out of the US regulatory tussling in recent years over content moderation and predatory pricing discussions that embroil the other Big Tech companies.

Microsoft was thus able slyly close deal, including the acquisitions of:

video-conferencing software Skype for $8.5 billion in 2011,

multiplayer gaming company Minecraft for $2.5 billion in 2014,

social network LinkedIn for $26 million in 2016,

software platform GitHub for $7.5 billion in 2018, and

the speech recognition company Nuance for $26 billion in 2021.

I do believe this is the beginning of something more insidious, where many tech companies are blocked from vanilla takeovers under the banner of anti-trust or anti-competitiveness.

To some extent, these preventative moves from the US government will stymy US tech companies from expanding through mergers and acquisition.

Therefore, the backup plan is to charge everyone more for the current products they sell now.

What’s worse, the next generation visionary technology has yet to surface that changes the rules of tech and the only hope – metaverse – appears to be a bust.

We have nothing to hang our hat on yet.

Ultimately, we are gearing up for an optimistic 2023 in the technology sector, the government won’t be able to stop revenue growth, but they will be able to stop explosive revenue growth.

The expectations of lower rates next year will finally breathe new life into technology stocks, while the government regulation and antitrust concerns will put a cap on accelerating growth.

After a terrible year in 2022, I will be more than happy to take moderate success over the demolition of 2022.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-09 15:02:092022-12-27 21:37:39The Good and Bad About Tech

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.