(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:04:402021-04-26 10:44:52April 26, 2021

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

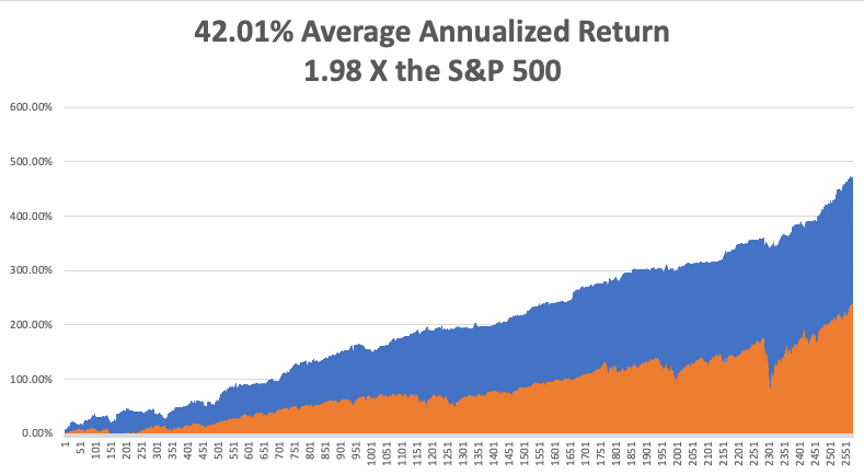

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/g-bebe-e1647874970894.png295450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:02:432021-04-26 10:45:23The Market Outlook for the Week Ahead, or The Correction is Over

Below please find subscribers’ Q&A for the April 14 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: How do you choose your buy areas?

A: It’s very simple; I read the Diary of a Mad Hedge Fund Trader. Beyond that, there are two main themes in the market right now: domestic recovery and tech; and I try to own both of those 50/50. It's impossible to know which one will be active and which one will be dead, and some of that rotation will happen on a day-by-day basis. As for single names, I tend to pick the ones I have been following the longest.

Q: In my 401k, should I continue placing my money in growth or move to something like emerging markets or value?

A: It depends on your age. The younger you are, the more aggressive you should be and the more tech stocks you should own. Because if you’re young, you still have time to earn the money back if you lose it. If you’re old like me, you basically only want to be in value stocks because if you lose all the money or we have a recession, there's not enough time to go earn the money back; you’re in spending mode. That is classic financial advisor advice.

Q: When you say “Buy on dips”, what percentage do you mean? 5% or 10%

A: It depends on the volatility of the stock. For highly volatile stocks, 10% is a piece of cake. Some of the more boring ones with lower volatility you may have to buy after only a 2% correction; a classic example of that is the banks, like JP Morgan (JPM).

Q: Even though you’re not a fan of cryptocurrency, what do you think of Coinbase?

A: It’ll come out vastly overvalued because of the IPO push. Eventually, it may fall to a lower level. And Coinbase isn’t necessarily a business model dependent on bitcoin; it is a business model based on other people believing in bitcoin, and as long as there’s enough of those creating two-way transactions, they will make money. But all of these things these days are coming out super hyped; and you never want to touch an IPO—wait for it to drop 50%, as I once did with Tesla (TSLA).

Q: Please explain the barbell portfolio.

A: The barbell works when you have half tech, half domestic recovery. That way you always have something going up, because the market tends to rotate back and forth between the two sectors. But over the long term everything goes up, and that is exactly what has been happening.

Q: Is the ProShares Ultra Technology Fund (ROM) an ETF?

A: Yes, it is an ETF issuer with $53 billion worth of funds based in Bethesda, MD. (ROM) is a 2x long technology ETF, and their largest holdings include all the biggest tech stocks like Apple (AAPL), Microsoft (MSFT), Facebook (FB), and so on.

Q: Will all this government spending affect the market?

A: Yes, it will make it go up. All we’re waiting to see now is how fast the government can spend the money.

Q: What is the target for ROM?

A: $150 this year, and a lot more on the bull call spread. The only shortcoming of (ROM) is you can only go out six months on the expiration. Even then, you have a good shot at making a 500% return on the farthest out of the money LEAPS, the November $130-$135 vertical bull call spread. That's because market makers just don’t want to take the risk being short technology two years out. It’s just too difficult to hedge.

Q: There have been many comments about hyperinflation around the corner. Will we be seeing hyperinflation?

A: No, the people who have been predicting hyperinflation have been predicting it for at least 20 years, and instead we got deflation, so don’t pay attention to those people. My view is that technology is accelerating so fast, thanks to the pandemic, that we will see either zero inflation or we will see deflation. That has been the pattern for the last 40 years and I like betting on 40-year trends.

Q: When we get called away on our short options, is it easier to close the trade than to exercise your option?

A: No, any action you take in the market costs money, costs commissions, costs dealing spreads. And it's much easier just to exercise the option if you have to cover your short, which is either free or will cost you $15.

Q: Are you worried about overspending?

A: No, the proof in that is we have a 1.53% ten-year US Treasury yield, and $20 trillion in QE and government spending is already known, it’s already baked in the price. So don’t listen to me, listen to Mr. Market; and it says we haven't come close to reaching the limit yet on borrowing. Look at the markets, they're the ones who have the knowledge.

Q: My Walt Disney (DIS) LEAPs are getting killed. I don't understand why my LEAPS go down even on green days for the stock.

A: The answer is that the Volatility Index (VIX) has been going down as well. Remember, if you’re long volatility through LEAPS, and volatility goes down, you take a hit. That said, we’re getting close to the lows of the year for volatility here, so any further stock gains and your LEAPS should really take off. And remember when you buy LEAPS, you’re doing multiple bets; one is that volatility stays high and goes higher, and one is that your stock is high and goes higher. If both those things don’t happen, and you can lose money.

Q: How do you best short the (TLT)?

A: If you can do the futures market, Treasury bonds are always your best short there because you have 10 to 1 leverage.

Q: How would you do a spread on Crisper Technology (CRSP)?

A: We have a recommendation in the Mad Hedge Biotech & Healthcare service to be long the two-year LEAP on Crisper, the $160-$170 vertical bull call spread.

Q: When do you see the largest dip this year?

A: Probably over the summer, but it likely won’t be over 10%. Too much cash in the market, too much government spending, too much QE. People will be in “buy the dips” mode for years.

Q: Is the SPAC mania running out of steam?

A: Yes, you can only get so many SPACS promising to buy the same theme at a discount. I think eventually, 80% of these SPACS go out of business or return the money to investors uninvested because they are promising to buy things at great bargains in one of the most expensive markets in history, which can’t be done.

Q: What do you think about Joe Biden’s attempt to tame the semiconductor chip shortage?

A: Most people don't know that all chips for military weapons systems are already made in the US by chip factories owned by the military. And the pandemic showed that a just-in-time model is high risk because all of a sudden when the planes stop flying, you couldn't get chips from China anymore. Instead, they had to come by ship which takes six weeks, or never. So a lot of companies are moving production back to the US anyway because it is a good risk control measure. And of course, doing that in the midst of the worst semiconductor shortage in history shows the importance of this. Even Tesla has had to delay their semi truck because of chip shortages. Keep buying NVIDIA (NVDA), Micron Technology (MU), Advanced Micro Devices (AMD), and Applied Materials (AMAT) on dips.

Q: Do you see a sell the news type of event for upcoming earnings?

A: Yes, but not by much. We got that in the first quarter, and stocks sold off a little bit after they announced great earnings, and then raced back up to new highs. You could get a repeat of that, as people are just sitting on monster profits these days and you can’t blame them for wanting to pull out a little bit of money to spend on their summer vacation.

Q: Has the stock market gotten complacent about COVID risk?

A: No, I would say COVID is actually disappearing. Some 100 million Americans have been vaccinated, 5 million more a day getting vaccinated, this thing does actually go away by June. So after that, you only have to worry about the anti-vaxxers infecting the rest of the population before they die.

Q: Do you see any imminent foreign policy disasters in Asia, the Middle East, or Europe that could derail the stock market?

A: I don’t, but then you never see these things coming. They always come out of the blue, they're always black swans, and for the last 40 years, they have been buying opportunities. So pray for a geopolitical disaster of some sort, take the 5-10% selloff and buy because at the end of the day, American stockholders really don't care what’s going on in the rest of the world. They do care, however, about increasing their positions in long-term bull markets. I don't worry about politics at all; I don’t say that lightly because it’s taking 50 years of my own geopolitical experience and throwing it down the toilet because nobody cares.

Q: Would you buy Coinbase?

A: Absolutely not, not even with your money. These things always come out overpriced. If you do want to get in, wait for the 50% selloff first.

Q: Is Canada a play on the dollar?

A: Absolutely yes. If they get a weaker dollar, it increases Canadian pricing power and is good for their economy. Canada is also a great commodities play.

Q: The IRS is using Palantir (PLTR) software to find US citizens avoiding taxes with Bitcoin.

A: Yes, absolutely they are. Anybody who thinks this is tax-free money is delusional. And this is one reason to buy Palantir; they’re involved in all sorts of these government black ops type things and we have a very strong buy recommendation on Palantir and their 2-year LEAPS.

Q: Are NFTs, or Non-Fundable Tokens, another Ponzi scheme?

A: Absolutely, if you want to pay millions of dollars for Paris Hilton’s music collection, go ahead; I'd rather buy more Tesla.

Q: When do you think you can go to Guadalcanal again?

A: Well, I’m kind of thinking next winter. Guadalcanal is one of the only places you can go and get more diseases than you can here in the US. Last year, I went there and picked up a bunch of dog tags from marines who died in the 1942 battle there, sent them back to Washington DC, and had them traced and returned to the families. And I happen to know where there are literally hundreds of more dog tags I can do this with. It’s not an easy place to visit and it’s very far away though. Watch out for malaria. My dad got it there.

Q: Walt Disney is already above the pre-pandemic price. Do you suggest any other hotel company name at this time?

A: Go with the Las Vegas casinos, Wynn (WYNN) and MGM (MGM) would be really good ones. Las Vegas is absolutely exploding right now, and we haven't seen that yet in the earnings yet, so buy Las Vegas for sure.

Q: Is the upcoming Roaring Twenties priced into the stock market already?

A: Absolutely not. You didn't want to sell the last Roaring Twenties in 1921 as it still had another eight years to go. You could easily have eight years on this bull market as well. We have historic amounts of money set up to spend, but none of it has been actually spent yet. That didn’t exist in 1921. I think that when they do start hitting the economy with that money, that we get multiple legs up in stock prices.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Beach-e1416856744606.png400276Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-16 09:02:052021-04-16 16:13:56April 14 Biweekly Strategy Webinar Q&A

I have prudently ignored investing in tech stocks for the past seven months, and justly so.

Tech has been peddling hard on the business front, but the shares have been going nowhere in a hurry. Many of the leading names are down 30%-50% from their peak prices.

As a result, they are rapidly approaching value territory. When growth becomes cheap and value gets expensive, it’s time to shift from one side of the barbell strategy to the other.

I’m not saying that tech stocks have bottomed. But we are getting close, perhaps within 10% in the best names. It’s now time to lists of stocks to pounce on when the big turn inevitably comes.

Fortunately, Arthur Henry’s Mad Hedge Technology Letter has already done that job for you. See below his list of recommendations.

By the way, if you want to subscribe to Arthur’s groundbreaking, cutting-edge service, please click here.

It’s the best read on technology investing in the entire market.

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

Here are the names of five of the best stocks to slip into your portfolio in no particular order when the next downside whoosh occurs.

Remember, tech ALWAYS comes back.

Apple

Steve Job’s creation is weathering the gale-fore storm quite well. Apple has been on a tear reconfirming its smooth pivot to software services tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has their supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and will gobble up a total of $200 billion in shares by the end of 2021. Get into this stock while you can as entry points are few and far between.

Oh, and their 5G phones are selling like hotcakes. Some one billion need to be replaced to bring consumers into the new high-speed 5G world.

Amazon (AMZN)

This is the best company in America hands down and commands 5% of total American retail sales or 49% of American e-commerce sales. The pandemic has vastly accelerated the growth of their business.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then oozing innovation and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2021 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter and that is a good thing.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon-effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox-related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business.

Microsoft Azure grew 87% YOY last quarter. The previous quarter saw Azure rocket by 98%. Shares are cheaper than Amazon and almost as potent.

Square (SQ)

CEO Jack Dorsey is doing everything right at this fin-tech company blazing a trail right to the doorsteps of the traditional banks.

The various businesses they have on offer make me think of Amazon’s portfolio because of the supreme diversity. The Cash App is a peer-to-peer money transfer program that cohabits with a bitcoin investing function on the same smartphone app.

Square has targeted the smaller businesses first and is a godsend for these entrepreneurs who lack immense capital to create a financial and payment infrastructure. Not only do they provide the physical payment systems for restaurant chains, but they also offer payroll services and other small loans.

The pipeline of innovation is strong with upper management mentioning they are considering stock trading products and other bank-like products. Wall Street bigwigs must be shaking in their boots.

Roku (ROKU)

Benefitting from the broad-based migration from cable tv to online steaming and cord-cutting, Roku is perfectly placed to delectably harvest the spoils.

This uber-growth company offers an over-the-top (OTT) streaming platform along with the necessary hardware and picks up revenue by selling digital ads.

Founder and CEO Anthony Woods owns 21 million shares of his brainchild and insistently notes that he has no interest in selling his company to a Netflix or Apple.

Viewers are reaffirming the obsession with on-demand online streaming content with hours streamed on the platform increasing 58% to 5.5 billion.

The Roku platform can be bought for just $30 and is easy to set-up. Roku enjoys the lead in the over-the-top (OTT) streaming device industry controlling 37% of the market share leading Amazon’s Fire Stick at 28%.

The runway is long as (OTT) boxes nestle cozily in only 40% of American homes with broadband, up from a paltry 6% in 2010.

They are consistently absent from the backbiting and jawboning the FANGs consistently find themselves in partly because they do not create original content and they are not an offshoot from a larger parent tech firm.

This growth stock experiences the same type of volatility as Square.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/02/John-thomas-air-niugini.png410525Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-24 11:02:022021-03-24 11:35:56Five Tech Stocks to Buy at the Market Bottom

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHAT’S UP WITH TECH?),

(MSFT), (TSLA), (AAPL), (QQQ), (NVDA), (MU), (AMD), (BRKB), (ARRK), (ROM), (VIX), (FCX), (TLT), (BRKB), (TSLA), (JPM), (SPY), (QQQ), (SPX)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-08 11:04:072021-03-08 11:21:08March 8, 2021

That great wellspring of personal wealth, technology stocks, has suddenly run dry.

The leading stock market sector for the past decade took some major hits last week. More stable stocks like Microsoft (MSFT) only shed 8%. Some of the highest beta stocks, like Tesla (TSLA), took a heart-palpitating 39% haircut in a mere two months.

Have tech stocks had it for good? Has the greatest investment miracle of all times ground to a halt? Is it time to panic and sell everything?

Fortunately, I have seen this happen many times before.

Technology is a sector that is prone to extremes. Most of the time it is a hero, but occasionally it is a goat. When too many short-term traders sit in one end of the canoe, we all end up in the drink.

This is one of those times.

Technology stocks undeniably need a periodic shaking out. You need to get rid of the day traders, the hot money, the excessively leveraged, and find out who has been swimming without a swimsuit. The sector rotates between being ridiculously cheap to wildly overvalued. We are currently suffering the latter.

During the past 12 years, Apple’s (AAPL) price earnings multiple has traded from 9X to 36X. It was a value play for the longest time, all the way up to 2016. Nobody believed in it. It is currently at a 33X multiple. While the stock has gone nowhere since August, its earnings have increased by more than 10%, and better is yet to come.

After trading tech stocks for more than 50 years, I can tell you one thing with certainty.

They always come back.

And this time, they are in position to come back sooner, faster, and bigger than ever before. Remember the Great Dotcom Bust of 2000-2003? It lasted two years and nine months and saw NASDAQ (QQQ) crater by 82%, from 5,000 to 1,000. This time, it’s only dropped by 13%, by 1,850 from 14,250 to 12,400.

I don’t see the selloff lasting much longer or lower, no more than another 5%-10% until September. For these are not your father’s technology stocks.

There are only three numbers you need to know. Technology now accounts for a mere 2% of the US workforce, but a massive 27% of stock market capitalization and 37% of total us company earnings. A sector with such an impressive earnings output won’t fall for very long, or very far.

The pandemic accelerated technological innovation tenfold. Companies now have mountains of cash with which to bring forward their futures.

This is no more true than for biotech stocks. The technologies used to create Covid-19 vaccines can be applied to cure all human diseases. And they now have mountains of cash to implement this.

So, I’ll be taking my time with tech stocks. But they are setting up the best long side entry point since the March 20, 2020 pandemic low.

The biggest call remaining for 2021 is when to take profits and sell domestic recovery value stocks and rotate back into tech. But if you are running the barbell strategy I have been harping about since the presidential election, the work is already being done for you. Nonfarm Payroll comes in at a blockbuster 379,000 in February, far better than expected. It a preview of explosive numbers to comes as the US economy crawls out of the pandemic. That’s with a huge drag from terrible winter weather. The headline Unemployment rate is 6.2%. The U-6 “discouraged worker” rate is still a sky-high 11%, those who have been jobless more than six months. Leisure & Hospitality were up an incredible 355,000 and Retail was up 41,000. Government lost 86,000 jobs. We are still 12 million jobs short of the year-ago trend. See what employers are willing to do when they see $20 trillion about to hit the economy?

Will US GDP Growth hit 10% this year? That is the sky-high number that is being mooted by the Atlanta Fed for the first three months of 2021. The vaccine is working! They do tend to be high in the home of Gone with the Wind. This Yankee would be happy at 7.5% growth. Manufacturing just hit a three-year high as companies try to front-run imminent explosive growth. The only weak spot is employment, which is still at recessionary highs.

Herd Immunity is here or says the latest numbers from Johns Hopkins University. New cases have plunged from 250,000 to 46,000 in a month, the fastest disease rollback in human history. We may be seeing new science at work here, where mass vaccinations combine with mass infections to obliterate the pandemic practically overnight. If true, the Dow has another 8,000 points in it….this year. Buy everything on dips. The economic data is about to get superheated.

Warren Buffet’s Berkshire Hathaway blows it away, buying back a staggering $25 billion worth of his own stock in 2020, including $9 billion in the most recent quarter. It’s what I’m always looking for, buying quality at a discount. Warren pulled in $5 billion in profits during the last quarter of 2020, up 13.6% over a year earlier. Net earnings were up 23%. If Buffet, a long time Mad Hedge reader, is buying his stock, you should too. Buy (BRKB) on dips. It's also a great LEAP candidate as the best domestic recovery play out there. Rising rates have yet to hurt Real Estate, as the structural shortage of housing is so severe. Historically speaking, interest rates are still very low, even though the ten-year yield has soared by 82% in two months. Cash is still pouring into REITs coming off the bottom. Home prices always see their fastest moves up at the beginning of a new rate cycle as everyone rushes to beat unaffordable mortgages. The Chip Shortage worsens, with Tesla shutting down its Fremont factory for two days. The Texas deep freeze made matters much worse, where many US fabs are located, like Samsung, NXP Semiconductors, and Infineon Technologies. Buy (NVDA), (MU), and (AMD) on dips.

Jay Powell lays an egg at a Wall Street Journal conference. He said it would take some time to return to a normal economy. The speed of the interest rate rise was “notable.” We are unlikely to return to maximum employment in a year. We couldn’t have heard of more dovish speech. But all that traders heard was that inflation was set to return, but will be “temporary.” That was worth a 600-point dive in the stock market and a 5-basis point pop in bond yields. My 10% correction is finally here! Here today, gone tomorrow. Cathie Wood was far and away the best fund manager of 2020. She, value investor Ron Baron, and I, were alone in the darkness four years ago saying that Tesla (TSLA) could rise 100-fold. Cathie’s flagship fund The Ark Innovation ETF (ARKK) rose a staggering 433% off the March 2020 bottom. Alas, it has since given up a gut-punching 30% since the February high, exactly when ten-year US Treasury bonds started to crash. Watch (ARKK) carefully. This is the one you want to own when rates stabilize. It’s like another (ROM). When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

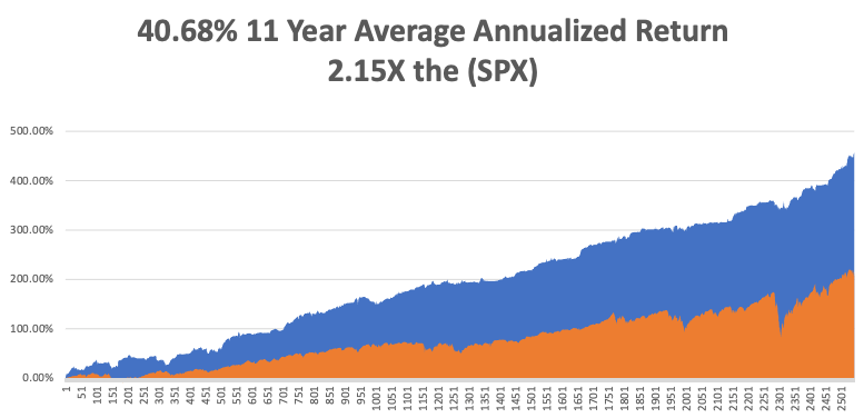

It’s amazing how well selling tops and buying bottoms can help your performance. My Mad Hedge Global Trading Dispatch reached a super-hot 11.61% during the first five days in March on the heels of a spectacular 13.28% profit in February. The Dow Average is up a miniscule 4.00% so far in 2021.

It was a week of frenetic trading, with the Volatility Index (VIX) all over the map. I took profits in Freeport McMoRan (FCX) and my short in US Treasury bonds (TLT) and buying Berkshire Hathaway (BRKB), Tesla (TSLA), JP Morgan (JPM). I opened new shorts in the S&P 500 (SPY) and the NASDAQ (QQQ).

This is my fifth double digit month in a row. My 2021 year-to-date performance soared to 35.10%. That brings my 11-year total return to 457.65%, some 2.12 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.68%.

My trailing one-year return exploded to 110.25%, the highest in the 13-year history of the Mad Hedge Fund Trader.

We need to keep an eye on the number of US Coronavirus cases at 29 million and deaths topping 525,000, which you can find here.

The coming week will be a boring one on the data front.

On Monday, March 8, at 11:00 AM EST, Consumer Inflation Expectations for February are out.

On Tuesday, March 9, at 7:00 AM, The NFIB Business Optimism Index for February is published. On Wednesday, March 10 at 8:30 AM, the US Inflation Rate for February is printed. On Thursday, March 11 at 8:30 AM, Weekly Jobless Claims are out. On Friday, March 12 at 8:30 AM, the Producer Price Index for February is disclosed.

At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, it was with great sadness that I learned of the passing of my old friend, Sheikh Zaki Yamani, the great Saudi Oil Minister. Yamani was a true genius, a self-taught attorney, and one of the most brilliant men of his generation.

It was Yamani who triggered the first oil crisis in 1973, raising the price from $3 to $12 a barrel in a matter of weeks. Until then, cheap Saudi oil had been powering the global economy for decades.

During the crisis, I relentlessly pestered the Saudi embassy in London for an interview for The Economist magazine. Then, out of the blue, I received a call and was told to report to a nearby Royal Air Force base….and to bring my passport.

There on the tarmac was a brand-new Boeing 747 with “Kingdom of Saudi Arabia” emblazoned on the side in bold green lettering. Yamani was the sole passenger, and I was the other. He then gave me an interview that lasted the entire seven-hour flight to Riyadh. We covered every conceivable economic, business, and political subject. It led to me capturing one of the blockbuster scoops of the decade for The Economist.

When Yamani debarked from the plane, I asked him “why me.” He said he saw a lot of me in himself and wanted to give me a good push along my career. The plane then turned around and flew me back to London. I was the only passenger on the plane.

When the pilot heard I’d recently been flying Pilatus Porters for Air America, he even let me fly it for a few minutes while he slept on the cockpit floor.

Yamani later became the head of OPEC. At one point, he was kidnapped by Carlos the Jackal and held for ransom, which the king readily paid.

And if you wonder where I acquired my deep knowledge of the oil and energy markets, this is where it started. Today, the Saudis are among the biggest investors in alternative energy in California.

We stayed in touch ever since.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-on-a-camel.png454470Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-08 11:02:032021-03-08 13:21:48The Market Outlook for the Week Ahead, or What’s Up with Tech?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.