Global Market Comments

August 21, 2025

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO)

Global Market Comments

August 21, 2025

Fiat Lux

Featured Trade:

(MY NEWLY UPDATED LONG-TERM PORTFOLIO)

Global Market Comments

August 19, 2025

Fiat Lux

Featured Trade:

(LAST CHANCE TO ATTEND THE FRIDAY, AUGUST 22, INCLINE VILLAGE, NEVADA STRATEGY DINNER)

(THE MAD HEDGE DICTIONARY OF TRADING SLANG)

Global Market Comments

August 18, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or CLUELESS),

(NVDA), (MSFT), (BAC), (DHI), (LEN), (KBH), (PHM), (GLD), (B),

(NEM), (AEM), (NFLX), (FCX), (TSLA), (SPY), ($VIX), (CATL)

Global Market Comments

August 11, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HOW TOOK COOK PLUCKED APPLE OUT OF THE FIRE BACK INTO THE FRYING PAN),

(SPY), (NVDA), (AAPL), (PANW), (CYBR), (META),

(MSFT), (TSLA), (FCX),(NFLX), (GLD), (DGE), (PERP)

Global Market Comments

August 4, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or REALITY STRIKES)

(TLT), (CCJ), (DHI), (LEN), (KBH), (RKT), (TSLA), (NFLX),

(FCX), (B), (NEM), (AMZN), (AAPL), (BA), (PANW), (V)

Global Market Comments

July 18, 2025

Fiat Lux

Featured Trade:

(JULY 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(GLD), (SLV), (DHI), (LEN), (CCI), (KRE), (META), (NFLX), (AMZN), (SLB), (PPL), (XOM), (OXY), (AGQ), (WFC), (DXJ), (FXE)

Mad Hedge Technology Letter

May 5, 2025

Fiat Lux

Featured Trade:

(COST OF DIGITAL CONTENT ON THE RISE)

(NFLX), (DIS)

A torpedo has just hit the world of digital content.

The cost of digital content is about to skyrocket as Washington D.C., plans to levy a 100% tariff on movies produced outside the states.

Actually, this is one of Hollywood’s dirty little secrets and a big way they cut costs by outsourcing film production to Eastern Europe or Southeast Asia.

Budapest, Hungary, has become a major hub for studios to geoarbitrage production, and a massive studio has sprouted up in this part of Europe.

Millions of expenses have been saved by not making movies in the United States, and so much has been outsourced that the administration has created a new tariff to get the movie business back in the United States.

I would not say this is anything like a national security threat, even to the point that I would say that Hollywood is more or less socially irrelevant in 2025.

However, corporate entertainment content still moves the needle even if people don’t watch it anymore.

It also keeps people employed, and this is a specific attempt to force whoever is making these movies to return to the United States instead of hiring cheaper Hungarians to make our movies.

Imposing a 100% tariff on all films produced abroad that are then sent into the United States will negate most of the cost savings.

A bombshell like this will hurt employment in the industry, causing companies to fire staff much like tech has been doing for the past few years.

Movie and TV production has been exiting Hollywood for years, heading to locations with tax incentives that make filming cheaper.

Governments around the world have increased credits and cash rebates to attract productions and capture a greater share of the $248 billion that will be spent globally in 2025 to produce content.

All major media companies, including Walt Disney (DIS), Netflix (NFLX), and Universal Pictures, film overseas to increase profits.

Film and television production has fallen by nearly 40% over the last decade in Hollywood’s home city of Los Angeles, because of the outrageous cost of doing business in the state of California.

The January wildfires accelerated concerns that producers may look outside Los Angeles, and that camera operators, costume designers, sound technicians, and other behind-the-scenes workers may move out of town rather than try to rebuild in their neighborhoods.

Ultimately, this tariff is devastating to digital content.

This is also on the heels of China limiting Hollywood to only 10 movie imports into China per year.

The city of Los Angeles is about to face a rash of job losses as digital content companies will turn to AI to fill out the rest of the production.

Much less content will be made if these large budget productions of over $20 million cannot be outsourced to cheaper global south employees.

In general, the cost of creating digital content will increase and be painful for the average content maker.

Who does this favor?

Those individual YouTubers who go around filming on a selfie stick while simultaneously editing their own content.

Any digital content company masquerading as a global Titanic will need to shrink accordingly and get leaner.

Americans will need to think twice whether to develop production outside of the United States with this new steep cost.

Companies that will be hurt from this are Netflix, Disney, Amazon, and Comcast.

If these executives don’t pay the tariffs, they could even find themselves locked up in Alcatraz.

Who would have thought that a few days ago?

Global Market Comments

May 5, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or EXPENSIVE AGAIN),

(SPY), (TSLA), (MSTR), (NVDA), (NFLX), (SPY), (GLD)

We certainly are having to work hard for our crust of bread in the stock market this year. April brought us the fastest downturn in stocks in 16 years, immediately followed by the sharpest upturn in 21 years.

It's like running for a treadmill heart test, but a sadistic doctor keeps raising the angle of incline.

Still, I was able to deliver the best trading profits since December 2023, up 14.57%. The harder I work, the luckier I get. Buying when everyone else is throwing up on their shoes is certainly a winning strategy, proven yet again.

The truly disappointing thing about this rally is that it has made stocks expensive once again. In valuation terms, we are now back at February’s peak earnings multiple of 22X for the S&P 500, up from 18X a month ago. This is happening because the growth rate of earnings is falling while share prices are rising.

We are now facing record-high share prices in an economy going into a recession, DOGE cutting chunks of government spending, with rising unemployment and inflation, and a budget deficit for 2025 that is likely to hit $4-$5 trillion.

It doesn’t sound like a great bargain to me. Maybe that’s why only 26% of investors are currently bullish.

We are in fact now at the top of a $4,800-$5,800 range while also bumping up against a solid ceiling at the 200-day moving average. If this bothers anyone, please raise your hand.

Looking at the grim, almost apocalyptic data that is marching our way, I think we are much more likely to next hit an earnings multiple of 16X than 23X. There are a lot of great shorts out there right now, but being up 28.45% so far this year, I am being very cautious when to pull the trigger.

One of the countless fascinating experiences in my life was spending a summer living with a Nazi family in West Berlin in 1968. There was a huge housing shortage in Berlin at the time, and I had to take what I could get. Besides, the apple strudel for dessert was fantastic.

And even though WWII had been over for 23 years, they never shed their extremist political beliefs. Over many dinner discussions I was exposed to the full Nazi philosophy. However, they loved Americans, as it were, they who saved them from the Bolsheviks in 1945.

You know, whenever you get a shot, the nurse always squeezes a little bit of the liquid out of the needle first before sticking it into your arm? This is to prevent an air bubble from getting into your heart, creating an airlock, and stopping it dead. One of the many torments the German Gestapo used to inflict on prisoners was to inject them with air bubbles. Then it was just a matter of minutes before the prisoner died or had a stroke.

I mention all of this because the US economy has just been injected with a big air bubble. If you’re looking for a recession, you can see it with a good set of binoculars off the California coast.

I’m watching the movement of this air bubble on a daily basis.

First, there were the prices for an eastbound 40-foot container shipped from China to the US, down from $8,000 to as low as $1,500 each. About 60 very large container ships carrying 1.2 million containers have gone missing.

Then there is congestion at the Port of Los Angeles, where 200 ships are stranded offshore, unable to unload. Truck drivers are now getting laid off because importers can’t afford to pay the 145% tariffs and are abandoning them, clogging warehouses. Store shelves will start to go bare from mid-May onward, with discount electronics going first.

Any positive growth we see in Q1 will be the result of a rush of post-election over-ordering to front-run the Trump tariffs. That creates a big air bubble in the system for Q2 and onward, maybe for years, even if the trade war ends tomorrow. That’s because shutting down and then restarting a massively complex international trade network takes at least a year.

It certainly was a confusing week for economic data. We saw a succession of very weak employment reports from the ADP Private Employment Report, JOLTS Jobs Openings, and Weekly Jobless Claims, which one might expect from trade war-induced economic collapse. Then, out of the blue, we got a somewhat respectable April Nonfarm Payroll Report at 177,000. Something in these disparate things does not compute.

We haplessly slogging away in the economic forecasting industry are constantly thwarted by constantly conflicting data. You’re probably all sick of hearing the words “on the one hand” and “on the other hand.” But could the unimaginable be happening? One thing I know for sure. You are definitely not going to see strong employment figures for health care (51,000) and Transportation and Warehousing (29,000) in May that we saw in April, once the trade war really starts to bite.

It’s not just the jobs figures that are going haywire. You can count on ALL economic data to be disrupted for at least the next year as the trade war unfolds, retreats, and does whatever it is going to do. It all makes my job so much harder. But then, I always love a challenge.

You may have noticed that I have started making a lot of money from Bitcoin plays like MicroStrategy (MSTR). This is not because I have suddenly become a died in the wool crypto acolyte, a mindless true believer, a guzzler of the Kool-Aid at every opportunity. I firmly believe that Bitcoin has another 95% decline ahead of it sometime in the future and that it is nothing more than a Ponzi scheme.

As I watch the many crypto “experts” wax lyrical about their $1 million upside targets, I can’t help but notice that most aren’t even old enough to be my grandchildren. The president has recently pardoned several crypto robber barons convicted of looting customer accounts of billions of dollars. Another term for “anti-regulation” is “pro-stealing.” The SEC has morphed from securities regulation to crypto promotion.

Nevertheless, I DO know what a chart is, downside support and upside resistance, and above all, euphoria and momentum. All of these started screaming “BUY” at me three weeks ago, and I started picking up crypto play with both, and if not three. I merely did what Mr. Market was begging me to notice.

Yes, sometimes even I have to trade charts for a living. But it is definitely a position I am only dating, not marrying. I’ll only be in crypto as long as there are more buyers than sellers and the suckers keep being born. I have a feeling that, at the end of the day, all crypto has really done is to pay for some very expensive parties in Miami and Dubai.

As far as I’m concerned, I’m hoping for the stroke and not the heart attack.

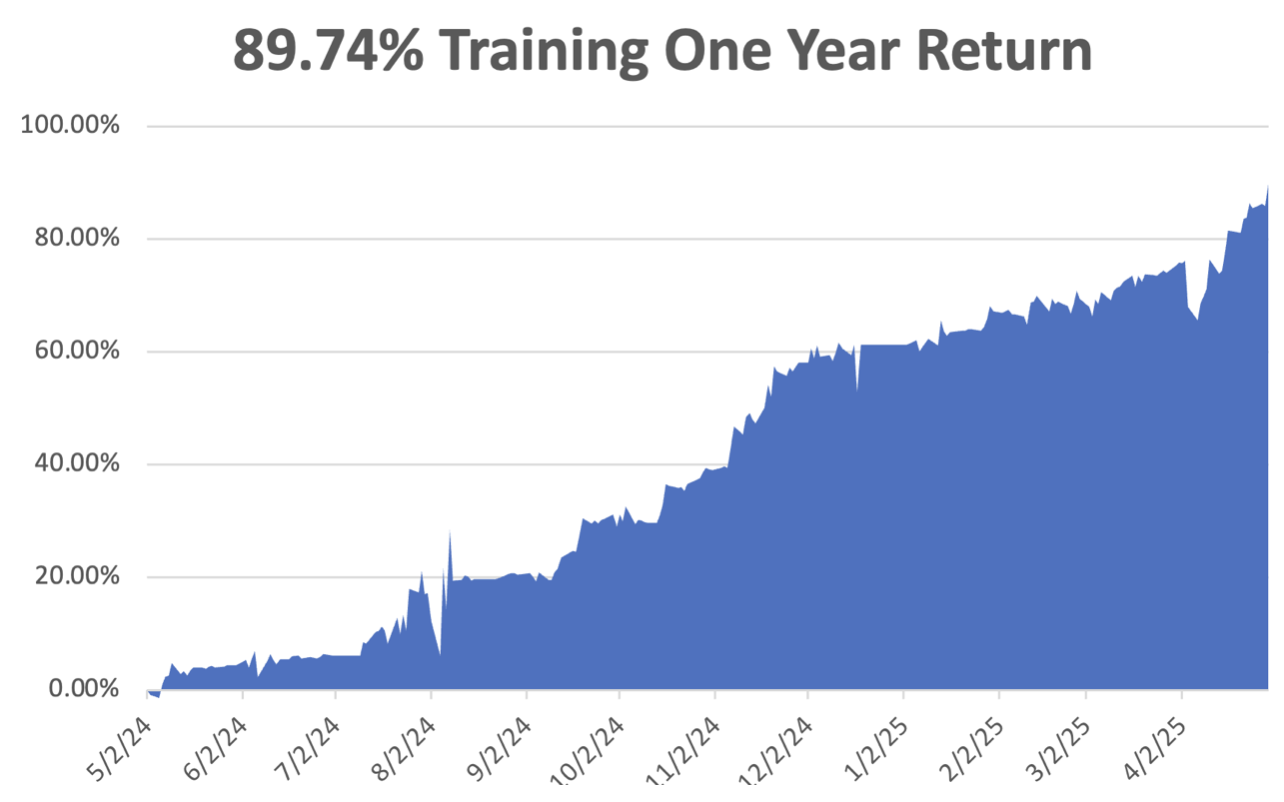

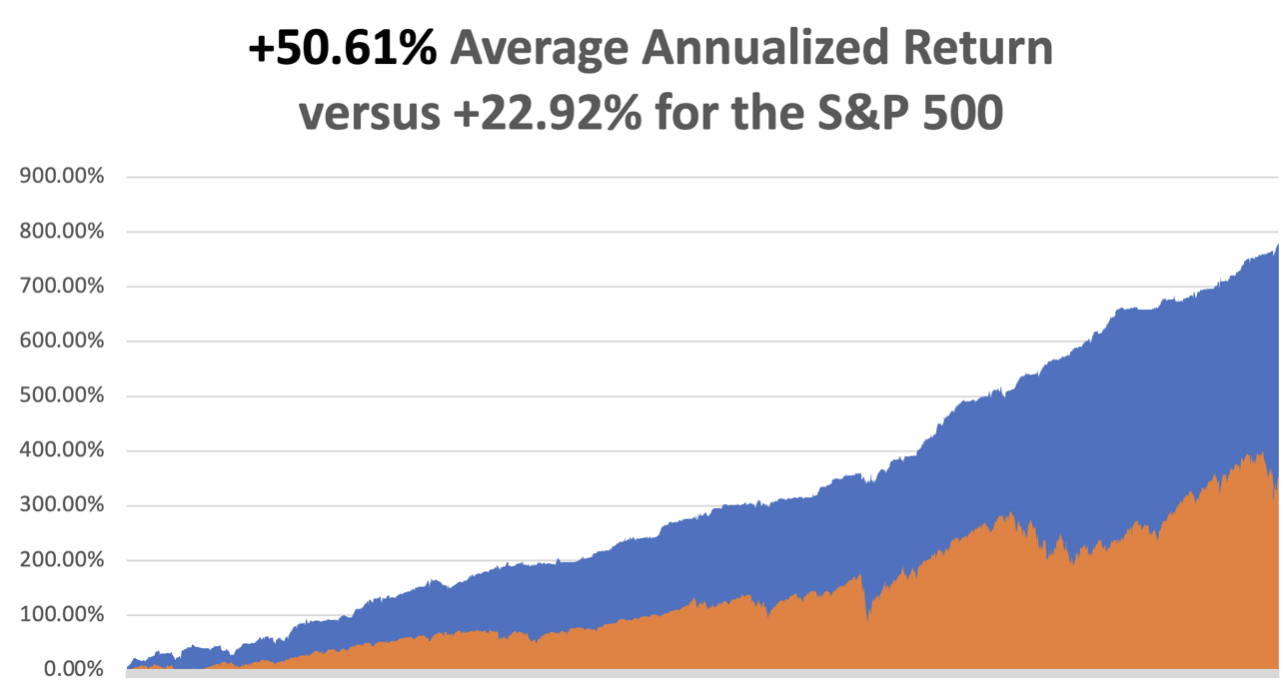

My April performance closed out at a spectacular +14.57%. That takes us to a year-to-date profit of +28.40% so far in 2025. My trailing one-year return stands at a spectacular +89.79%. That takes my average annualized return to +50.61% and my performance since inception to +780.29%, a new all-time high.

It has been another wild week in the market, with the stock market up every day. I used a brief $25 dip in (TSLA) to take profits in my short play there. That leaves me 40% long, with a double position in (MSTR), and longs in (NVDA) and (NFLX). I have 20% short in (SPY) and a “risk off” position in (GLD), and 40% cash. I’m just waiting for this rally to burn out before topping up my shorts, not a bad idea in the wake of the biggest run-up in 21 years.

Some 63 of my 70 round trips in 2023, or 90%, were profitable. Some 74 of 94 trades

were profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

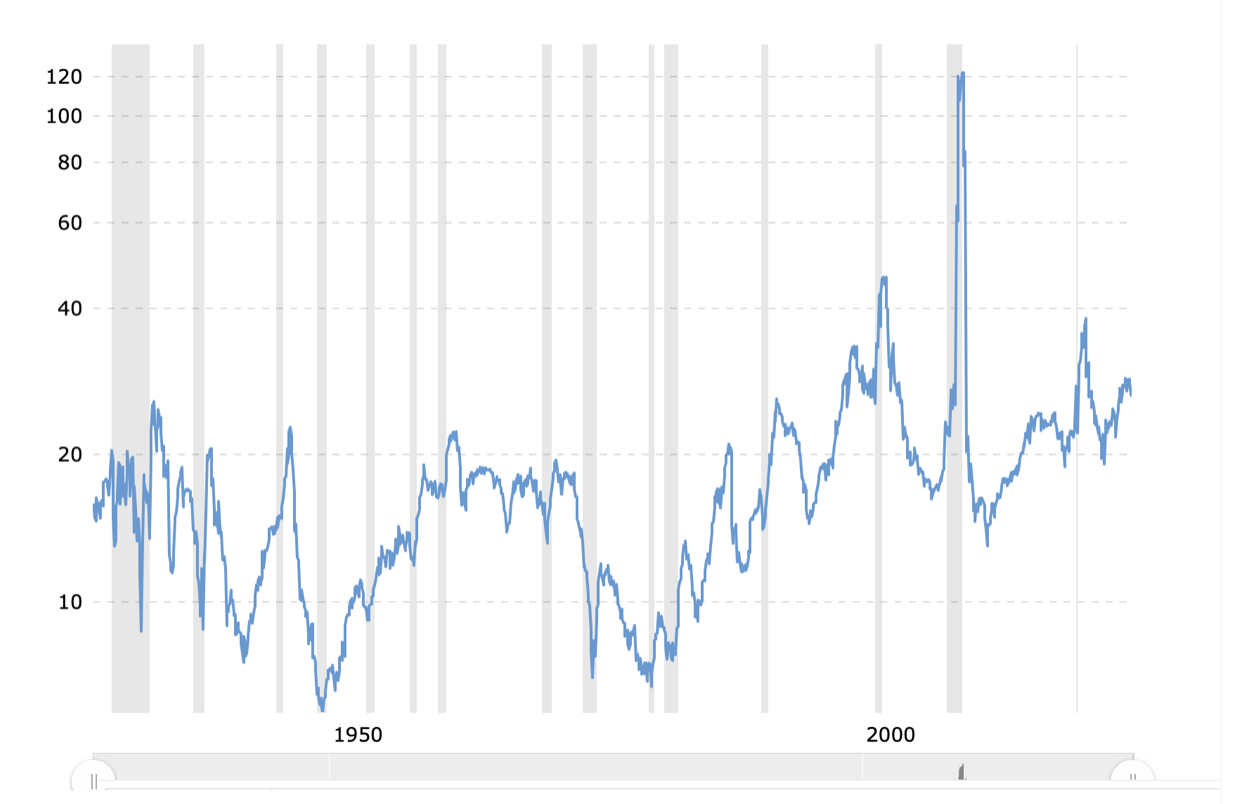

100 Years of S&P 500 Earnings Multiples

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, May 5, at 8:30 AM EST, the S&P Global Composite PMI is announced.

On Tuesday, May 6, at 3:30 AM, the Balance of Trade is released.

On Wednesday, May 7, at 1:00 PM, the Federal Reserve announces its interest rate decision. No move is expected in the face of a rising inflation rate. A press conference follows at 1:30.

On Thursday, May 8, at 8:30 AM, the Weekly Jobless Claims are disclosed.

On Friday, May 9, at 12:00 PM, the Baker Hughes Rig Count is published.

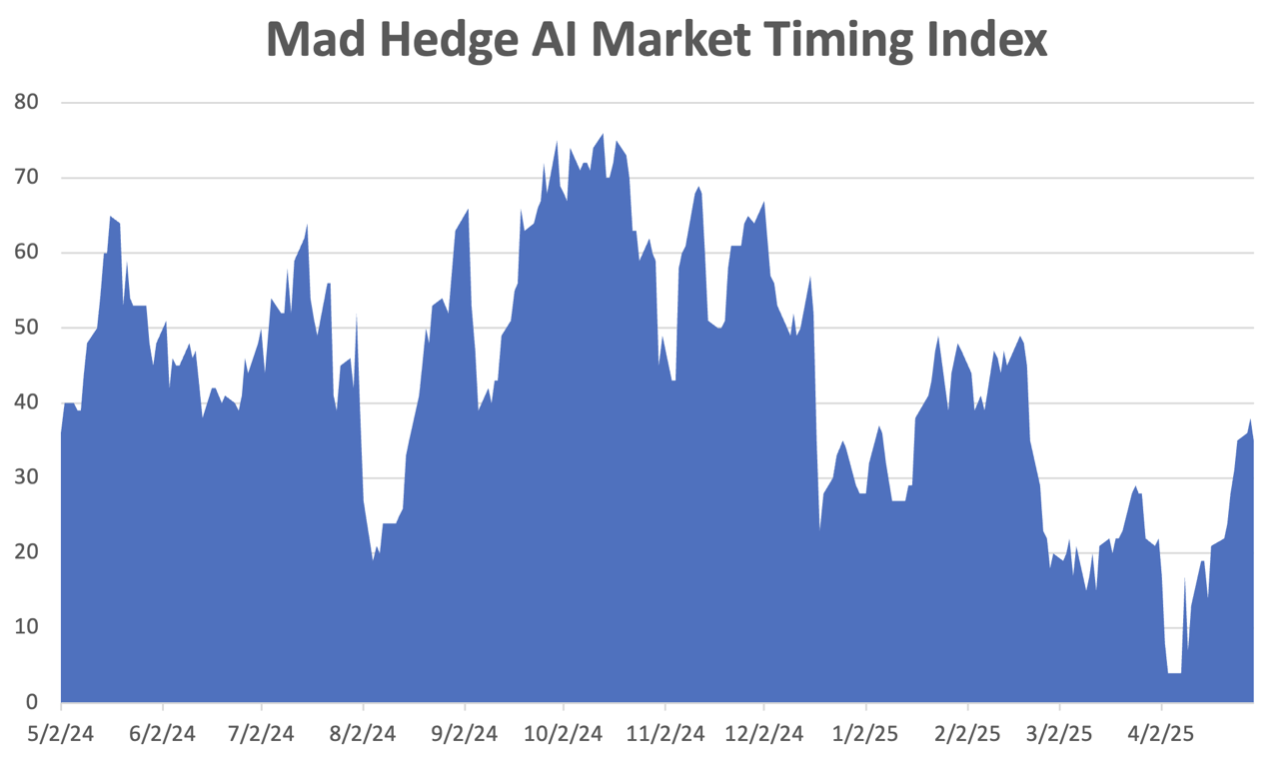

I’m Always Cautious When Pulling the Trigger

Microsoft Goes Ballistic, with the second 10% move in a month. Indications are that AI spending is continuing unabated, taking the entire tech space up with it.

ISM Manufacturing Index Says the Recession is Here. Economic activity in the manufacturing sector contracted in April for the second month in a row, following a two-month expansion preceded by 26 straight months of contraction, say the nation's supply executives in the latest Manufacturing ISM Report On Business®. Manufacturing in high-cost America has been in a structural decline for three years now and is accelerating to the downside.

US Q1 GDP Crashes in Q1, down 0.3%, thanks to the massive front-running of imports to beat the Trump tariffs. This quarter will certainly be worse as almost all international trade has ceased, giving us a second negative quarter that officially constitutes a recession. A three-quarter recession gives us an S&P 500 of 4,500, four quarters, 4,000.

JOLTS Job Openings Report was Weak in March at 7.1 Million, said the U.S. Bureau of Labor Statistics. Over the month, hires held at 5.4 million, and total separations changed little at 5.1 million. Within separations, quits (3.3 million) were unchanged, and layoffs and discharges (1.6 million) edged down.

Consumer Confidence Collapses, hitting a 15-Year Low, according to the Conference Board. The Index fell to 86 on the month, down a hefty 7.9 points from its prior reading and below the Dow Jones estimate for 87.7. The board’s Expectations Index, which measures how respondents look at the next six months, tumbled to 54.4, a decline of 12.5 points and the lowest reading since October 2011.

New Homes are Now Cheaper than Existing Homes, for the first time. A 30% rise in existing inventories has made the difference. New home builders can more easily discount with free upgrades and offer loan buy-downs. Some 40% of homes on the market have seen price drops, and time on the market is growing.

Weekly Jobless Claims Rocket by 18,000. First-time filings for unemployment insurance totaled a seasonally adjusted 241,000 for the week ended April 26, up 18,000 from the prior period and higher than the estimate for 225,000. Continuing claims, which run a week behind and provide a broader view of layoff trends, rose to 1.92 million, up 83,000 to the highest level since Nov. 13, 2021.

General Motors to take $5 Billion Hit on Tariffs. GM on Thursday lowered its 2025 earnings guidance to include a possible $4 billion to $5 billion impact as a result of President Donald Trump’s auto tariffs. GM said its new guidance includes adjusted EBIT of between $10 billion and $12.5 billion, down from $13.7 billion to $15.7 billion. GM released first quarter results Tuesday that beat Wall Street’s expectations but delayed its investor call and updated guidance details amid expected changes to the auto tariffs.

S&P Case-Shiller National Home Price Index Slows to 3.9% YOY, in February, a sharp slowdown. Home prices are increasingly untenable to potential home buyers. Waning consumer confidence, heightened insecurity over economic uncertainties, and the future of household budgets are impacting the consumer housing market. New York (+7.7%), Chicago (+7.0%), and Cleveland (+6.6%) show the biggest gains, while Tampa showed a (-1.4%) loss. Expect real estate to remain a major drag on the US economy, with mortgage rates at 7.0%.

Bitcoin ETF’s Suck in $3.5 Billion Last Week, as the “Sell America” trade expands. Exchange-traded funds tracking Bitcoin and Ether attracted more than $3.2 billion last week, with the iShares Bitcoin Trust ETF (IBIT) alone seeing a nearly $1.5 billion inflow — the most this year.

Crude Oil Drops on Global Recession Fears. Brent crude futures were down $1.09, or 1.63%, at $65.78 a barrel. West Texas Intermediate crude fell $1.15, or 1.82%, to $61.87 a barrel. The U.S.-China trade war is dominating investor sentiment in moving oil prices, superseding nuclear talks between the U.S. and Iran, and discord within the OPEC+ coalition. Markets have been rocked by conflicting signals from the U.S. over what progress was being made to de-escalate a trade war that threatens to sap global growth.

As for me, by the 1980s, my mother was getting on in years. Fluent in Russian, she managed the CIA’s academic journal library from Silicon Valley, putting everything on microfilm.

That meant managing a team that translated over 1,000 monthly publications on topics as obscure as Arctic plankton, deep space phenomena, and advanced mathematics. She often called me to ascertain the value of some of her findings.

But her arthritis was getting to her, and all those trips to Washington, DC were wearing her out. So I offered Mom a job. Write the Thomas family history, no matter how long it took. She worked on it for the rest of her life.

Dad’s side of the family was easy. He was traced to a small village called Monreale above the Sicilian port city of Palermo, famed for its Byzantine church. Employing a local priest, she traced birth and death certificates going all the way back to an orphanage in 1820. It is likely he was a direct illegitimate descendant of Lord Nelson of Trafalgar.

Grandpa fled to the United States when his brother joined the Mafia in 1915. The most interesting thing she learned was that his first job in New York was working for Orville Wright at Wright Aero Engines (click here). That explains my family’s century-long fascination with aviation.

Grandpa became a tail gunner on a biplane in WWI. My dad was a tail gunner on a B-17 flying out of Guadalcanal in WWII. As for me, you’ve all heard plenty of my own flying stories, and there are many more to come.

My Mom’s side of the family was an entirely different story.

Here ancestors first arrived to found Boston, Massachusetts in 1630 during the second Pilgrim wave on a ship called the Pied Cow, steered by Captain Ashley (click here for the link).

I am a direct descendant of two of the Pilgrims executed for witchcraft in the Salem Witch Trials of 1692, Sarah Good and Sarah Osborne, where children’s dreams were accepted as evidence (click here). They were later acquitted.

When the Revolutionary War broke out in 1776, the original Captain John Thomas, whom I am named after, served as George Washington’s quartermaster at Valley Forge, responsible for supplying food to the Continental Army during the winter.

By the time Mom completed her research, she had discovered 17 ancestors who fought in the War for Independence, and she became the West Coast head of the Daughters of the American Revolution. It seems the government still owes us money from that event.

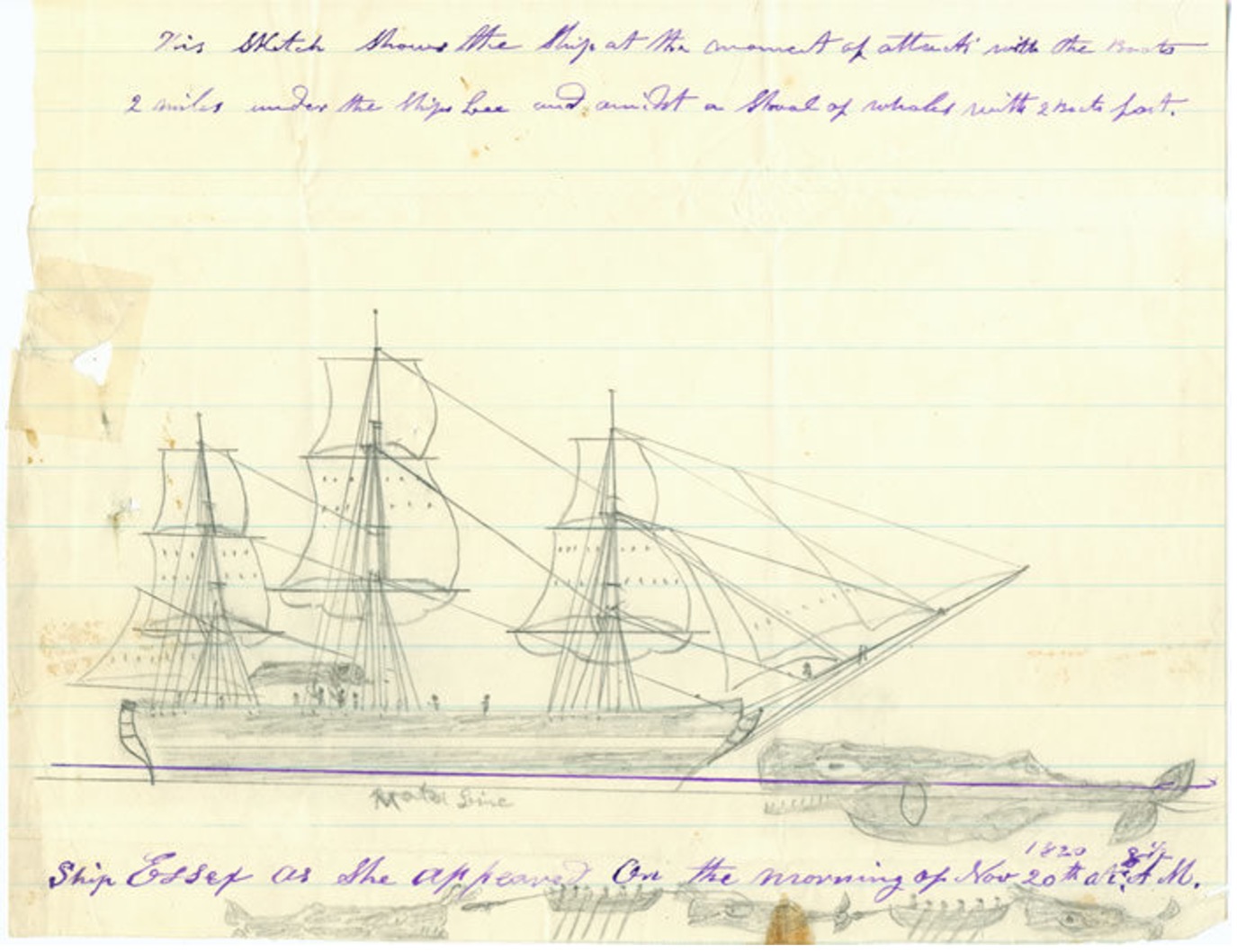

Fast forward to 1820 with the sailing of the whaling ship Essex from Nantucket, Massachusetts, the basis for Herman Melville’s 1851 novel Moby Dick. Our ancestor, a young sailor named Owen Coffin signed on for the two year voyage, and his name “Coffin” appears in Moby Dick seven times.

In the South Pacific, 2,000 miles west of South America, they harpooned a gigantic sperm whale. Enraged, the whale turned around and rammed the ship, sinking it. The men escaped to whale boats. And here is where they made the fatal navigational errors that are taught in many survival courses today.

Captain Pollard could easily have just ridden the westward currents, where they would have ended up in the Marquesas Islands in a few weeks. But these islands were known to be inhabited by cannibals, which the crew greatly feared. They also might have landed in the Pitcairn Islands, where the mutineers from Captain Bligh’s HMS Bounty still lived. So the boats rowed east, exhausting the men.

At day 88, the men were starving and on the edge of death, so they drew lots to see who should live. Owen Coffin drew the black lot and was immediately shot and devoured. The next day, the men were rescued by the HMS Indian within sight of the coast of Chile and returned to Nantucket by the USS Constellation.

Another Thomas ancestor, Lawson Thomas, was on the second whaleboat that was never seen again and presumed lost at sea. For more details about this incredible story, please click here.

When Captain Pollard died in 1870, the neighbors discovered a vast cache of stockpiled food in the attic. He had never recovered from his extended starvation.

Mom eventually traced the family to a French weaver 1,000 years ago. Our name is mentioned in England’s Domesday Book, a listing of all the land ownership in the country published in 1086 (click here for the link). Mom died in 2018 at the age of 88, a very well-educated person.

There are many more stories to tell about my family’s storied past, and I will in future chapters. This week, being Thanksgiving, I thought it appropriate to mention our Pilgrim connection.

I have learned over the years that most Americans have history-making swashbuckling ancestors, but few bother to look.

I did.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

USS Essex